MARKET INSIGHTS

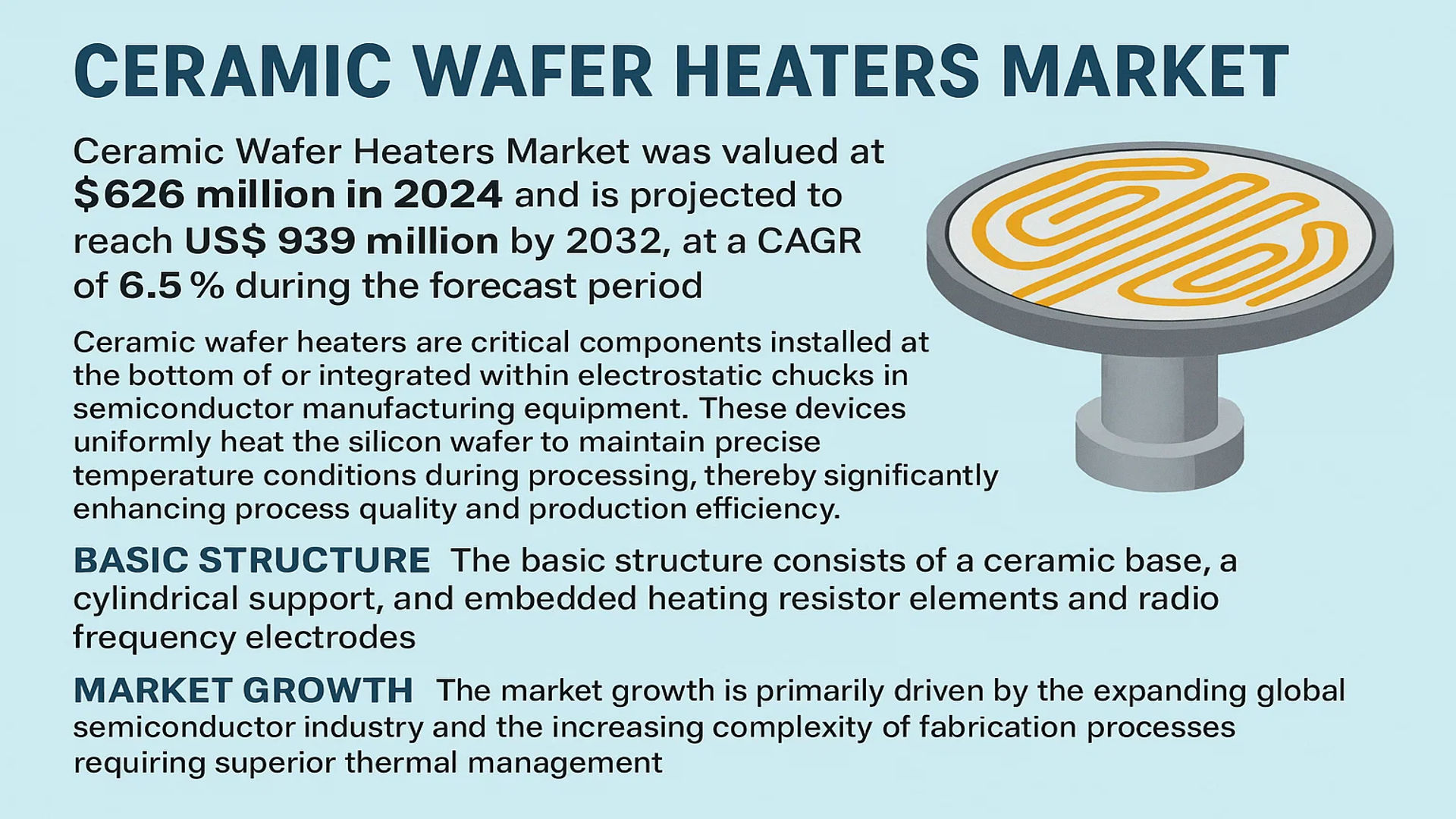

The global Ceramic Wafer Heaters Market was valued at 626 million in 2024 and is projected to reach US$ 939 million by 2032, at a CAGR of 6.5% during the forecast period.

Ceramic wafer heaters are critical components installed at the bottom of or integrated within electrostatic chucks in semiconductor manufacturing equipment. These devices uniformly heat the silicon wafer to maintain precise temperature conditions during processing, thereby significantly enhancing process quality and production efficiency. The basic structure consists of a ceramic base, a cylindrical support, and embedded heating resistor elements and radio frequency electrodes.

The market growth is primarily driven by the expanding global semiconductor industry and the increasing complexity of fabrication processes requiring superior thermal management. A key material trend is the dominance of aluminum nitride (AlN) based heaters, which are favored for their high thermal conductivity, excellent electrical insulation, and a thermal expansion coefficient similar to silicon, minimizing thermal stress on wafers. The industry is highly concentrated, with the top three companies holding over 90% of the market share; NGK Insulators leads with approximately 70% alone. Geographically, major manufacturing is centered in Japan and South Korea, while the United States represents the largest downstream consumption region due to demand from key equipment OEMs like Applied Materials and Lam Research.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Semiconductor Manufacturing Capacities to Drive Market Growth

The global semiconductor industry is experiencing unprecedented growth, driven by increasing demand for advanced electronics, artificial intelligence applications, and automotive semiconductors. This expansion directly fuels the demand for ceramic wafer heaters, which are critical components in chemical vapor deposition (CVD) and atomic layer deposition (ALD) equipment. The semiconductor equipment market is projected to reach over $100 billion annually by 2025, with CVD/ALD equipment representing approximately 25% of this total. Major semiconductor manufacturers are investing heavily in new fabrication facilities, with global semiconductor capital expenditure expected to exceed $200 billion in 2024. This substantial investment in manufacturing infrastructure creates a robust demand for ceramic wafer heaters, as each new fabrication line requires numerous deposition systems equipped with these essential components.

Advancements in Thin Film Deposition Technologies to Boost Market Expansion

Technological advancements in thin film deposition processes are driving the need for more sophisticated ceramic wafer heaters. The transition to smaller process nodes below 7nm requires extremely precise temperature control and uniformity during deposition processes. Modern ceramic heaters achieve temperature uniformity within ±1°C across 300mm wafers, enabling the production of advanced semiconductor devices. The development of new materials and processes, such as high-k metal gates and 3D NAND structures, demands heaters capable of operating at higher temperatures while maintaining exceptional thermal stability. These technological requirements are pushing manufacturers to develop advanced aluminum nitride-based heaters with improved thermal conductivity exceeding 180 W/mK and enhanced mechanical properties.

Furthermore, the increasing adoption of compound semiconductors and the emergence of new application areas are creating additional growth opportunities.

➤ For instance, the gallium nitride semiconductor market is growing at approximately 20% annually, requiring specialized heating solutions that can handle the unique processing requirements of these materials.

Additionally, the integration of Industry 4.0 technologies and smart manufacturing practices is enabling real-time monitoring and control of heater performance, further enhancing process efficiency and yield rates in semiconductor fabrication.

MARKET CHALLENGES

High Manufacturing Complexity and Technical Barriers to Challenge Market Participants

The production of ceramic wafer heaters involves extremely complex manufacturing processes and requires specialized expertise that presents significant challenges for market entrants. The fabrication of aluminum nitride-based heaters demands precise control over material composition, sintering processes, and electrode patterning. Achieving the required thermal and electrical properties while maintaining mechanical integrity involves sophisticated manufacturing techniques that have been refined over decades. The development cycle for new heater designs typically spans 12-18 months, requiring substantial investment in research and development. Current manufacturing yields for advanced 300mm heaters range between 65-75%, indicating the technical difficulty of producing defect-free components that meet the stringent requirements of semiconductor manufacturing.

Other Challenges

Material Supply Chain Constraints

The specialized raw materials required for ceramic heater production, particularly high-purity aluminum nitride powder, face supply chain challenges. The global production capacity for semiconductor-grade aluminum nitride is limited to a few specialized suppliers, creating potential bottlenecks. Recent geopolitical tensions and trade restrictions have further complicated the supply chain, leading to longer lead times and price volatility for critical materials.

Technical Performance Requirements

Meeting the increasingly stringent performance specifications for next-generation semiconductor processes presents ongoing challenges. Requirements for improved temperature uniformity, faster ramp rates, and longer operational lifetimes demand continuous innovation. The need for heaters to operate in corrosive environments while maintaining electrical insulation properties adds another layer of complexity to the design and manufacturing processes.

MARKET RESTRAINTS

High Development Costs and Long Qualification Cycles to Limit Market Entry

The ceramic wafer heater market faces significant restraints due to the substantial financial investment required for product development and the extended qualification processes mandated by semiconductor equipment manufacturers. Developing a new ceramic heater platform typically requires capital investment ranging from $20-50 million, covering advanced manufacturing equipment, clean room facilities, and testing infrastructure. The qualification process with major equipment manufacturers can take 18-24 months, involving rigorous testing under actual production conditions. This lengthy and costly process creates substantial barriers for new market entrants and limits the ability of smaller manufacturers to expand their product portfolios.

Additionally, the concentrated nature of the customer base amplifies these challenges, as the top three semiconductor equipment manufacturers account for approximately 70% of the total market demand.

Moreover, the need for continuous investment in research and development to keep pace with evolving semiconductor technology nodes further strains the financial resources of market participants, particularly smaller companies with limited capital reserves.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Packaging and Compound Semiconductors to Create Growth Opportunities

The rapid growth of advanced packaging technologies and compound semiconductors presents significant opportunities for ceramic wafer heater manufacturers. The advanced packaging market is expanding at approximately 8% annually, driven by requirements for heterogeneous integration and 3D packaging solutions. These applications require specialized heating solutions for processes such as temporary bonding, debonding, and through-silicon via formation. The compound semiconductor market, particularly gallium nitride and silicon carbide devices, is growing at over 15% annually to meet demand from power electronics, RF applications, and optoelectronics. These materials require processing at higher temperatures than traditional silicon, creating opportunities for heaters with enhanced thermal capabilities.

Additionally, the increasing adoption of ceramic heaters in emerging technology areas such as microLED manufacturing and quantum computing applications provides new revenue streams for innovative manufacturers.

Furthermore, the ongoing geographic diversification of semiconductor manufacturing, particularly the expansion of production capabilities in regions seeking technological independence, creates additional market opportunities for ceramic wafer heater suppliers able to support these new manufacturing clusters.

CERAMIC WAFER HEATERS MARKET TRENDS

Advanced Semiconductor Fabrication Processes Driving Demand for High-Performance Heating Solutions

The relentless push towards smaller semiconductor nodes and more complex 3D architectures is creating unprecedented demand for precision thermal management solutions. Ceramic wafer heaters have become indispensable components in critical fabrication processes such as chemical vapor deposition (CVD) and atomic layer deposition (ALD), where maintaining exact temperature uniformity across the wafer surface directly impacts yield and device performance. The transition to advanced nodes below 10nm requires temperature control within ±1°C across 300mm wafers, a specification that only advanced ceramic heaters can consistently achieve. This technological requirement is driving substantial investment in R&D for improved heater designs, with manufacturers developing increasingly sophisticated multi-zone heating elements and enhanced temperature sensing capabilities. The market is responding to these technical challenges with innovations in materials science, particularly in aluminum nitride (AlN) ceramics which offer exceptional thermal conductivity exceeding 170 W/mK while maintaining excellent electrical insulation properties crucial for semiconductor processing environments.

Other Trends

Geopolitical Factors Reshaping Manufacturing and Supply Chain Dynamics

Recent geopolitical developments and trade policies are significantly influencing the ceramic wafer heaters market landscape. The concentration of manufacturing capability in Japan and South Korea, where the top three companies control over 90% of the market share, creates both advantages and vulnerabilities in the global supply chain. While this concentration has enabled technological excellence and manufacturing efficiency, it also presents risks that are driving diversification efforts. Countries are implementing policies to develop domestic semiconductor capabilities, leading to emerging production centers in previously underrepresented regions. This strategic shift is creating new market opportunities while simultaneously introducing competitive pressures that may reshape the industry’s structure over the coming years.

Expansion into Emerging Applications and Materials Innovation

Beyond traditional semiconductor applications, ceramic wafer heaters are finding new opportunities in emerging technology sectors. The rapid growth of compound semiconductor manufacturing for power electronics, RF devices, and photonics applications requires specialized heating solutions capable of handling unique material properties and process requirements. Additionally, the development of wide bandgap semiconductors based on silicon carbide (SiC) and gallium nitride (GaN) presents both challenges and opportunities for heater manufacturers, as these materials often require higher processing temperatures and different thermal management approaches. Manufacturers are responding with specialized heater designs featuring improved temperature ranges and enhanced durability. Furthermore, research into new ceramic compositions and manufacturing techniques promises to deliver heaters with even better performance characteristics, including faster ramp rates, improved temperature uniformity, and longer operational lifetimes in demanding semiconductor fabrication environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Superiority and Regional Dominance Define Market Leadership

The competitive landscape of the global ceramic wafer heaters market is highly concentrated, with a select few players commanding the majority of market share. This dominance is primarily due to the significant technological barriers to entry and the critical need for ultra-high purity and reliability in semiconductor manufacturing applications. NGK Insulators, Ltd. stands as the undisputed market leader, holding an estimated 70% of the global market share. Their supremacy is built on decades of advanced ceramics expertise, deep-rooted relationships with major semiconductor equipment OEMs, and a commanding presence in the key consumption regions of Japan and the United States.

Following NGK, a small group of established players, including MiCo Ceramics Co., Ltd. and Sumitomo Electric Industries, Ltd., collectively account for a significant portion of the remaining market. These companies compete by leveraging their specialized material science capabilities and focus on high-performance aluminum nitride (AlN) solutions. Their growth is intrinsically linked to the expansion of the thin-film deposition equipment market, particularly for Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD) systems.

Furthermore, these leading companies are continuously engaged in research and development to enhance heater performance, such as improving thermal uniformity and enabling faster ramp-up and cool-down cycles. Strategic partnerships and long-term supply agreements with equipment giants like Applied Materials and Lam Research are commonplace, cementing their market positions and creating high entry barriers for new competitors.

Meanwhile, other notable players like Kyocera Corporation and CoorsTek, Inc. are strengthening their foothold through targeted innovations and expansions into emerging applications. The competitive dynamics are also shifting with the emergence of companies in South Korea and China, such as Boboo Hi-Tech and Suzhou Kematek, who are beginning to develop localized production capabilities. Supported by national semiconductor independence policies, these newer entrants are poised to gradually increase their presence, particularly within their domestic markets, intensifying competition in the coming years.

List of Key Ceramic Wafer Heater Companies Profiled

- NGK Insulators, Ltd. (Japan)

- MiCo Ceramics Co., Ltd. (South Korea)

- Sumitomo Electric Industries, Ltd. (Japan)

- NTK Ceratec, Inc. (Japan)

- Kyocera Corporation (Japan)

- CoorsTek, Inc. (U.S.)

- Boboo Hi-Tech (China)

- Fralock (U.S.)

- Semixicon LLC (U.S.)

- Suzhou Kematek Inc. (China)

Segment Analysis:

By Wafer Size

300 mm Segment Dominates the Market Due to its Pervasive Adoption in Advanced Semiconductor Manufacturing Nodes

The market is segmented based on wafer size into:

- 300 mm

- 200 mm

- Others

By Application

Equipment Suppliers Segment Leads Due to High Integration in New CVD and ALD System Sales

The market is segmented based on application into:

- Equipment Suppliers

- Wafer Suppliers

By Material Type

Aluminum Nitride (AlN) Segment is Favored for its Superior Thermal and Electrical Properties in High-Temperature Processes

The market is segmented based on material type into:

- Aluminum Nitride (AlN)

- Alumina (Al2O3)

- Others

By End-User Industry

Semiconductor Fabrication Segment Holds the Largest Share Driven by Global Expansion of Foundry and Memory Production

The market is segmented based on end-user industry into:

- Semiconductor Fabrication

- Flat Panel Display (FPD) Manufacturing

- Solar Cell Production

- Others

Regional Analysis: Ceramic Wafer Heaters Market

Asia-Pacific

The Asia-Pacific region dominates the global Ceramic Wafer Heaters market, accounting for the largest consumption volume and the most significant manufacturing base. This supremacy is driven by the concentration of major semiconductor equipment manufacturers and wafer fabrication plants in key countries like Japan, South Korea, and Taiwan. Japan is the global epicenter for production, with NGK Insulators holding an estimated 70% market share, supported by a robust ecosystem of advanced material science and precision engineering. South Korea follows as a critical hub, home to leading equipment makers like Wonik IPS and Eugene Technology. The region is also witnessing explosive growth in China, fueled by substantial government investments in domestic semiconductor self-sufficiency. Companies such as Piotech Inc. and NAURA Technology are driving local demand for ceramic heaters integrated into their new CVD and ALD tools. While cost sensitivity remains a factor, the overarching trend is a rapid shift toward adopting high-performance, aluminum nitride-based heaters to support the manufacturing of next-generation chips.

North America

North America represents the largest downstream consumption market for Ceramic Wafer Heaters, primarily due to the presence of global semiconductor equipment giants Applied Materials and Lam Research. These companies are major customers, sourcing heaters for integration into their advanced thin-film deposition systems sold worldwide. The market is characterized by a demand for the highest quality and reliability, with a strong focus on innovation to support the development of cutting-edge process technologies at sub-5nm nodes. While local manufacturing presence is limited compared to Asia, with only a few smaller producers like CoorsTek and MiCo Ceramics operating, the region’s influence is immense. Its stringent technical specifications and performance requirements effectively set the global standard for product quality. The market is further propelled by significant investments in domestic chip manufacturing, such as those incentivized by the CHIPS and Science Act, which will sustain long-term demand for these critical components.

Europe

Europe holds a specialized, technologically advanced niche within the Ceramic Wafer Heaters market. The region’s strength lies in its strong research institutions and the presence of key equipment suppliers that serve specific, high-value segments of the semiconductor industry. While it does not have the volume of Asia or the concentrated downstream demand of North America, European innovation is crucial for developing next-generation heater technologies that offer improved thermal uniformity, faster ramp rates, and enhanced durability. The market is driven by the need to comply with stringent EU regulations on material sourcing and manufacturing processes, pushing for sustainable and traceable production. Collaboration between academic research, material science companies, and equipment manufacturers fosters a environment of continuous improvement, ensuring European players remain at the forefront of high-performance ceramic heater design for specialized applications beyond mass-market logic and memory production.

South America

The Ceramic Wafer Heaters market in South America is in its nascent stages and is characterized by minimal local manufacturing and limited direct consumption. The region’s semiconductor industry is underdeveloped compared to other global hubs, resulting in very small, niche demand primarily for maintenance, repair, and operations (MRO) purposes within existing wafer fabs or research facilities. Economic volatility and a lack of significant government investment in building a local semiconductor supply chain are the primary factors hindering market growth. Consequently, demand is met almost entirely through imports from established manufacturers in Asia, Europe, and North America. While the long-term potential exists should regional economies prioritize technological industrialization, the current market remains a minor segment with negligible influence on global supply, demand, or technological trends.

Middle East & Africa

The Middle East and Africa region represents an emerging but currently underdeveloped market for Ceramic Wafer Heaters. Activity is concentrated in a few nations, such as Israel and Saudi Arabia, which are making strategic investments to diversify their economies into technology and advanced manufacturing. Israel, with its strong tech sector, has some demand linked to research, development, and specialized fabrication. However, the region lacks a significant semiconductor manufacturing base, resulting in extremely limited volume consumption. The market is primarily served by international imports for very specific projects or research initiatives. Long-term growth is contingent on substantial, sustained investment in building a foundational semiconductor ecosystem, which is a complex and capital-intensive endeavor. For the foreseeable future, this region will remain a marginal player in the global Ceramic Wafer Heaters landscape.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Ceramic Wafer Heaters markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ceramic Wafer Heaters Market?

-> Ceramic Wafer Heaters Market was valued at 626 million in 2024 and is projected to reach US$ 939 million by 2032, at a CAGR of 6.5% during the forecast period..

Which key companies operate in Global Ceramic Wafer Heaters Market?

-> Key players include NGK Insulator, MiCo Ceramics, Sumitomo Electric, NTK Ceratec, and Kyocera, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for advanced semiconductor fabrication, expansion of CVD and ALD equipment markets, and the need for precise thermal management in wafer processing.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing region, driven by semiconductor manufacturing hubs in Japan, South Korea, and China.

What are the emerging trends?

-> Emerging trends include the development of larger 300mm wafer heaters, integration of advanced aluminum nitride (AlN) materials, and the rise of domestic manufacturing in China.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...