MARKET INSIGHTS

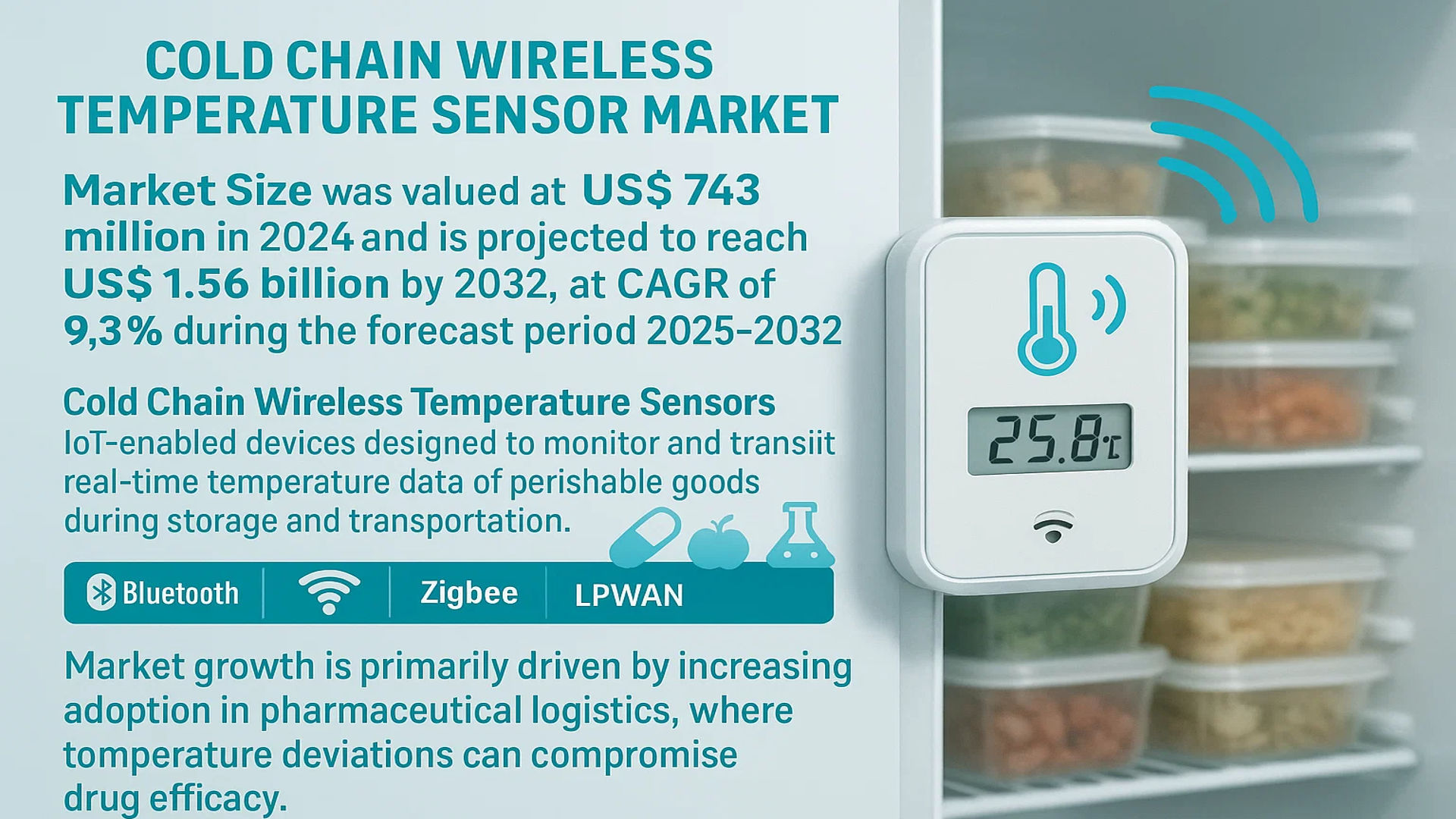

The global Cold Chain Wireless Temperature Sensor Market size was valued at US$ 743 million in 2024 and is projected to reach US$ 1.56 billion by 2032, at a CAGR of 9.3% during the forecast period 2025-2032.

Cold Chain Wireless Temperature Sensors are IoT-enabled devices designed to monitor and transmit real-time temperature data of perishable goods during storage and transportation. These sensors utilize wireless technologies such as Bluetooth, Wi-Fi, Zigbee, or LPWAN (Low-Power Wide-Area Networks) to ensure temperature-sensitive products like pharmaceuticals, food, and chemicals remain within specified ranges. The demand for these sensors is surging due to stringent regulatory requirements and the need to minimize spoilage risks.

Market growth is primarily driven by increasing adoption in pharmaceutical logistics, where temperature deviations can compromise drug efficacy. For instance, the FDA mandates strict temperature monitoring for biologics, creating a significant demand for reliable wireless sensors. Additionally, the food industry is leveraging these technologies to comply with food safety regulations such as the Food Safety Modernization Act (FSMA). Leading players like Honeywell, Sensitech Inc., and Monnit Corporation are expanding their product portfolios with advanced LPWAN-based sensors, further accelerating market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Global Expansion of Cold Chain Logistics to Fuel Demand for Wireless Temperature Sensors

The global cold chain logistics market is experiencing exponential growth, projected to exceed $650 billion by 2030, creating substantial demand for advanced monitoring solutions. Wireless temperature sensors play a critical role in maintaining product integrity across pharmaceutical, food, and chemical supply chains. With perishable goods accounting for nearly 40% of global food production, the need for real-time temperature monitoring has never been greater. This technology enables stakeholders to track product conditions remotely, ensuring compliance with stringent regulatory requirements while minimizing spoilage risks. Recent technological advancements in LPWAN (Low Power Wide Area Network) sensors are further accelerating adoption rates in long-distance cold chain applications.

Stringent Regulatory Standards Driving Technology Adoption Across Industries

Regulatory bodies worldwide are implementing stricter temperature monitoring mandates, particularly in pharmaceutical and food sectors. The FDA’s revised guidance on temperature-controlled logistics requires comprehensive monitoring throughout the supply chain, creating mandatory demand for wireless sensor solutions. Similar regulations in the EU’s Good Distribution Practice guidelines now mandate continuous temperature recording for sensitive biologics. These requirements are pushing companies to replace manual monitoring with automated wireless systems that provide audit-ready documentation. The global pharmaceutical cold chain market, valued at over $20 billion, represents a particularly strong growth sector for these technologies given the temperature sensitivity of vaccines and biologics.

IoT Infrastructure Expansion Enabling Widespread Sensor Deployment

The rapid development of global IoT infrastructure provides the backbone for widespread cold chain sensor deployment. With over 14 billion connected IoT devices currently in operation and 5G networks expanding coverage, wireless temperature monitoring systems can now transmit data more reliably across global supply chains. Emerging LPWAN technologies like LoRaWAN and NB-IoT offer extended battery life exceeding 10 years and kilometer-range connectivity, making them ideal for cold chain applications. The maturation of these networks allows for cost-effective scaling of monitoring solutions, particularly in emerging markets where cold chain infrastructure is rapidly developing.

MARKET RESTRAINTS

High Implementation Costs Limit Adoption Among Small-Scale Operators

While wireless temperature monitoring delivers significant value, the initial investment remains prohibitive for many businesses. Complete cold chain monitoring solutions can require capital expenditures exceeding $50,000 for medium-sized operations, with ongoing subscription fees for cloud-based data platforms. This financial barrier particularly affects small-scale food producers and regional logistics providers operating on thin margins. Many operators continue relying on manual logging methods despite their limitations because of these cost considerations. The challenge intensifies in developing markets where cold chain infrastructure itself is still being established.

Interoperability Challenges Create Integration Headaches

The lack of standardized communication protocols among sensor manufacturers creates significant implementation challenges. Many wireless temperature monitoring systems operate on proprietary platforms that don’t integrate smoothly with existing enterprise resource planning (ERP) or warehouse management systems. This forces companies to either replace entire monitoring infrastructures or maintain parallel systems – both costly propositions. The situation is particularly acute in global supply chains where different partners may use incompatible technologies. While industry consortia are working on standardization, the current fragmentation remains a substantial barrier to seamless cold chain visibility.

MARKET OPPORTUNITIES

Emerging Markets Present Significant Growth Potential

Developing economies represent the fastest-growing opportunity for cold chain temperature monitoring solutions. Countries across Southeast Asia, Africa, and Latin America are investing heavily in cold chain infrastructure to support growing middle-class consumption and pharmaceutical distribution networks. The Asia-Pacific cold chain logistics market alone is projected to grow at over 15% annually through 2030. This expansion creates demand for cost-effective wireless monitoring solutions tailored to regional infrastructure challenges. Companies that can deliver rugged, easy-to-deploy systems at competitive price points stand to capture significant market share in these high-growth regions.

AI-Powered Analytics Creating New Value Propositions

The integration of artificial intelligence with temperature monitoring systems is unlocking powerful new capabilities. Advanced analytics platforms can now predict equipment failures before they occur by analyzing temperature patterns and compressor performance data. Some systems can optimize refrigerator settings in real-time based on inventory levels and external weather conditions, reducing energy consumption by up to 20%. As these intelligent features demonstrate measurable ROI through reduced spoilage and energy savings, they’re driving upgrades from basic monitoring systems to more sophisticated AI-enabled platforms.

MARKET CHALLENGES

Battery Life Limitations Create Maintenance Headaches

While wireless sensor technology has advanced significantly, battery life remains a persistent challenge in extreme cold chain environments. Sub-zero temperatures can dramatically reduce battery performance, forcing more frequent replacements that disrupt operations. In pharmaceutical ultra-cold chain applications (-70°C), some sensors require battery swaps as often as every three months. This maintenance burden increases total cost of ownership and creates potential gaps in temperature monitoring during replacement procedures. While energy harvesting technologies show promise, they haven’t yet achieved the reliability needed for mission-critical cold chain applications.

Data Security Concerns Impede Cloud Adoption

As temperature monitoring systems increasingly rely on cloud-based platforms, data security has become a significant concern. Pharmaceutical companies handling sensitive clinical trial materials or proprietary formulations are particularly cautious about transmitting temperature data to external servers. Recent high-profile supply chain cyberattacks have heightened these concerns, causing some organizations to delay cloud-based monitoring implementations. Manufacturers must invest heavily in end-to-end encryption and blockchain-based audit trails to address these security apprehensions and gain customer trust.

COLD CHAIN WIRELESS TEMPERATURE SENSOR MARKET TRENDS

Rising Demand for Real-Time Temperature Monitoring to Drive Market Growth

The global cold chain wireless temperature sensor market is witnessing significant growth, primarily driven by the increasing need for real-time temperature monitoring in perishable supply chains. The market was valued at approximately $592.4 million in 2024 and is projected to grow at a CAGR of 10.8% through 2032. This is largely attributed to the stringent regulatory requirements in pharmaceuticals and food safety, where temperature control is critical. The adoption of IoT-enabled sensors is accelerating as businesses seek data accuracy and compliance with international standards such as the FDA’s Food Safety Modernization Act (FSMA) and WHO GDP guidelines for pharmaceuticals.

Other Trends

Integration of AI and LPWAN Technologies

Companies are increasingly leveraging AI-driven analytics alongside wireless temperature sensors to optimize cold chain logistics. Predictive maintenance, anomaly detection, and automated alerts have become standard features, enhancing operational efficiency. For instance, LPWAN technologies like LoRaWAN and NB-IoT now account for over 35% of new cold chain sensor deployments due to their long-range, low-power consumption capabilities. The rise of 5G networks, particularly in North America and Asia-Pacific, is further supporting high-density IoT applications in cold storage facilities.

Expansion of Pharmaceutical Cold Chain Logistics

The pharmaceutical sector remains a dominant end-user, with biologics and vaccines demanding ultra-cold storage solutions. Post-pandemic, investments in vaccine distribution networks have surged, with wireless sensor deployments growing by 22% annually in this segment. Meanwhile, emerging markets are witnessing rapid infrastructure upgrades; for example, India’s cold chain capacity expanded by 28% in 2023 to meet vaccine storage needs. Customizable sensor solutions with multi-parameter monitoring (temperature, humidity, light exposure) are gaining traction to meet diverse regulatory and logistical requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Alliances Drive Market Competition

The global cold chain wireless temperature sensor market features a dynamic mix of established semiconductor giants and specialized IoT solution providers, creating a semi-competitive ecosystem. Texas Instruments leads the market with its comprehensive portfolio of low-power wireless connectivity solutions, capturing approximately 18% of the 2024 market share. The company’s dominance stems from its robust R&D investments—allocating 12% of annual revenue to innovation—and strategic partnerships with logistics providers.

Sensirion AG and STMicroelectronics have emerged as strong contenders, particularly in the European and Asian markets where regulatory requirements for pharmaceutical cold chains are stringent. These companies differentiate themselves through ultra-accurate sensors (±0.1°C precision) and battery optimization technologies that extend device lifespans beyond 5 years—a critical advantage in remote monitoring applications.

Meanwhile, Honeywell is aggressively expanding its position through vertical integration, combining its industrial automation expertise with newly acquired wireless sensor technologies. The company’s recent $450 million investment in IoT infrastructure demonstrates its commitment to capturing a larger share of the cold chain monitoring segment.

The market also sees growing participation from Japanese conglomerates like Panasonic, whose proprietary LPWAN solutions specifically address Asia’s unique cold storage challenges. These include high-density urban distribution networks and tropical climate conditions that demand robust humidity resistance alongside temperature monitoring.

List of Key Cold Chain Wireless Temperature Sensor Providers

- Texas Instruments (U.S.)

- Sensirion AG (Switzerland)

- STMicroelectronics (Switzerland)

- Honeywell International Inc. (U.S.)

- Panasonic Holdings Corporation (Japan)

- TE Connectivity (Switzerland)

- NXP Semiconductors (Netherlands)

- Robert Bosch GmbH (Germany)

- Analog Devices, Inc. (U.S.)

Segment Analysis:

By Type

LPWANs Technology Segment Leads Due to Enhanced Energy Efficiency and Long-Range Connectivity

The market is segmented based on type into:

- Traditional Wireless Technology

- Subtypes: Wi-Fi, Bluetooth, Zigbee, and others

- LPWANs Technology

- Subtypes: LoRaWAN, NB-IoT, Sigfox, and others

By Application

Cold Chain Logistics Segment Dominates Owing to Rising Demand for Real-Time Temperature Monitoring

The market is segmented based on application into:

- Refrigerated Storage

- Cold Chain Logistics

- Others

By End User

Pharmaceutical & Healthcare Sector Holds Significant Share Due to Strict Regulatory Compliance

The market is segmented based on end user into:

- Pharmaceutical & Healthcare

- Food & Beverage

- Chemicals

- Others

Regional Analysis: Cold Chain Wireless Temperature Sensor Market

Asia-Pacific

The Asia-Pacific region leads the global Cold Chain Wireless Temperature Sensor market, driven by rapid industrialization, expanding cold chain infrastructure, and the rising adoption of IoT-enabled solutions in logistics. Countries like China, Japan, and India exhibit strong demand due to increasing pharmaceutical and food safety regulations. China’s cold chain logistics market surpassed $42 billion in 2023, with wireless sensors becoming critical for regulatory compliance in temperature-sensitive shipments. India’s government initiatives like the National Cold Chain Development Program further propel adoption, though cost sensitivity limits penetration among small-scale operators. Meanwhile, Japan’s advanced manufacturing capabilities position it as a key supplier of high-precision sensors.

North America

North America’s market growth is fueled by strict FDA and USDA mandates requiring real-time temperature monitoring for perishable goods. The U.S. dominates with over 60% of the regional revenue share, supported by widespread 5G connectivity and investments in automated warehousing. The pharmaceutical sector is a major adopter, with companies like McKesson and Pfizer integrating LPWAN-based sensors for vaccine logistics. Canada’s cold chain expansion, particularly in Alberta’s Agri-food corridor, presents untapped opportunities. However, high installation costs and data security concerns remain challenges for SMEs.

Europe

Europe’s market thrives on stringent EU regulations, including GDP compliance for pharmaceuticals and EC No 852/2004 for food safety. Germany and France lead in technological adoption, with 40% of regional sensor deployments utilizing energy-efficient LoRaWAN protocols. The UK’s focus on reducing food waste—9.5 million tonnes annually—drives logistics modernization, while Nordic countries prioritize sustainable refrigeration solutions. Challenges include fragmented cold chain networks in Eastern Europe and Brexit-related trade complexities affecting cross-border sensor standardization.

South America

Growth in South America is uneven, with Brazil and Argentina accounting for 75% of regional demand. Brazil’s ANVISA regulations mandate temperature monitoring for biologics, boosting pharmaceutical applications. Argentina’s meat export industry increasingly adopts sensors to meet EU import standards. However, infrastructure gaps and economic instability slow broader adoption. Chile and Colombia show promise with public-private partnerships to upgrade perishable logistics, yet reliance on imported sensors limits cost competitiveness.

Middle East & Africa

The MEA region is nascent but exhibits high growth potential, driven by GCC countries’ investments in healthcare infrastructure. The UAE’s Dubai Industrial Strategy 2030 prioritizes smart logistics, with wireless sensors integral to temperature-controlled airport hubs. South Africa leads in sub-Saharan Africa due to its pharmaceutical manufacturing hub in Gauteng. Barriers include low awareness, budget constraints, and extreme climates straining sensor durability. Long-term opportunities lie in vaccine distribution networks and expanding supermarket chains.

Report Scope

This market research report provides a comprehensive analysis of the Global Cold Chain Wireless Temperature Sensor Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at US$ 743 million in 2024 and is projected to reach US$ 1.56 billion by 2032, growing at a CAGR of 9.3%.

- Segmentation Analysis: Detailed breakdown by product type (Traditional Wireless Technology, LPWANs Technology), application (Refrigerated Storage, Cold Chain Logistics, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates with 42% market share.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of IoT (with over 14 billion connected devices globally), 5G networks (China has deployed 2.3 million 5G base stations), and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing pharmaceutical cold chain demand, food safety regulations) along with challenges (high implementation costs, data security concerns).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Cold Chain Wireless Temperature Sensor Market?

-> Cold Chain Wireless Temperature Sensor Market size was valued at US$ 743 million in 2024 and is projected to reach US$ 1.56 billion by 2032, at a CAGR of 9.3% during the forecast period 2025-2032.

Which key companies operate in Global Cold Chain Wireless Temperature Sensor Market?

-> Key players include Robert Bosch GmbH, Honeywell, Analog Devices, NXP Semiconductors, Infineon Technologies, and TE Connectivity, among others.

What are the key growth drivers?

-> Key growth drivers include increasing pharmaceutical cold chain demand, stringent food safety regulations, and growth in IoT adoption (14 billion connected devices globally).

Which region dominates the market?

-> Asia-Pacific is the dominant market with 42% share, driven by China’s rapid 5G deployment (2.3 million base stations) and growing cold chain infrastructure.

What are the emerging trends?

-> Emerging trends include integration with 5G networks, AI-powered predictive analytics, and ultra-low power LPWAN technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...