Market Insights

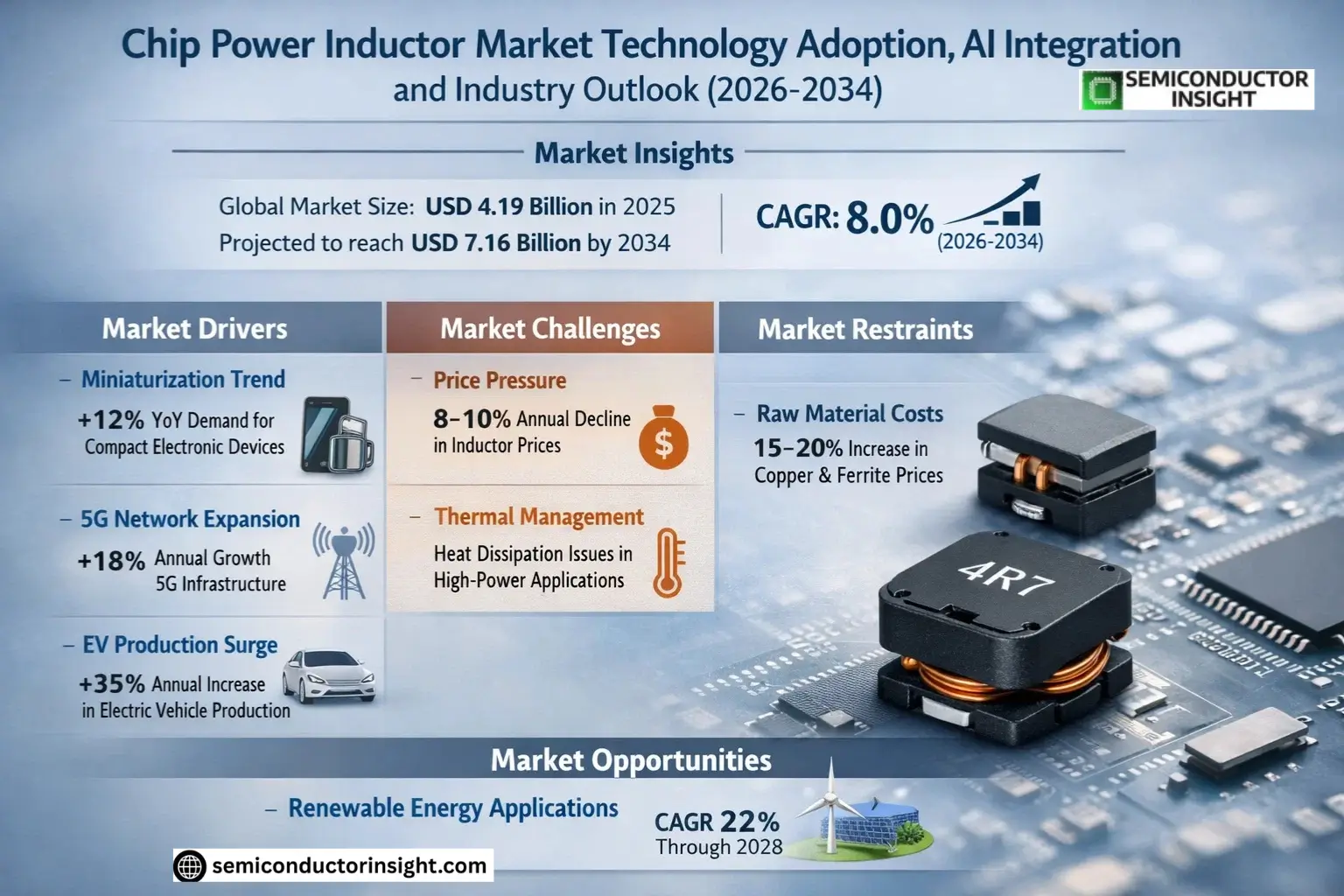

Global Chip Power Inductor Market size was valued at USD 4.19 billion in 2025. The market is projected to grow from USD 4.53 billion in 2026 to USD 7.16 billion by 2034, exhibiting a CAGR of 8.0% during the forecast period.

Chip power inductors are surface-mount components designed for PCB assembly, primarily used in DC-DC conversion, voltage regulation, and power filtering applications. These inductors are constructed using wire-wound, multilayer, co-fired, or molded techniques to provide energy storage, EMI suppression, and stable current flow in electronic circuits. Key performance requirements include compact size, low DC resistance (DCR), high saturation current tolerance, and thermal stability.

Market growth is driven by increasing demand for miniaturized electronics and higher power density solutions across industries. The automotive sector’s electrification trends and industrial automation requirements are creating new opportunities for advanced inductor technologies. Leading manufacturers are focusing on material innovations and production scalability to meet evolving application needs while maintaining cost competitiveness.

MARKET DRIVERS

Growing Demand for Miniaturized Electronic Components

Chip Power Inductor Market is witnessing strong growth driven by the increasing demand for compact, high-performance electronic devices. As smartphones, wearables, and IoT devices require smaller form factors, manufacturers are adopting chip power inductors for their space-saving advantages. Global miniaturization trend has led to a 12% year-over-year increase in demand for compact inductor solutions.

Expansion of 5G Infrastructure

5G network deployments are accelerating globally, creating substantial demand for chip power inductors in base stations and communication equipment. These components play a critical role in power management circuits for 5G infrastructure, with the market expected to grow by 18% annually in this segment. The superior high-frequency performance of modern chip power inductors makes them ideal for 5G applications.

Electric vehicle production growth of 35% annually is further propelling the Chip Power Inductor Market, as these components are essential for DC-DC converters and battery management systems.

MARKET CHALLENGES

Price Pressure from Commoditization

Standard chip power inductors are facing significant price erosion due to intense competition among manufacturers. Average selling prices have declined by 8-10% annually for basic inductor models, squeezing profit margins. This commoditization is particularly pronounced in consumer electronics applications.

Other Challenges

Thermal Management Constraints

As chip power inductors shrink in size while handling greater currents, managing heat dissipation becomes increasingly difficult. This thermal challenge affects reliability and performance in high-power-density applications.

MARKET RESTRAINTS

Raw Material Price Volatility

Fluctuating prices of key materials such as copper, ferrite, and specialty alloys used in chip power inductor manufacturing pose significant challenges. Recent supply chain disruptions have caused material costs to increase by 15-20%, impacting production economics and limiting market growth potential.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Systems

The renewable energy sector presents substantial growth opportunities for chip power inductor manufacturers. Solar inverters, wind power systems, and energy storage solutions increasingly require high-efficiency inductors capable of operation in harsh environments. This segment is projected to grow at a CAGR of 22% through 2028.

Chip Power Inductor Market Trends

Automotive Electronics Driving Quality and Reliability Demands

Chip Power Inductor Market is experiencing significant growth from automotive applications, particularly in advanced driver-assistance systems (ADAS), electrified powertrains, and vehicle domain controllers. Manufacturers are focusing on products with wider operating temperature ranges (-55°C to 150°C), higher current ratings, and improved vibration resistance to meet AEC-Q200 standards.

Other Trends

Miniaturization and Power Density Requirements

Demand for smaller package sizes (0201 and 0402) is growing in smartphones and wearables, while high-current applications favor 0603 and 0805 packages with flat-wire designs. Multilayer construction types are gaining share where space constraints dominate, while molded types excel in thermal management scenarios.

Material Innovations Enhancing Performance

Metal composite magnetic materials are replacing traditional ferrites in high-frequency applications, offering lower core losses and better DC bias characteristics. Leading suppliers are developing proprietary material formulations to achieve saturation currents above 30A while maintaining stable inductance under load.

Regional Manufacturing Shifts and Supply Chain Resilience

Japanese and Taiwanese firms continue to lead in high-end automotive and industrial segments, while Chinese manufacturers are expanding capacity for consumer electronics applications. Southeast Asia is emerging as an alternative production base to mitigate geopolitical risks in the supply chain.

Technology Integration with Power Management ICs

Close collaboration between Chip Power Inductor manufacturers and PMIC developers is creating optimized power delivery networks. This co-design approach improves system-level efficiency in applications like server VRMs and automotive power distribution units.

COMPETITIVE LANDSCAPE

Key Industry Players

Global leadership concentrated among Japanese, Taiwanese, and Chinese manufacturers with increasing competition from specialized suppliers

Chip Power Inductor Market is dominated by established Japanese suppliers like TDK, Murata, and Taiyo Yuden, who maintain technological leadership in high-reliability automotive and industrial applications. These companies leverage advanced material science and multilayer/laminated processes to achieve superior performance in miniaturized packages. Taiwanese firms such as YAGEO and Delta Electronics compete through scale manufacturing and vertical integration, particularly in consumer electronics segments.

Chinese manufacturers like Sunlord Electronics and Shenzhen Microgate Technology are rapidly gaining market share through cost competitiveness and improving technical capabilities. Specialized players including Coilcraft, Vishay, and Würth Elektronik focus on high-performance niches like ultra-low DCR designs and high-current applications. The competitive landscape shows increasing bifurcation between high-volume general purpose suppliers and specialty manufacturers developing optimized solutions for automotive and industrial power systems.

List of Key Chip Power Inductor Companies Profiled

- TDK

- Murata Manufacturing

- Taiyo Yuden

- YAGEO Group

- Delta Electronics

- Sunlord Electronics

- Vishay Intertechnology

- Sumida Corporation

- Coilcraft

- Shenzhen Microgate Technology

- Tai-Tech Advanced Electronics

- MinebeaMitsumi

- Panasonic

- Eaton

- Würth Elektronik

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Shielded Chip Power Inductor

|

| By Application |

|

Automotive Electronics

|

| By End User |

|

OEMs

|

| By Manufacturing Process |

|

Molded Process

|

| By Package Size |

|

0402 & 0603

|

Regional Analysis: Chip Power Inductor Market

Asia-Pacific

Japan leads in thin-film chip inductor development, with R&D focus on high-frequency applications for advanced communication systems and automotive radar technologies.

China accounts for over 60% of regional production capacity, benefitting from centralized electronics manufacturing clusters and vertical integration capabilities.

Taiwan and South Korea excel in advanced packaging technologies, enabling higher density chip inductor integration for cutting-edge semiconductor applications.

India and Southeast Asia show accelerating demand for chip power inductors in renewable energy systems and industrial automation equipment.

North America

The North American Chip Power Inductor Market thrives on aerospace/defense applications and electric vehicle adoption. U.S. manufacturers specialize in high-reliability inductors for mission-critical systems, leveraging advanced materials science. Regional companies collaborate closely with automotive OEMs to develop customized power management solutions. Strict energy efficiency regulations push innovation in low-loss ferrite materials and integrated magnetic components.

Europe

Europe demonstrates strong demand for automotive-grade chip power inductors, particularly in Germany and France. The region leads in adoption of eco-friendly manufacturing processes for magnetic components. Industrial automation and renewable energy sectors drive specialized inductor requirements. Collaborative R&D initiatives between academia and manufacturers foster innovations in high-temperature superconducting materials.

Middle East & Africa

The MEA region shows growing chip power inductor consumption in telecommunications infrastructure and oil/gas automation systems. Local assembly plants in UAE and Saudi Arabia are emerging to service regional demand. Market growth is propelled by smart city initiatives and industrial digitalization projects requiring robust power management solutions.

South America

Brazil and Mexico represent the fastest-growing South American markets for chip power inductors, primarily servicing automotive and consumer appliance industries. Local manufacturing capabilities focus on cost-competitive solutions for mid-range electronics. The region benefits from proximity to North American supply chains while developing domestic technical expertise.

Report Scope

This market research report provides a comprehensive analysis of the Chip Power Inductor Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining the current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of chip power inductors in powering advancements across industries such as automotive, consumer electronics, industrial automation, and telecommunications.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, manufacturing process, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of advanced materials, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chip Power Inductor Market?

-> Chip Power Inductor Market size was valued at USD 4.19 billion in 2025. The market is projected to grow from USD 4.53 billion in 2026 to USD 7.16 billion by 2034, exhibiting a CAGR of 8.0% during the forecast period.

What is the expected CAGR for the Chip Power Inductor Market?

-> The market is expected to grow at a CAGR of 8.0% during the forecast period (2025-2034).

Which key companies operate in Chip Power Inductor Market?

-> Key players include Delta Electronics, TDK, Murata, YAGEO, Taiyo Yuden, Sunlord Electronics, Vishay, Sumida, Coilcraft, and Panasonic, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand in automotive electronics, increasing switching frequencies in power management systems, and expansion of consumer electronics and industrial automation applications.

Which region dominates the market?

-> Asia dominates the market, with manufacturing clusters centered in Japan, China, Taiwan, and South Korea, which accounted for the majority of production capacity in 2025.

What are the emerging trends?

-> Emerging trends include adoption of metal composite magnetic materials, molded structures, flat-wire windings, and products meeting AEC-Q200 automotive qualification standards.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...