CMOS image sensor column-parallel ADC with digital CDS Market Insights

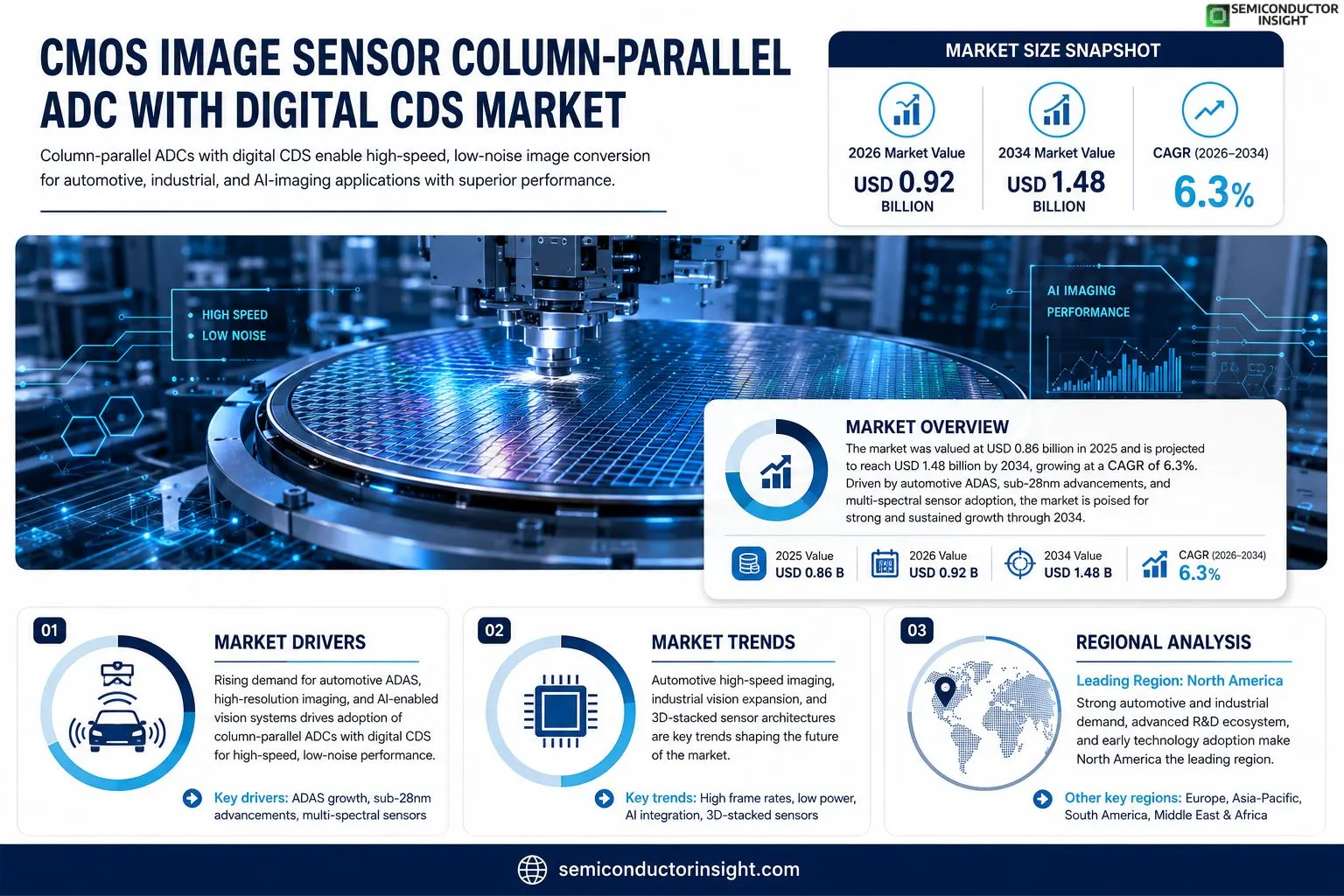

CMOS image sensor column‑parallel ADC with digital CDS market size was valued at USD 0.86 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.48 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Column‑parallel analog‑to‑digital converters (ADCs) integrated on CMOS image sensors enable simultaneous conversion of pixel outputs, while digital correlated double sampling (CDS) suppresses fixed‑pattern noise and improves signal‑to‑noise ratio. This architecture is essential for high‑speed automotive cameras, industrial vision systems, and emerging AI‑enabled imaging applications.The market is experiencing rapid growth because automotive driver‑assistance systems demand higher frame rates and lower power consumption, prompting manufacturers to adopt column‑parallel ADCs with digital CDS. Furthermore, advances in semiconductor process nodes below 28 nm are reducing pixel pitch constraints, while increasing adoption of multi‑spectral sensors fuels demand. Key players such as Sony Semiconductor Solutions, Samsung Electronics, OmniVision Technologies, and ON Semiconductor are accelerating development through strategic partnerships and new product launches.

MARKET DRIVERS

Increasing Adoption in Automotive ADAS

CMOS image sensor column-parallel ADC with digital CDS Market is being propelled by the surge in advanced driver‑assistance systems, where low‑noise, high‑speed conversion is critical for real‑time image processing. Automakers are integrating higher‑resolution cameras to meet safety regulations, creating a steady demand for column‑parallel architectures.

Growth of High‑Resolution Mobile Imaging

Smartphone manufacturers are targeting sensor formats above 1 µm pixel size, which requires efficient on‑chip analog‑to‑digital conversion. Column‑parallel ADCs with digital correlated double sampling (CDS) reduce power consumption while preserving image quality, making them attractive for next‑generation mobile devices.

➤ Industry analysts note that the convergence of automotive safety standards and consumer demand for superior imaging is the primary catalyst for market expansion.

In addition, the rise of edge‑AI vision modules in industrial automation leverages the fast, low‑latency output of column‑parallel ADCs, further broadening the addressable market base.

MARKET CHALLENGES

Manufacturing Complexity and Yield

Implementing column‑parallel ADC arrays requires precise layout and matching of numerous analog components on a single die, increasing process variability. Yield losses during wafer fabrication can elevate unit costs, slowing adoption among price‑sensitive OEMs.

Other Challenges

Supply Chain Constraints

The limited number of foundries capable of advanced mixed‑signal CMOS processes creates bottlenecks, especially when demand spikes for automotive grade parts with stringent reliability criteria.Furthermore, the need for rigorous qualification testing under automotive temperature cycles adds to development timelines, posing a barrier for smaller suppliers.

MARKET RESTRAINTS

Cost Sensitivity in Consumer Segments

While performance advantages are clear, the incremental cost of integrating column‑parallel ADCs with digital CDS can be prohibitive for mass‑market devices where price points are fiercely competitive.Moreover, established CMOS sensor designs that use shared‑column ADCs remain entrenched, requiring compelling ROI arguments to justify redesign.Regulatory compliance costs for automotive safety standards also act as a restraint, as manufacturers must allocate additional resources for certification.

MARKET OPPORTUNITIES

Emergence of 3D‑Stacked Sensor Architectures

3D‑stacked image sensors present a natural platform for integrating column‑parallel ADCs directly beneath the photodiode layer, unlocking higher fill‑factor and reduced parasitics. This architectural shift creates a fertile opportunity for suppliers to differentiate their offerings.The expanding ecosystem of machine‑vision applications, including robotics and smart surveillance, demands high‑speed, low‑noise conversion that column‑parallel ADCs uniquely provide, signaling untapped growth potential.

CMOS image sensor column-parallel ADC with digital CDS Market Trends

Automotive and High‑Speed Imaging Growth

CMOS image sensor column‑parallel ADC with digital CDS Market was valued at USD 0.86 billion in 2025. Forecasts indicate a rise to USD 0.92 billion in 2026 and a projection of USD 1.48 billion by 2034, reflecting a compound annual growth rate of approximately 6.3 % over the forecast horizon. This expansion is driven primarily by the escalating demand for advanced driver‑assistance systems (ADAS) and autonomous‑vehicle cameras that require higher frame rates, lower latency, and reduced power consumption. Concurrently, industrial vision and AI‑enabled imaging solutions are adopting column‑parallel ADC architectures to meet tighter performance specifications while maintaining cost efficiency.

Other Trends

Advancements in Process Nodes and Multi‑Spectral Sensors

Semiconductor process nodes below 28 nm are now enabling smaller pixel pitches without sacrificing conversion accuracy, which directly benefits column‑parallel ADC integration. The finer geometry reduces parasitic capacitance, improving signal‑to‑noise ratio when paired with digital correlated double sampling (CDS). Moreover, the emergence of multi‑spectral CMOS sensorscapturing visible, infrared, and short‑wave infrared bands on a single chipcreates a new demand vector for ADCs capable of handling diverse data streams simultaneously. These technological strides are expanding the addressable market beyond automotive into security, agriculture, and consumer electronics where high‑resolution, low‑noise imaging is critical.

Competitive Landscape and Strategic Partnerships

Key industry players such as Sony Semiconductor Solutions, Samsung Electronics, OmniVision Technologies, and ON Semiconductor are intensifying R&D investments and forging alliances to accelerate product rollouts. Recent collaborations focus on integrating next‑generation column‑parallel ADCs with on‑chip digital CDS into flagship image sensor families, targeting both mass‑market automotive platforms and premium industrial cameras. These partnerships are complemented by accelerated silicon‑photonic packaging techniques that further diminish power draw while preserving high frame‑rate capabilities. As the market matures, differentiation will hinge on the ability to deliver scalable, low‑cost solutions that satisfy the rigorous reliability standards demanded by safety‑critical applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of CMOS Image Sensor Column‑Parallel ADC with Digital CDS Market

Sony Semiconductor Solutions remains the dominant force in the column‑parallel ADC with digital CDS segment, leveraging its advanced 0.9 µm BSI‑CMOS platform and extensive automotive‑grade sensor portfolio. Sony’s ability to co‑integrate high‑speed ADCs and digital CDS on a single chip has created a defensible moat that underpins most high‑frame‑rate automotive camera modules. Samsung Electronics follows closely, differentiating through aggressive scaling to sub‑28 nm processes and offering vertically integrated sensor‑to‑system‑on‑chip solutions that attract tier‑1 automotive OEMs. OmniVision Technologies, now part of a larger imaging conglomerate, competes by delivering cost‑effective multi‑spectral sensors with embedded column‑parallel ADCs, targeting consumer‑grade and emerging AI‑vision markets. The overall market structure resembles an oligopoly where these three firms capture the majority of revenue, while each pursues strategic partnershipssuch as Sony’s collaboration with automotive chipset makers and Samsung’s joint development with tier‑1 suppliersto expand ecosystem lock‑in.Beyond the headline leaders, a cadre of niche players enriches the competitive landscape. ON Semiconductor focuses on power‑efficient automotive sensors, embedding digital CDS to meet stringent noise requirements. STMicroelectronics leverages its analog expertise to supply customized ADC front‑ends for industrial vision systems. Canon and Panasonic continue to nurture specialty sensor lines for medical imaging and high‑resolution machine vision. Sharp and Toshiba contribute legacy expertise in large‑format sensors, increasingly integrating column‑parallel conversion for high‑speed inspection. Himax and GalaxyCore add depth to the market with compact, low‑power solutions for IoT and wearables, while PixArt Imaging and Hamamatsu Photonics target niche scientific and biophotonic applications. These companies, although smaller in scale, provide critical diversification and foster innovation across automotive, industrial, and emerging AI‑enabled imaging domains.

List of Key CMOS Image Sensor Column‑Parallel ADC with Digital CDS Companies Profiled

- Sony Semiconductor Solutions

- Samsung Electronics

- OmniVision Technologies

- ON Semiconductor

- STMicroelectronics

- Canon Inc.

- Panasonic Corporation

- Sharp Corporation

- Toshiba Electronic Devices & Storage

- Himax Technologies

- GalaxyCore Inc.

- PixArt Imaging

- Hamamatsu Photonics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Analog Front‑End Integrated

|

| By Application |

|

Automotive ADAS

|

| By End User |

|

OEM Camera Module Manufacturers

|

| By Technology |

|

Sub‑28nm Process Nodes

|

| By Market Trend |

|

Demand for Higher Frame Rates

|

Regional Analysis: CMOS image sensor column-parallel ADC with digital CDS Market

North America

The convergence of high‑speed imaging and AI processing fuels demand for column‑parallel ADC architectures that deliver low latency and superior signal integrity, positioning North America as a catalyst for rapid adoption.

Expanding automotive ADAS functions and the rise of 8K video capture create fertile ground for advanced digital CDS techniques, opening new revenue streams for key players.

High development costs and the need for tight integration with emerging process nodes present barriers that require collaborative R&D investments to overcome.

A handful of leading semiconductor firms dominate, yet start‑ups focused on niche imaging niches intensify competition, driving continuous innovation.

Europe

Europe exhibits a balanced mix of mature automotive OEMs and emerging consumer electronics manufacturers, fostering steady demand for CMOS image sensor column‑parallel ADC with digital CDS Market. Collaborative research programs across Germany, France, and the Netherlands aid in refining low‑noise ADC designs that meet stringent automotive safety standards. While the market pace is slightly slower than North America, strong regulatory frameworks and a focus on sustainability encourage adoption of energy‑efficient sensor solutions, positioning Europe as a significant contributor to growth.

Asia‑Pacific

Asia‑Pacific, anchored by high‑volume manufacturing hubs in China, South Korea, and Taiwan, drives scale economies for CMOS image sensor column‑parallel ADC with digital CDS Market. The region’s emphasis on cost‑effective production aligns with the rapid expansion of mobile device markets and smart city initiatives. While technological leadership is evolving, partnerships between local foundries and multinational design houses accelerate the integration of advanced digital CDS techniques, enhancing overall market dynamism across the Asia‑Pacific landscape.

South America

South America presents emerging opportunities as automotive and consumer electronics sectors modernize. Growing interest in advanced driver‑assist systems and high‑definition surveillance applications stimulates demand for sophisticated sensor architectures. Regional manufacturers are beginning to collaborate with suppliers, leveraging CMOS image sensor column‑parallel ADC with digital CDS Market’s performance benefits to differentiate their product offerings in a competitive environment.

Middle East & Africa

Middle East & Africa remain nascent but promising markets for CMOS image sensor column‑parallel ADC with digital CDS Market, driven by increasing investments in smart infrastructure and defense imaging projects. While overall market size is modest, strategic initiatives to adopt cutting‑edge sensor technologies in security and autonomous systems are laying the groundwork for future growth, positioning the region as an up‑and‑coming participant in the landscape.

Report Scope

This market research report provides a comprehensive analysis of the CMOS image sensor column-parallel ADC with digital CDS Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of CMOS image sensor column-parallel ADC with digital CDS Market?

-> CMOS image sensor column-parallel ADC with digital CDS Market was valued at USD 0.86 billion in 2025 and is expected to reach USD 1.48 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Which key companies operate in CMOS image sensor column-parallel ADC with digital CDS Market?

-> Key players include Sony Semiconductor Solutions, Samsung Electronics, OmniVision Technologies, and ON Semiconductor, among others.

What are the key growth drivers?

-> Key growth drivers include automotive driver‑assistance systems demanding higher frame rates and lower power consumption, advances in semiconductor process nodes below 28 nm, and growing adoption of multi‑spectral sensors for AI‑enabled imaging applications.

Which region dominates the market?

-> market presence is widespread, with strong demand across automotive and industrial sectors worldwide.

What are the emerging trends?

-> Emerging trends include high‑speed automotive camera integration, industrial vision system expansion, and AI‑enabled imaging solutions leveraging column‑parallel ADC architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...