Chiplets for molecular dynamics simulation accelerator Market Insights

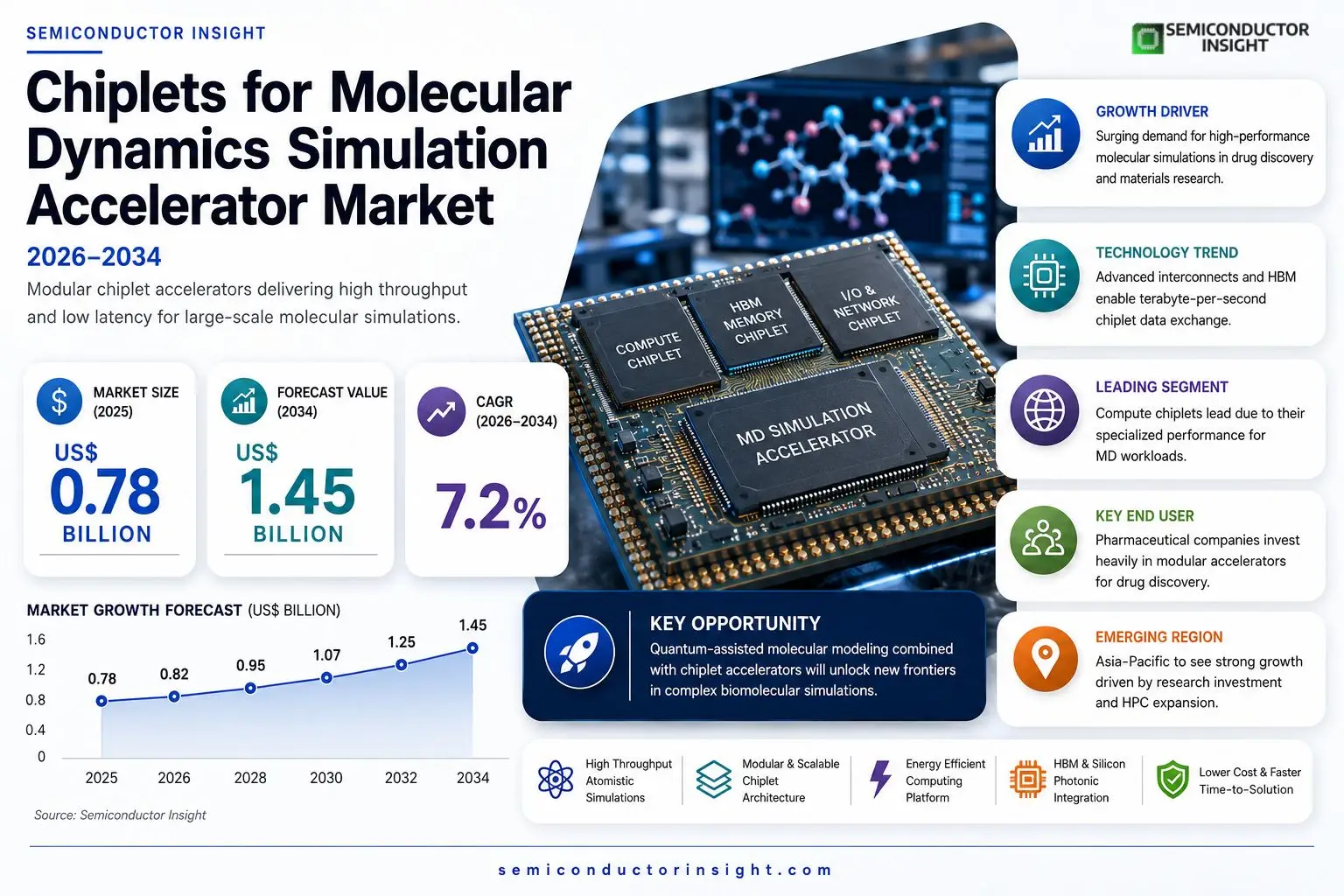

Chiplets for molecular dynamics simulation accelerator market size was valued at USD 0.78 billion in 2025. The market is projected to grow from USD 0.82 billion in 2025 to USD 1.45 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period.

Chiplets are modular silicon building blocks that can be heterogeneously integrated using advanced interconnect technologies such as EMIB or fan‑out wafer‑level packaging. By assembling specialized compute, memory and networking die, chiplet‑based accelerators deliver the high throughput and low latency required for large‑scale molecular dynamics simulations used in drug discovery and materials research.The market is accelerating because pharmaceutical firms are investing heavily in AI‑driven drug design, while academic supercomputing centers seek energy‑efficient solutions for atomistic modeling. Furthermore, breakthroughs in silicon photonics and high‑bandwidth memory enable chiplet architectures to outperform monolithic GPUs on specific workloads. Leading playersincluding Intel, AMD (via Xilinx), TSMC and NXPare launching dedicated MD‑simulation chiplet families, and strategic collaborations such as the Intel‑IBM joint development announced in March 2024 are expected to further expand adoption.

MARKET DRIVERS

Increasing Demand for High‑Performance Molecular Simulations

Chiplets for molecular dynamics simulation accelerator Market is being propelled by the surge in drug discovery and materials science projects that require sub‑nanosecond simulation cycles. Researchers are moving away from monolithic ASICs toward modular chiplet architectures that deliver greater scalability and lower time‑to‑solution.

Advancements in 3D‑Integration and Interconnect Technologies

Recent breakthroughs in silicon‑photonic interposers and high‑bandwidth memory interfaces enable Chiplets to exchange data at terabyte‑per‑second rates, directly enhancing the throughput of molecular dynamics workloads. This technical edge is driving early adoption among leading supercomputing centers.

➤ Analysts estimate that modular chiplet solutions could reduce system‑level cost by up to 25 % compared with traditional monolithic designs.

Combined with growing government funding for computational chemistry, these drivers are positioning the market for a robust expansion trajectory over the next decade.

MARKET CHALLENGES

Design Complexity and Integration Overheads

Integrating heterogeneous Chiplets requires sophisticated design tools and verification flows. Companies lacking mature ecosystem support face longer time‑to‑market, which can erode the cost advantage of modular solutions.

Other Challenges

Supply Chain Fragmentation

The reliance on multiple foundries for different chiplet components introduces variability in lead times and yield, complicating volume production for large‑scale accelerators.

MARKET RESTRAINTS

High Initial Capital Expenditure

Deploying a chiplet‑based accelerator platform often entails significant upfront investment in custom interposer fabrication and validation infrastructure. Many mid‑size research institutions view this expense as a barrier to entry, limiting broader market penetration.

MARKET OPPORTUNITIES

Emerging Applications in Quantum‑Assisted Molecular Modeling

The convergence of quantum computing techniques with chiplet accelerators opens new pathways for simulating complex biomolecular interactions. Early collaborations between semiconductor firms and quantum hardware providers suggest a lucrative niche that could accelerate market growth well beyond current forecasts.

Chiplets for molecular dynamics simulation accelerator Market Trends

Accelerated Adoption Fueled by Pharma and Academia

Recent years have seen a marked acceleration in the adoption of chiplet‑based accelerators for molecular dynamics simulations. Pharmaceutical companies, seeking to shorten drug‑discovery cycles, are investing heavily in AI‑augmented simulation pipelines that demand high‑throughput, low‑latency compute. At the same time, university supercomputing centers are prioritizing energy‑efficient architectures that can handle atomistic modeling workloads without the power penalties of traditional monolithic GPUs. The modular nature of Chiplets allows designers to combine compute, memory, and networking die in proportions that match specific scientific workloads, reducing both development cost and time‑to‑market. This convergence of forces creates a sustained demand for flexible silicon building blocks that can be rapidly reconfigured as research priorities evolve.

Other Trends

Advanced Interconnect Technologies Enable Higher Bandwidth

Emerging interconnect solutions such as embedded multi‑die interconnect bridges (EMIB) and fan‑out wafer‑level packaging are unlocking bandwidth levels previously unattainable in heterogeneous integration. By linking compute, memory, and networking die with sub‑nanosecond latency, chiplet architectures can sustain the data‑intensive kernels typical of large‑scale molecular dynamics. This technical advantage is prompting early adopters to replace legacy GPU clusters with custom chiplet clusters that achieve comparable performance while reducing overall system footprint. Moreover, the scalability of these interconnects supports future expansions, allowing additional die to be added without redesigning the entire substrate.

Strategic Partnerships Expand the Chiplet Ecosystem

Leading semiconductor vendors, including Intel, AMD (through Xilinx), TSMC, and NXP, have announced dedicated development roadmaps for molecular dynamics acceleration. Collaborative programs, such as the joint effort launched in early 2024 between Intel and IBM, are delivering reference designs that integrate silicon photonics and high‑bandwidth memory into a unified chiplet package. These alliances accelerate time‑to‑market for end users and foster a broader ecosystem of third‑party IP providers, software toolchains, and validation suites, reinforcing the market’s momentum. In addition, ecosystem partners are contributing optimized compilers and libraries that translate molecular dynamics workloads directly onto chiplet topologies, further lowering the barrier for researchers to adopt this technology.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Chiplets for Molecular Dynamics Simulation Accelerators

The market is dominated by a handful of silicon giants that have leveraged advanced interconnect technologies such as EMIB and fan‑out wafer‑level packaging to create dedicated MD‑simulation chiplet families. Intel leads with its Xeon‑based accelerator platform, partnering with IBM on a joint road‑map announced in March 2024 to integrate high‑bandwidth memory and silicon photonics. AMD, through its Xilinx acquisition, offers programmable chiplet solutions that combine compute and networking dies for flexible workload scaling. TSMC provides the foundry backbone, delivering heterogeneous integration services that enable both monolithic and chiplet‑based designs. NXP contributes specialized I/O and sensor interface Chiplets that support low‑latency data ingestion from lab‑scale instrumentation. Collectively, these leaders shape a market structure where vertical integration and strategic alliances accelerate time‑to‑market for high‑performance molecular dynamics accelerators, driving the projected CAGR of 7.2 % through 2034.Beyond the primary tier, a growing cohort of niche innovators is expanding the ecosystem with differentiated architectures. Graphcore’s IPU‑centric Chiplets focus on graph‑based molecular simulations, while Cerebras offers wafer‑scale chiplet assemblies that deliver unprecedented memory bandwidth. Qualcomm is adapting its Snapdragon AI chiplet portfolio for scientific workloads, and Samsung’s advanced packaging unit supplies high‑density interposers for hybrid memory cubes. Marvell, Broadcom, and Arm contribute networking and interface Chiplets that enable seamless scale‑out across supercomputing clusters. Synopsys offers design‑for‑chiplet IP, Foundries provides specialty process nodes, and Alibaba’s Pingtouge (Xuantie) introduces cost‑effective RISC‑V based compute Chiplets for emerging markets. These players enrich the competitive landscape by targeting specific performance, power‑efficiency, or cost niches within the molecular dynamics simulation accelerator domain.

List of Key Chiplets for Molecular Dynamics Simulation Accelerator Companies Profiled

- Intel

- AMD (Xilinx)

- TSMC

- NXP

- IBM

- Graphcore

- Cerebras

- Qualcomm

- Samsung

- Marvell

- Broadcom

- Arm

- Synopsys

- Foundries

- Alibaba Pingtouge (Xuantie)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Compute Chiplets

|

| By Application |

|

Drug Discovery

|

| By End User |

|

Pharmaceutical Companies

|

| By Integration Technology |

|

EMIB

|

| By Market Driver |

|

AI‑Driven Molecular Design

|

Regional Analysis: North America

North America

The United States leads the North American market, spearheaded by advancements from prominent semiconductor companies and academic institutions. Strong government initiatives promoting scientific research are also contributing to the growth of Chiplets for molecular dynamics simulation accelerator Market. Focus on high-performance computing centers is a key driver.

Canada presents a growing opportunity, benefiting from close collaboration with the US and a skilled workforce in the technology sector. Investments in advanced manufacturing and research are fostering a supportive environment for Chiplets for molecular dynamics simulation accelerator Market development. The country’s strengths in computational science are particularly relevant.

Mexico is experiencing rising interest in advanced technology and is positioned as an attractive location for manufacturing and research related to Chiplets for molecular dynamics simulation accelerator Market. Lower labor costs and proximity to the US market are key advantages.

While currently a smaller market, South America is beginning to explore the potential of Chiplets for molecular dynamics simulation accelerator Market, particularly in areas like pharmaceutical research. Growth is anticipated as the region’s scientific capabilities develop.

Europe

Europe is demonstrating steady growth in Chiplets for molecular dynamics simulation accelerator Market, driven by strong research funding and a concentration of leading universities and research institutions. Germany, the UK, and France are key markets, with a focus on applications in drug discovery and materials design. The region’s commitment to sustainable technologies also provides an avenue for growth as computational modeling aids in materials innovation.

Asia-Pacific

Asia-Pacific is poised for substantial expansion in Chiplets for molecular dynamics simulation accelerator Market. Countries like China, Japan, and South Korea are investing heavily in semiconductor technology and high-performance computing. The increasing demand for personalized medicine and advanced materials is fueling the need for faster and more accurate simulations. Government support and strategic partnerships are accelerating market development within this dynamic region.

South America

South America represents an emerging market for Chiplets for molecular dynamics simulation accelerator Market. The region’s growing investment in scientific research and development, particularly in biotechnology and agriculture, is creating demand for advanced computational tools. While adoption is currently limited, the potential for future growth is significant.

Middle East & Africa

The Middle East & Africa region is an early-stage market for Chiplets for molecular dynamics simulation accelerator Market. Increased investment in healthcare and scientific research, coupled with government initiatives to promote technological advancement, are expected to drive future growth. The demand is currently concentrated in specialized research institutions and pharmaceutical companies.

Report Scope

This market research report provides a comprehensive analysis of the Chiplets for molecular dynamics simulation accelerator Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chiplets for molecular dynamics simulation accelerator Market?

-> Chiplets for molecular dynamics simulation accelerator Market was valued at USD 0.78 billion in 2025 and is expected to reach USD 1.45 billion by 2034.

Which key companies operate in Chiplets for molecular dynamics simulation accelerator Market?

-> Key players include Intel, AMD (via Xilinx), TSMC and NXP, among others.

What are the key growth drivers?

-> Key growth drivers include heavy investment by pharmaceutical firms in AI‑driven drug design, rising demand from academic supercomputing centers for energy‑efficient atomistic modeling, and breakthroughs in silicon photonics and high‑bandwidth memory that enhance chiplet performance.

Which region dominates the market?

-> Regional dominance information was not disclosed in the source material.

What are the emerging trends?

-> Emerging trends include the integration of heterogeneous chiplet architectures to outperform monolithic GPUs on specific molecular dynamics workloads, the use of advanced interconnects such as EMIB and fan‑out wafer‑level packaging, and collaborative development programs between major foundries and ecosystem partners.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...