Compute Express Link (CXL) Attached Memory Module for AI Market Insights

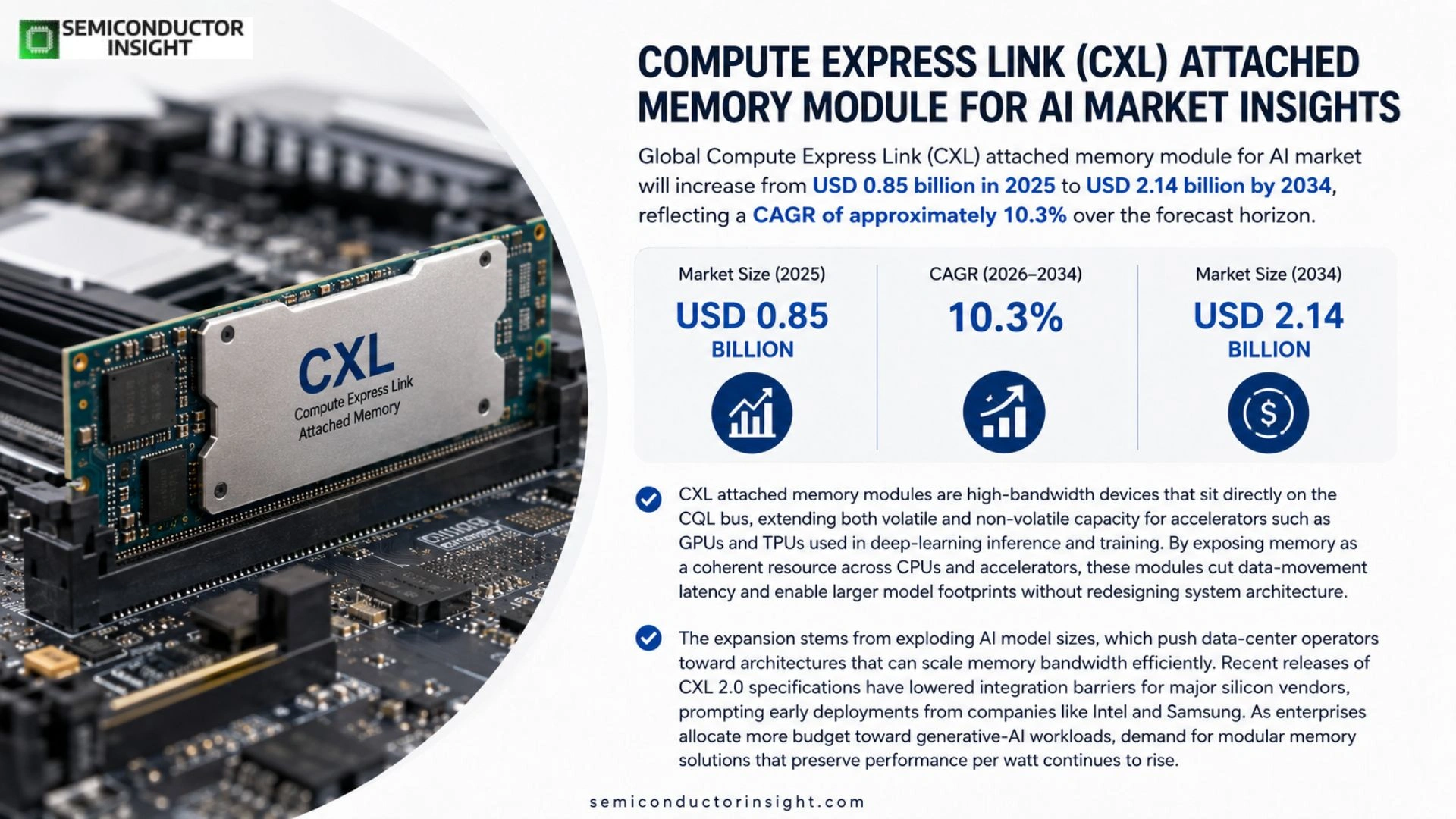

Global Compute Express Link (CXL) attached memory module for AI market size was valued at USD 0.85 billion in 2025. The market will increase from USD 0.85 billion in 2025 to USD 2.14 billion by 2034, reflecting a CAGR of approximately 10.3% over the forecast horizon.

CXL attached memory modules are high‑bandwidth devices that sit directly on the CQL bus, extending both volatile and non‑volatile capacity for accelerators such as GPUs and TPUs used in deep‑learning inference and training. By exposing memory as a coherent resource across CPUs and accelerators, these modules cut data‑movement latency and enable larger model footprints without redesigning system architecture.

The expansion stems from exploding AI model sizes, which push data‑center operators toward architectures that can scale memory bandwidth efficiently. Recent releases of CXL 2.0 specifications have lowered integration barriers for major silicon vendors, prompting early deployments from companies like Intel and Samsung. As enterprises allocate more budget toward generative‑AI workloads, demand for modular memory solutions that preserve performance per watt continues to rise.

MARKET DRIVERS

Performance Demands from Generative AI Workloads

Enterprises that run large language models and multimodal AI pipelines are encountering bandwidth ceilings on traditional memory interfaces. Compute Express Link (CXL) Attached Memory Module for AI Market addresses this bottleneck by delivering a unified, cache‑coherent pathway that reduces data movement latency and enables near‑memory compute. Consequently, system architects are redesigning servers to exploit the extra throughput, which translates into faster inference and shorter training cycles.

Standardization and Ecosystem Maturity

The release of CXL 3.0 and its rapid incorporation into major CPU and GPU silicon have fostered a stable foundation for attached memory solutions. Software stacks are beginning to expose native APIs, allowing developers to allocate memory directly on CXL modules without custom drivers. This convergence lowers entry barriers for OEMs and encourages a broader portfolio of memory‑centric accelerators.

➤ “CXL’s coherent fabric is reshaping how AI infrastructures think about memory, turning what used to be a peripheral concern into a strategic asset.”

These dynamics create a virtuous cycle: as performance expectations rise, vendors accelerate CXL‑based designs, which in turn expands the pool of compatible silicon. Business leaders recognizing this loop are allocating capital to early‑stage CXL memory projects, anticipating a competitive edge in AI service delivery.

MARKET CHALLENGES

Integration Complexity in Heterogeneous Systems

Deploying CXL‑attached memory alongside legacy DDR4/DDR5 stacks demands careful orchestration of firmware, BIOS settings, and operating‑system awareness. Misaligned configuration can negate latency benefits, forcing IT teams to invest in specialized validation tools. The learning curve slows adoption, especially for organizations with entrenched supply chains.

Other Challenges

Component Availability

The semiconductor shortage that began in 2020 still influences the supply of high‑bandwidth CXL memory chips. Tier‑1 manufacturers prioritize larger customers, leaving midsized firms to contend with longer lead times and premium pricing.

MARKET RESTRAINTS

Cost Premium of CXL‑Attached Memory

Compared with conventional DIMM solutions, CXL modules command a price premium of roughly 30‑45 % due to advanced packaging and additional logic layers. For cost‑sensitive data‑center operators, the ROI calculation hinges on clear performance gains, which are not yet uniformly quantified across all AI workloads. This financial hurdle tempers the pace of large‑scale procurement.

MARKET OPPORTUNITIES

Edge AI Deployments Requiring Compact Memory Pools

Edge devices that process video analytics or sensor fusion locally benefit from the reduced footprint of CXL‑attached memory, which consolidates compute and storage on a single fabric. As regulatory pressures push data processing to the edge, vendors that ship pre‑validated CXL memory kits stand to capture a growing niche. Early partnerships with telecom and autonomous‑vehicle players could unlock multi‑year revenue streams.

Compute Express Link (CXL) Attached Memory Module for AI Market Trends

Higher‑Bandwidth Memory Pools for AI Accelerators

The emergence of large‑scale generative‑AI models has forced data‑center architects to reconsider memory provisioning. By placing CXL‑attached memory modules directly on the interconnect bus, operators can expand both volatile and non‑volatile capacity without redesigning the host system. The net effect is a measurable reduction in data‑movement latency, which translates into higher throughput per watt for GPUs and TPUs during both inference and training phases. This technical advantage is prompting early‑stage investments from hyperscale providers seeking to sustain model growth while containing energy costs.

Other Trends

Standardization and Vendor Momentum

The debut of the CXL 2.0 specification lowered the entry barrier for silicon manufacturers, resulting in a wave of prototype announcements from Intel, Samsung, and a handful of emerging memory suppliers. These firms are emphasizing pin‑compatible designs that slot into existing server platforms, thereby accelerating time‑to‑market for AI workloads. As the ecosystem matures, we expect a cascade effect: broader software support, tighter integration with orchestration tools, and an increasingly competitive pricing environment.

Modular Memory as a Business Enabler

Enterprises are allocating a larger share of their capital budgets to generative‑AI initiatives, and they view modular memory as a flexible asset. Because CXL‑attached modules can be added or swapped in line with workload demand, organizations gain the ability to scale capacity incrementally rather than committing to monolithic upgrades. This modularity also aligns with sustainability goals, as refurbished modules can be redeployed across multiple clusters, extending the useful life of hardware and reducing total cost of ownership.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of CXL Attached Memory Modules for AI

Intel remains the anchor of the CXL attached‑memory ecosystem, leveraging its early‑stage silicon leadership and deep ties to data‑center OEMs. The company’s roadmap couples CXL 2.0‑compatible CPUs with proprietary DDR5‑on‑CXL modules that promise sub‑microsecond latency when accessed by GPUs or TPUs. This integration reduces the need for custom PCB designs and lowers total cost of ownership for hyperscale operators scaling generative‑AI workloads. Intel’s aggressive IP licensing strategy has also encouraged downstream vendors to adopt its reference designs, creating a de‑facto standardization layer that shapes procurement decisions across the industry.

Beyond Intel, a coalition of memory‑focused and compute‑centric firms is broadening the solution set. Samsung and Micron have launched high‑bandwidth DIMM‑form factor modules that exploit the extended address space of CXL, targeting workloads that require both volatile and persistent memory. SK Hynix, NVIDIA, and AMD contribute differentiated accelerators that directly consume CXL‑attached memory, while Google’s TPU teams are experimenting with proprietary CXL packs to accelerate training of trillion‑parameter models. Enterprise‑grade system integrators such as Dell Technologies, HPE, and Lenovo are packaging these components into turn‑key racks, whereas networking specialists like Cisco and Marvell embed CXL switches to orchestrate memory sharing across multi‑node clusters. The result is a multi‑tiered value chain where hardware innovators, module manufacturers, and systems integrators each capture distinct margins while collectively expanding the addressable market for AI‑focused memory solutions.

List of Key Compute Express Link (CXL) Attached Memory Module Companies Profiled

- Intel Corporation

- Samsung Electronics

- Micron Technology

- SK Hynix

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Google LLC (TPU Division)

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Lenovo Group Limited

- Cisco Systems

- Marvell Technology Group

- Broadcom Inc.

- Qualcomm Incorporated

- IBM Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

DRAM‑based modules are favored for latency‑critical AI workloads because they provide immediate data access across CPUs and accelerators.

|

| By Application |

|

Training accelerators drive demand for attached memory because they require sustained high bandwidth.

|

| By End User |

|

Cloud service providers lead adoption due to their need for flexible, scalable infrastructure.

|

| By Architecture |

|

Heterogeneous compute platforms emerge as the preferred architecture for advanced AI pipelines.

|

| By Performance Tier |

|

High‑bandwidth tier is critical for generative‑AI workloads that move massive data sets rapidly.

|

Regional Analysis: Compute Express Link (CXL) Attached Memory Module for AI Market

Large cloud providers are re‑architecting their AI clusters to reduce memory bottlenecks, and CXL‑attached modules appear as the most pragmatic bridge between compute and storage. By decoupling memory capacity from the processor package, operators can upgrade capacity without costly silicon redesigns, a flexibility that aligns with the rapid iteration cycles of AI model development.

A handful of silicon vendors have announced roadmaps that embed CXL link logic directly into their AI chips, while memory manufacturers are rolling out DDR‑compatible DIMMs certified for CXL operation. This dual-track approach creates a competitive yet collaborative environment, prompting incumbents to differentiate through firmware optimizations and latency‑tuning services.

Data‑centric regulations in the United States encourage firms to keep computation close to storage, indirectly favoring architectures that minimize data movement. CXL‑attached memory modules satisfy this regulatory thrust by allowing secure, high‑speed access to protected datasets without exposing them to external networks.

Beyond traditional neural‑network training, sectors such as autonomous vehicle simulation and real‑time video analytics are experimenting with CXL‑enhanced pipelines. The ability to attach terabytes of memory on demand shortens latency spikes, a characteristic prized by latency‑sensitive inference workloads.

Europe

European manufacturers are leveraging the continent’s strong standards‑setting heritage to craft interoperable CXL specifications that ease cross‑vendor integration. Nations with advanced semiconductor clusters, such as Germany and the Netherlands, are piloting hybrid memory systems within national AI research programs. The focus on sustainability is prompting designers to assess the energy profile of memory disaggregation, encouraging innovations that lower power per operation while preserving throughput. These dynamics position Europe as a strategic testbed for environmentally conscious deployment of Compute Express Link (CXL) Attached Memory Module for AI Market solutions.

Asia‑Pacific

In the Asia‑Pacific, rapid expansion of data‑center capacity is intersecting with aggressive governmental AI initiatives, creating a fertile ground for CXL adoption. Countries like Japan and South Korea possess deep expertise in high‑density packaging, allowing local OEMs to integrate CXL links directly onto system‑in‑package modules. Meanwhile, emerging markets such as India are investing in cloud‑first strategies that prioritize modular memory upgrades, making the region a prime candidate for cost‑effective scaling of AI workloads through attached memory technologies.

South America

South American enterprises are navigating a mixed landscape of legacy infrastructure and burgeoning AI curiosity. Early adopters in Brazil’s financial sector are experimenting with CXL‑enabled memory expansion to meet regulatory‑driven data residency requirements while boosting model performance. The region’s incremental approach, guided by pilot projects and university‑industry collaborations, suggests a gradual but steady infusion of Compute Express Link (CXL) Attached Memory Module for AI Market capabilities into mission‑critical applications.

Middle East & Africa

The Middle East & Africa region is witnessing a convergence of sovereign cloud ambitions and a desire to leapfrog traditional data‑center architectures. Initiatives in the United Arab Emirates and South Africa prioritize high‑performance AI research, and CXL‑attached memory modules are being evaluated for their ability to deliver memory elasticity without extensive capital expenditure. Investment funds are allocating capital toward niche start‑ups that specialize in low‑latency interconnects, indicating that Compute Express Link (CXL) Attached Memory Module for AI Market could become a cornerstone of the region’s next wave of digital transformation.

Report Scope

This market research report provides a comprehensive analysis of the Compute Express Link (CXL) Attached Memory Module for AI Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Compute Express Link (CXL) Attached Memory Module for AI Market?

-> Compute Express Link (CXL) Attached Memory Module for AI Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 2.14 billion by 2034.

Which key companies operate in Compute Express Link (CXL) Attached Memory Module for AI Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...