MARKET INSIGHTS

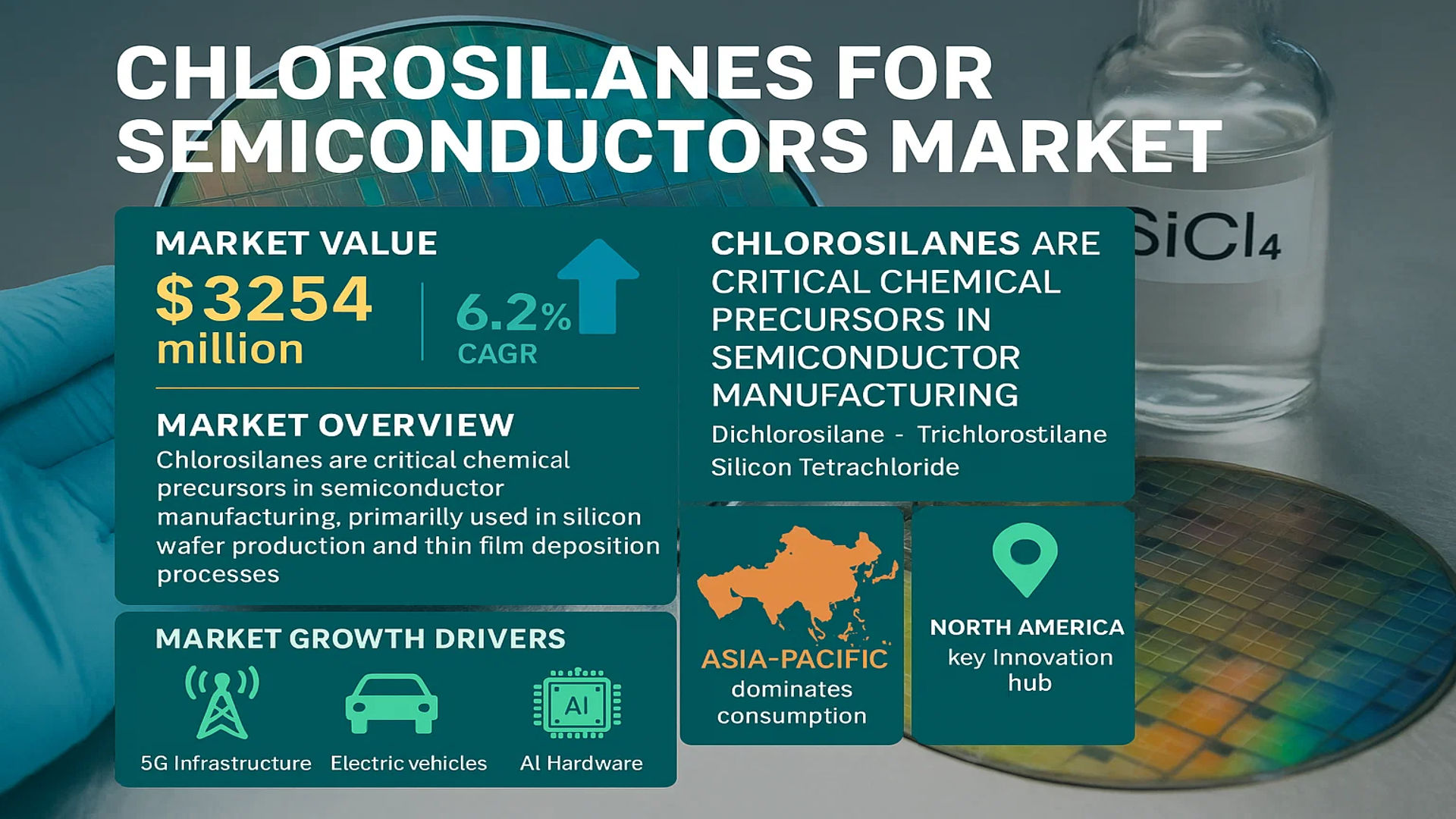

The global Chlorosilanes for Semiconductors Market was valued at 3254 million in 2024 and is projected to reach US$ 5013 million by 2032, at a CAGR of 6.2% during the forecast period.

Chlorosilanes are critical chemical precursors in semiconductor manufacturing, primarily used in silicon wafer production and thin film deposition processes. These compounds, including dichlorosilane, trichlorosilane, and silicon tetrachloride, serve as key raw materials for high-purity polysilicon – the foundational material for integrated circuits and photovoltaic cells. The Asia-Pacific region dominates consumption due to concentrated semiconductor fabrication facilities, while North America remains a key innovation hub for advanced manufacturing techniques.

Market growth is driven by expanding 5G infrastructure, electric vehicle adoption, and AI hardware demands, which collectively require advanced semiconductor components. However, supply chain volatility and stringent environmental regulations pose challenges. Recent industry developments include capacity expansions by major players like Wacker Chemie and OCI Company, who collectively hold over 35% market share. The dichlorosilane segment is projected to grow at 7.1% CAGR through 2032, favored for its efficiency in epitaxial silicon deposition processes.

MARKET DYNAMICS

MARKET DRIVERS

Growing Semiconductor Industry to Fuel Chlorosilanes Demand

The global semiconductor industry’s rapid expansion is driving significant growth in the chlorosilanes market. With semiconductor revenues projected to exceed $500 billion in 2024, manufacturers are scaling up production capacities, creating substantial demand for high-purity chlorosilanes used in wafer processing and thin film deposition. These specialty chemicals are critical for producing polysilicon, which forms the foundation of semiconductor devices. The increasing adoption of advanced chip architectures requiring more complex manufacturing processes is further accelerating consumption. Major semiconductor fabrication plants being constructed worldwide will require stable chlorosilane supply chains to maintain production schedules.

Technological Advancements in Semiconductor Manufacturing Create New Applications

Emerging semiconductor technologies are creating novel applications for chlorosilanes across the manufacturing process. The transition to smaller node sizes below 5nm requires ultra-pure materials with precise chemical properties that only specialized chlorosilane formulations can provide. Industry adoption of 3D NAND flash memory and FinFET transistors has increased demand for high-quality silicon precursors. Additionally, the development of new deposition techniques such as atomic layer deposition (ALD) is opening opportunities for chlorosilane derivatives in advanced packaging solutions. These technical requirements are pushing manufacturers to develop customized formulations that meet stringent purity standards while improving process efficiency.

The shift toward compound semiconductors is presenting additional growth avenues. While silicon remains dominant, gallium nitride and silicon carbide technologies require specialized chlorosilane precursors for epitaxial growth processes. This diversification in semiconductor materials is broadening the application scope for chlorosilane products across different device types.

MARKET RESTRAINTS

Stringent Safety Regulations and Handling Challenges Limit Market Expansion

Chlorosilanes’ highly reactive nature creates significant barriers to market growth. These chemicals require specialized handling procedures and storage infrastructure due to their flammability and tendency to react violently with moisture. Regulatory agencies worldwide have implemented strict transportation and workplace exposure limits that increase operational costs for manufacturers and end-users. Many fabrication facilities are reluctant to stock large quantities due to safety concerns, forcing just-in-time delivery models that strain supply chains. Compliance with evolving environmental regulations regarding emissions and waste disposal adds further complexity to production and usage.

Supply chain vulnerabilities present another constraint. Chlorosilanes cannot be easily substituted in semiconductor manufacturing, yet their hazardous nature limits transportation options and creates geographic dependencies. Many semiconductor fabs cluster near production facilities to mitigate supply risks, restricting market access in regions without local manufacturing capabilities. Recent disruptions in global logistics networks have highlighted the fragility of these supply chains, causing some manufacturers to reevaluate their reliance on these critical but challenging materials.

MARKET CHALLENGES

High Production Costs and Energy Intensive Processes Challenge Profitability

The energy-intensive manufacturing process for high-purity chlorosilanes creates significant cost pressures. Producing semiconductor-grade materials requires multiple purification steps and sophisticated quality control measures that dramatically increase production expenses. Rising energy costs in key producing regions have compressed profit margins, with some facilities operating at minimal profitability despite strong demand. The capital expenditure required for new production capacity can exceed $100 million for a single plant, creating substantial barriers to market entry and expansion.

Other Challenges

Raw Material Volatility

Chlorosilane production depends on consistent supplies of metallurgical-grade silicon and chlorine, both subject to price fluctuations influenced by broader industrial demand. Recent supply constraints in the silicon market have created unpredictable pricing scenarios that complicate long-term planning for chlorosilane producers.

Technical Complexity

Developing formulations that meet evolving semiconductor process requirements demands significant R&D investment. The time required to qualify new materials with chip manufacturers can span multiple years, delaying returns on development costs. Many producers struggle to maintain the technical expertise needed to keep pace with advancing semiconductor technologies while managing operational performance.

MARKET OPPORTUNITIES

Expansion in Emerging Semiconductor Markets to Create Growth Potential

Government initiatives to build domestic semiconductor capabilities in several countries present significant opportunities for chlorosilane suppliers. Major investment programs in semiconductor manufacturing across Asia, North America, and Europe will require localized supply chains for critical materials. Established producers can leverage their technical expertise to form strategic partnerships with new fabrication facilities. The development of specialty chemical industrial parks adjacent to semiconductor clusters creates possibilities for integrated supply solutions that reduce transportation risks while improving responsiveness to customer needs.

Innovations in chlorosilane formulations also offer promising prospects. Manufacturers developing next-generation products with improved deposition characteristics and reduced environmental impact can capture premium pricing opportunities. The transition to more sustainable semiconductor manufacturing processes is driving demand for chlorosilane alternatives that maintain performance while reducing hazardous byproducts. Producers investing in these advanced material solutions position themselves favorably within an industry increasingly focused on environmental responsibility.

Vertical integration strategies present additional growth avenues. Several leading producers are expanding into downstream polysilicon production to capture more value from their chlorosilane operations. This approach provides greater supply chain stability while allowing companies to benefit from growth across multiple semiconductor material segments. Such strategic expansions help mitigate cyclical demand patterns in the semiconductor industry.

CHLOROSILANES FOR SEMICONDUCTORS MARKET TRENDS

Growing Demand for Advanced Semiconductors Drives Chlorosilanes Adoption

The global semiconductor industry is experiencing unprecedented growth, with chlorosilanes playing a pivotal role as key precursors in silicon wafer production and thin film deposition processes. The market for chlorosilanes in semiconductor applications is projected to grow at a robust CAGR of 6.2% from 2024 to 2032, reaching a valuation of US$ 5,013 million by 2032. This growth is largely fueled by the surging demand for high-performance computing, 5G infrastructure, and Internet of Things (IoT) devices, all of which require advanced semiconductor components. Dichlorosilane, a critical chlorosilane variant, is expected to demonstrate particularly strong growth due to its superior purity levels and efficiency in silicon deposition processes.

Other Trends

Technological Advancements in Semiconductor Manufacturing

The push towards smaller node sizes in semiconductor fabrication is driving innovation in chlorosilane formulations. Manufacturers are investing in ultra-high purity variants to meet the stringent requirements of sub-7nm chip production, which demands contamination levels below 1 part per billion. This technological race is particularly evident in foundries across Asia, where companies are scaling up production of trichlorosilane and silicon tetrachloride for advanced etching applications. These developments are reshaping the competitive landscape, with key players enhancing their R&D expenditures by an estimated 8-12% annually to maintain technological leadership.

Supply Chain Diversification and Regional Market Growth

The semiconductor industry’s strategic shift towards supply chain resilience is influencing chlorosilane market dynamics. While China currently accounts for approximately 35% of global consumption, other regions are rapidly building capacity to reduce dependency. North America and Europe are witnessing significant investments in local chlorosilane production facilities, supported by government incentives for semiconductor independence. This geographical diversification is creating new market opportunities while simultaneously addressing concerns about raw material security in the semiconductor value chain. The U.S. market is projected to maintain steady growth, supported by increasing fab construction activities and technological leadership in advanced packaging solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Capacity Expansion and Technological Advancements

The global chlorosilanes for semiconductors market features a mix of established chemical manufacturers and specialized silicon material providers. Wacker Chemie AG dominates the industry with vertically integrated operations spanning from silicon metal production to high-purity chlorosilanes, accounting for approximately 18% of global capacity in 2024.

OCI Company and Tokuyama Corporation follow closely, leveraging their expertise in ultra-high purity chemical manufacturing to serve leading semiconductor foundries. These players have been actively expanding production capabilities in Asia to meet growing demand from chip manufacturers.

The market remains dynamic, with mid-size players like Hemlock Semiconductor and SK Specialty gaining traction through strategic partnerships with equipment manufacturers. Recent developments include long-term supply agreements with semiconductor firms, ensuring stable demand channels.

Emerging Chinese suppliers such as XinAn Chemical Industrial and Sunfar Silicon are making significant inroads, supported by government initiatives in domestic semiconductor production. These companies are rapidly upgrading purification technologies to meet stringent semiconductor-grade requirements.

List of Key Chlorosilanes for Semiconductors Companies Profiled

- Wacker Chemie AG (Germany)

- OCI Company (South Korea)

- Tokuyama Corporation (Japan)

- Hemlock Semiconductor (U.S.)

- SK Specialty (South Korea)

- REC Silicon (Norway)

- Evonik Industries (Germany)

- Sunfar Silicon (China)

- XinAn Chemical Industrial (China)

- Yingde Sai Electronics (China)

- China Silicon Corporation (China)

- Hubei Heyuan Gas (China)

While European and Japanese manufacturers continue to lead in technology innovation, Chinese players are closing the gap through accelerated R&D investments. The competitive intensity is further heightened by the industry’s transition to larger wafer sizes and more advanced nodes, requiring even higher purity levels. Market participants are responding through both organic capacity expansions and strategic collaborations across the semiconductor value chain.

Segment Analysis:

By Type

Dichlorosilane Segment Leads Due to High Demand in Silicon Wafer Manufacturing

The market is segmented based on type into:

- Dichlorosilane

- Trichlorosilane

- Silicon Tetrachloride

- Hexachlorodisilane

- Others

By Application

Silicon Wafer Preparation Dominates the Market Due to Rising Semiconductor Production

The market is segmented based on application into:

- Silicon Wafer Preparation

- Thin Film Deposition

- Etching Process

- Others

By End User

Semiconductor Manufacturers Hold the Largest Share in the Market

The market is segmented based on end user into:

- Semiconductor Device Manufacturers

- Foundries

- IDMs (Integrated Device Manufacturers)

- Research Institutions

Regional Analysis: Chlorosilanes for Semiconductors Market

Asia-Pacific

The Asia-Pacific region dominates the global Chlorosilanes for Semiconductors market, accounting for the largest share in both volume and revenue. Led by semiconductor manufacturing hubs like China, Japan, South Korea, and Taiwan, the region benefits from established supply chains, high-tech infrastructure investments, and government support for semiconductor self-sufficiency. China alone is projected to contribute over 40% of the global demand by 2032, driven by its Made in China 2025 initiative and rapid expansion of domestic semiconductor fabs. Dichlorosilane remains the most sought-after product type due to its critical role in silicon wafer preparation. However, environmental regulations in countries like Japan are accelerating the shift toward high-purity, low-emission variants.

North America

The U.S. is a key innovator in the Chlorosilanes for Semiconductors market, with strong demand from leading semiconductor companies such as Intel and Texas Instruments. Stricter environmental protocols under the U.S. EPA and hefty investments in domestic chip production (e.g., the CHIPS and Science Act’s $52 billion funding) are driving advancements in high-grade chlorosilanes. Canada and Mexico are emerging as secondary markets, leveraging trade agreements to supply raw materials to U.S. manufacturers. While trichlorosilane dominates for thin-film deposition applications, suppliers are increasingly focusing on sustainable production methods to comply with regional carbon-neutral targets.

Europe

Europe maintains a strong foothold in the market, particularly in Germany and the Nordic countries, owing to their advanced materials science sector and investments in next-gen semiconductor technologies like silicon carbide (SiC). Compliance with EU REACH regulations has led to higher purity standards, favoring specialized producers like Wacker and Evonik. The region also emphasizes circular economy practices, with recycling initiatives for silicon tetrachloride byproducts gaining traction. Nevertheless, high production costs and reliance on imports for some intermediates remain challenges.

South America

Chlorosilanes adoption in South America is still in early stages, with limited local semiconductor production. Brazil and Argentina are exploring partnerships with global players to develop niche applications, but the market is hindered by infrastructure gaps and volatile economic conditions. Most demand stems from imported electronics manufacturing, though rising interest in renewable energy (e.g., solar panels using silicon wafers) could spur gradual growth.

Middle East & Africa

The region shows nascent potential, primarily in Saudi Arabia and the UAE, where diversification from oil-driven economies is fostering investments in tech sectors. While current chlorosilanes consumption is minimal, planned semiconductor hubs (e.g., NEOM in Saudi Arabia) may create opportunities. A lack of local expertise and dependency on imports for high-purity materials presently restrict market expansion.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Chlorosilanes for Semiconductors markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Chlorosilanes for Semiconductors market was valued at USD 3,254 million in 2024 and is projected to reach USD 5,013 million by 2032, at a CAGR of 6.2% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Dichlorosilane, Trichlorosilane, Silicon Tetrachloride, Hexachlorodisilane, Others) and application (Silicon Wafer Preparation, Thin Film Deposition, Etching Process, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is expected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants including Wacker, KCC, Hemlock, OCI, Tokuyama, SK Specialty, REC, SunEdision, Evonik, and Sunfar Silicon, among others. In 2024, the global top five players held a significant market share.

- Technology Trends & Innovation: Assessment of emerging semiconductor fabrication techniques and evolving industry standards in chlorosilane applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges such as supply chain constraints and regulatory issues.

- Stakeholder Analysis: Strategic insights for chemical suppliers, semiconductor manufacturers, investors, and policymakers.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Chlorosilanes for Semiconductors Market?

-> Chlorosilanes for Semiconductors Market was valued at 3254 million in 2024 and is projected to reach US$ 5013 million by 2032, at a CAGR of 6.2% during the forecast period.

Which key companies operate in Global Chlorosilanes for Semiconductors Market?

-> Key players include Wacker, KCC, Hemlock, OCI, Tokuyama, SK Specialty, REC, SunEdision, Evonik, and Sunfar Silicon, among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor demand, expansion of electronics manufacturing, and advancements in semiconductor fabrication technologies.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, driven by semiconductor manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of high-purity chlorosilanes, integration of AI in semiconductor manufacturing, and sustainable production methods.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...