MARKET INSIGHTS

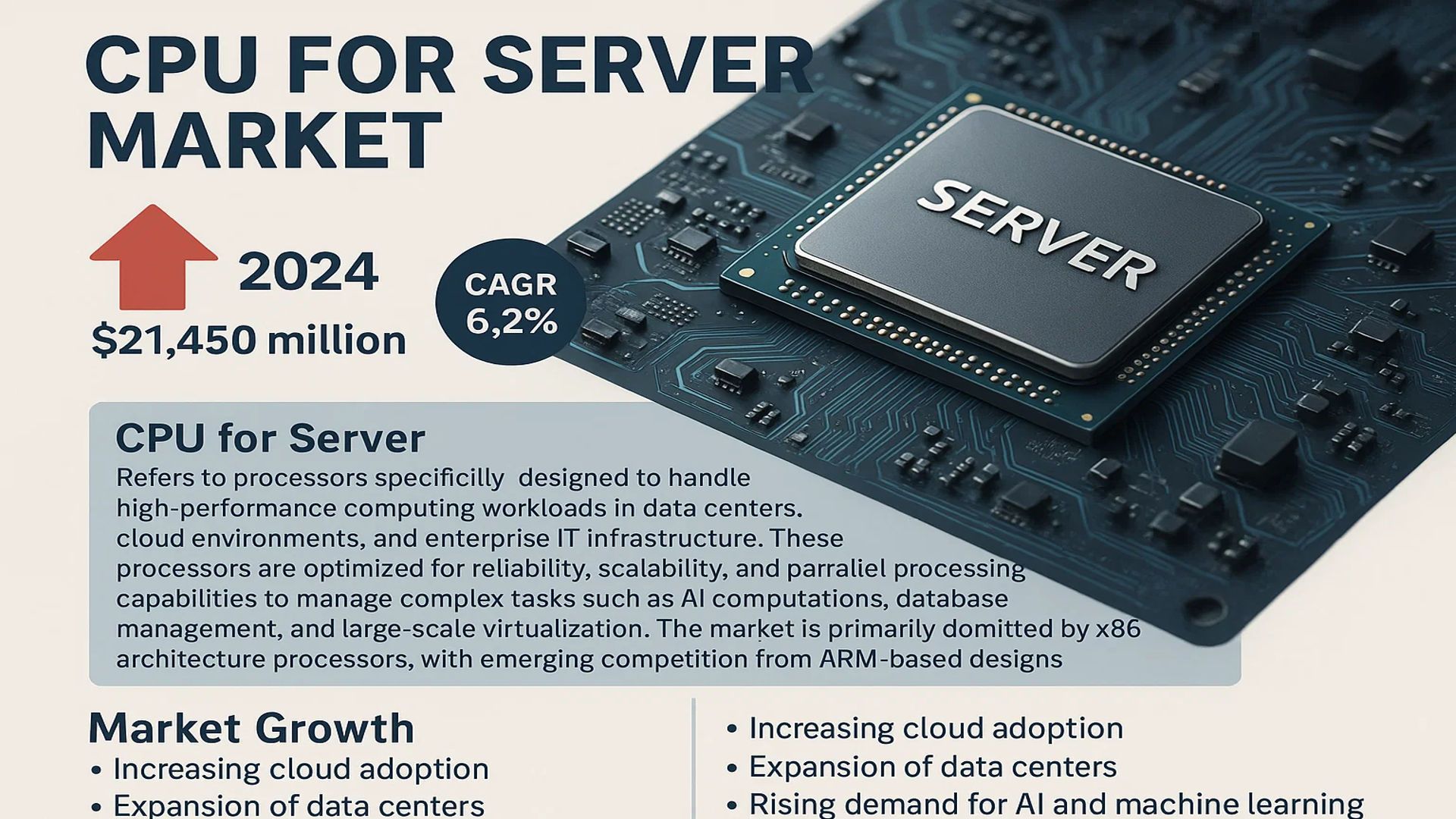

The global CPU for Server Market was valued at 21450 million in 2024 and is projected to reach US$ 33260 million by 2032, at a CAGR of 6.2% during the forecast period.

CPU for Server refers to processors specifically designed to handle high-performance computing workloads in data centers, cloud environments, and enterprise IT infrastructure. These processors are optimized for reliability, scalability, and parallel processing capabilities to manage complex tasks such as AI computations, database management, and large-scale virtualization. The market is primarily dominated by x86 architecture processors, with emerging competition from ARM-based designs.

The market growth is driven by increasing cloud adoption, expansion of data centers, and rising demand for AI and machine learning applications. While Intel maintains market leadership with over 70% share through its Xeon processors, AMD’s EPYC series has gained significant traction with its competitive pricing and performance. Furthermore, the growing adoption of edge computing and 5G networks is creating new opportunities for specialized server processors, particularly in the Asia-Pacific region where digital transformation initiatives are accelerating.

MARKET DYNAMICS

MARKET DRIVERS

Booming Cloud Computing and Data Center Expansion Fuel Server CPU Demand

The global server CPU market is experiencing robust growth driven by unprecedented expansion in cloud computing and data center infrastructure. Cloud service providers are investing billions annually to scale their operations worldwide, with hyperscale data center capacity projected to grow at nearly 20% CAGR through 2030. These facilities require high-performance server processors capable of handling massive parallel workloads efficiently. The shift to hybrid cloud environments and multi-cloud strategies across enterprises further accelerates adoption of advanced server CPUs, particularly those optimized for virtualization and containerized workloads.

AI and Machine Learning Workloads Drive Specialized Processor Adoption

Artificial intelligence adoption across industries is transforming server CPU requirements, with the AI server market expected to triple in value by 2026. Modern AI workloads demand processors with enhanced matrix operation capabilities, larger cache sizes, and superior memory bandwidth. This has led to innovative architectural developments, such as AMD’s incorporation of AI accelerators in their EPYC processors and Intel’s Advanced Matrix Extensions in Xeon Scalable CPUs. The machine learning inference market alone accounts for over 35% of new server processor deployments, illustrating how AI specialization is reshaping the competitive landscape.

5G and Edge Computing Create New Infrastructure Requirements

The global rollout of 5G networks and edge computing infrastructure is generating demand for power-efficient server processors optimized for distributed environments. Edge data centers require CPUs that balance performance with thermal design power (TDP) constraints, favoring ARM-based designs and specialized SoCs. With mobile edge computing investment projected to exceed $15 billion annually by 2025, processor manufacturers are developing new product lines specifically for these low-latency, high-efficiency applications. This represents a significant growth vector beyond traditional data center deployments.

MARKET RESTRAINTS

Supply Chain Disruptions and Semiconductor Shortages Constrain Market Growth

The server CPU market continues to face challenges from global semiconductor supply chain constraints, with lead times for advanced nodes remaining above 30 weeks. Foundry capacity for cutting-edge process technologies is particularly strained, affecting the production of high-end server processors. These bottlenecks have led to allocation systems and prioritization of strategic customers, making it difficult for smaller data center operators to secure inventory. Component shortages affecting complementary technologies like power management ICs further compound production challenges across the server ecosystem.

Rising Power Consumption and Thermal Challenges Limit Performance Scaling

As server CPUs push performance boundaries, power consumption has emerged as a critical constraint, with flagship server processors now exceeding 400W TDP. Data center operators face increasing pressure to balance performance gains with energy efficiency and sustainability goals. The cost of power and cooling now represents over 40% of total data center operating expenses in many regions, forcing careful evaluation of processor choices. This thermal wall is driving architectural innovations but simultaneously slowing raw performance improvements compared to historical Moore’s Law trends.

MARKET CHALLENGES

Heterogeneous Computing Architectures Increase Software Complexity

The rise of specialized server processors for AI, HPC, and edge computing has created significant software compatibility and optimization challenges. Developers now face the burden of optimizing applications for diverse instruction sets and accelerator architectures, from x86 to ARM and custom accelerators. This software fragmentation can reduce the effective performance of cutting-edge processors and increase total cost of ownership through additional development overhead. Industry standardization efforts remain fragmented, with competing ecosystems vying for developer mindshare.

Geopolitical Tensions Impact Global Supply and Technology Access

Trade restrictions and export controls in the semiconductor sector are creating uncertainty for server CPU manufacturers and buyers alike. Restrictions on advanced chip technologies to certain markets have forced regionalization of supply chains, potentially leading to bifurcated product roadmaps. These geopolitical factors introduce additional complexity in long-term infrastructure planning for global enterprises and cloud providers who require consistent worldwide deployment capabilities.

MARKET OPPORTUNITIES

Emerging RISC-V Architecture Presents Disruptive Potential

The open-standard RISC-V instruction set architecture is gaining traction in specialized server applications, offering customization opportunities that proprietary architectures cannot match. Early adopters are leveraging RISC-V for specific workloads like AI inference and security processing, with performance-per-watt advantages in targeted scenarios. The ecosystem is rapidly maturing, with RISC-V server processors expected to capture meaningful market share in edge and hyperscale environments within the next 3-5 years.

Chiplet-Based Designs Enable Flexible Performance Scaling

Advanced packaging technologies and chiplet architectures are revolutionizing server CPU design, allowing manufacturers to mix and match compute, I/O, and accelerator modules. This modular approach enables more responsive product development cycles and targeted performance enhancements. Industry adoption of universal chiplet interconnect standards will further accelerate this trend, potentially reducing development costs by 30-40% while enabling rapid customization for specific workload requirements.

CPU FOR SERVER MARKET TRENDS

Shift Toward Heterogeneous Computing Architectures

The server CPU market is witnessing a transformative shift toward heterogeneous computing architectures, driven by the growing demand for specialized workloads like AI training, cloud computing, and high-performance analytics. Intel and AMD are leading this transition with their hybrid core designs, integrating performance and efficiency cores to optimize power consumption while maintaining computational throughput. The rise of AI-accelerated workloads has further propelled the adoption of server processors with enhanced matrix multiplication capabilities, a trend that accounted for nearly 30% of data center processor upgrades in 2024. Additionally, innovations in advanced node technologies, such as Intel’s Intel 4 process and AMD’s 5nm Zen 4 architecture, are enabling higher transistor density and superior energy efficiency.

Other Trends

Edge Computing Driving Demand for Low-Power CPUs

Edge computing has emerged as a critical growth driver for server CPUs, particularly those designed for low-power yet high-performance applications. Enterprises are increasingly deploying ARM-based server processors from vendors like Ampere Computing and Qualcomm, which offer superior thermal efficiency for decentralized computing environments. Providers delivering cloud-to-edge infrastructure report a 45% increase in demand for power-efficient server processors since 2023, primarily for IoT, industrial automation, and real-time analytics. Furthermore, the global 5G rollout is accelerating edge computing adoption, necessitating server CPUs capable of handling ultra-low-latency workloads at distributed locations.

Accelerated Cloud Adoption Bolsters Server CPU Innovation

The rapid expansion of hyperscale data centers, particularly by cloud service providers like AWS, Microsoft Azure, and Google Cloud, is a major contributor to server CPU market growth. These providers accounted for over 60% of new server processor deployments in 2024, prioritizing scalable and multi-tenant architectures. Leading vendors such as AMD and Intel have responded with EPYC and Xeon processors optimized for virtualization-heavy workloads, with some models supporting up to 128 cores per socket. Meanwhile, cloud-native applications are pushing demand for scalable, multi-threaded processors, with a notable 20% year-over-year increase in high-core-count CPU adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Market Expansion Drive Fierce Competition in Server CPU Sector

The global server CPU market remains highly competitive, dominated by established players while facing disruption from emerging innovators. Intel Corporation continues to lead the market with over 70% share in 2024, leveraging its powerful Xeon processor family that has become the backbone of enterprise data centers worldwide. The company’s deep integration with cloud providers and long-standing ecosystem partnerships reinforce its market dominance.

Advanced Micro Devices (AMD) has emerged as the primary challenger, growing its market share significantly through its EPYC processor lineup. AMD’s focus on high core counts and energy efficiency has resonated particularly well with hyperscale data center operators. The company’s recent innovations in 3D V-Cache technology and chiplet design architecture demonstrate its commitment to pushing performance boundaries in the server CPU space.

Meanwhile, ARM-based competitors are gaining traction, with companies like Ampere Computing and Huawei’s HiSilicon carving out niche positions in cloud-native and edge computing applications. While ARM server CPUs currently represent a smaller portion of the market, their energy efficiency advantages and growing software compatibility are driving increased adoption among certain enterprise segments.

Chinese manufacturers including Phytium Technology and Hygon Information Technology are expanding their domestic market presence through government-supported initiatives, though they remain minor players in the global arena. These companies are focusing on developing localized alternatives to reduce dependence on Western technology, particularly in sensitive sectors.

List of Key Server CPU Companies Profiled

- Intel Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- HiSilicon (Huawei) (China)

- Ampere Computing (U.S.)

- IBM (U.S.)

- Google Axion (U.S.)

- Phytium Technology (China)

- Chengdu Sunway Technologies (China)

- Montage Technology (China)

- Hygon Information Technology (China)

Segment Analysis:

By Type

x86 CPU Segment Dominates the Market Due to Widespread Adoption in Data Centers and Cloud Computing

The market is segmented based on type into:

- x86 CPU

- Subtypes: Intel Xeon, AMD EPYC, and others

- Arm-based CPU

- Subtypes: Huawei Kunpeng, Ampere Computing, AWS Graviton, and others

By Application

AI Server Segment Grows Rapidly Due to Increasing Demand for Machine Learning and Deep Learning Workloads

The market is segmented based on application into:

- AI Server

- General Purpose Server

By Architecture

Multi-Core Processors Gain Traction for High-Performance Computing Applications

The market is segmented based on architecture into:

- Single-Core

- Multi-Core

- Subtypes: Dual-Core, Quad-Core, Hexa-Core, Octa-Core, and others

By End User

Cloud Service Providers Lead Adoption Due to Expansion of Hyperscale Data Centers

The market is segmented based on end user into:

- Cloud Service Providers

- Enterprises

- Government Organizations

- Academic & Research Institutions

Regional Analysis: CPU for Server Market

North America

The North American server CPU market remains the most technologically advanced and mature, with the U.S. accounting for over 85% of regional demand due to strong data center expansion and enterprise digitization initiatives. Major cloud service providers like AWS, Microsoft Azure, and Google Cloud are driving significant adoption of next-generation processors, particularly for AI and high-performance computing workloads. Intel continues to dominate with its Xeon Scalable processors, though AMD has gained notable traction with EPYC chips offering superior price-to-performance ratios. The region is also witnessing early ARM-based server adoption through Amazon’s Graviton processors and Ampere Computing’s offerings.

Europe

European enterprises display growing preference for energy-efficient server processors to comply with strict sustainability regulations, creating opportunities for both x86 and ARM architectures. Germany leads regional demand, followed by the UK and France, with hyperscalers investing heavily in green data centers. While Intel maintains majority share, AMD’s EPYC processors have gained popularity for cloud-native applications. The region shows cautious but growing interest in alternative architectures from Ampere and other ARM-based vendors, particularly for specialized workloads like telecommunications and edge computing.

Asia-Pacific

APAC represents the fastest-growing server CPU market globally, driven by massive digital infrastructure projects and expanding cloud ecosystems in China, Japan, and India. China’s domestic semiconductor policies have boosted adoption of locally-developed ARM processors like Huawei’s Kunpeng and Phytium’s solutions, though x86 remains dominant for enterprise applications. Japan and South Korea show strong preference for leading-edge server processors to support advanced manufacturing and 5G infrastructure. The region’s diverse requirements span from cost-sensitive general-purpose servers to cutting-edge AI accelerators, creating opportunities across all processor segments.

South America

Server CPU adoption in South America shows steady but slower growth, constrained by economic volatility and infrastructure limitations. Brazil accounts for nearly half of regional demand, with financial services and telecom sectors driving most purchases. While Intel processors dominate, there’s growing interest in AMD’s value-oriented EPYC lineup among cost-conscious enterprises. Cloud adoption remains in early stages compared to other regions, delaying widespread deployment of next-generation architectures. However, the region shows long-term potential as digital transformation initiatives gain momentum across key industries.

Middle East & Africa

The MEA server CPU market displays uneven development, with Gulf Cooperation Council countries leading adoption while other regions lag due to infrastructure constraints. UAE and Saudi Arabia are investing heavily in smart city and cloud infrastructure projects, driving demand for high-performance server processors. ARM-based solutions show promise for energy-efficient deployments in harsh climates, though x86 remains standard for most applications. The region presents long-term growth potential as digital transformation accelerates, though adoption patterns will likely follow oil-driven economic cycles in key markets.

Report Scope

This market research report provides a comprehensive analysis of the Global CPU for Server Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global CPU for Server market was valued at USD 21,450 million in 2024 and is projected to reach USD 33,260 million by 2032, growing at a CAGR of 6.2% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (x86 CPU, Arm-based CPU), application (AI Server, General Purpose Server), and end-user industry to identify high-growth segments and investment opportunities. x86 CPU currently dominates with over 70% market share in 2024.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific is the fastest-growing region due to increasing data center investments.

- Competitive Landscape: Profiles of leading market participants including Intel, AMD, HiSilicon, Ampere Computing, and IBM, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments. Intel currently holds over 70% market share with its Xeon processors.

- Technology Trends & Innovation: Assessment of emerging technologies including ARM-based processors, AI-optimized chips, advanced fabrication techniques (5nm and below), and evolving industry standards for data center efficiency.

- Market Drivers & Restraints: Evaluation of factors driving market growth (cloud computing expansion, AI adoption, 5G deployment) along with challenges (supply chain constraints, geopolitical factors, high R&D costs).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the server CPU market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global CPU for Server Market?

-> CPU for Server Market was valued at 21450 million in 2024 and is projected to reach US$ 33260 million by 2032, at a CAGR of 6.2% during the forecast period.

Which key companies operate in Global CPU for Server Market?

-> Key players include Intel, AMD, HiSilicon, Ampere Computing, IBM, Google Axion, Phytium Technology, Chengdu Sunway Technologies, Montage Technology, and Hygon Information Technology.

What are the key growth drivers?

-> Key growth drivers include cloud computing expansion, increasing AI workloads, data center investments, and 5G network deployment.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia-Pacific is the fastest-growing region.

What are the emerging trends?

-> Emerging trends include ARM-based server processors, AI-optimized chips, chiplet architectures, and advanced process nodes (5nm and below).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...