Charge redistribution SAR ADC with asynchronous logic Market Insights

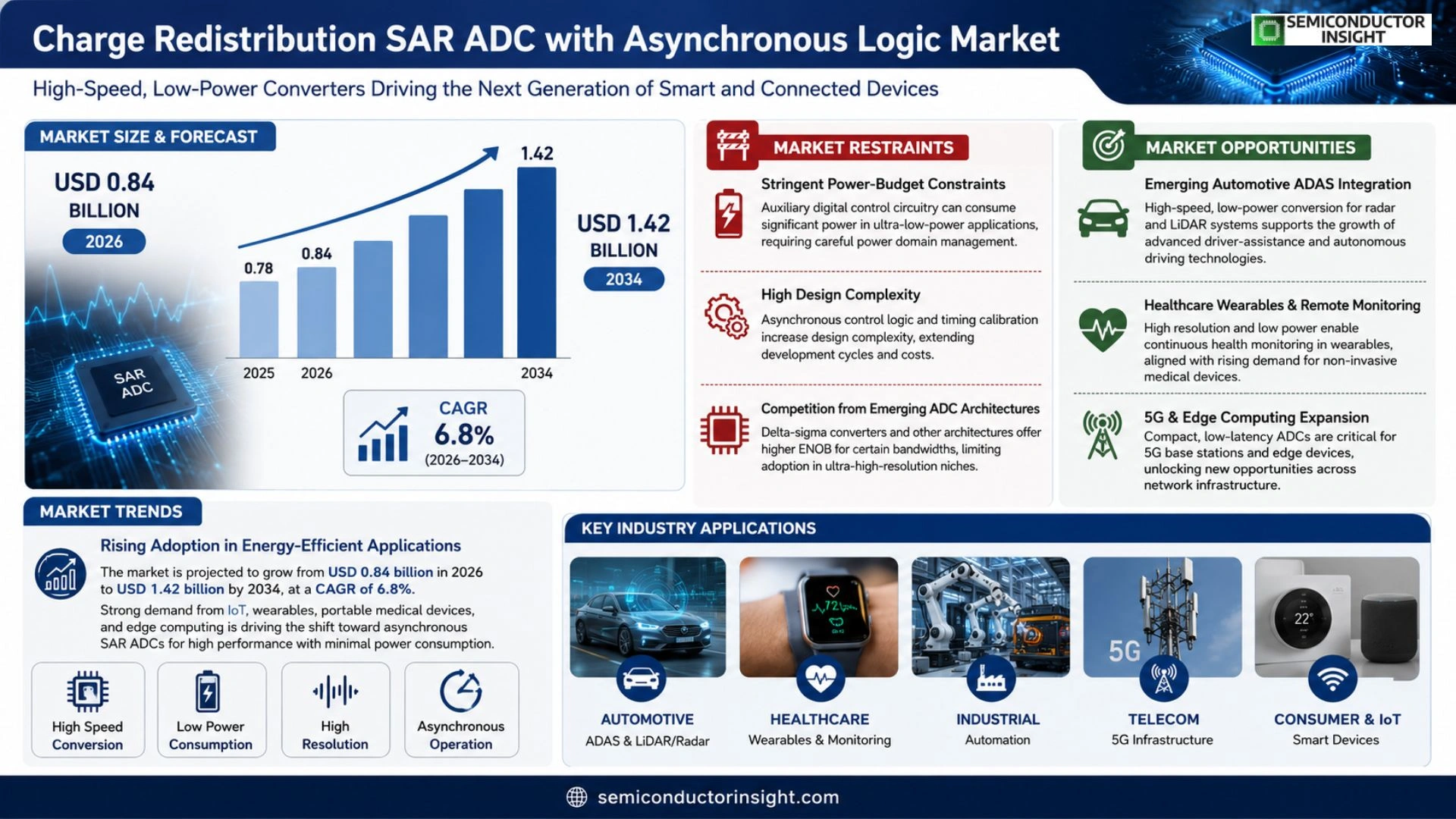

Global Charge redistribution SAR ADC with asynchronous logic market size was valued at USD 0.78 billion in 2025. The market is projected to grow from USD 0.84 billion in 2026 to USD 1.42 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

Charge redistribution successive approximation register (SAR) analog‑to‑digital converters (ADCs) employing asynchronous logic are high‑speed, low‑power conversion solutions that leverage capacitor‑based charge sharing and event‑driven sampling to achieve fine resolution while minimizing energy consumption. These converters are essential for portable medical devices, IoT sensors, and automotive radar systems because they deliver rapid digitization without compromising battery life.

The market is experiencing rapid growth due to several factors, including rising demand for energy‑efficient electronics, expansion of autonomous‑vehicle technologies, and increasing adoption of edge‑computing sensors. Furthermore, advancements in semiconductor process nodes enable higher integration density for asynchronous SAR architectures. Initiatives by key players such as Texas Instruments, Analog Devices, and Maxim Integrated are also expected to fuel market expansion through new product launches and strategic collaborations.

MARKET DRIVERS

Rising Demand for Low‑Power High‑Resolution Converters

Charge redistribution SAR ADC with asynchronous logic Market is being propelled by a surge in applications that require ultra‑low power consumption without sacrificing resolution. Devices such as wearable health monitors and battery‑operated sensors are adopting these converters to extend operational life while maintaining precise analog‑to‑digital conversion.

Growth of Edge AI and IoT Applications

Edge AI platforms are integrating charge redistribution SAR ADCs to process sensor data locally, reducing latency and bandwidth demands. This trend is especially evident in smart factories and predictive maintenance solutions, where real‑time analytics depend on high‑speed conversion.

➤ Industry forecasts predict a compound annual growth rate of approximately 9% for Charge redistribution SAR ADC with asynchronous logic Market through 2032, driven primarily by IoT expansion.

In addition, regulatory pressure for energy‑efficient designs in consumer electronics is encouraging OEMs to transition from legacy architectures to the asynchronous logic approach, further reinforcing market momentum.

MARKET CHALLENGES

Design Complexity and Calibration

Implementing asynchronous logic within charge redistribution SAR ADCs introduces intricate timing relationships that complicate design verification. Engineers must address non‑linearities and calibrate conversion stages to meet stringent accuracy targets, which can lengthen development cycles.

Other Challenges

Manufacturing Yield

The precision required for on‑chip capacitor matching often leads to lower wafer yields, increasing production costs and limiting price competitiveness for high‑volume markets.

Furthermore, cost‑sensitive segments such as mass‑market IoT devices place pressure on suppliers to reduce bill‑of‑materials while preserving performance, creating a delicate balance between innovation and affordability.

MARKET RESTRAINTS

Stringent Power‑Budget Constraints

Although asynchronous designs are inherently low‑power, the auxiliary digital control circuitry can consume a noticeable portion of the total budget in ultra‑low‑power applications. Designers must carefully partition power domains to avoid violating the strict energy envelopes of battery‑free or energy‑harvesting devices.

Competitive pressure from emerging delta‑sigma converters, which offer higher effective number of bits (ENOB) for certain bandwidths, also restrains adoption in niches where ultra‑high resolution outweighs conversion speed.

MARKET OPPORTUNITIES

Emerging Automotive ADAS Integration

Advanced driver‑assistance systems (ADAS) demand rapid, low‑power conversion of radar and LiDAR signals. Charge redistribution SAR ADC with asynchronous logic Market offers the speed and power profile suited for these safety‑critical applications, presenting a sizable growth avenue as automotive electrification accelerates.

Healthcare Wearables and Remote Monitoring

Medical wearables that continuously track physiological parameters benefit from the high resolution and asynchronous operation, which minimize noise and power draw. Regulatory trends favoring non‑invasive monitoring create a clear pathway for market expansion in the healthcare sector.

Finally, the convergence of 5G infrastructure with edge computing amplifies the need for compact, low‑latency converters, positioning asynchronous charge redistribution SAR ADCs as a strategic component in next‑generation network equipment.

Charge redistribution SAR ADC with asynchronous logic Market Trends

Rising Adoption in Energy‑Efficient Applications

Charge redistribution SAR ADC with asynchronous logic Market recorded a valuation of USD 0.78 billion in 2025 and is forecast to reach USD 1.42 billion by 2034, implying an average annual growth rate of roughly 6.8 % over the next decade. This trajectory reflects strong demand for high‑speed, low‑power conversion solutions in portable medical equipment, Internet‑of‑Things sensors, and edge‑computing platforms. By leveraging capacitor‑based charge sharing and event‑driven sampling, these converters achieve fine resolution while consuming minimal energy, a combination that aligns with the broader industry shift toward battery‑optimized electronics. The upward trend is further supported by expanding design win rates in consumer wearables, where extended battery life directly translates into higher user satisfaction. Regulatory pressures for lower energy consumption in medical devices have accelerated certification pathways for low‑power converters, further solidifying market momentum. Moreover, the growing emphasis on sustainable electronics drives OEMs to prioritize components that minimize standby draw, a niche where asynchronous SAR converters excel.

Other Trends

Automotive Radar and Autonomous Vehicles

Automotive radar systems and autonomous‑vehicle platforms have emerged as a decisive growth catalyst. As manufacturers integrate more advanced driver‑assistance features, the need for rapid digitization of analog radar signals grows. Asynchronous SAR architectures provide the required sampling speed without imposing a thermal or power penalty, making them suitable for integration in compact radar front‑ends. Recent vehicle prototypes demonstrate that replacing conventional clocked SAR blocks with asynchronous logic can shave up to 15 % of system power, directly contributing to longer electric‑vehicle range and lower cooling requirements. In addition, sensor‑fusion modules that combine radar, lidar, and camera inputs rely on synchronized digitization pipelines; the event‑driven nature of asynchronous SAR ADCs simplifies timing alignment, reducing firmware complexity and improving overall system reliability.

Advancements in Asynchronous SAR Architecture

The market is also shaped by continuous semiconductor process improvements that enable denser integration of charge‑redistribution blocks and on‑chip calibration circuits. Nodes at 28 nm and below allow designers to embed asynchronous control logic alongside high‑precision analog front‑ends, resulting in single‑chip solutions that reduce board‑level BOM costs. Leading vendors such as Texas Instruments, Analog Devices, and Maxim Integrated have announced new product families featuring built‑in temperature compensation and programmable sampling rates, reinforcing the competitive landscape. Collaborative development programs with foundry partners accelerate time‑to‑market, ensuring that Charge redistribution SAR ADC with asynchronous logic Market remains responsive to emerging application demands. Design ecosystems are evolving with enhanced SPICE models and automated layout generators that incorporate charge‑redistribution behavior, shortening development cycles for system‑level engineers and lowering entry barriers for mid‑tier manufacturers seeking to adopt the technology.

COMPETITIVE LANDSCAPE

Key Industry Players

Charge Redistribution SAR ADC with Asynchronous Logic – Competitive Overview

The market is dominated by a handful of large semiconductor firms that command both design expertise and high‑volume manufacturing capability. Texas Instruments leads with its ADS8860 family, leveraging a mature 65 nm CMOS process to deliver sub‑1 µW power consumption at 12‑bit resolution. Analog Devices follows closely, offering the AD7626 series that integrates asynchronous SAR engines with on‑chip digital calibration, positioning the company as a preferred supplier for automotive radar and IoT edge devices. Maxim Integrated (now part of Analog Devices) complements the landscape with its MAX11270 line, targeting portable medical instrumentation where ultra‑low latency is critical. These tier‑1 players shape market structure through extensive IP portfolios, aggressive roadmap updates, and strategic collaborations with foundries to push process nodes, thus setting performance benchmarks for the entire segment.

Beyond the incumbents, a diverse set of niche innovators is expanding the technology envelope. Microchip Technology provides cost‑effective SAR solutions for consumer wearables, while STMicroelectronics and NXP Semiconductors focus on mixed‑signal platforms that integrate SAR ADCs with automotive‑grade safety features. Infineon Technologies and ON Semiconductor are strengthening their presence in power‑sensitive automotive radar modules. Smaller firms such as Silicon Labs, Rohm Semiconductor, and Skyworks Solutions differentiate through specialized asynchronous logic blocks optimized for ultra‑high‑speed sampling in 5G front‑ends. Emerging players like AMS and Cirrus Logic contribute advanced capacitor‑stack architectures that enhance resolution without sacrificing power budget, highlighting a vibrant ecosystem of both global leaders and agile specialists.

List of Key Charge Redistribution SAR ADC with Asynchronous Logic Companies Profiled

- Texas Instruments

- Analog Devices

- Maxim Integrated (Analog Devices)

- Microchip Technology

- STMicroelectronics

- NXP Semiconductors

- Infineon Technologies

- ON Semiconductor

- Silicon Labs

- Rohm Semiconductor

- Skyworks Solutions

- Cirrus Logic

- AMS (Austriamicrosystems)

- Qorvo

- Renesas Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Asynchronous SAR Architecture

|

| By Application |

|

IoT Edge Sensors

|

| By End User |

|

Medical Device Manufacturers

|

| By Technology Trend |

|

Advanced Process Nodes

|

| By Integration Strategy |

|

System‑in‑Package (SiP) Solutions

|

Regional Analysis: Charge redistribution SAR ADC with asynchronous logic Market

The need for ultra‑low power consumption in IoT sensors and the rise of autonomous systems propel adoption of advanced SAR ADC architectures, especially those employing asynchronous logic to reduce idle‑state energy draw.

Emerging energy‑efficiency standards across North America encourage manufacturers to embed charge‑redistribution techniques, ensuring compliance while delivering higher performance per watt.

Early‑stage deployment in automotive ADAS modules showcases the practical benefits of asynchronous SAR ADCs, fostering broader acceptance across related high‑precision domains.

Leading semiconductor vendors leverage extensive IP portfolios to differentiate their offerings, while niche players focus on custom solutions for specialized industrial applications.

Europe

European manufacturers emphasize precision and reliability, integrating charge‑redistribution SAR ADCs into medical imaging and high‑frequency communication equipment. Collaborative EU research programs promote cross‑border innovation, while stringent electromagnetic compatibility directives guide design choices that favor asynchronous operation for reduced noise. Market growth is supported by strong automotive pipelines, particularly in electric‑vehicle power‑train control, where efficiency gains translate directly into extended range and lower thermal budgets.

Asia‑Pacific

The Asia‑Pacific region benefits from expansive electronics manufacturing capacity and cost‑effective talent pools. Companies in Japan, South Korea, and Taiwan are rapidly incorporating asynchronous SAR ADC technology into consumer electronics, seeking longer battery life and faster response times. While the market remains price‑sensitive, increasing demand for smart home devices and wearable health monitors drives qualitative improvements in ADC performance without substantial cost penalties.

South America

South American players focus on niche applications such as renewable‑energy inverters and agricultural monitoring systems. Adoption of charge‑redistribution techniques is motivated by the need to operate under demanding environmental conditions while conserving power. Regional collaborations with U.S. and European technology partners accelerate knowledge transfer, enabling local firms to integrate advanced ADC solutions into emerging smart‑grid initiatives.

Middle East & Africa

In the Middle East and Africa, growth is linked to infrastructure development and telecommunications expansion. Operators seek ADCs that combine high accuracy with low power draw for remote base stations and satellite communication equipment. Emerging smart‑city projects provide a platform for trialing asynchronous SAR ADCs, positioning the region to benefit from incremental efficiencies and enhanced signal fidelity.

Report Scope

This market research report provides a comprehensive analysis of the Charge redistribution SAR ADC with asynchronous logic Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Charge redistribution SAR ADC with asynchronous logic Market?

-> Charge redistribution SAR ADC with asynchronous logic market size is projected to grow from USD 0.84 billion in 2026 to USD 1.42 billion by 2034, reflecting a CAGR of 6.8% during the forecast period.

Which key companies operate in Charge redistribution SAR ADC with asynchronous logic Market?

-> Key players include Texas Instruments, Analog Devices, and Maxim Integrated, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy‑efficient electronics, expansion of autonomous‑vehicle technologies, increasing adoption of edge‑computing sensors, and advancements in semiconductor process nodes enabling higher integration density for asynchronous SAR architectures.

Which region dominates the market?

-> The report highlights North America, Europe, and Asia‑Pacific as major regions, with North America often cited as a leading market for high‑performance ADC technologies.

What are the emerging trends?

-> Emerging trends include higher integration density asynchronous SAR designs, strategic collaborations among semiconductor vendors, and the incorporation of AI/IoT functionalities into ADC solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...