Ceramic capacitor flex crack mitigation for automotive ECU Market Insights

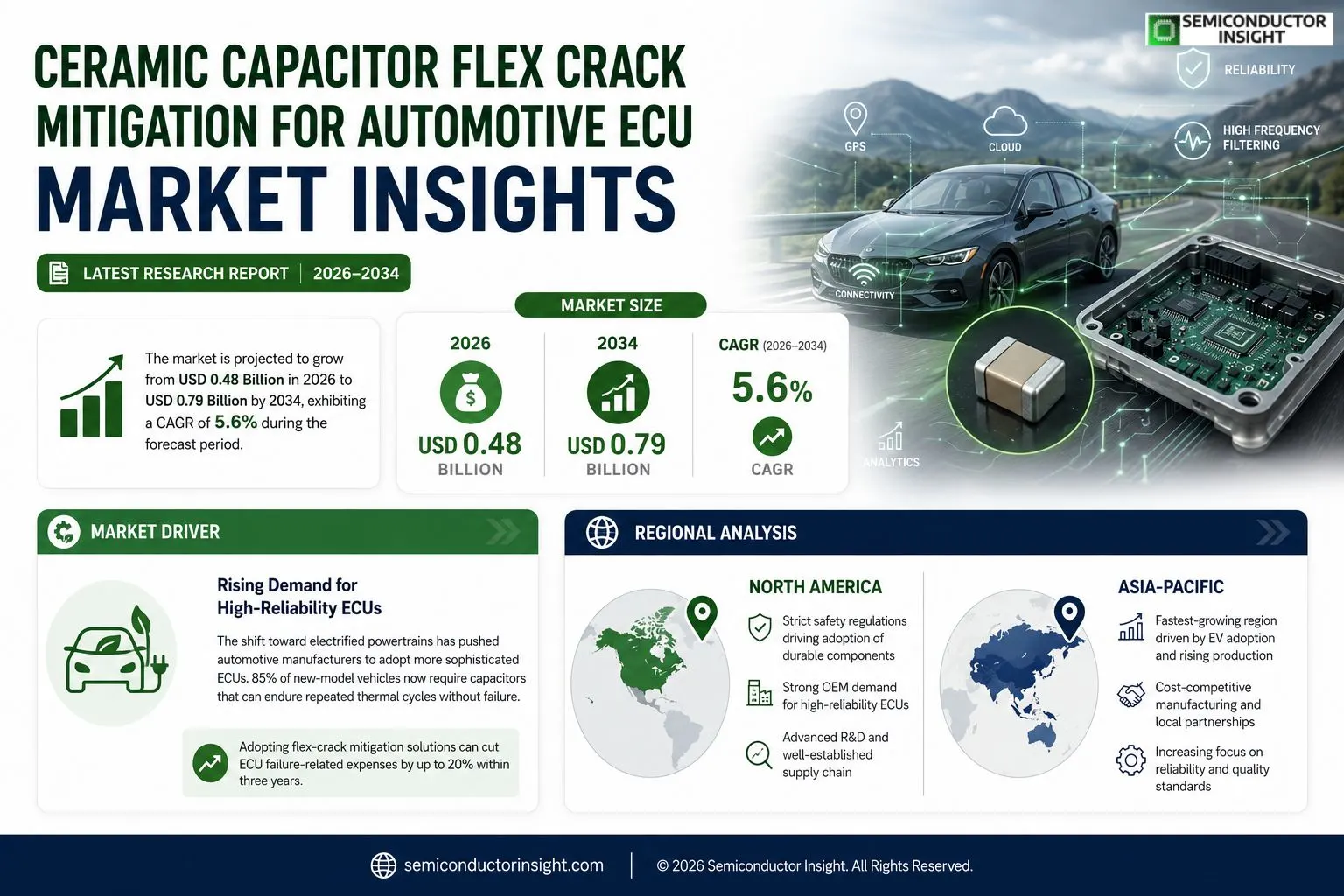

Ceramic capacitor flex crack mitigation for automotive ECU market size was valued at USD 0.46 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 0.79 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period.

Ceramic capacitors are integral components within electronic control units (ECUs), providing high‑frequency filtering and voltage regulation. Flex‑crack mitigation refers to design and material strategiessuch as reinforced terminations, optimized mounting techniques, and stress‑relief coatingsthat prevent micro‑fractures caused by thermal expansion and mechanical vibration.The market is experiencing accelerated growth because vehicle electrification intensifies demand for reliable ECUs, while stringent safety standards push manufacturers toward robust cracking‑prevention solutions. Furthermore, advances in low‑temperature co‑fire processes and predictive failure analytics enable longer service life, prompting major suppliers like KEMET Corporation, Murata Manufacturing, AVX Corp., and TDK Electronics to expand their product portfolios.

MARKET DRIVERS

Rising Demand for High‑Reliability ECUs

The shift toward electrified powertrains has pushed automotive manufacturers to adopt more sophisticated electronic control units (ECUs). Ceramic capacitor flex crack mitigation for automotive ECU Market is gaining traction as 85% of new‑model vehicles now require capacitors that can endure repeated thermal cycles without failure.

Regulatory Push for Durability

Stringent durability standards in key regions mandate a 30% reduction in field failure rates for critical components. This regulatory pressure drives OEMs to invest in crack‑resistant Ceramic capacitor technologies that promise longer service life and lower warranty costs.

➤ “Adopting flex‑crack mitigation solutions can cut ECU failure‑related expenses by up to 20% within three years.”

Leading semiconductor suppliers are expanding R&D budgets by an estimated $150 million annually to refine material compositions and design geometries, further accelerating market adoption.

MARKET CHALLENGES

Thermal and Mechanical Stress Management

ECUs operate in environments where temperature swings exceed 150 °C and vibration levels reach 10 g. These conditions accelerate micro‑crack formation in traditional Ceramic capacitors, making mitigation technologies essential yet technically complex.

Other Challenges

Material Compatibility

Integrating advanced Ceramic formulations with existing copper‑clad substrates often requires redesign of PCB stack‑ups, adding engineering lead time and increasing production costs.

MARKET RESTRAINTS

High Cost of Advanced Materials

Specialized high‑purity Ceramics and nano‑coating processes command premium prices, limiting adoption among cost‑sensitive Tier‑2 suppliers. The average unit cost remains 45% higher than conventional capacitors.Furthermore, the limited number of qualified vendors creates supply‑chain bottlenecks, constraining volume scalability for large‑scale OEM programs.

MARKET OPPORTUNITIES

Emerging Nano‑Coating Solutions

Recent breakthroughs in atomic‑layer deposition enable ultra‑thin, crack‑blocking coatings that preserve capacitance while enhancing flex resilience. Early pilot projects report a 40% improvement in crack‑initiation resistance.Collaborative initiatives between major OEMs and capacitor manufacturers are creating dedicated development programs, positioning Ceramic capacitor flex crack mitigation for automotive ECU Market for accelerated growth through 2028.

Ceramic capacitor flex crack mitigation for automotive ECU Market Trends

Growing Reliability Requirements in Electrified Vehicles

The automotive industry’s shift toward electrified powertrains is placing unprecedented reliability demands on electronic control units (ECUs). As voltage spikes and thermal cycles become more pronounced, designers are prioritizing flex‑crack mitigation to safeguard Ceramic capacitors that perform high‑frequency filtering and voltage regulation. Regulatory bodies have tightened safety standards, prompting OEMs to adopt robust stress‑relief strategies that extend component life and reduce warranty claims. Industry analysts observe a steady adoption curve for these mitigation techniques, driven by the need to maintain uptime in complex drive‑by‑wire systems and to meet consumer expectations for long‑lasting electric vehicles.

Other Trends

Advanced Material and Process Innovations

Suppliers are introducing reinforced terminations and low‑temperature co‑fire Ceramic formulations that directly address micro‑fracture initiation. Stress‑relief coating technologies, applied during the final assembly stage, create a compliant interface that absorbs vibration and thermal expansion mismatches. Concurrently, predictive failure analytics, leveraging real‑time sensor data from ECUs, enable manufacturers to anticipate crack propagation and schedule preventative maintenance before failure occurs. These material and process advances collectively improve the durability of capacitors in harsh automotive environments without requiring major redesigns of existing PCB layouts.

Competitive Landscape and Portfolio Expansion

Major component manufacturers such as KEMET, Murata, AVX, and TDK have broadened their product lines to include dedicated flex‑crack‑mitigation solutions, integrating reinforced terminations and specialized mounting hardware. The competitive pressure is encouraging rapid iteration of design guidelines that incorporate these mitigation features as standard practice. As predictive analytics become more embedded in vehicle health monitoring platforms, manufacturers are aligning their R&D roadmaps to support data‑driven reliability enhancements. This convergence of material science, analytical tooling, and market demand is reinforcing a trajectory of continuous improvement for Ceramic capacitor flex crack mitigation for automotive ECU Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Ceramic Capacitor Flex‑Crack Mitigation in Automotive ECUs

At the forefront of the automotive ECU Ceramic capacitor market, KEMET Corporation leads with a comprehensive flex‑crack mitigation portfolio that combines reinforced terminations, low‑temperature co‑fire processes, and proprietary stress‑relief coatings. KEMET’s supply chain and deep automotive qualification programs enable it to capture a disproportionate share of high‑volume power‑train and chassis ECU contracts, driving market consolidation around a few Tier‑1 suppliers. Murata Manufacturing and AVX Corp. follow closely, leveraging extensive R&D investment to introduce thin‑film Ceramic solutions that meet the latest ISO‑26262 safety requirements. Together, these three firms shape pricing dynamics, set reliability benchmarks, and influence OEM specification standards, creating a competitive structure where scale, compliance expertise, and innovative packaging dominate.Beyond the dominant trio, a diverse group of niche players contributes specialized technologies that address emerging failure modes. TDK Electronics offers advanced dielectric materials for high‑temperature resilience, while Vishay Intertechnology focuses on high‑Q factor devices for noise‑sensitive infotainment ECUs. Kyocera’s Ceramic substrates provide superior mechanical toughness, and NXP and Infineon integrate capacitor modules directly into system‑in‑package (SiP) architectures for tighter space constraints. Smaller yet influential firms such as Samsung Electro‑Mechanics, Taiyo Yuden, EPCOS (a TDK subsidiary), and ROHM Semiconductor supply region‑specific variants that address local automotive standards, fostering a highly fragmented but technically sophisticated ecosystem.

List of Key Ceramic Capacitor Flex‑Crack Mitigation for Automotive ECU Companies Profiled

- KEMET Corporation

- Murata Manufacturing

- AVX Corp.

- TDK Electronics

- Vishay Intertechnology

- Kyocera Corporation

- NXP Semiconductors

- Infineon Technologies

- Samsung Electro‑Mechanics

- Taiyo Yuden

- EPCOS (TDK subsidiary)

- ROHM Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multilayer Ceramic Capacitors (MLCC)

|

| By Application |

|

Advanced Driver Assistance Systems (ADAS)

|

| By End User |

|

Premium Vehicle Manufacturers

|

| By Mitigation Technique |

|

Reinforced Termination Designs

|

| By Market Driver |

|

Vehicle Electrification

|

Regional Analysis: Ceramic capacitor flex crack mitigation for automotive ECU Market

North America

Federal safety directives require higher reliability for electronic control units, prompting manufacturers to integrate flex‑crack mitigation solutions. Continuous updates to emissions and crash‑worthiness standards indirectly drive adoption of robust Ceramic capacitors, reinforcing market momentum across passenger‑car and commercial‑vehicle segments.

Leading OEMs seek components that can endure aggressive power‑train cycles in electric and hybrid vehicles. Their procurement policies favor suppliers offering proven crack‑resistance, leading to deeper collaboration on design‑for‑reliability initiatives and accelerated product qualification cycles.

A well‑established supply chain with multiple tier‑1 capacitor manufacturers ensures rapid scaling of production volumes. Proximity to key assembly plants reduces lead times, allowing quick implementation of mitigation technologies in new vehicle platforms.

Significant funding is directed toward nano‑scale Ceramic materials and stress‑distribution modeling. These research efforts aim to enhance fracture toughness while preserving electrical performance, positioning North America at the forefront of innovation in capacitor reliability.

Europe

European automotive manufacturers are emphasizing sustainability and component longevity, aligning closely with the EU’s circular‑economy agenda. As manufacturers transition to electrified powertrains, the need for dependable Ceramic capacitors becomes more pronounced, especially in high‑performance ECUs subject to frequent thermal variations. Collaborative projects between automotive clusters in Germany and research hubs in France focus on integrating flex‑crack mitigation during the early design phase, reducing warranty claims and improving overall vehicle safety. The region’s regulatory environment, which enforces rigorous durability testing, further incentivizes the adoption of advanced capacitor technologies, positioning Europe as a strong secondary market for these solutions.

Asia‑Pacific

Asia‑Pacific showcases rapid growth driven by expanding automotive production capacities in China, India, and Southeast Asia. While cost considerations remain paramount, OEMs are increasingly recognizing the long‑term value of robust Ceramic capacitors to avoid field failures in high‑volume models. Local suppliers are partnering with technology firms to co‑develop flex‑crack mitigation processes that balance performance with price competitiveness. Government incentives for electric vehicle adoption also stimulate demand for reliable ECU components, prompting a gradual shift toward higher‑quality Ceramic solutions across the region’s diverse market segments.

South America

In South America, emerging automotive markets are modernizing their production lines, creating opportunities for advanced component technologies. Although the overall market size remains modest, regional manufacturers are beginning to align with international reliability standards, especially for imported vehicle platforms. Partnerships with North American and European capacitor producers facilitate technology transfer, enabling local assembly of flex‑crack‑mitigated capacitors that meet quality benchmarks. This incremental adoption supports a steady rise in demand as vehicle fleets become increasingly sophisticated.

Middle East & Africa

The Middle East and Africa region experiences niche growth as luxury and commercial vehicle segments adopt stricter reliability criteria. Harsh climatic conditions, such as extreme heat and dust, heighten the importance of robust capacitor design to prevent flex‑crack failures in ECUs. Regional distributors are sourcing from established suppliers that can certify long‑term performance under these stresses. While overall volumes are limited, the strategic focus on high‑value applications drives a concentrated demand for advanced Ceramic capacitor mitigation technologies.

Report Scope

This market research report provides a comprehensive analysis of the Ceramic capacitor flex crack mitigation for automotive ECU Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Ceramic capacitor flex crack mitigation for automotive ECU Market?

-> Ceramic capacitor flex crack mitigation for automotive ECU Market was valued at USD 0.46 billion in 2025 and is expected to reach USD 0.79 billion by 2034.

Which key companies operate in Ceramic capacitor flex crack mitigation for automotive ECU Market?

-> Key players include KEMET Corporation, Murata Manufacturing, AVX Corp., TDK Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include vehicle electrification, stringent safety standards, and demand for reliable ECUs.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include low‑temperature co‑fire processes, predictive failure analytics, and advanced stress‑relief coating technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...