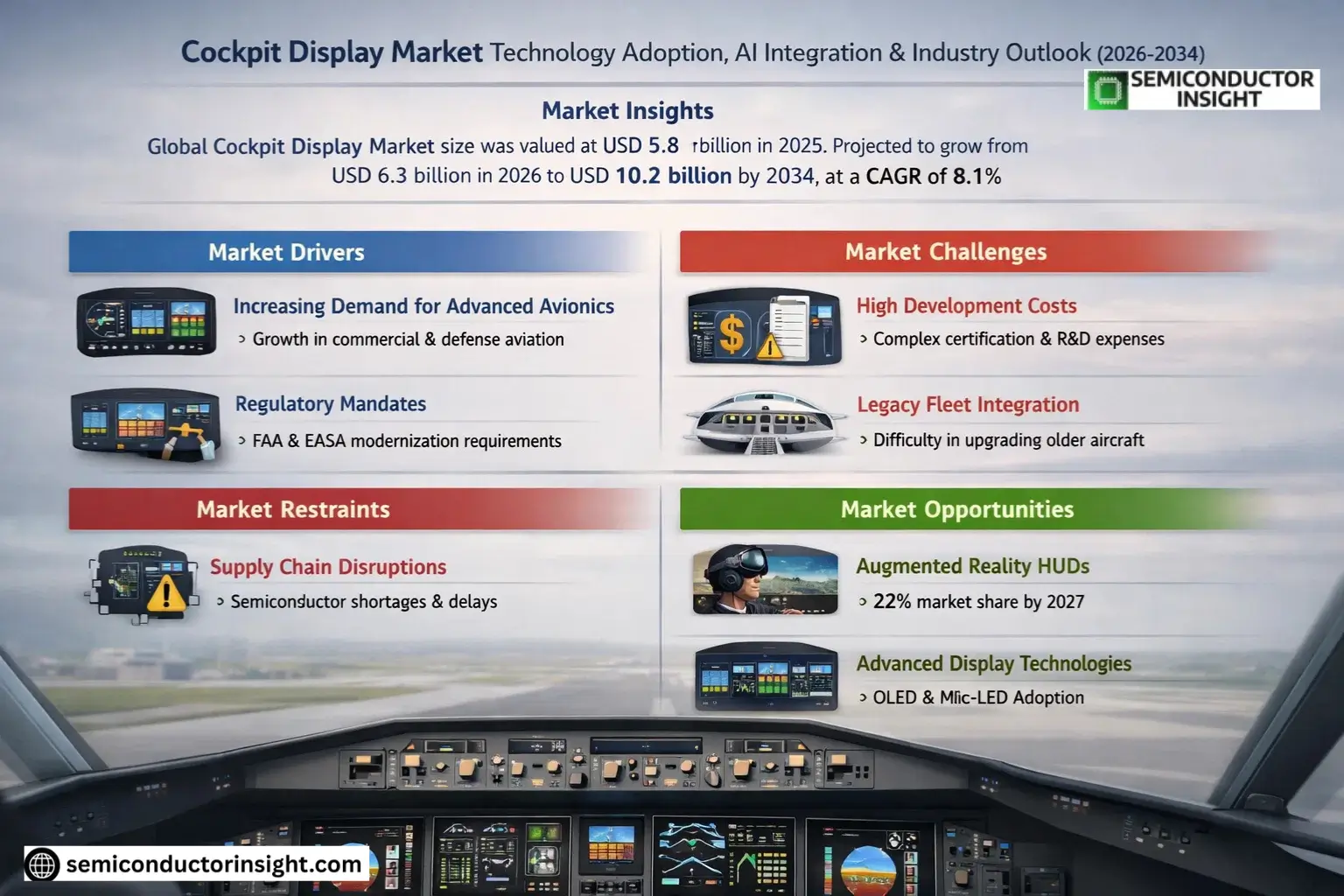

Market Insights

Global Cockpit Display Market size was valued at USD 5.8 billion in 2025. The market is projected to grow from USD 6.3 billion in 2026 to USD 10.2 billion by 2034, exhibiting a CAGR of 8.1% during the forecast period.

Cockpit displays are advanced human-machine interface systems used in aircraft and automotive applications to present critical operational data such as navigation, communication, and vehicle performance metrics. These systems integrate multiple technologies including LCD, OLED, and Mini LED panels with touch interfaces and projection systems to create centralized information hubs for pilots and drivers.

The market growth is driven by increasing demand for advanced avionics in commercial aviation and the rapid adoption of digital instrument clusters in premium vehicles. While aerospace applications currently dominate revenue share, automotive adoption is accelerating due to rising consumer expectations for connected car features. Major manufacturers are investing heavily in augmented reality displays and head-up display technologies to enhance situational awareness across both sectors.

MARKET DRIVERS

Increasing Demand for Advanced Avionics Systems

Cockpit Display Market is experiencing robust growth due to the rising adoption of advanced avionics in modern aircraft. Airlines and defense sectors are prioritizing glass cockpit technologies to enhance flight safety, operational efficiency, and situational awareness. The global commercial aviation sector’s expansion further accelerates demand for these systems.

Regulatory Mandates Driving Modernization

Stringent aviation regulations, including mandates by the FAA and EASA for NextGen and SESAR implementations, compel aircraft operators to upgrade legacy displays. By 2025, over 65% of new aircraft deliveries are projected to feature integrated cockpit display systems as standard equipment.

Military modernization programs worldwide are allocating substantial budgets for cockpit display upgrades, particularly for multi-function displays (MFDs) and head-up displays (HUDs).

MARKET CHALLENGES

High Development and Certification Costs

Cockpit Display Market faces significant barriers due to the complex certification processes and substantial R&D investments required for avionics systems. Each display unit must undergo rigorous testing to meet DO-178C and DO-254 standards, increasing time-to-market by 18-24 months.

Other Challenges

Legacy Fleet Integration Issues

Retrofitting older aircraft with modern cockpit displays presents technical compatibility challenges, with over 35% of operators reporting integration difficulties during avionics upgrades.

MARKET RESTRAINTS

Supply Chain Disruptions Impacting Production

Cockpit Display Market faces constraints from semiconductor shortages and fluctuating display panel availability. Lead times for critical components have extended to 9-12 months, delaying delivery schedules across the aviation industry. This has particularly affected the production of OLED-based cockpit displays, which require specialized materials.

MARKET OPPORTUNITIES

Emergence of Augmented Reality Displays

Cockpit Display Market is witnessing transformative opportunities with the development of augmented reality HUDs that project critical flight information directly onto the windshield. These systems are expected to capture 22% market share by 2027, driven by their ability to reduce pilot cognitive load during critical flight phases. The growing adoption of touchscreen cockpit displays in business jets also presents significant growth potential.

Cockpit Display Market Trends

Rising Adoption of Advanced Display Technologies

Cockpit Display Market is experiencing rapid technological evolution, with automotive and aerospace sectors increasingly adopting OLED and mini-LED displays. These technologies offer superior brightness, contrast ratios, and energy efficiency compared to traditional LCD solutions. Major manufacturers are focusing on developing displays with higher resolution (up to 8K) and wider color gamuts to meet strict aviation and automotive visibility requirements.

Other Trends

Cost Pressure from Raw Material Inflation

Display modules, driver chips, and printed circuit boards collectively account for approximately 85% of cockpit display material costs. Recent supply chain disruptions have exacerbated cost pressures, with automotive-grade display manufacturers implementing localization strategies and long-term supplier contracts to stabilize pricing. The industry is responding with design optimizations to reduce reliance on scarce semiconductor components.

Integration of Multi-functional HMI Systems

Cockpit displays are evolving from simple information screens to comprehensive human-machine interfaces incorporating touch, gesture, and voice controls. The market sees growing demand for configurable displays that can present flight/driving data, navigation, and entertainment content through unified interfaces. This integration trend is particularly strong in commercial aviation and premium automotive segments.

Geographical Market Shifts

Asia-Pacific has emerged as the fastest-growing region for cockpit display adoption, driven by expanding commercial aviation fleets and premium automotive production in China, South Korea, and Japan. North America maintains leadership in advanced aerospace applications, while European manufacturers emphasize modular display solutions for electric vehicle platforms. The Middle East shows increasing demand for cockpit displays in business aviation and defense applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Cockpit Display Market Poised for 8.1% CAGR Growth Through 2034

Cockpit Display Market is dominated by established aerospace and automotive electronics suppliers, with Continental AG, Honeywell Aerospace, and Thales leading through integrated smart cockpit solutions. These top-tier suppliers control approximately 42% of the global market share, leveraging vertical integration from display panels to human-machine interface software. The industry shows a mix of specialized display manufacturers like AU Optronics and Japan Display Inc collaborating with system integrators to deliver certified aviation and automotive-grade solutions.

Niche innovators like Garmin Ltd and Elbit Systems are gaining traction with specialized mission displays for general aviation and defense applications. The market sees increasing participation from automotive display specialists such as Alpine Electronics and Innolux Corporation, who bring cost-optimized solutions for mass-market vehicles. Emerging competition comes from defense contractors like Northrop Grumman and Rockwell Collins, focusing on ruggedized military cockpit systems with advanced visualization capabilities.

List of Key Cockpit Display Companies Profiled

- AU Optronics Corp

- Rockwell Collins Inc

- Innolux Corporation

- General Dynamics

- Alpine Electronics

- Garmin Ltd

- Continental AG

- Honeywell Aerospace

- Japan Display Inc

- Transdigm

- Thales

- Collins Aerospace

- Elbit Systems

- Northrop Grumman

- Visteon Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Driver-Assist Displays are gaining prominence in the cockpit display sector due to increasing demand for advanced driver assistance systems.

|

| By Application |

|

Automotive applications dominate cockpit display demand with evolving smart cockpit technologies.

|

| By End User |

|

OEMs represent the primary customer base for cockpit displays with stringent integration requirements.

|

| By Display Technology |

|

OLED technology is emerging as a preferred choice for premium cockpit displays.

|

| By Display Size |

|

8-12 inches displays represent the sweet spot for current cockpit implementations.

|

Regional Analysis: Cockpit Display Market

North America

Technology Leadership

North American manufacturers lead in developing advanced cockpit display technologies including 4K resolution screens, sunlight-readable displays, and intuitive touch interfaces. The region accounts for nearly half of global R&D investments in aviation display systems.

AI Integration

Significant progress in AI-based predictive maintenance displays and adaptive interfaces that adjust to pilot preferences. Machine learning algorithms help optimize information presentation based on flight phase and operational conditions.

Regulatory Advantage

FAA’s progressive stance on display certification facilitates faster implementation of new technologies. The regulator actively collaborates with manufacturers to establish standards for emerging display systems.

Military Innovation

Pentagon-funded programs drive development of ruggedized, high-performance displays for fighter jets and helicopters. Specialized systems integrate sensor fusion and threat visualization capabilities for enhanced situational awareness.

Europe

Europe maintains strong position in the Cockpit Display Market through collaborative aerospace programs and emphasis on pilot-centric design. Airbus-led initiatives promote standardization across commercial aviation displays, while defense manufacturers develop high-reliability systems for military applications. The region shows growing adoption of curved and reconfigurable displays that optimize cockpit space. Strict environmental regulations push development of energy-efficient display technologies with lower power consumption.

Asia-Pacific

Asia-Pacific emerges as the fastest-growing Cockpit Display Market, driven by expanding commercial fleets and indigenous aircraft programs. China and Japan lead regional innovation with government-backed display technology initiatives. Local manufacturers focus on cost-effective solutions without compromising performance, catering to budget-conscious airlines. Increasing defense spending across the region spurs demand for advanced military aircraft displays with localized interfaces.

Middle East & Africa

The Middle East shows notable cockpit display adoption in premium commercial aviation segments, with Gulf carriers specifying the latest display technologies for their fleets. African markets demonstrate gradual modernization, focusing on retrofitting older aircraft with modern display systems. Regional military forces invest in helicopter and trainer aircraft displays to enhance operational capabilities with constrained budgets.

South America

South America presents steady cockpit display demand focused on fleet upgrades and regional aircraft modernization. Local regulatory bodies work to align with international aviation display standards. The region shows particular interest in multifunction displays that consolidate flight information while reducing cockpit clutter, suitable for diverse operational environments.

Report Scope

This market research report provides a comprehensive analysis of the Cockpit Display Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of cockpit displays in powering advancements across industries such as aerospace, automotive, and rail/marine sectors.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Mission Displays, Driver-Assist Displays), interaction dimension (2D, 3D), imaging method (Direct-view Panel, Reflective HUD), and application (Aerospace, Automotive, Railway/Marine).

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging display technologies, integration of smart systems, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, and raw material cost issues.

- Stakeholder Insights: Insights for display manufacturers, OEMs, system integrators, and investors regarding the evolving ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Cockpit Display Market?

-> Cockpit Display Market size was valued at USD 5.8 billion in 2025. The market is projected to grow from USD 6.3 billion in 2026 to USD 10.2 billion by 2034, exhibiting a CAGR of 8.1% during the forecast period.

What was the unit shipment volume in 2025?

-> Global cockpit display sales reached 309,000 units in 2025, with an average price of USD 20,493 per unit.

Which companies lead the Cockpit Display Market?

-> Key players include AU Optronics, Rockwell Collins, Continental AG, Honeywell Aerospace, Thales, and Japan Display Inc, among others.

What are the main cost components?

-> Display modules account for 35% of costs, while driver chips, PCBs and structural components make up 50%. Raw materials constitute >60% of total production costs.

What are the key application segments?

-> Major applications are Aerospace, Automotive, and Railway/Marine sectors, with automotive being the dominant segment.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...