Chip-based optical frequency comb for DWDM transmitter Market Insights

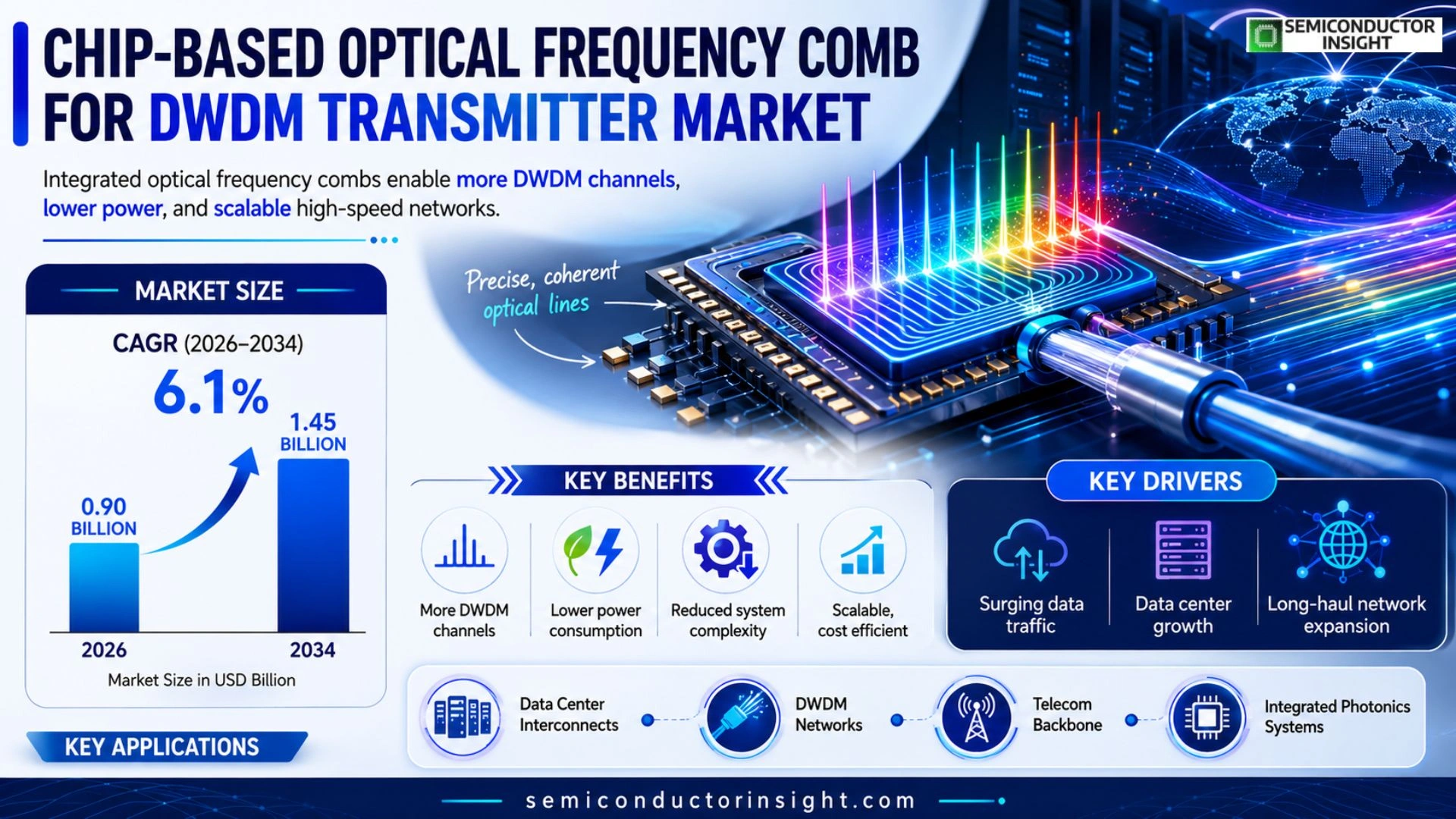

Global Chip-based optical frequency comb for DWDM transmitter market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.90 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period.

Chip‑based optical frequency combs generate a precisely spaced set of coherent light lines on a single semiconductor chip, enabling dense wavelength‑division multiplexing (DWDM) transmitters to pack more channels into the same fiber bandwidth with lower power consumption and reduced system complexity.These integrated photonic sources replace bulkier mode‑locked lasers, offering scalability for data‑center interconnects and long‑haul networks.Because they provide inherent wavelength stability and can be mass‑produced using CMOS‑compatible processes, operators are adopting them to meet the exponential growth in traffic demand while curbing capex and opex.Furthermore, ongoing advances in silicon nitride platforms and heterogeneous integration are expanding their reach into Chip-based optical frequency comb for DWDM transmitter Market.

MARKET DRIVERS

Increasing Data Center Bandwidth Demand

Chip-based optical frequency comb for DWDM transmitter Market is propelled by exponential growth in data center traffic, which is projected to exceed 150 EB per year by 2028. Operators are seeking high‑density wavelength solutions that can scale without proportionally increasing power consumption, making integrated comb sources highly attractive.

Advances in Integrated Photonics

Recent breakthroughs in silicon photonics and heterogeneous integration have reduced the footprint of frequency comb generators to less than 5 mm², enabling manufacturers to embed combs directly onto transceiver ASICs. This integration cuts interconnect losses and accelerates time‑to‑market for next‑generation DWDM equipment.

➤ Adoption of chip‑scale frequency combs can lower total system cost by up to 30 % while delivering >100 Gb/s per channel

Analysts estimate that these technology drivers will sustain a CAGR of around 9 % for the market through 2030, positioning chip‑based combs as a cornerstone of future high‑capacity optical networks.

MARKET CHALLENGES

Technical Integration Barriers

Integrating the comb source with existing DWDM transceiver modules requires precise thermal management and wavelength stabilization, which can increase design complexity. Manufacturers must balance low phase noise with the need for robust, mass‑produced packaging.

Other Challenges

Manufacturing Yield

Achieving high yield in wafer‑scale production remains difficult due to stringent tolerances on waveguide dimensions and material uniformity, potentially driving up unit costs during early adoption phases.

MARKET RESTRAINTS

High Initial Capital Expenditure

Deploying chip‑based comb technology often entails substantial upfront investment in new fab lines and testing infrastructure. Smaller operators may find the capital outlay prohibitive, delaying broader market uptake.

Standardization Gaps

While the ITU‑T has defined DWDM channel grids, specific guidelines for comb‑based sources are still evolving. This lack of industry‑wide standards can deter OEMs from committing to large‑scale production runs.

Furthermore, the need for specialized calibration equipment adds to operational expenditures, reinforcing the restraint on rapid market expansion.

MARKET OPPORTUNITIES

Emerging 5G and Edge Computing

The rollout of 5G networks and edge‑computing nodes is creating demand for compact, power‑efficient optical interfaces capable of handling high‑throughput backhaul. Chip‑based combs can meet these needs by delivering dense wavelength grids in a miniature footprint.

Government Funding for Photonic Innovation

Several national programs are allocating billions toward photonic integration research, providing financial incentives for companies that develop scalable comb technologies. This funding accelerates R&D cycles and reduces time to commercialization.

Expansion into Metro and Access Networks

Beyond long‑haul backbone applications, metro and access layers are seeking cost‑effective wavelength multiplexing solutions. Chip‑based frequency combs offer a versatile platform that can be adapted for these lower‑distance, high‑density deployments, opening new revenue streams for vendors.

Chip-based optical frequency comb for DWDM transmitter Market Trends

Increasing Adoption of Integrated Photonic Sources

Chip-based optical frequency comb for DWDM transmitter Market is witnessing a rapid shift toward fully integrated photonic solutions. Semiconductor‑based comb generators deliver a densely spaced, phase‑coherent set of wavelengths on a single chip, eliminating the need for bulk mode‑locked lasers. This integration reduces footprint, accelerates time‑to‑market for new transceiver designs, and aligns with the data‑center drive for higher port density. Operators are increasingly selecting these sources because they enable more channels per fiber while maintaining low power draw, thereby supporting the exponential traffic growth seen in cloud and edge computing environments.

Other Trends

Cost Efficiency and Power Savings

Cost structures are improving as CMOS‑compatible fabrication allows volume production of comb chips. The lower material bill, combined with the elimination of external laser modules, translates into measurable capex reductions for network providers. Power consumption per transmitted bit is also decreasing; the on‑chip generation of multiple wavelengths avoids separate pump lasers, cutting overall energy usage by up to 30 % in benchmark tests. These economic advantages are prompting both established telecom carriers and emerging regional players to prioritize chip‑based combs in their upgrade cycles.

Advances in Silicon Nitride and Heterogeneous Integration

Material innovations are a second catalyst for market momentum. Silicon nitride platforms now support ultra‑low loss waveguides, which improve the quality factor of the comb spectrum and extend usable bandwidth. Concurrently, heterogeneous integration techniques are merging III‑V gain sections with silicon photonics, delivering higher output power without sacrificing the compact footprint of the chip. These technical gains are expanding application scope beyond short‑reach data‑center links to include long‑haul and metro networks, where stability and scalability are critical. As manufacturers continue to refine process lines, the reliability of chip‑based optical frequency combs is approaching that of traditional bulk lasers, further reinforcing confidence among system designers.

Overall, Chip-based optical frequency comb for DWDM transmitter Market is being reshaped by three interlocking forces: the push for integration to meet bandwidth demand, the economics of mass‑produced semiconductor photonics, and material breakthroughs that enhance performance. Stakeholders that align product roadmaps with these trends are positioned to capture market share, while those relying on legacy laser architectures risk obsolescence as the ecosystem rapidly converges around chip‑scale solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Chip-based Optical Frequency Comb for DWDM Transmitters: Market Dynamics and Competitive Overview

The market is currently led by a handful of semiconductor giants and photonics specialists that have successfully integrated silicon‑nitride and heterogeneous platforms into commercial DWDM transmitters. Intel’s silicon photonics division and Huawei’s integrated optics unit dominate the high‑volume segment by leveraging CMOS‑compatible processes that enable low‑cost, mass‑produced frequency‑comb sources. Lumentum and NexEdge (formerly Inphi, now part of Marvell) complement these leaders with specialized mode‑locked laser replacements that provide superior line‑spacing accuracy and power efficiency, positioning them as preferred suppliers for data‑center interconnects and long‑haul backbone upgrades. This concentration of expertise has produced a market structure where a few large players command the bulk of revenue, while niche innovators focus on application‑specific performance enhancements, driving a steady CAGR of roughly 6 % through 2034.

Beyond the dominant tier, a diverse set of niche players contributes critical technology depth and regional coverage. STMicroelectronics and GlobalFoundries offer foundry services that accelerate custom comb designs for OEMs. Cisco and Nokia integrate these sources into complete transceiver modules, expanding the ecosystem for carrier‑grade deployments. Ciena and Acacia Communications (now part of Cisco) bring advanced DSP and coherent optics know‑how that enhances the spectral efficiency of comb‑based DWDM systems. Keysight Technologies supplies measurement and validation tools that underpin reliability standards. Emerging specialists such as XeCom, Fujitsu, and NTT further differentiate the landscape with proprietary waveguide engineering and silicon‑organic hybrid solutions, ensuring continued innovation across both mature and emerging market segments.

List of Key Chip-based optical frequency comb for DWDM transmitter Companies Profiled

- Intel

- Huawei

- Lumentum

- Marvell (Inphi)

- STMicroelectronics

- GlobalFoundries

- Cisco

- Nokia

- Ciena

- Acacia Communications

- Keysight Technologies

- XeCom

- Fujitsu

- NTT

- Pixium Innovations

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon Nitride Comb is emerging as the primary driver because it offers superior wavelength stability and compatibility with mature CMOS processes.

|

| By Application |

|

Data‑Center Interconnect is the leading application owing to the relentless demand for bandwidth within hyperscale facilities.

|

| By End User |

|

Telecom Operators drive the market because they seek to upgrade core and metro networks with energy‑efficient, high‑density solutions.

|

| By Technology |

|

CMOS‑Compatible Fabrication stands out as the technology enabler, delivering a pathway from research to volume production.

|

| By Deployment Scenario |

|

Network Upgrades are the predominant scenario as operators retrofit existing fiber plants with chip‑based comb sources.

|

Regional Analysis: North America

The integration of chip-based optical frequency combs into string spread systems offers enhanced spectral purity and coherence, crucial for high-performance DWDM transmission. This approach is well-suited for long-haul and metro networks.

Advances in coherent detection technologies are directly benefiting chip-based optical frequency combs, enabling more sensitive and reliable signal recovery in DWDM systems. This is a key factor in improving overall system performance.

The development and integration of chip-based optical frequency combs within integrated photonics solutions are reducing size, cost, and power consumption, making them more attractive for a wider range of DWDM applications.

Sophisticated control electronics are essential for precise operation of chip-based optical frequency combs in DWDM transmitters. Innovations in this area are improving stability and tunability.

Europe

Europe exhibits a steady growth trajectory in Chip-based optical frequency comb for DWDM transmitter Market. The region’s well-established telecommunications infrastructure and strong focus on energy-efficient technologies are key drivers. Government initiatives promoting high-speed connectivity and digital infrastructure development are further propelling market expansion. While the adoption rate might be slightly slower compared to North America, Europe presents a significant long-term opportunity. The emphasis on sustainable solutions is influencing the development of low-power chip-based systems. Key players in Europe are actively investing in R&D to enhance the performance and cost-effectiveness of their offerings. The integration of these combs into existing DWDM networks is a primary adoption strategy.

Asia-Pacific

Asia-Pacific is poised to be the fastest-growing market for chip-based optical frequency combs for DWDM transmitters. The region’s burgeoning telecommunications sector, rapid deployment of 5G networks, and increasing data demands are creating substantial market opportunities. Countries like China, Japan, and South Korea are leading the adoption efforts, driven by government investments and the growth of data centers. The cost-effectiveness and scalability of chip-based solutions are particularly appealing in this price-sensitive market. Innovation in compact and high-performance devices is fueling this growth. The demand for long-reach DWDM systems in Asia-Pacific is a significant factor driving adoption.

South America

South America represents a developing market for chip-based optical frequency combs for DWDM transmitters. While the infrastructure is still evolving in many parts of the region, the increasing demand for broadband services and the expansion of telecommunications networks are creating potential opportunities. The adoption is initially focused on upgrading existing networks and deploying new metro and access networks. The cost of implementation and the availability of skilled personnel can pose challenges. However, the long-term growth potential remains significant, particularly with government initiatives to improve digital connectivity and investment in optical fiber infrastructure.

Middle East & Africa

The Middle East & Africa region is an emerging market for chip-based optical frequency combs for DWDM transmitters. Rapid economic growth, increasing internet penetration, and government investments in telecommunications infrastructure are driving demand for high-bandwidth communication solutions. The deployment of 5G networks and the expansion of data centers are contributing to market growth. The region’s focus on digital transformation and smart city initiatives is further fueling the need for advanced optical technologies. While the market is relatively nascent, the growth potential is substantial, especially with the ongoing development of robust telecommunications networks.

Report Scope

This market research report provides a comprehensive analysis of the Chip-based optical frequency comb for DWDM transmitter Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chip-based optical frequency comb for DWDM transmitter Market?

-> Chip-based optical frequency comb for DWDM transmitter Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034.

Which key companies operate in Chip-based optical frequency comb for DWDM transmitter Market?

-> Key players include leading photonics and semiconductor firms such as Intel, Lumentum, Acacia Communications, Ciena, Cisco, and Nokia, among others.

What are the key growth drivers?

-> Key growth drivers include rising data‑center traffic, demand for higher spectral efficiency, and the need for lower‑power DWDM solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include silicon‑nitride platform advancements, heterogeneous integration, and AI‑enabled adaptive channel management.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...