CMOS temperature sensor with calibration-free BJT-based front-end Market Insights

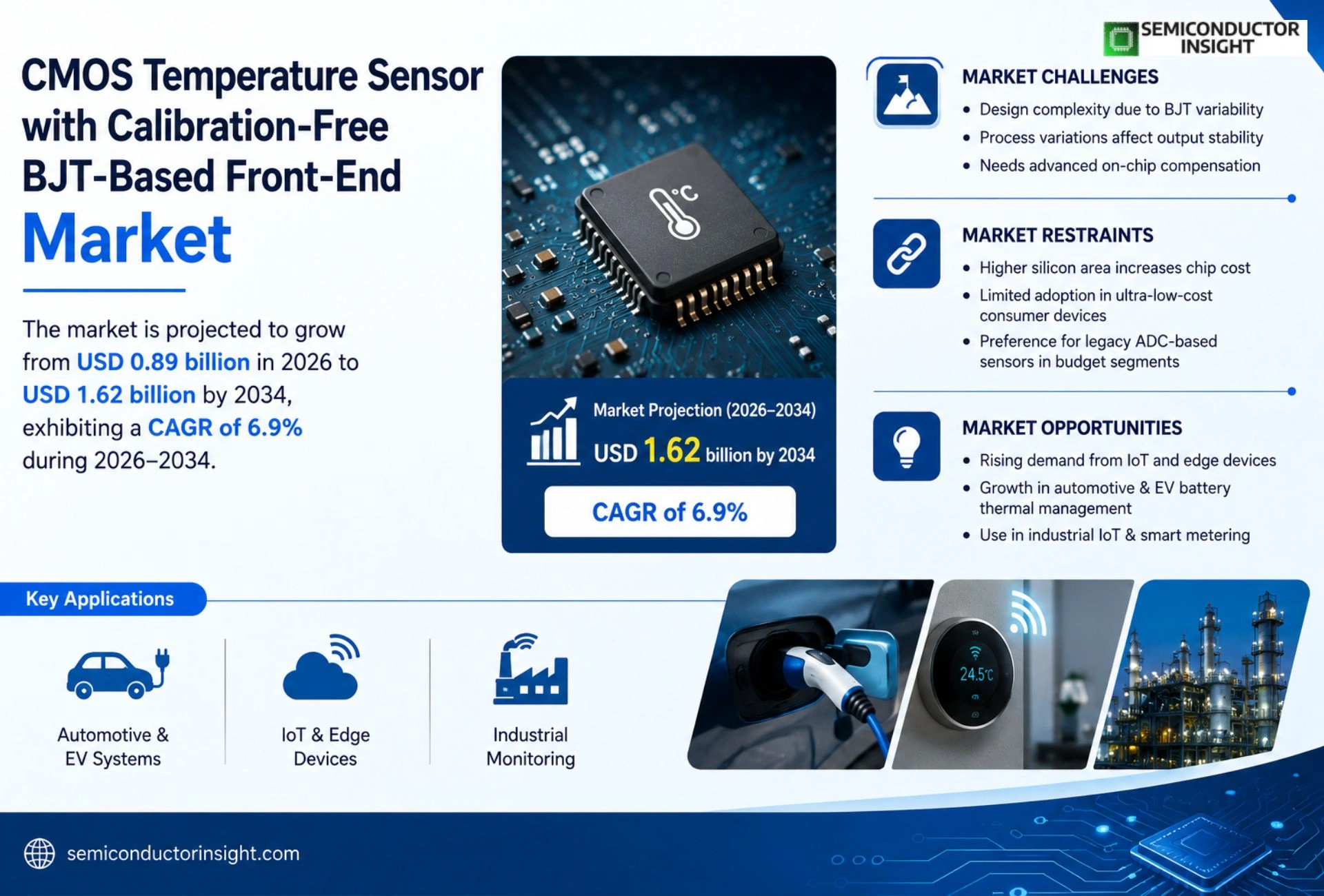

Global CMOS temperature sensor with calibration‑free BJT‑based front‑end market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.89 billion in 2026 to USD 1.62 billion by 2034, exhibiting a CAGR of 6.9% during the forecast period.

CMOS temperature sensors integrate a bipolar junction transistor (BJT) front‑end that provides an intrinsic curvature‑free response without external calibration. This architecture enables high accuracy (<±0.5 °C), low power consumption, and seamless integration into System‑on‑Chip platforms for automotive, IoT, and industrial applications.

The market is accelerating because demand for precise thermal management in electric vehicles and edge AI devices is rising, while advances in silicon scaling reduce cost. Key players such as Texas Instruments, Analog Devices, STMicroelectronics, and Infineon are expanding portfolios through recent releases of self‑calibrating CMOS temperature sensors.

MARKET DRIVERS

Increasing Demand for High‑Precision Temperature Monitoring

The rise of smart factories and autonomous vehicles is driving a surge in demand for CMOS temperature sensor with calibration‑free BJT‑based front‑end Market solutions that can deliver sub‑0.1 °C accuracy across a wide temperature range. Industry analysts estimate that device shipments will grow at a compound annual growth rate of roughly 9 % through 2028, fueled by stricter thermal management standards.

Advancements in Calibration‑Free BJT Front‑End Architecture

Recent innovations in on‑chip BJT biasing eliminate the need for external calibration circuitry, reducing board space and power consumption. This architectural breakthrough shortens time‑to‑market for OEMs and lowers total cost of ownership, making the technology attractive for mass‑produced consumer electronics.

➤ Integrated calibration reduces BOM cost by up to 15 % while improving long‑term stability in harsh environments.

Overall, the combination of regulatory pressure, performance gains, and cost efficiencies creates a robust growth engine for CMOS temperature sensor with calibration‑free BJT‑based front‑end Market.

MARKET CHALLENGES

Design Complexity and Process Variability

Designing a reliable calibration‑free front‑end requires precise modeling of BJT characteristics across process corners. Variability in silicon parameters can lead to drift in sensor output, necessitating sophisticated on‑chip compensation algorithms that increase design effort.

Other Challenges

Manufacturing Yield Sensitivity

Yield losses may arise if BJT‑based bias networks are not tightly controlled during wafer fabrication, potentially raising unit costs and limiting adoption in price‑sensitive segments.

MARKET RESTRAINTS

Cost Sensitivity in High‑Volume Consumer Segments

While performance advantages are clear, the incremental silicon area required for the BJT front‑end can increase per‑chip cost. For ultra‑low‑cost wearables, manufacturers often favor legacy ADC‑based temperature sensors, constraining market penetration of the calibration‑free solution.

MARKET OPPORTUNITIES

Emerging IoT and Edge‑Computing Applications

Edge devices that process data locally require highly accurate temperature measurements to maintain sensor fidelity and system reliability. The calibration‑free nature of the CMOS sensor simplifies integration, opening opportunities in smart meters, environmental monitoring stations, and industrial IoT gateways.

Furthermore, the automotive industry’s move toward electrification and battery management systems creates a niche where precise thermal profiling is critical. Deploying these sensors can enhance safety margins and extend battery life, presenting a lucrative avenue for market participants.

CMOS temperature sensor with calibration-free BJT-based front-end Market Trends

Growing Adoption in Edge‑AI Devices

The increasing need for precise thermal monitoring in compact edge‑AI modules is reshaping CMOS temperature sensor with calibration-free BJT-based front-end Market. System‑on‑chip designs now favor integrated BJT front‑ends because they eliminate external calibration loops, reducing component count and board space. This simplification aligns with the broader industry push toward lower power budgets and higher reliability in applications such as autonomous sensors, wearable health monitors, and industrial robotics. As manufacturers prioritize design‑for‑manufacturability, the calibration‑free architecture is becoming a default choice for new product generations.

Other Trends

Shift Toward Sustainable Manufacturing

Environmental regulations and corporate sustainability goals are encouraging suppliers to adopt processes that minimize waste and energy consumption. The calibration‑free nature of the BJT‑based front‑end reduces the need for post‑fabrication trimming steps, directly supporting greener production cycles. Companies are also leveraging silicon‑on‑insulator (SOI) technologies to further improve thermal isolation, which enhances sensor accuracy while meeting stricter eco‑design standards. This trend is especially pronounced in European and North American markets where compliance frameworks are most rigorous.

Expansion in Automotive Safety Systems

Automotive safety platforms are integrating these sensors to monitor battery packs, power electronics, and cabin climate systems. The inherent linearity of the BJT front‑end enables seamless integration with vehicle‑wide temperature management algorithms, improving fault detection speed. OEMs are also capitalizing on the reduced calibration effort to shorten development cycles for next‑generation electric vehicles. This accelerates time‑to‑market for safety‑critical components while maintaining the high reliability demanded by automotive standards.

COMPETITIVE LANDSCAPE

Key Industry Players

CMOS Temperature Sensor Market Competitive Overview

CMOS temperature sensor market with a calibration‑free BJT‑based front‑end is dominated by a handful of large analog‑mixed‑signal specialists that leverage deep silicon‑on‑insulator (SOI) expertise and extensive automotive and industrial portfolios. Texas Instruments continues to lead the segment, offering a broad family of precision temperature monitors that benefit from its vast global distribution network and proven silicon foundry relationships. Analog Devices follows closely, integrating BJT‑enabled curvature‑free sensing into its high‑performance sensor suites, which are increasingly adopted in automotive power‑train control and data‑center thermal management. Both firms exploit economies of scale to maintain competitive pricing while delivering sub‑0.1 °C accuracy, reinforcing a market structure that favors well‑capitalized incumbents capable of sustaining R&D investment and multi‑year product roadmaps.

Beyond the tier‑one leaders, a diverse set of niche players contributes specialized IP and region‑focused solutions. NXP Semiconductors and Infineon Technologies have introduced BJT‑front‑end sensors targeting automotive safety and renewable‑energy applications, respectively. STMicroelectronics, Microchip Technology, and Renesas Electronics provide mid‑range offerings that balance cost and performance for consumer‑grade IoT devices. Smaller innovators such as Melexis, ROHM, AMS AG, Silicon Labs, and Samsung Electronics bring differentiated form‑factors or integration with MEMS platforms, expanding the competitive landscape and creating opportunities for design‑win differentiation in emerging markets.

List of Key CMOS Temperature Sensor Companies Profiled

- Texas Instruments

- Analog Devices

- NXP Semiconductors

- Infineon Technologies

- STMicroelectronics

- Microchip Technology

- Renesas Electronics

- ON Semiconductor

- Melexis

- ROHM Semiconductor

- AMS AG

- Silicon Labs

- Samsung Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Analog‑Dominant Types are favored for their intrinsic low‑noise characteristics and the ability to preserve the curvature‑free response of the BJT front‑end.

|

| By Application |

|

Automotive Power Management emerges as the leading application due to the stringent thermal safety requirements of modern electric and hybrid vehicles.

|

| By End User |

|

Design Engineers drive adoption by valuing the simplicity of a calibration‑free solution.

|

| By Integration Level |

|

Package‑Level Integration is gaining traction because it consolidates the sensor and signal conditioning within a single footprint.

|

| By Market Drivers |

|

Regulatory Accuracy Demands shape product roadmaps across multiple verticals.

|

Regional Analysis: CMOS temperature sensor with calibration-free BJT-based front-end Market

North America

Strong automotive electrification programs and growing demand for precise thermal management in data centers are accelerating adoption. OEMs value calibration‑free sensors for faster time‑to‑market, while manufacturers appreciate the reduced bill‑of‑materials, reinforcing a virtuous cycle of investment and deployment.

Harmonized safety and emissions standards across the United States and Canada create a predictable compliance pathway. Agencies encourage low‑power, high‑accuracy solutions, which aligns well with the capabilities of calibration‑free BJT‑based front‑ends, smoothing certification processes.

Leading semiconductor firms are expanding product portfolios through strategic acquisitions and joint development agreements. Emphasis on modular sensor platforms and software‑defined calibration tools further differentiates offerings in a competitive landscape.

University research clusters in the Midwest and West Coast are pioneering novel BJT architectures that enhance temperature linearity. These collaborations accelerate technology transfer, positioning North America as an innovation epicenter for the market.

Europe

Europe’s CMOS temperature sensor with calibration‑free BJT‑based front‑end Market is shaped by stringent energy‑efficiency directives and a strong emphasis on Industry 4.0. Automotive manufacturers in Germany and France are integrating these sensors to meet emissions targets, while industrial players appreciate the reduced calibration overhead in complex machinery. Collaborative EU research programs fund next‑generation BJT designs, fostering cross‑border knowledge sharing. Although market growth is moderate compared with North America, the region’s focus on sustainability and robust standards continues to drive steady adoption across aerospace and medical device segments.

Asia‑Pacific

The Asia‑Pacific region exhibits rapid expansion of CMOS temperature sensor with calibration‑free BJT‑based front‑end Market, propelled by burgeoning electronics manufacturing hubs in China, South Korea, and Taiwan. High‑volume consumer electronics and aggressive smart‑city initiatives create demand for compact, low‑power temperature monitoring solutions. Local semiconductor firms are scaling production capacity while leveraging cost‑effective fabs, enabling competitive pricing. Government incentives for advanced sensor technologies further stimulate R&D, positioning the region as a fast‑growing market despite occasional supply‑chain volatility.

South America

South America’s market activity is centered around Brazil’s growing automotive sector and emerging renewable‑energy projects. Companies are attracted to calibration‑free sensors for their simplified integration and reduced maintenance needs in harsh operating environments. While overall market size remains modest, regional trade agreements and increasing investments in semiconductor assembly are unlocking new opportunities for local manufacturers to serve both domestic and export markets.

Middle East & Africa

In the Middle East & Africa, CMOS temperature sensor with calibration‑free BJT‑based front‑end Market is driven by expanding oil‑&‑gas infrastructure and rising demand for reliable thermal monitoring in remote installations. Countries such as the United Arab Emirates are investing in smart‑grid initiatives that require accurate temperature data for efficiency optimization. Although adoption is nascent, partnerships with global OEMs and targeted training programs are laying the groundwork for future growth across the region.

Report Scope

This market research report provides a comprehensive analysis of the CMOS temperature sensor with calibration-free BJT-based front-end Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of CMOS temperature sensor with calibration-free BJT-based front-end Market?

-> CMOS temperature sensor with calibration‑free BJT‑based front‑end market size is projected to grow from USD 0.89 billion in 2026 to USD 1.62 billion by 2034, exhibiting a CAGR of 6.9%

Which key companies operate in CMOS temperature sensor with calibration-free BJT-based front-end Market?

-> Key players include Texas Instruments, Analog Devices, STMicroelectronics, and Infineon, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for precise thermal management in electric vehicles and edge AI devices, advances in silicon scaling reducing cost, and the need for high‑accuracy low‑power sensors in automotive, IoT, and industrial applications.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include self‑calibrating CMOS temperature sensors, deeper integration into System‑on‑Chip platforms, and expanded use in electric vehicle thermal management and edge AI workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...