Co-Packaged Optics (CPO) Market Insights

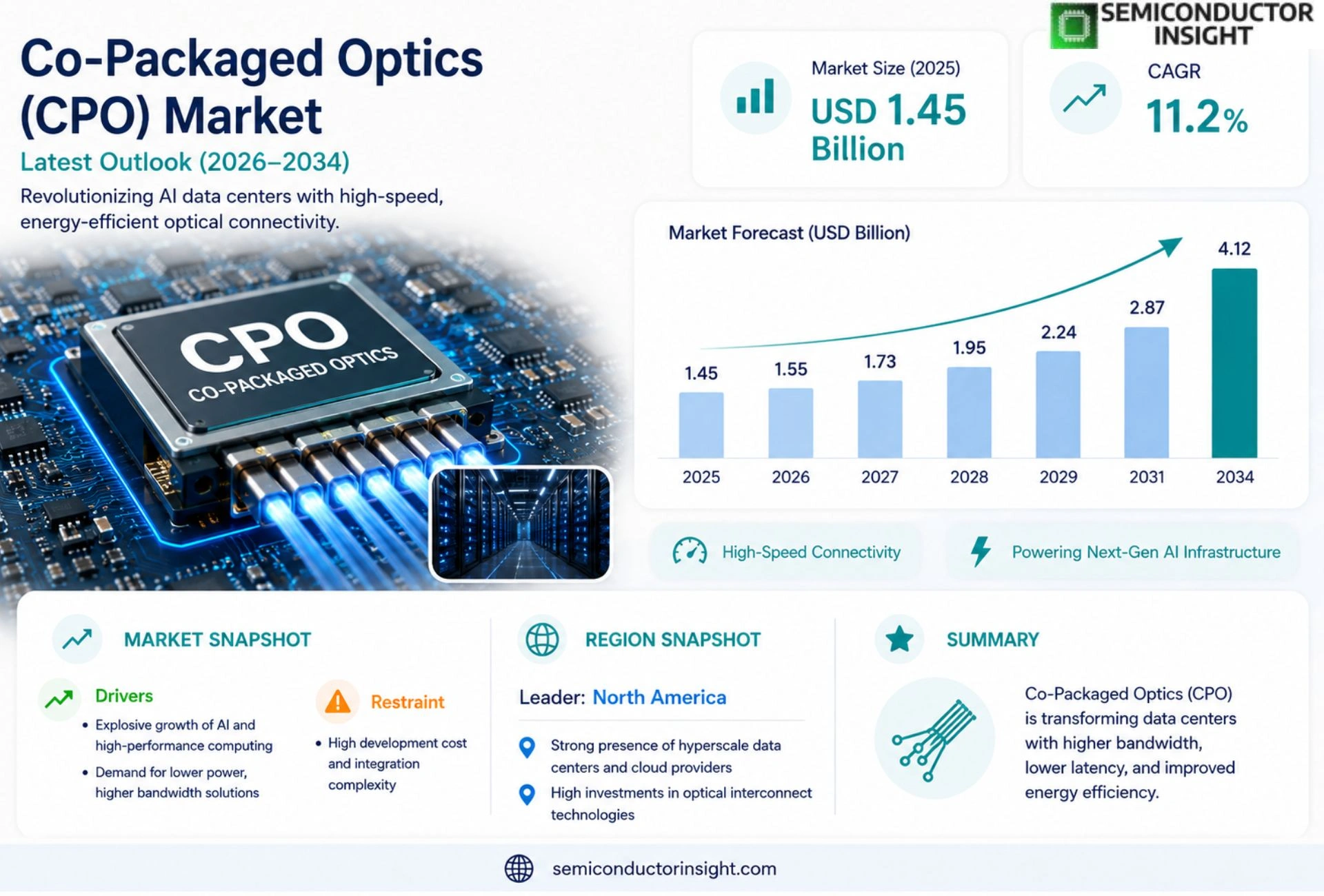

Global Co-Packaged Optics (CPO) market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 4.12 billion by 2034, exhibiting a CAGR of 11.2% during the forecast period.

CPO technology integrates optical transceiver components directly with electronic driver ASICs within a single package, eliminating traditional electrical‑optic interfaces. This co‑packaging reduces power consumption, improves signal integrity, and enables higher lane counts such as 400 Gbps and beyond,critical for next‑generation data‑center and telecom infrastructure.

The market is accelerating because hyperscale data‑center expansion, rollout of 5G/6G networks, and demand for higher bandwidth drive adoption of compact, energy‑efficient solutions. Furthermore, major players,including Intel, Broadcom, Cisco and Acacia Communications,are investing heavily in R&D and strategic partnerships to broaden product portfolios and capture emerging opportunities.

MARKET DRIVERS

Increasing Data‑Center Bandwidth Demand

Enterprises are expanding hyperscale data‑center footprints to support cloud‑native workloads, driving a need for aggregated optical capacity that exceeds 400 Gb/s per port. The Co‑Packaged Optics (CPO) Market meets this need by integrating photonics directly onto switch ASICs, thereby reducing latency and enabling higher throughput without proportional power increase.

Cost Efficiency and Power Savings

By eliminating discrete transceiver modules, CPO solutions cut bill‑of‑materials costs by up to 30 % and lower power consumption per bit transmitted. Operators observe measurable OPEX reductions as cooling requirements decline and rack density improves, which accelerates adoption across carrier and enterprise segments.

➤ “Integrating optics at the silicon level is reshaping network economics, delivering both performance and sustainability gains.”

Strategic partnerships between silicon vendors and optical foundries are further shortening time‑to‑market, ensuring that the Co‑Packaged Optics (CPO) Market remains aligned with evolving Ethernet standards and customer rollout schedules.

MARKET CHALLENGES

Technical Integration Complexity

Co‑packaging requires precise alignment of photonic components with high‑speed ASICs, demanding advanced packaging processes and rigorous testing. Any mismatch can introduce signal integrity issues, compelling manufacturers to invest heavily in specialized equipment and expertise.

Other Challenges

Supply‑Chain Volatility

The reliance on a limited number of silicon photonics foundries heightens exposure to material shortages and geopolitical risks, potentially slowing the scale‑up of CPO production lines.

MARKET RESTRAINTS

Regulatory and Standardization Hurdles

While industry bodies are progressing toward unified 800 Gb/s and 1.6 Tb/s specifications, the interim lack of universally accepted standards creates uncertainty for early adopters, limiting broader deployment of Co‑Packaged Optics (CPO) Market solutions.

MARKET OPPORTUNITIES

Emerging 800G and 1.6T Platforms

Next‑generation Ethernet roadmaps set the stage for 800 Gb/s and 1.6 Tb/s transceiver lanes, areas where CPO’s integration advantage is most pronounced. early pilots in high‑performance computing clusters indicate strong willingness to transition once mature, creating a sizable growth runway for vendors that can deliver reliable, cost‑effective solutions.

Co-Packaged Optics (CPO) Market Trends

Integration of Optics and Electronics Drives Adoption

Co-Packaged Optics (CPO) market is increasingly defined by the seamless integration of optical transceivers with ASIC driver circuits inside a single package. This integration eliminates traditional electrical‑optic interfaces, delivering lower power consumption and tighter signal integrity. As data‑center operators expand capacity to support cloud workloads, the ability to deliver 400 Gbps lane speeds or higher within a compact footprint becomes a decisive factor. Energy‑efficient designs also align with sustainability goals of hyperscale facilities, reducing cooling load and overall operational expense. Consequently, customers prioritize solutions that combine high bandwidth with reduced power per bit, positioning co‑packaged optics as a preferred technology for next‑generation infrastructure.

Other Trends

Strategic Partnerships and R&D Investment

Key industry players,including Intel, Broadcom, Cisco, and Acacia Communications,are accelerating R&D programs and forming strategic alliances to broaden their co‑packaged product portfolios. Collaborative efforts focus on expanding module density, standardizing interfaces, and ensuring compatibility with emerging 5G and future 6G transport networks. These partnerships shorten time‑to‑market for advanced optics solutions and create a competitive ecosystem that drives continuous innovation across Co-Packaged Optics (CPO) market.

Emerging Applications Beyond Traditional Data Centers

Beyond core data‑center deployments, Co-Packaged Optics (CPO) market is witnessing adoption in edge computing nodes and telecom backhaul where space constraints and power efficiency are critical. Operators targeting low‑latency services leverage co‑packaged modules to extend high‑speed connectivity to remote sites without the overhead of separate transceiver and driver components. This trend broadens the addressable market and reinforces the technology’s relevance across the full spectrum of network architecture, from core to edge.

COMPETITIVE LANDSCAPE

Key Industry Players

Co-Packaged Optics (CPO) Market Competitive Overview

Intel remains the market’s most visible anchor in Co‑Packaged Optics, leveraging its integrated silicon photonics roadmap and deep relationships with hyperscale data‑center operators. By co‑packaging ASIC drivers with optical transceivers, Intel has established a modular design that supports 400 Gbps and higher lane counts, positioning it as a de‑facto standard‑setter. Broadcom and Cisco augment this structure; Broadcom supplies high‑bandwidth PHY IP and driver ASICs, while Cisco, via its acquisition of Acacia Communications, contributes advanced coherent optical modules. This triad creates a tiered supply chain where fabless semiconductor leaders partner with established optical component manufacturers, driving a consolidated yet competitive ecosystem that is attracting sizable R&D investment.

Beyond the leading trio, a suite of niche innovators is expanding the CPO value chain. Lumentum and II‑VI Incorporated offer high‑performance laser engines and silicon photonic integration platforms that feed into custom co‑packaged solutions. Ciena and Juniper Networks focus on carrier‑grade transport, deploying CPO modules in 5G and metro‑edge networks. European players such as ADVA Optical Networking and Fujitsu deliver ultra‑low‑latency modules for financial trading and high‑frequency data paths. Asian manufacturers Nokia, Huawei and Marvell Technology (including the former Inphi portfolio) are accelerating development of CPO silicon for both data‑center and telecom back‑haul, diversifying the market and fostering regional competition.

List of Key Co-Packaged Optics Companies Profiled

- Intel

- Broadcom

- Cisco

- Lumentum

- II-VI Incorporated

- Ciena

- Juniper Networks

- ADVA Optical Networking

- Fujitsu

- Nokia

- Huawei

- Marvell Technology

- Inphi (now part of Marvell)

- Mellanox (NVIDIA)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Electrical Co‑Packaged Optics is emerging as the leading segment because it leverages mature driver ASIC ecosystems and offers a smoother transition for manufacturers. • Provides a reliable path for legacy transceiver designs to adopt co‑packaging without extensive redesign of photonic components. • Enables rapid time‑to‑market for data‑center modules where power efficiency and signal integrity are paramount. • Facilitates incremental cost reductions through reuse of established silicon‑based driver platforms. |

| By Application |

|

Data Center Interconnect dominates as the primary application driver. • Hyperscale operators demand ultra‑high bandwidth links that co‑packaged optics can deliver while curbing power budgets. • The elimination of traditional electrical‑optic interfaces simplifies board layout, supporting higher lane counts essential for next‑generation server fabrics. • Growing adoption of modular data‑center architectures aligns with the compact form factor of CPO solutions. |

| By End User |

|

Hyperscale Cloud Providers are the leading end‑user segment. • Their relentless drive for bandwidth, combined with aggressive power‑efficiency targets, makes CPO a strategic enabler. • Large‑scale deployments allow economies of scale that accelerate product refinement and ecosystem maturity. • Integration of CPO into spine‑leaf architectures simplifies network planning and reduces overall system complexity. |

| By Integration Architecture |

|

Hybrid Integration currently leads the architecture landscape. • Balances the design flexibility of modular components with the performance gains of tighter co‑packaging. • Allows vendors to adopt proven driver ASICs while integrating emerging photonic modules, facilitating a smoother technology transition. • Supports a broad portfolio of form factors, catering to both data‑center and telecom equipment manufacturers. |

| By Performance Tier |

|

400 Gbps and above is the dominant performance tier driving market momentum. • Enables next‑generation data‑center fabrics and 5G/6G backhaul links that demand ultra‑high data rates. • The co‑packaged approach mitigates signal degradation at such speeds, delivering superior eye‑diagram performance. • Early adoption by leading cloud operators creates a virtuous cycle of innovation and ecosystem investment. |

Regional Analysis: North America

The medical device sector is a major consumer of Co-Packaged Optics, utilizing them in endoscopes, surgical microscopes, and diagnostic imaging systems. The stringent quality requirements and the need for high precision in these applications drive demand for specialized CPO solutions. Innovation in minimally invasive surgery and advanced diagnostic techniques are further propelling the growth of this segment.

Industrial applications, including quality control and automation, rely heavily on CPO for vision systems. These systems are used for defect detection, product sorting, and dimensional measurements. The increasing need for automated inspection processes across various industries contributes to the steady demand for CPO. Advancements in machine learning and artificial intelligence are further enhancing the capabilities of these systems, driving demand for high-performance optical components.

Scientific research and development across academia and industry utilize CPO in areas like spectroscopy, microscopy, and laser technology. The demand is driven by ongoing advancements in scientific exploration and the pursuit of deeper understanding in various fields. The need for highly specialized and precisely manufactured CPO caters to the unique requirements of scientific instruments.

While a smaller segment currently, the telecommunications sector is showing increasing interest in CPO for applications in fiber optic communication and optical sensing. The drive for higher bandwidth and more efficient data transmission is fueling exploration of CPO in this area. The development of advanced optical modules and transceivers is contributing to this nascent market segment.

Europe

Europe presents a significant market for Co-Packaged Optics, driven by a strong foundation in advanced manufacturing and a thriving research sector. Germany, the United Kingdom, and France are key contributors to the demand. The automotive industry’s increasing reliance on advanced driver-assistance systems (ADAS) and autonomous driving technologies is fueling demand for CPO in sensors and imaging systems. The medical device market in Europe also presents substantial opportunities for CPO, particularly in areas like minimally invasive surgery and diagnostic imaging. Stringent regulatory requirements and a focus on sustainability are influencing the development and adoption of CPO solutions in the region. The European market is characterized by a strong emphasis on innovation and collaboration between research institutions and industry players. The growth of the industrial automation sector further contributes to the demand for CPO in inspection systems and machine vision applications.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing market for Co-Packaged Optics, particularly driven by China and Japan. The rapid expansion of the electronics industry, the increasing adoption of advanced manufacturing techniques, and government investments in research and development are key factors contributing to this growth. The demand for CPO in smartphones, consumer electronics, and industrial automation is robust. The burgeoning medical device market in China presents significant opportunities for CPO suppliers. The region is witnessing a shift towards localized manufacturing and a growing emphasis on cost-effectiveness, influencing the types of CPO solutions being adopted. The development of sophisticated optical systems for telecommunications and 5G infrastructure is also driving demand in the Asia-Pacific region.

South America

South America represents a relatively smaller but steadily growing market for Co-Packaged Optics. Brazil and Argentina are the primary contributors to demand, driven by the expansion of industries like mining, agriculture, and manufacturing. The mining sector’s increasing use of advanced imaging systems for ore exploration and processing is a key driver of demand. The agricultural sector is utilizing CPO in precision farming applications, such as crop monitoring and yield optimization. The relatively nascent medical device market in the region presents long-term growth potential. Increasing investments in infrastructure development are also contributing to the demand for CPO in various sectors.

Middle East & Africa

The Middle East & Africa region exhibits moderate but promising growth potential for Co-Packaged Optics. The oil and gas sector in the Middle East is a significant consumer of CPO for inspection and monitoring applications. The increasing focus on infrastructure development and urbanization across the region is driving demand for CPO in construction, transportation, and security systems. The growing healthcare sector in some African countries presents opportunities for CPO in medical imaging and diagnostics. Government initiatives aimed at diversifying economies and promoting technological advancement are also contributing to the growth of the CPO market in the region.

Report Scope

This market research report provides a comprehensive analysis of the Co-Packaged Optics (CPO) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Co-Packaged Optics (CPO) Market?

-> Co-Packaged Optics (CPO) market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 4.12 billion by 2034.

Which key companies operate Co-Packaged Optics (CPO) market?

-> Key players include Intel, Broadcom, Cisco, and Acacia Communications, among others.

What are the key growth drivers?

-> Key growth drivers include hyperscale data‑center expansion, rollout of 5G/6G networks, and the increasing demand for higher bandwidth and energy‑efficient optical solutions.

Which region dominates the market?

-> Asia‑Pacific is emerging as the fastest‑growing region, while North America remains a dominant market due to early adoption of advanced data‑center technologies.

What are the emerging trends?

-> Emerging trends include integration of AI/IoT for intelligent optical modules, higher lane‑count architectures (e.g., 400 Gbps and beyond), and the development of silicon‑photonic co‑packaged solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...