Class-AB output stage with adaptive biasing for audio line drivers Market Insights

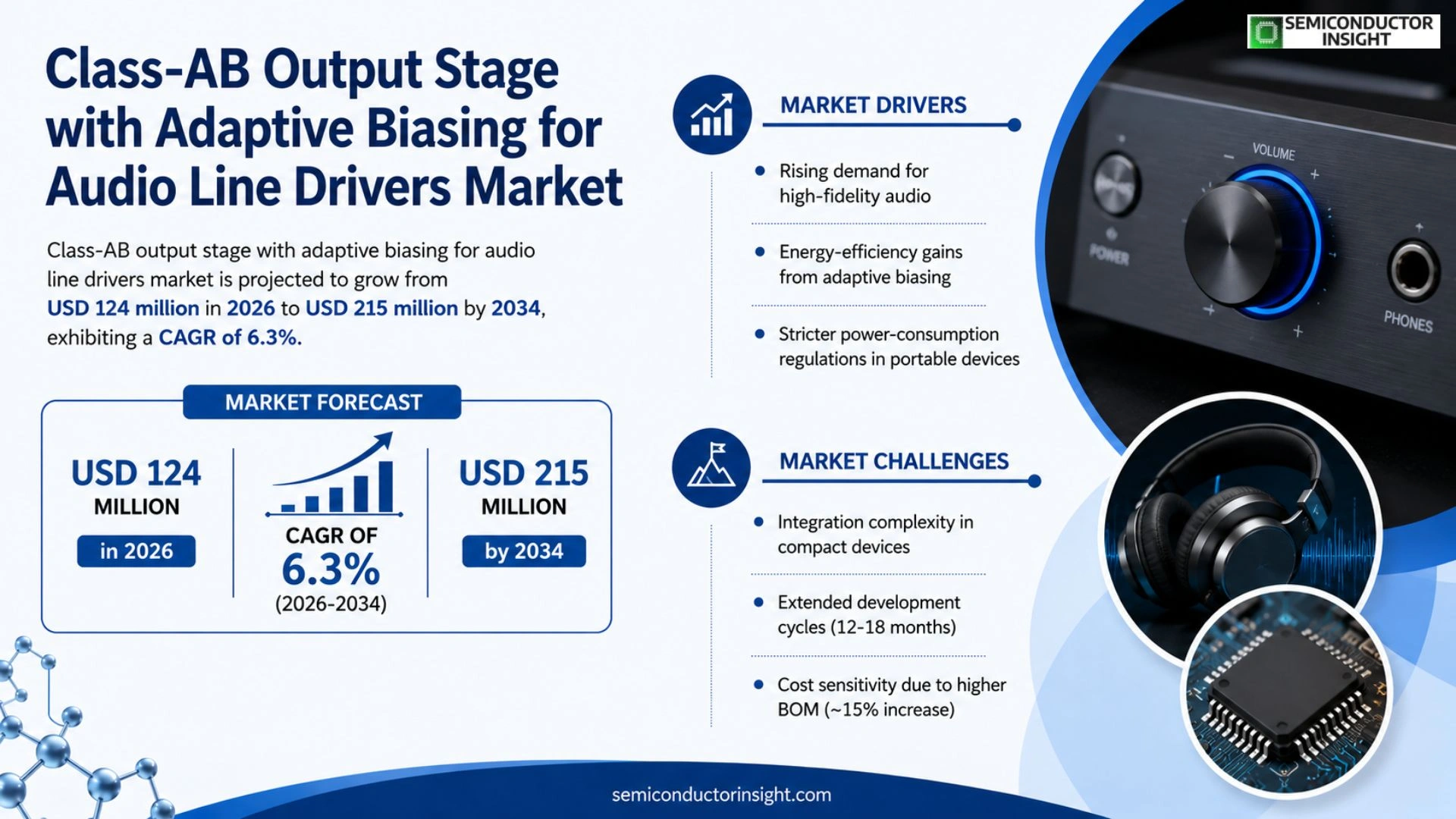

Global Class‑AB output stage with adaptive biasing for audio line drivers market size was valued at USD 118 million in 2025. The market is projected to grow from USD 124 million in 2026 to USD 215 million by 2034, exhibiting a CAGR of 6.3% during the forecast period.

This technology combines the low‑distortion characteristics of Class‑AB operation with an adaptive bias circuit that continuously optimises quiescent current based on signal dynamics. By automatically adjusting bias, the stage maintains high linearity while reducing power consumption, making it ideal for professional audio mixers, studio monitors, and high‑fidelity consumer equipment.

The market is gaining momentum because manufacturers seek solutions that balance audio fidelity, efficiency, and thermal management. Furthermore, the rise of portable high‑resolution audio devices and stricter energy‑efficiency standards are driving adoption. Key players such as Texas Instruments, Analog Devices, STMicroelectronics, and NXP Semiconductors are expanding their portfolios with integrated adaptive‑bias modules, reinforcing growth prospects.

MARKET DRIVERS

Rising Demand for High‑Fidelity Audio

The global push toward premium sound experiences in consumer electronics has accelerated adoption of Class-AB output stage with adaptive biasing for audio line drivers Market. Revenue from premium headphones and high‑end home audio systems is projected to grow at a compound annual rate of 7‑8% through 2030, creating a robust demand pipeline for energy‑efficient line‑driver technologies.

Energy‑Efficiency Gains from Adaptive Biasing

Adaptive biasing allows Class‑AB stages to maintain linearity while reducing idle‑current draw by up to 30 %. This efficiency advantage aligns with stricter power‑consumption regulations in portable devices, prompting manufacturers to preferentially select adaptive‑bias solutions.

➤ “Adaptive biasing delivers the acoustic performance of Class‑AB while cutting power consumption, a decisive factor for next‑generation audio platforms.”

Combined, higher audio expectations and tighter energy budgets are the twin engines driving Class‑AB output stage with adaptive biasing for audio line drivers Market toward sustained expansion.

MARKET CHALLENGES

Integration Complexity in Compact Devices

Designers must balance the thermal constraints of densely packed smartphones with the bias‑adjustment circuitry required for adaptive operation. This integration challenge can extend development cycles by 12‑18 months, limiting rapid product launches.

Other Challenges

Cost Sensitivity

The additional analog control loops increase bill‑of‑materials by roughly 15 %, a cost premium that can deter price‑sensitive OEMs, especially in emerging markets.

MARKET RESTRAINTS

High Component Cost

Precision bias‑generation ICs and low‑noise feedback networks required for adaptive Class‑AB stages remain more expensive than conventional fixed‑bias alternatives. The elevated component cost restricts adoption in low‑margin consumer segments, thereby tempering market momentum.

MARKET OPPORTUNITIES

Growth in Automotive Audio Systems

Automakers are integrating high‑definition soundbars and voice‑assistants into vehicle cabins, demanding line drivers that deliver both power efficiency and low distortion. Forecasts suggest a 9 % CAGR for adaptive‑bias Class‑AB solutions in the automotive sector, presenting a lucrative expansion avenue for Class‑AB output stage with adaptive biasing for audio line drivers Market.

Class-AB output stage with adaptive biasing for audio line drivers Market Trends

Increasing Adoption Driven by Energy‑Efficiency Standards

Class-AB output stage with adaptive biasing for audio line drivers Market is experiencing a notable shift as manufacturers prioritize power‑saving designs without compromising sonic fidelity. Adaptive bias circuitry continuously matches quiescent current to signal dynamics, which means the stage delivers low distortion while consuming less energy during silence or low‑level passages. This capability aligns with stricter energy‑efficiency regulations that are being adopted across consumer electronics and professional audio equipment. As a result, design engineers are integrating these adaptive modules into portable high‑resolution players, studio monitors, and mixed‑signal audio mixers to achieve both thermal stability and extended battery life.

Other Trends

Integration with System‑on‑Chip (SoC) Platforms

Chip manufacturers are embedding adaptive bias functionality directly into SoC architectures, reducing board count and simplifying layout requirements. Texas Instruments, Analog Devices, STMicroelectronics, and NXP Semiconductors have announced next‑generation audio families that feature built‑in adaptive bias blocks. This integration accelerates time‑to‑market for OEMs and supports the trend toward highly integrated audio front‑ends in compact devices.

Growth of High‑Fidelity Portable Audio

The surge in demand for high‑fidelity portable audio devices is another catalyst for the market. Listeners expect studio‑grade clarity from earbuds and compact speakers, and the adaptive bias approach helps manufacturers meet those expectations by delivering consistent linearity across a wide dynamic range while keeping power draw low. Consequently, product roadmaps increasingly list adaptive‑bias Class‑AB stages as a differentiating feature for premium audio lines.

COMPETITIVE LANDSCAPE

Key Industry Players

Class‑AB Output Stage with Adaptive Biasing for Audio Line Drivers – Competitive Overview

The market is dominated by a handful of large semiconductor firms that leverage extensive analog‑mixed‑signal portfolios to integrate adaptive‑bias modules with Class‑AB output stages. Texas Instruments leads the space with its OPA series and dedicated audio driver families that combine low distortion with power‑saving bias control, positioning the company as a preferred supplier for professional mixers and high‑fidelity consumer devices. Analog Devices follows closely, offering high‑performance SigmaDSP‑based audio processors that embed adaptive bias circuits, while STMicroelectronics and NXP Semiconductors provide highly integrated System‑in‑Package (SiP) solutions targeting portable high‑resolution audio equipment. These incumbents benefit from deep relationships with OEMs, robust supply chains, and aggressive roadmap investment, establishing a tier‑1 market structure that shapes product specifications and pricing dynamics across the forecast horizon.

Beyond the tier‑1 tier, a diverse set of niche and emerging players enriches the competitive landscape with specialized analog front‑ends and ASICs. Maxim Integrated (now part of Analog Devices) continues to ship low‑noise bias‑controlled drivers for boutique studio gear, whereas Infineon Technologies and ROHM Semiconductor focus on automotive‑grade audio modules that meet stringent thermal and reliability standards. ON Semiconductor, Cirrus Logic, and Renesas Electronics target consumer‑grade headphone amplifiers, delivering compact solutions with integrated adaptive bias. Marvell, Toshiba, Qualcomm, Microchip Technology, and Cypress Semiconductor (Infineon) round out the ecosystem, offering custom‑design services and fabless innovations that address niche applications such as portable DACs, Bluetooth audio peripherals, and next‑generation hearing‑aid platforms.

List of Key Class‑AB Output Stage with Adaptive Biasing for Audio Line Drivers Companies Profiled

- Texas Instruments

- Analog Devices

- STMicroelectronics

- NXP Semiconductors

- Maxim Integrated

- Infineon Technologies

- ROHM Semiconductor

- ON Semiconductor

- Cirrus Logic

- Renesas Electronics

- Marvell Technology

- Toshiba

- Qualcomm

- Microchip Technology

- Cypress Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Adaptive‑Bias Class‑AB

|

| By Application |

|

High‑Fidelity Home Audio

|

| By End User |

|

Audio Equipment Manufacturers

|

| By Technology |

|

Integrated Adaptive‑Bias ICs

|

| By Market Driver |

|

Energy‑Efficiency Regulations

|

Regional Analysis: Class-AB output stage with adaptive biasing for audio line drivers Market

North America

Environmental directives and energy‑efficiency standards in key markets encourage the shift toward adaptive biasing solutions. Compliance frameworks such as IEC 62368‑1 promote designs that minimize hazardous emissions, positioning Class‑AB output stage as a preferred technology for compliant audio products.

Advances in semiconductor processes enable tighter integration of bias‑control loops, delivering faster response times and lower distortion. Emerging 28‑nm and 14‑nm CMOS nodes allow designers to embed adaptive algorithms directly within driver chips, unlocking new performance thresholds.

Major players differentiate through proprietary adaptive circuits and extensive verification suites. Strategic acquisitions of niche analog firms enhance portfolio breadth, while collaborations with audio hardware manufacturers accelerate time‑to‑market for next‑generation driver solutions.

Europe

Europe’s audio ecosystem, characterized by a strong tradition in music production and broadcast engineering, is rapidly embracing adaptive biasing to meet stringent EU energy‑efficiency directives. Leading semiconductor firms are establishing joint development centers with premier automotive and consumer‑electronics manufacturers, fostering co‑innovation of Class‑AB output stage solutions tailored for compact, high‑performance devices. The market benefits from a dense network of research institutions that contribute advanced bias‑control algorithms, positioning Europe as a hotbed for next‑generation acoustic technologies. Anticipated growth is driven by expanding demand for premium in‑car entertainment systems and immersive virtual‑reality audio platforms across the region.

Asia‑Pacific

Asia‑Pacific exhibits strong momentum as manufacturers seek cost‑effective, high‑performance audio drivers for a booming consumer electronics market. Rapid adoption of smart speakers, wearable audio, and 5G‑enabled mobile devices increases the relevance of adaptive biasing, which balances performance with thermal constraints. Regional design houses are leveraging the extensive foundry capacity in China, Taiwan, and South Korea to produce finely tuned Class‑AB stages that cater to diverse application requirements. The outlook remains upbeat, with regional OEMs prioritizing integration of adaptive biasing to differentiate products in increasingly competitive markets.

South America

In South America, growing investments in broadcast infrastructure and live‑event production create a niche for high‑quality audio amplification. While the overall market size remains modest, the need for reliable, low‑power driver solutions drives interest in adaptive biasing techniques that extend device longevity in varied climatic conditions. Local manufacturers are forming alliances with North American technology partners to import advanced Class‑AB designs, gradually building indigenous expertise and fostering a nascent ecosystem focused on premium audio experiences.

Middle East & Africa

The Middle East & Africa region presents emerging opportunities as smart‑city initiatives and upscale hospitality projects integrate sophisticated audio systems. Adaptive biasing’s ability to maintain audio integrity in high‑temperature environments aligns well with regional climate challenges. Early adopters, particularly in the United Arab Emirates and South Africa, are partnering with global semiconductor leaders to pilot Class‑AB output stage solutions that combine efficiency with high fidelity, laying groundwork for broader market penetration over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the Class-AB output stage with adaptive biasing for audio line drivers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Class-AB output stage with adaptive biasing for audio line drivers Market?

-> Class‑AB output stage with adaptive biasing for audio line drivers market is projected to grow from USD 124 million in 2026 to USD 215 million by 2034.

Which key companies operate in Class-AB output stage with adaptive biasing for audio line drivers Market?

-> Key players include Texas Instruments, Analog Devices, STMicroelectronics, and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include audio fidelity demands, power‑efficiency requirements, thermal‑management challenges, and the rising adoption of portable high‑resolution audio devices alongside stricter energy‑efficiency standards.

Which region dominates the market?

-> Regional insights indicate strong demand across North America, Europe, and Asia‑Pacific, with all three regions contributing significantly to market growth.

What are the emerging trends?

-> Emerging trends include integration of adaptive‑bias modules into next‑generation audio chips, adoption of AI‑enhanced audio processing, and increased focus on semiconductor designs that optimise both performance and power consumption.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...