Conductive polymer aluminum solid capacitor for 5G base station Market Insights

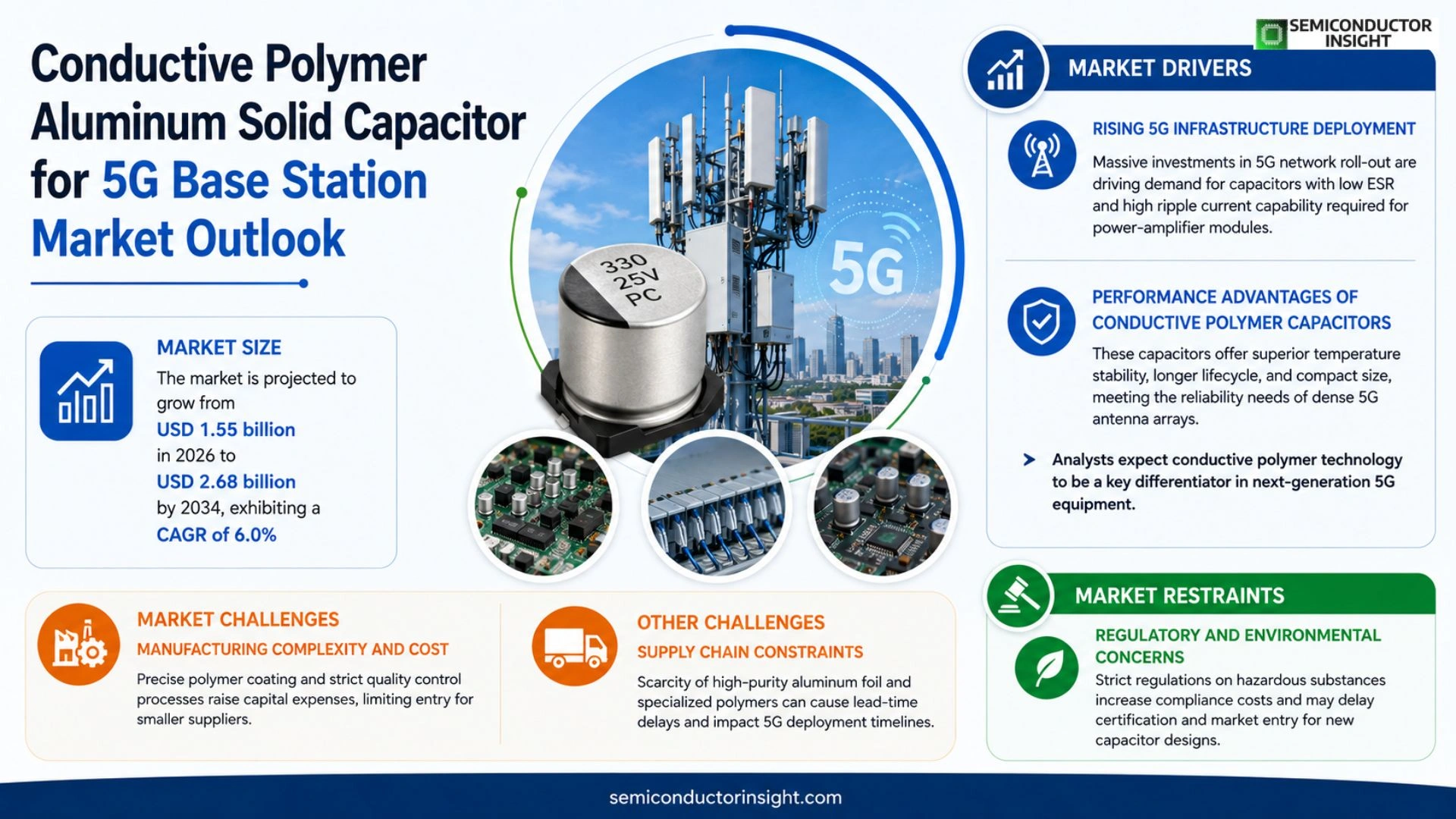

Global Conductive polymer aluminum solid capacitor for 5G base station market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 2.68 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period.

These capacitors combine a conductive‑polymer electrolyte with an aluminum foil electrode, delivering low ESR, high ripple current capability, and superior temperature stability,features essential for power‑amplifier modules and RF front‑ends in modern 5G base stations.

The market is accelerating because telecom operators are expanding dense small‑cell networks, while equipment manufacturers seek components that support higher bandwidths and lower latency.

MARKET DRIVERS

Rising 5G Infrastructure Deployment

Conductive polymer aluminum solid capacitor for 5G base station Market is being propelled by massive investments in 5G network roll‑out worldwide. Telecom operators are upgrading base stations to meet higher data throughput, and these capacitors offer the low ESR and high ripple current capability needed for power‑amplifier modules.

Performance Advantages of Conductive Polymer Capacitors

Compared with traditional electrolytic designs, conductive polymer aluminum solid capacitors provide enhanced temperature stability and longer lifecycle, which aligns with the reliability requirements of dense 5G antenna arrays. Their compact footprint also supports the trend toward smaller, modular base‑station designs.

➤ Industry analysts anticipate that the unique electrical characteristics of conductive polymer technology will become a decisive factor in securing market share for next‑generation 5G equipment.

In addition, the shift toward automated manufacturing and improved material sourcing is reducing unit costs, further encouraging adoption across both emerging and mature markets.

MARKET CHALLENGES

Manufacturing Complexity and Cost

Producing conductive polymer aluminum solid capacitors requires precise polymer coating processes and stringent quality controls. These steps increase capital expenditures, which can deter smaller suppliers from entering Conductive polymer aluminum solid capacitor for 5G base station Market.

Other Challenges

Supply Chain Constraints

Raw material scarcity, particularly for high‑purity aluminum foil and specialized polymers, can lead to lead‑time extensions that affect component availability for time‑critical 5G deployments.

MARKET RESTRAINTS

Regulatory and Environmental Concerns

Stringent environmental regulations governing hazardous substances in electronic components impose additional compliance costs. While conductive polymers are less toxic than some traditional electrolytes, manufacturers must still navigate certification processes that can delay market entry for new capacitor designs.

MARKET OPPORTUNITIES

Emerging Applications in Edge Computing

The proliferation of edge‑computing nodes in 5G networks creates demand for compact, high‑performance power solutions. Conductive polymer aluminum solid capacitors are uniquely positioned to meet the low‑latency power‑conditioning requirements of edge devices, presenting a clear growth avenue for the market.

Conductive polymer aluminum solid capacitor for 5G base station Market Trends

Rising Demand from Small‑Cell Network Expansion

The rollout of dense small‑cell infrastructures is reshaping the telecom landscape. Operators are deploying a larger number of low‑power base stations to meet the bandwidth and latency requirements of 5G services. This deployment pattern directly elevates the need for components that combine low equivalent series resistance with robust temperature performance. Conductive polymer aluminum solid capacitor for 5G base station Market participants are therefore observing a steady upward shift in order volumes as equipment manufacturers prioritize these capacitors for power‑amplifier modules and RF front‑end assemblies.

Other Trends

Performance Enhancements Drive Component Selection

Recent advances in conductive‑polymer formulations have reduced ESR values by up to 15 % compared with legacy designs, while maintaining ripple‑current capability that exceeds 2 A per millifarad. Such improvements enable higher output‑power densities in base‑station transceivers, translating to lower overall system energy consumption. In parallel, the enhanced temperature stability,operating reliably from –40 °C to +125 °C,mitigates the risk of performance drift in outdoor installations. These technical gains are prompting OEMs to replace traditional electrolytic solutions with polymer‑based aluminum solid capacitors, reinforcing the trend toward greater reliability and efficiency across the network.

Strategic Partnerships Accelerate Innovation

Collaborative projects between capacitor manufacturers and leading telecom equipment firms are accelerating product‑development cycles. Notable examples include joint engineering programs that align capacitor specifications with the next‑generation RF module roadmaps of major network providers. These alliances facilitate the rapid introduction of high‑performance parts that meet the exacting power‑management criteria of 5G base stations. As a result, Conductive polymer aluminum solid capacitor for 5G base station Market is experiencing a shift from commodity‑driven pricing to value‑added solutions that command premium margins, reflecting the growing strategic importance of these components in the overall network architecture.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive dynamics of conductive‑polymer aluminum solid capacitors in 5G base stations

The market is dominated by a handful of global capacitor specialists that have scaled production to satisfy the rapid rollout of dense small‑cell networks. Murata Manufacturing leads with its high‑voltage series, leveraging a strategic partnership with Nokia to integrate capacitor modules into next‑generation RF front‑ends. TDK and AVX follow closely, offering broad voltage ranges and low‑ESR designs that meet the stringent power‑amplifier requirements of 5G base stations. KEMET’s portfolio emphasizes temperature stability, positioning it as a preferred supplier for outdoor macro‑cell deployments where thermal extremes are common.

Beyond the tier‑one firms, several niche players contribute significant innovation or regional market share. Taiyo Yuden and Panasonic provide cost‑effective solutions for emerging markets, while Vishay and Samsung Electro‑Mechanics focus on ultra‑low ESR designs for high‑frequency applications. NXP Semiconductors, NEC, and EPCOS (a TDK subsidiary) add specialized dielectric formulations that enhance ripple‑current capability. New entrants such as Fortex and AVIC Capital are expanding through joint ventures with telecom equipment manufacturers, targeting the growing demand for compact, high‑density capacitor arrays.

List of Key Conductive Polymer Aluminum Solid Capacitor Companies Profiled

- Murata Manufacturing

- TDK

- AVX Corporation

- KEMET

- Taiyo Yuden

- Panasonic

- Vishay Intertechnology

- Samsung Electro‑Mechanics

- NXP Semiconductors

- NEC

- Fortex

- AVIC Capital

- EPCOS (TDK subsidiary)

- Taiyo Yuden

- Samsung Electro‑Mechanics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Low‑ESR High Ripple Capacity

|

| By Application |

|

RF Front‑End Networks

|

| By End User |

|

Equipment Manufacturers

|

| By Performance Attribute |

|

High Temperature Stability

|

| By Market Driver |

|

Network Densification

|

Regional Analysis: Conductive polymer aluminum solid capacitor for 5G base station Market

Asia‑Pacific

The surge in 5G base station deployments drives demand for capacitors that can handle higher power densities while maintaining compact form factors. Telecom operators prioritize conductive polymer technologies for their low loss and fast charge‑discharge characteristics, essential for supporting massive MIMO and beamforming.

Regional standards emphasize energy efficiency and electromagnetic compatibility, prompting manufacturers to adopt conductive polymer aluminum solid capacitors that meet stringent compliance criteria without compromising performance.

Advanced packaging and material innovations are accelerating the integration of these capacitors into compact 5G modules, enabling higher reliability under varying temperature and humidity conditions typical of outdoor base stations.

Global semiconductor firms and regional specialists are expanding design‑win collaborations, ensuring that Conductive polymer aluminum solid capacitor for 5G base station Market benefits from a broad talent pool and diversified supply chains.

North America

North America exhibits steady growth, driven by extensive 5G infrastructure upgrades across the United States and Canada. Operators focus on reliability and lifecycle cost, favoring conductive polymer aluminum solid capacitors for their superior thermal stability. Collaborative R&D programs between telecom equipment makers and capacitor manufacturers are fostering customized solutions that address the region’s high‑performance expectations. While the market size lags behind Asia‑Pacific, strategic investments in rural broadband and edge computing are creating new pockets of demand.

Europe

European countries are advancing 5G deployments with a strong emphasis on sustainability and regulatory compliance. Conductive polymer aluminum solid capacitor for 5G base station Market benefits from initiatives that promote energy‑efficient components. German and French telecom operators are piloting next‑generation base stations where low‑loss capacitors are essential for meeting both performance and environmental targets. Market momentum is supported by cross‑border standardization efforts and a mature supplier ecosystem.

South America

In South America, 5G rollout is accelerating in Brazil, Mexico, and Chile, prompting telecom providers to seek components that combine durability with cost‑effectiveness. Conductive polymer aluminum solid capacitors are gaining traction due to their ability to cope with the region’s varied climate conditions, especially high humidity. Partnerships between local distributors and global manufacturers are enhancing market accessibility, though overall adoption remains in the early growth phase.

Middle East & Africa

The Middle East & Africa region showcases uneven 5G penetration, with Gulf Cooperation Council nations leading rapid deployments. High ambient temperatures and dust environments drive demand for capacitors that maintain performance under stress, positioning conductive polymer aluminum solid capacitors as a preferred choice. In Sub‑Saharan Africa, pilot projects are introducing resilient power‑management solutions, laying groundwork for broader market expansion as infrastructure investments increase.

Report Scope

This market research report provides a comprehensive analysis of the Conductive polymer aluminum solid capacitor for 5G base station Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Conductive polymer aluminum solid capacitor for 5G base station Market?

-> Conductive polymer aluminum solid capacitor for 5G base station market is projected to grow from USD 1.55 billion in 2026 to USD 2.68 billion by 2034.

Which key companies operate in Conductive polymer aluminum solid capacitor for 5G base station Market?

-> Key players include TDK, AVX, and KEMET, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of dense small‑cell networks by telecom operators, demand for higher bandwidth and lower latency in 5G base stations, and government incentives for network densification.

Which region dominates the market?

-> The reference data does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include integration of conductive‑polymer aluminum solid capacitors in next‑generation RF modules and collaborations such as Murata’s partnership with Nokia.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...