Capacitor discharge welding energy storage electrolytic Market Insights

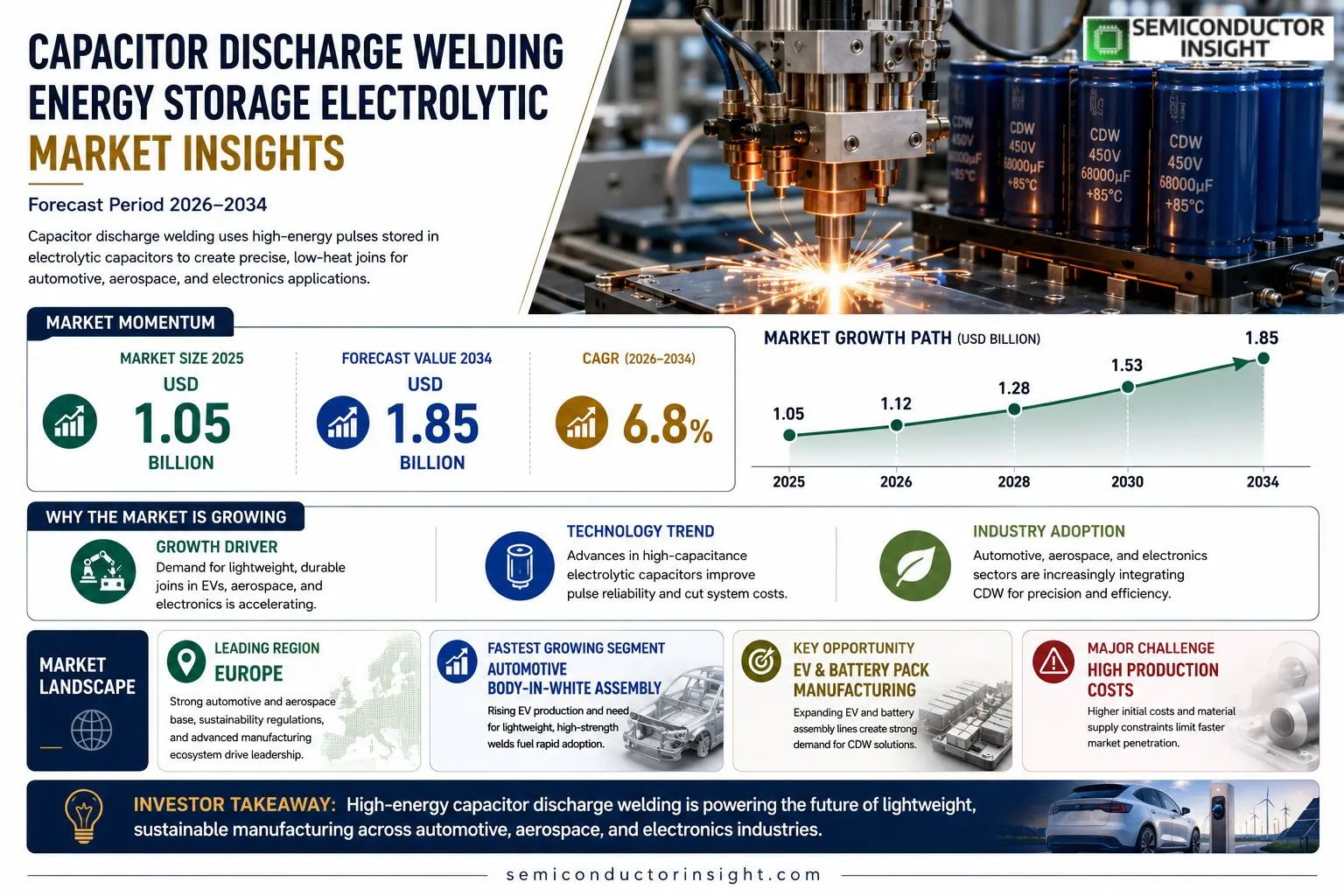

Capacitor discharge welding energy storage electrolytic market size was valued at USD 1.05 billion in 2025. The market is projected to grow from USD 1.12 billion in 2026 to USD 1.85 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

Capacitor discharge welding (CDW) employs high‑energy pulses stored in electrolytic Capacitors to join conductive materials instantly without external heat sources. This process delivers precise joins with minimal thermal distortion, making it ideal for thin‑walled components used in automotive, aerospace and electronics manufacturing.The market is experiencing rapid growth because manufacturers are pursuing lightweight yet durable assembly methods for electric‑vehicle bodies and battery packs. Furthermore, advances in high‑capacitance electrolytic devices are reducing system costs while enhancing pulse reliability. However, competition from laser and friction stir welding persists; nevertheless, strategic collaborationssuch as the March 2024 partnership between Schunk Group and TDK on next‑generation CDW modulesare expected to accelerate adoption.

MARKET DRIVERS

Growing Adoption of Advanced Welding Technologies

Capacitor discharge welding energy storage electrolytic Market is being propelled by manufacturing sectors that require rapid burst power for spot‑welding and resistance‑welding processes. Electrolytic Capacitors provide high discharge rates with minimal voltage droop, enabling tighter weld seams and higher production throughput.

Regulatory Push for Energy‑Efficient Manufacturing

Environmental regulations across Europe and North America are mandating lower energy consumption per unit produced. Electrolytic energy‑storage solutions reduce standby losses compared with traditional battery packs, helping facilities meet sustainability targets while maintaining weld quality.

➤ “Integrating electrolytic Capacitors into welding lines has cut cycle time by up to 30 % without sacrificing joint strength,”

These drivers collectively create a robust demand pipeline, encouraging OEMs and system integrators to invest in next‑generation Capacitor discharge welding platforms.

MARKET CHALLENGES

Technical Limitations in High‑Current Applications

While electrolytic Capacitors excel in rapid discharge, their ripple current capability can be a limiting factor for ultra‑high‑current welding stations. Engineers must carefully design thermal management systems to avoid overheating, which adds complexity and cost.

Other Challenges

Cost Sensitivity

The initial capital outlay for high‑performance electrolytic modules remains higher than conventional battery solutions, making price‑sensitive manufacturers hesitant to transition quickly.

MARKET RESTRAINTS

Material Availability Constraints

Supply chains for high‑purity aluminum and electrolyte chemicals have experienced volatility, which can delay production of Capacitors. These material bottlenecks restrict the ability of suppliers to scale up to meet sudden spikes in demand within Capacitor discharge welding energy storage electrolytic Market.

MARKET OPPORTUNITIES

Emerging Markets in Automotive Electronics

Electric‑vehicle manufacturers are incorporating spot‑welding cells for battery pack assembly, where precise, high‑energy bursts are critical. The rise of these assembly lines offers a clear growth pathway for electrolytic Capacitor solutions, positioning Capacitor discharge welding energy storage electrolytic Market for accelerated expansion.

Capacitor discharge welding energy storage electrolytic Market Trends

Growing Adoption in Electric‑Vehicle Assembly

The sector is witnessing accelerated uptake of Capacitor discharge welding (CDW) as manufacturers target lightweight yet robust joining solutions for electric‑vehicle bodies and battery modules. By delivering high‑energy pulses from electrolytic Capacitors, CDW creates precise welds with minimal heat input, thereby preserving thin‑walled structural integrity. Automotive OEMs are integrating CDW lines to reduce assembly cycle times and to meet stringent weight‑reduction targets essential for range improvement. Parallel trends in aerospace are encouraging the use of CDW for rivet‑free fuselage panels, where thermal distortion must be limited. The technology’s inherent repeatability also supports the high‑volume production required for next‑generation mobility platforms, positioning CDW as a strategic alternative to conventional thermal welding processes.

Other Trends

Advances in Electrolytic Capacitor Technology

Recent developments in high‑capacitance electrolytic devices are reshaping cost structures and performance expectations. Manufacturers report that newer Capacitor chemistries provide higher pulse energy density while maintaining compact form factors, which lowers the overall system footprint on production lines. Improved dielectric stability translates into longer component lifetimes and reduced maintenance intervals, enhancing the total cost of ownership for end users. These technical gains are reinforced by collaborative R&D programs, notably the March 2024 partnership between Schunk Group and TDK, which aims to scale next‑generation CDW modules for broader industrial adoption. As reliability data accumulate, early‑stage skepticism among conservative adopters diminishes, encouraging wider penetration across automotive and aerospace supply chains.

Competitive Landscape and Sustainability Drivers

While laser and friction‑stir welding retain strong market positions, CDW’s low‑energy footprint and ability to join dissimilar metals without auxiliary heating are gaining regulatory attention. Environmental standards increasingly favor processes that reduce auxiliary power consumption and emissions, and CDW aligns with these objectives by eliminating the need for supplemental heating sources. Furthermore, the modular nature of Capacitor‑based systems simplifies retrofitting of existing assembly cells, offering a cost‑effective pathway for manufacturers seeking to upgrade without extensive re‑tooling. Looking ahead, the convergence of material‑science breakthroughs and strategic alliances is expected to sustain the upward trajectory of the market, reinforcing CDW’s role as a cornerstone technology for next‑generation manufacturing.

COMPETITIVE LANDSCAPE

Key Industry Players

Capacitor Discharge Welding Energy Storage Electrolytic Market – Competitive Landscape

Capacitor discharge welding (CDW) energy‑storage electrolytic market was valued at approximately USD 1.05 billion in 2025 and is forecast to reach USD 1.85 billion by 2034, driven by a robust CAGR of 6.8 %. Leading firms such as Schunk Group, TDK, KEMET and AVX dominate the high‑performance Capacitor segment, leveraging extensive manufacturing capacity and deep R&D pipelines. These incumbents benefit from vertically integrated supply chains that couple electrolytic Capacitor production with precision welding module assembly, creating a barrier to entry for smaller specialists. Market structure is bifurcated between large multinational conglomerates controlling >60 % of volume and a fragmented cohort of niche players that focus on ultra‑high‑capacitance devices for aerospace and electric‑vehicle battery pack applications.Beyond the headline leaders, a cadre of niche manufacturersNichicon, Vishay, Panasonic, Murata, Cornell Dubilier, Hitachi, Samsung Electro‑Mechanics, Ohio Capacitor, EPCOS (a TDK subsidiary) and LRCcontribute innovative cell chemistries and form‑factor options that address specific thermal‑management challenges. Strategic collaborations are reshaping the competitive set; the March 2024 partnership between Schunk Group and TDK to co‑develop next‑generation CDW modules exemplifies how joint‑venture R&D accelerates technology diffusion while moderating cost pressures from laser and friction‑stir alternatives. These alliances, combined with expanding application footprints in automotive lightweighting and aerospace assembly, are intensifying competition and fostering a dynamic, innovation‑focused ecosystem.

List of Key Capacitor Discharge Welding Energy Storage Electrolytic Companies Profiled

- Schunk Group

- TDK

- KEMET Corporation

- AVX (Kyocera AVX)

- Vishay Intertechnology

- Panasonic Corporation

- Murata Manufacturing Co., Ltd.

- Cornell Dubilier Electronics

- Hitachi Metals, Ltd.

- Samsung Electro‑Mechanics

- Ohio Capacitor, Inc.

- EPCOS (TDK subsidiary)

- LRC (Linear Resonant Converter)

- Nichicon Corporation

- United Chemi-Con Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Electrolytic Capacitors

|

| By Application |

|

Automotive Body-in-White Assembly

|

| By End User |

|

Original Equipment Manufacturers (OEMs)

|

| By Technology |

|

High‑Capacitance Electrolytic Modules

|

| By Market Driver |

|

Lightweight Vehicle Construction

|

Regional Analysis: Capacitor discharge welding energy storage electrolytic Market

Europe

The European Union’s tightening of CO₂ emission standards has accelerated the adoption of low‑energy welding technologies. Incentive programs for eco‑friendly manufacturing encourage firms to replace legacy equipment with Capacitor discharge solutions, aligning compliance with cost‑effective production.

Germany’s Baden‑Wurttemberg and Italy’s Lombardy host clusters of OEMs and component suppliers that prioritize high‑precision welding. These hubs benefit from close collaboration between manufacturers, universities, and technology providers, fostering rapid diffusion of Capacitor‑based systems.

European research consortia focus on enhancing pulse control and electrolyte formulations, delivering greater energy density and longer component lifespan. Patent activity reflects a steady flow of incremental improvements rather than disruptive breakthroughs.

A mature supply chain of specialty electrolytes, high‑purity Capacitors, and precision machining services underpins market stability. Local sourcing reduces lead times and supports the region’s push for resilient, low‑carbon manufacturing networks.

North America

North America remains a significant secondary market, with the United States leading adoption in the automotive and defense sectors. Companies are attracted by the potential to lower operational costs and meet voluntary sustainability targets. While regulatory pressure is less stringent than in Europe, industry groups promote best practices that favor Capacitor discharge welding for its repeatability and reduced downstream finishing requirements.

Asia‑Pacific

The Asia‑Pacific region shows rapid expansion, driven by high‑volume production in China, Japan, and South Korea. Manufacturers seek to improve throughput and energy efficiency in electronics assembly and consumer‑goods fabrication. Although cost considerations dominate, growing environmental awareness is prompting early trials of electrolytic Capacitor‑based welding in select facilities.

South America

In South America, Brazil and Argentina are the primary adopters, primarily within the automotive components supply chain. Market growth is cautious, reflecting limited local expertise and reliance on imported technology. Nevertheless, strategic partnerships with European firms are introducing Capacitor discharge welding concepts to improve product quality.

Middle East & Africa

The Middle East & Africa region exhibits modest uptake, focused on oil‑field equipment and shipbuilding where high‑strength welds are essential. Investment in training and localized service networks is gradually building confidence in Capacitor discharge solutions, positioning the region for incremental adoption over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the Capacitor discharge welding energy storage electrolytic Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Capacitor discharge welding energy storage electrolytic Market?

-> Capacitor discharge welding energy storage electrolytic Market was valued at USD 1.05 billion in 2025 and is expected to reach USD 1.85 billion by 2034. The market is projected to grow from USD 1.12 billion in 2026 to the 2034 level, reflecting a CAGR of 6.8% during the forecast period.

Which key companies operate in Capacitor discharge welding energy storage electrolytic Market?

-> Key players include Schunk Group and TDK, among others, as highlighted by their March 2024 strategic partnership on next‑generation CDW modules.

What are the key growth drivers?

-> Key growth drivers include the pursuit of lightweight yet durable assembly methods for electric‑vehicle bodies and battery packs, advances in high‑capacitance electrolytic Capacitors that reduce system costs and improve pulse reliability, and strategic collaborations such as the Schunk Group‑TDK partnership accelerating technology adoption.

Which region dominates the market?

-> The reference material does not specify a dominant region for the market.

What are the emerging trends?

-> Emerging trends include development of next‑generation CDW modules through collaborations, integration of higher‑capacitance electrolytic devices to enhance pulse performance, and broader adoption of CDW in automotive and aerospace applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...