MARKET INSIGHTS

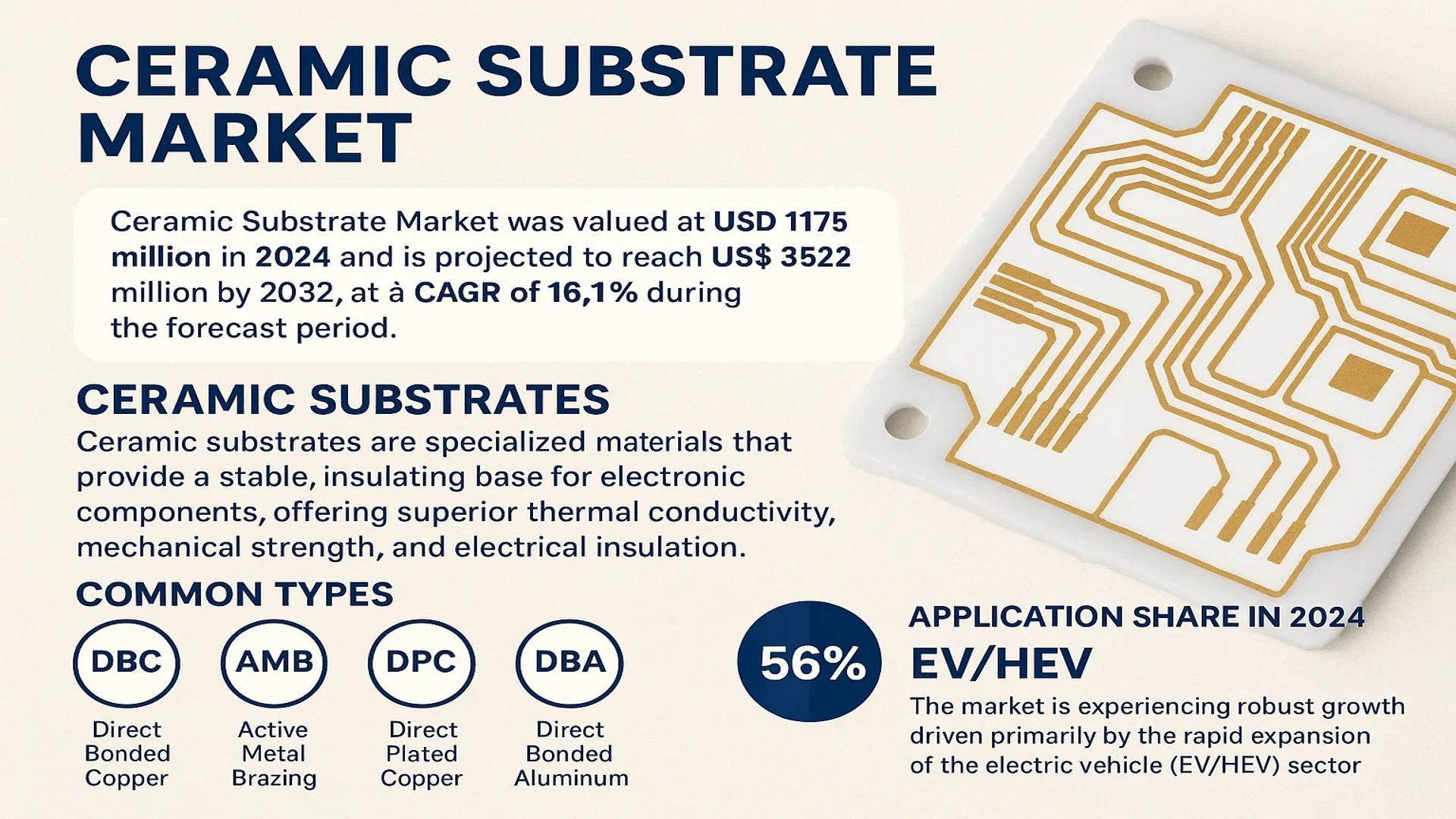

The global Ceramic Substrate Market was valued at 1175 million in 2024 and is projected to reach US$ 3522 million by 2032, at a CAGR of 16.1% during the forecast period.

Ceramic substrates are specialized materials that provide a stable, insulating base for electronic components, offering superior thermal conductivity, mechanical strength, and electrical insulation. These substrates are crucial for managing heat dissipation and ensuring reliability in high-power and high-frequency applications. Common types include DBC (Direct Bonded Copper), AMB (Active Metal Brazing), DPC (Direct Plated Copper), and DBA (Direct Bonded Aluminum), each tailored for specific performance requirements in various industries.

The market is experiencing robust growth driven primarily by the rapid expansion of the electric vehicle (EV/HEV) sector, which accounted for approximately 56% of the application share in 2024. Furthermore, increasing investments in renewable energy infrastructure, such as photovoltaic (PV) and wind power systems, are contributing significantly to demand. The Asia-Pacific region dominates the market, holding a 58% share, due to strong manufacturing bases and government support for electronics and automotive industries. Key players like Rogers Corporation, Jiangsu Fulehua Semiconductor Technology, and BYD are leading the market, with the top five companies collectively holding about 59% of the global market share.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Adoption of Electric Vehicles to Propel Ceramic Substrate Demand

The global shift toward electric vehicles represents a primary catalyst for ceramic substrate market expansion. These substrates are indispensable in EV power modules due to their superior thermal conductivity, electrical insulation, and mechanical stability under extreme conditions. With over 10 million electric vehicles sold worldwide in 2023 and projections indicating 45 million annual sales by 2030, the automotive sector’s reliance on ceramic substrates continues to intensify. The technology enables efficient heat dissipation in high-power electronic components, directly enhancing vehicle performance and battery longevity. Major automotive manufacturers are increasingly integrating advanced ceramic substrates in traction inverters, onboard chargers, and DC-DC converters, creating sustained demand across the value chain.

Expansion of 5G Infrastructure and High-Frequency Communications to Fuel Market Growth

The rapid deployment of 5G networks worldwide is driving substantial demand for ceramic substrates in RF power amplifiers and base station applications. These substrates provide critical performance advantages in high-frequency environments, including low signal loss, excellent thermal management, and stable dielectric properties. With approximately 2.5 million 5G base stations deployed globally and anticipated growth to over 7 million by 2027, the telecommunications sector represents a significant growth vector. Ceramic substrates enable higher power density and improved reliability in RF components, which is essential for meeting the stringent requirements of modern communication systems. The ongoing expansion of IoT devices and smart infrastructure further amplifies this demand, creating a robust foundation for market expansion.

Advancements in Renewable Energy Systems to Drive Ceramic Substrate Integration

Renewable energy applications, particularly in solar and wind power conversion systems, are emerging as significant drivers for ceramic substrate adoption. These substrates are critical components in power electronic systems that convert and manage energy in photovoltaic inverters and wind turbine converters. The global renewable energy capacity exceeded 3,500 gigawatts in 2023, with projections indicating a compound annual growth rate of approximately 12% through 2030. Ceramic substrates enable higher efficiency power conversion, reduced system size, and improved reliability in harsh environmental conditions. The increasing focus on grid modernization and energy storage systems further amplifies the need for advanced ceramic substrates that can handle higher power densities and operating temperatures.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Processes to Limit Market Penetration

Despite growing demand, ceramic substrate manufacturing involves sophisticated processes and substantial capital investment, creating significant cost barriers. The production requires specialized equipment for screen printing, high-temperature firing, and precision metallization, with manufacturing facilities typically requiring investments exceeding $100 million for advanced production lines. Raw material costs, particularly for high-purity alumina and aluminum nitride, remain elevated due to stringent quality requirements and limited supplier availability. These cost factors translate to higher final product prices, making ceramic substrates less competitive against alternative solutions in price-sensitive applications. The industry faces ongoing pressure to develop more cost-effective manufacturing techniques while maintaining the exceptional performance characteristics that define ceramic substrates.

Technical Challenges in Large-Scale Production to Constrain Market Expansion

Scaling ceramic substrate production while maintaining consistent quality presents substantial technical hurdles. The manufacturing process involves precise control of multiple parameters including temperature profiles, material composition, and dimensional stability during firing. Variations in these parameters can lead to defects such as warping, delamination, or inconsistent thermal properties, resulting in yield rates typically ranging between 75-85% for advanced substrates. The industry continues to face challenges in achieving perfect co-firing of ceramic and metal layers, particularly for larger substrate sizes required in high-power applications. These technical limitations affect production scalability and increase manufacturing costs, ultimately restricting market growth in applications where reliability and consistency are paramount.

Supply Chain Vulnerabilities and Raw Material Dependencies to Impede Market Stability

The ceramic substrate industry faces significant supply chain challenges related to specialized raw materials and manufacturing equipment. Key materials including high-purity ceramic powders, precious metal pastes, and specialized binders are sourced from limited suppliers worldwide, creating potential bottlenecks during periods of high demand. The industry experienced supply constraints during recent global events, with lead times for certain materials extending beyond six months. Additionally, manufacturing equipment for advanced ceramic substrates is highly specialized and primarily supplied by a handful of equipment manufacturers, creating dependencies that can affect production capacity expansion. These supply chain vulnerabilities introduce uncertainty in production planning and may limit the industry’s ability to respond rapidly to increasing market demand.

MARKET OPPORTUNITIES

Emerging Applications in Aerospace and Defense to Create New Growth Frontiers

The aerospace and defense sectors present substantial growth opportunities for advanced ceramic substrates, particularly in radar systems, electronic warfare, and satellite communications. These applications require substrates capable of operating in extreme environments with exceptional reliability and performance stability. The global defense electronics market is projected to reach $250 billion by 2028, driven by modernization programs and increased spending on advanced electronic systems. Ceramic substrates offer unique advantages in these applications, including resistance to high temperatures, radiation hardness, and superior high-frequency performance. Recent advancements in substrate materials and manufacturing techniques are enabling new applications in phased array radars, missile guidance systems, and space-based electronics, creating significant expansion opportunities for market participants.

Development of Next-Generation Semiconductor Packaging Technologies to Drive Innovation

Advanced semiconductor packaging represents a transformative opportunity for ceramic substrate manufacturers. The transition towards heterogeneous integration and 3D packaging architectures requires substrates with enhanced thermal management capabilities and superior electrical performance. The semiconductor packaging market is expected to grow at approximately 8% annually, reaching $50 billion by 2028. Ceramic substrates are increasingly being adopted in high-performance computing, artificial intelligence accelerators, and advanced sensor packaging where thermal density exceeds conventional solutions. Innovations in substrate design, including embedded components and multilayer architectures, are enabling higher integration density and improved system performance. This evolution in packaging technology creates new application spaces and technical requirements that align with the unique capabilities of advanced ceramic substrates.

Expansion in Medical Electronics and Healthcare Applications to Open New Markets

The medical electronics sector offers promising growth opportunities for ceramic substrates, particularly in diagnostic imaging, therapeutic equipment, and implantable devices. These applications demand substrates with exceptional reliability, biocompatibility, and performance stability in medical environments. The global medical electronics market is projected to exceed $90 billion by 2027, driven by technological advancements and increasing healthcare expenditure. Ceramic substrates are finding new applications in MRI systems, ultrasound equipment, and advanced surgical instruments where their electrical insulation properties and thermal management capabilities provide critical advantages. The growing adoption of minimally invasive surgical techniques and wearable medical devices further expands the addressable market for specialized ceramic substrates designed for medical applications.

MARKET CHALLENGES

Intense Competition from Alternative Substrate Technologies to Challenge Market Position

Ceramic substrates face increasing competition from advanced organic substrates and emerging technologies that offer cost advantages in certain applications. Organic substrates have made significant progress in thermal performance and reliability, capturing market share in consumer electronics and some automotive applications. The development of advanced thermal interface materials and cooling solutions has enabled organic substrates to address thermal challenges that previously required ceramic solutions. This competitive pressure forces ceramic substrate manufacturers to continuously innovate and demonstrate clear performance advantages to justify premium pricing. The industry must navigate this competitive landscape while maintaining investment in research and development to stay ahead of alternative technologies.

Other Challenges

Technical Standardization and Qualification Requirements

The absence of universal technical standards across applications creates challenges in product development and market entry. Different industries and customers have unique qualification requirements that necessitate extensive testing and certification processes. These requirements can extend product development cycles and increase time-to-market, particularly for new applications or emerging technologies. The industry must balance customization with standardization efforts to achieve economies of scale while meeting diverse customer requirements.

Environmental Regulations and Sustainability Considerations

Increasing environmental regulations regarding material usage, manufacturing processes, and end-of-life management present ongoing challenges. Ceramic substrate manufacturing involves energy-intensive processes and uses materials that may face regulatory scrutiny. The industry must address sustainability concerns through improved manufacturing efficiency, material recycling initiatives, and development of environmentally friendly alternatives while maintaining performance standards. These environmental considerations add complexity to product development and may affect cost structures across the value chain.

CERAMIC SUBSTRATE MARKET TRENDS

Electrification of Automotive and EV/HEV Sector Drives Unprecedented Demand

The global shift towards vehicle electrification represents the most powerful trend shaping the ceramic substrate market. With over 56% of the market’s application share, the automotive and electric/hybrid electric vehicle (EV/HEV) sector is the primary growth engine. This surge is directly tied to the critical role ceramic substrates play in power electronics, particularly in Insulated Gate Bipolar Transistors (IGBTs) and power modules that manage high voltages and currents in electric drivetrains. The superior thermal conductivity, electrical insulation, and mechanical strength of materials like Aluminum Nitride (AlN) and Alumina (Al2O3) make them indispensable for managing the intense heat generated in these applications. As global electric vehicle sales are projected to exceed 16 million units annually by 2024, the demand for reliable, high-performance ceramic substrates is scaling proportionally, compelling manufacturers to expand production capacity to meet the needs of major automotive suppliers.

Other Trends

Technological Advancements in Substrate Manufacturing

While automotive demand grows, technological innovation in manufacturing processes is crucial for meeting performance and cost requirements. Significant R&D investment is focused on refining Direct Bonded Copper (DBC) and Active Metal Brazing (AMB) technologies. AMB substrates, in particular, are gaining substantial traction because they offer superior thermal cycling performance and higher reliability compared to traditional DBC, especially in high-power applications where thermal stress is a major concern. This has led to their increased adoption in the renewable energy sector for solar inverters and wind power converters. Furthermore, advancements in laser drilling and metallization techniques for Direct Plated Copper (DPC) substrates are enabling more complex and miniaturized circuit patterns, which is critical for the next generation of high-density power modules and radio frequency (RF) devices used in 5G infrastructure.

Expansion into Renewable Energy and High-Power Industrial Applications

The expansion of renewable energy infrastructure is another major trend driving market diversification. Ceramic substrates are fundamental components in photovoltaic (PV) inverters and converters for wind power systems, which require components that can operate efficiently under high power and harsh environmental conditions. The global push for clean energy, with annual investments in renewables surpassing $500 billion, directly fuels demand for these high-reliability electronic materials. Furthermore, the industrial sector continues to be a stable and growing consumer, utilizing ceramic substrates in motor drives, uninterruptible power supplies (UPS), and industrial automation systems that demand robust thermal management. This diversification beyond automotive helps to stabilize the market against sector-specific fluctuations and opens new avenues for growth in high-temperature and high-frequency applications that are unsuitable for conventional printed circuit boards.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global ceramic substrate market is semi-consolidated, characterized by a mix of large multinational corporations, specialized medium-sized enterprises, and emerging regional players. Rogers Corporation stands as a dominant force, primarily due to its technologically advanced product portfolio, particularly in the DBC (Direct Bonded Copper) and AMB (Active Metal Brazed) segments, and its extensive global distribution network across North America, Europe, and Asia-Pacific. The company’s stronghold is further solidified by its strategic focus on high-growth applications like automotive and renewable energy.

Jiangsu Fulehua Semiconductor Technology and Tong Hsing also command significant market share, largely attributed to their deep-rooted presence in the Asia-Pacific region, which accounts for approximately 58% of the global market. Their growth is fueled by robust manufacturing capabilities, cost-competitive offerings, and strong relationships with local automotive and industrial electronics manufacturers. These players are increasingly investing in R&D to enhance their product performance and reliability to compete on a global scale.

Furthermore, these leading companies are actively pursuing growth through strategic initiatives such as capacity expansions, technological partnerships, and new product launches tailored for the burgeoning electric vehicle sector, which constitutes the largest application segment at 56%. This aggressive expansion is expected to further consolidate their market positions over the forecast period.

Meanwhile, other key players like Heraeus Electronics and Kyocera are strengthening their market presence through significant investments in research and development, focusing on next-generation substrates for 5G communication, advanced driver-assistance systems (ADAS), and high-power LED applications. Their strategy involves developing substrates with higher thermal conductivity, improved mechanical strength, and superior reliability to meet the evolving demands of high-performance electronics.

List of Key Ceramic Substrate Companies Profiled

- Rogers Corporation (U.S.)

- Jiangsu Fulehua Semiconductor Technology Co., Ltd. (China)

- BYD Company Ltd. (China)

- Tong Hsing Electronic Industries, Ltd. (Taiwan)

- Heraeus Electronics (Germany)

- NGK Electronics Devices, Inc. (Japan)

- KCC Corporation (South Korea)

- Toshiba Materials Co., Ltd. (Japan)

- Denka Company Limited (Japan)

- Kyocera Corporation (Japan)

- Mitsubishi Materials Corporation (Japan)

- Maruwa Co., Ltd. (Japan)

Segment Analysis:

By Type

DBC Ceramic Substrate Segment Dominates the Market Due to Superior Thermal Performance and High Reliability in Power Electronics

The market is segmented based on type into:

- DBC Ceramic Substrate

- Subtypes: Alumina DBC, Aluminum Nitride DBC, and others

- AMB Ceramic Substrate

- DPC Ceramic Substrate

- DBA Ceramic Substrate

- Others

By Application

Automotive & EV/HEV Segment Leads Due to Massive Adoption in Power Modules, Inverters, and Battery Management Systems

The market is segmented based on application into:

- Automotive & EV/HEV

- PV and Wind Power

- Industrial

- Consumer Appliance

- Rail Transport

- Military & Aerospace

- LED

- Laser and Optical Communication

- Others

By Material

Alumina (Al2O3) Substrates Hold a Significant Share Owing to their Cost-Effectiveness and Widespread Availability

The market is segmented based on material into:

- Alumina (Al2O3)

- Aluminum Nitride (AlN)

- Silicon Nitride (Si3N4)

- Beryllium Oxide (BeO)

- Others

By End-User Industry

Electronics and Semiconductor Manufacturing is a Principal End-User Industry Driving Demand for High-Performance Substrates

The market is segmented based on end-user industry into:

- Electronics and Semiconductor Manufacturing

- Automotive

- Telecommunications

- Energy and Power

- Aerospace and Defense

- Others

Regional Analysis: Ceramic Substrate Market

Asia-Pacific

Asia-Pacific is the dominant global market for ceramic substrates, holding approximately 58% of the total market share. This leadership is primarily driven by China, which is the world’s largest producer and consumer, followed by significant contributions from Japan, South Korea, and India. The region’s supremacy is anchored in its massive electronics manufacturing ecosystem and the world’s most aggressive push for electric vehicle (EV) adoption. China’s “Made in China 2025” initiative and substantial government subsidies for EVs have created immense demand for DBC (Direct Bonded Copper) and AMB (Active Metal Brazed) substrates used in power modules. Furthermore, the region is home to leading manufacturers like Jiangsu Fulehua Semiconductor Technology, BYD, and Tong Hsing, whose extensive production capacities and cost-competitive offerings solidify the region’s pivotal role. The relentless expansion of 5G infrastructure, consumer electronics production, and renewable energy projects continues to fuel robust growth, making Asia-Pacific the undisputed engine of the global ceramic substrate industry.

Europe

Europe represents the second-largest market with a share of about 30%, characterized by a strong emphasis on high-performance and technologically advanced ceramic substrates. The region’s stringent automotive emissions regulations and ambitious green energy targets, such as the EU’s Fit for 55 package, are key drivers. This has accelerated the adoption of EVs and investments in PV and wind power infrastructure, directly increasing demand for reliable ceramic substrates in power electronics. Germany, a hub for automotive excellence, and countries like Italy and France are at the forefront of this demand. The presence of major players like Heraeus Electronics and a strong focus on research and development in materials science fosters innovation, particularly in substrates for demanding applications in aerospace and industrial automation. The market is defined by a preference for quality, reliability, and compliance with rigorous EU environmental and safety standards.

North America

Holding an 11% share of the global market, North America is a significant and technologically advanced region. Demand is heavily influenced by the well-established aerospace, defense, and telecommunications sectors in the United States and Canada. The region’s push towards electrification, supported by policies like the U.S. Inflation Reduction Act, is also spurring growth in the automotive & EV/HEV segment. Key North American-based companies, such as Rogers Corporation, are global technology leaders, specializing in high-end substrates for critical applications in radar systems, electric vehicle power trains, and high-frequency communication devices. While production volume may be lower than in Asia-Pacific, the region competes effectively through innovation, intellectual property, and a focus on high-value, specialized substrates that command premium prices.

South America

The ceramic substrate market in South America is nascent but presents long-term growth potential. Current demand is primarily fueled by the gradual modernization of industrial automation and consumer electronics markets in countries like Brazil and Argentina. However, the adoption of advanced ceramic substrates, particularly for EVs and renewable energy, is hindered by economic volatility, less developed manufacturing supply chains, and slower regulatory pushes for electrification compared to other regions. The market currently relies heavily on imports, and while local assembly of electronics provides some demand, widespread growth is contingent on greater economic stability and targeted industrial policies that encourage local production and technology adoption.

Middle East & Africa

This region represents an emerging market with minimal current share but future potential. Development is largely focused on specific nations investing in technological infrastructure, such as Israel, Turkey, and the UAE. Demand stems from telecommunications infrastructure projects, oil & gas industry automation, and modest consumer electronics markets. However, the lack of a local manufacturing base for advanced electronics and ceramic substrates means the market is almost entirely import-dependent. Growth is slow and is directly tied to national economic diversification plans and foreign investment in technology sectors. The high cost of advanced substrates and a focus on more immediate infrastructure needs currently limit widespread market penetration.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Ceramic Substrate markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ceramic Substrate Market?

-> Ceramic Substrate Market was valued at 1175 million in 2024 and is projected to reach US$ 3522 million by 2032, at a CAGR of 16.1% during the forecast period.

Which key companies operate in Global Ceramic Substrate Market?

-> Key players include Rogers, Jiangsu Fulehua Semiconductor Technology, BYD, Tong Hsing, and Heraeus Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include the rapid expansion of the electric vehicle industry, increasing demand for high-power electronics, and advancements in 5G and LED technologies.

Which region dominates the market?

-> Asia-Pacific is the dominant market, holding a share of approximately 58%, driven by strong manufacturing bases in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include the development of advanced AMB substrates, integration of ceramic substrates in wide-bandgap semiconductors, and increasing adoption in renewable energy applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...