MARKET INSIGHTS

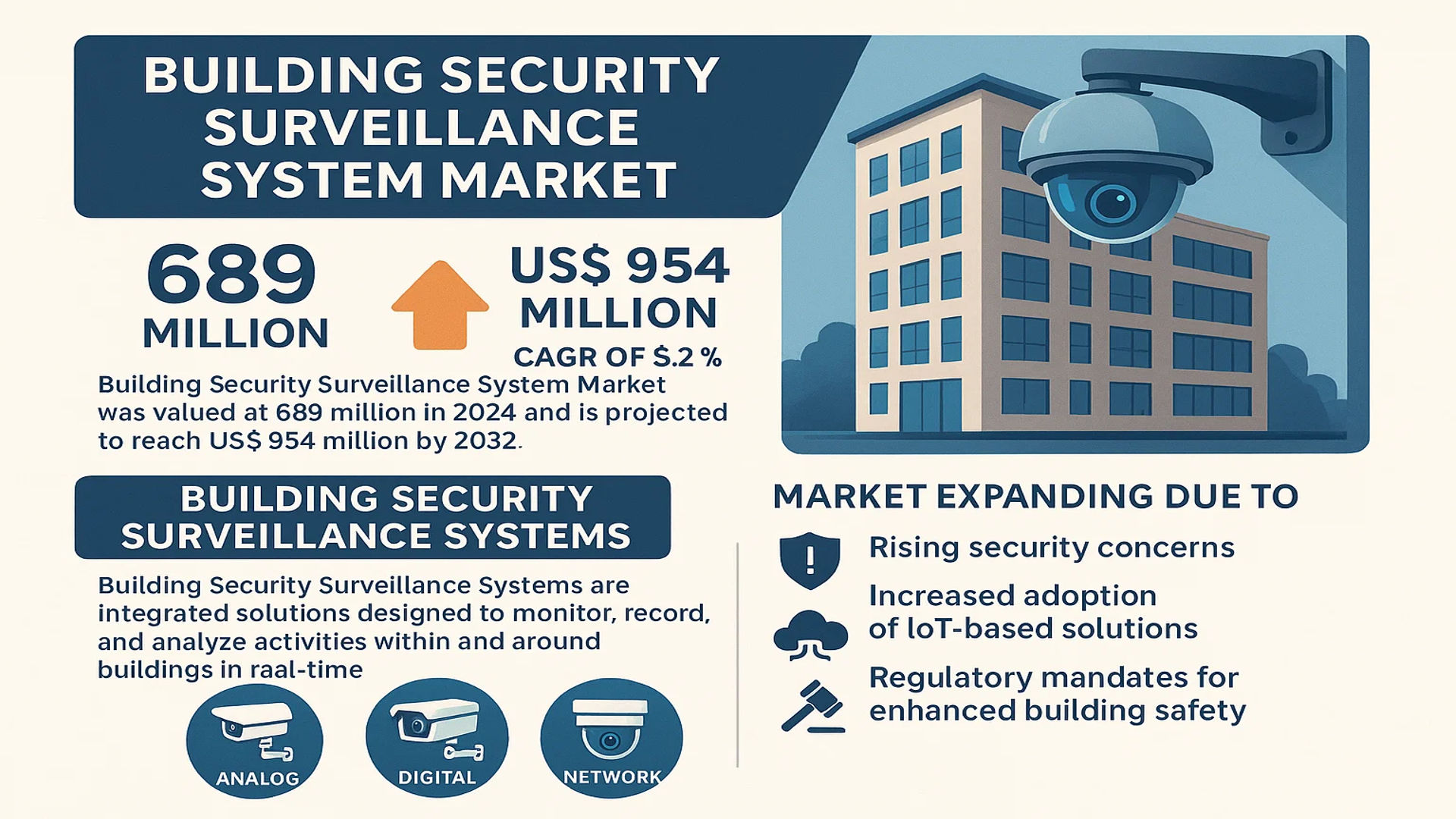

The global Building Security Surveillance System Market was valued at 689 million in 2024 and is projected to reach US$ 954 million by 2032, at a CAGR of 5.2% during the forecast period.

Building Security Surveillance Systems are integrated solutions designed to monitor, record, and analyze activities within and around buildings in real-time. These systems deploy a combination of hardware (such as cameras, sensors, and access control devices) and software to enhance security by detecting and responding to potential threats. Key components include analog, digital, and network surveillance systems, which provide varying levels of resolution, scalability, and connectivity.

The market is expanding due to rising security concerns, increased adoption of IoT-based solutions, and regulatory mandates for enhanced building safety. While North America remains a dominant market, Asia-Pacific is witnessing rapid growth, driven by urbanization and infrastructure development. Major players such as Hikvision, Bosch Security Systems, and Honeywell are investing in AI-powered analytics and cloud-based solutions to strengthen their market positions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Smart Building Solutions Accelerates Market Adoption

The global shift toward smart infrastructure is driving significant demand for advanced building security surveillance systems. Smart buildings, which integrate IoT-enabled surveillance technologies, require real-time monitoring and automated threat detection capabilities. The commercial sector accounts for over 45% of installations, with growing adoption in healthcare and education facilities due to heightened security requirements. Modern systems now incorporate AI-powered analytics, enabling features like facial recognition and behavioral analysis, which significantly enhance threat prevention capabilities.

Increasing Urbanization and Security Concerns Drive Government Investments

Rapid urbanization has led to increased investments in public safety infrastructure, with municipal governments allocating 30-35% of smart city budgets toward surveillance technologies. Recent terrorism incidents and property crimes have accelerated regulatory mandates for surveillance in high-traffic buildings. Airports, transit hubs and government facilities now prioritize multi-layered surveillance networks combining thermal imaging, LiDAR and traditional CCTV. This trend is particularly strong in emerging economies where urban populations are growing at 2-3% annually, creating urgent demands for modern security infrastructure.

Technological Advancements in Video Analytics Fuel Market Growth

Breakthroughs in edge computing and deep learning have transformed surveillance capabilities, enabling real-time processing without cloud dependency. Modern systems can now analyze crowd density, detect unattended objects, and recognize license plates with over 98% accuracy. The integration of 5G networks further enhances data transmission speeds, allowing for higher resolution feeds and faster emergency response times. These technological leaps have expanded applications beyond security into business intelligence, with retail sectors using foot traffic analytics to optimize store layouts and operations.

MARKET RESTRAINTS

High Implementation Costs Create Adoption Barriers

While advanced surveillance systems offer superior security, their implementation requires significant capital expenditure that deters smaller organizations. A comprehensive installation with AI analytics and thermal imaging can cost 40-60% more than traditional systems, with ongoing maintenance adding 15-20% to total cost of ownership. This pricing structure makes the technology inaccessible for budget-constrained sectors like public schools and small businesses, despite growing security needs. The cost barrier is even more pronounced in developing regions where infrastructure limitations add complexity to deployments.

Privacy Regulations and Data Protection Concerns

Increasing global focus on data privacy has led to stringent regulations governing surveillance system usage. The European Union’s GDPR and similar legislation in other regions impose heavy fines for non-compliance, creating legal liabilities for system operators. Public resistance to facial recognition technologies has resulted in outright bans or restrictions in several municipalities, limiting market potential. This regulatory environment forces manufacturers to invest heavily in compliance features, adding 20-25% to development costs while potentially reducing system effectiveness through required data anonymization.

Cybersecurity Vulnerabilities Pose Operational Risks

Network-connected surveillance systems present attractive targets for cyberattacks, with industry reports indicating a 300% increase in IoT device breaches over recent years. Compromised systems can expose sensitive footage or even provide attackers with building access controls. The lack of standardized security protocols across manufacturers creates vulnerabilities that are difficult to patch across mixed-vendor installations. These risks require continuous security updates and trained IT personnel, adding to operational expenses and creating hesitation among potential buyers.

MARKET CHALLENGES

Integration Complexities with Legacy Systems

Many existing buildings struggle to integrate modern surveillance solutions with legacy security infrastructure. Retrofitting older structures with IP cameras and smart sensors often requires complete cabling overhauls, increasing project costs by 35-50%. Compatibility issues between different generations of equipment frequently create blind spots in coverage or analytics gaps. This challenge is particularly acute in historical buildings where structural modifications face additional regulatory restrictions, forcing compromise solutions that limit system effectiveness.

Shortage of Skilled Technicians Impacts Service Quality

The rapid evolution of surveillance technology has outpaced the availability of trained professionals capable of designing and maintaining complex systems. Industry surveys indicate a 40% gap between demand and supply for certified security technicians, leading to project delays and suboptimal installations. The shortage is most severe in emerging markets where technical education programs haven’t yet adapted to incorporate the latest surveillance technologies. This skills gap not only impedes new deployments but also reduces the effectiveness of existing systems that require sophisticated tuning and regular updates.

False Alarm Rates Undermine System Credibility

Advanced analytics features, while powerful, often trigger false alerts due to environmental factors like lighting changes or wildlife movement. Some AI-powered systems exhibit false positive rates as high as 15-20%, causing “alert fatigue” among security personnel. This undermines confidence in automated threat detection and leads many organizations to disable advanced features, negating their investment benefits. Developing more sophisticated algorithms that account for contextual factors remains an ongoing challenge for the industry.

MARKET OPPORTUNITIES

Growing Adoption of Cloud-Based Surveillance Solutions

The shift toward cloud-managed surveillance systems presents significant growth opportunities, particularly for small and medium-sized enterprises. Cloud solutions reduce upfront costs by 30-40% compared to on-premise installations while offering enterprise-grade features through subscription models. Providers are now bundling cybersecurity insurance with their offerings, addressing a key customer concern. The cloud market segment is projected to grow at nearly 2.5 times the rate of traditional systems as organizations prioritize scalability and remote management capabilities.

Expansion into Non-Security Applications Creates New Revenue Streams

Forward-thinking companies are leveraging surveillance infrastructure for business intelligence applications beyond security. Retailers use foot traffic patterns to optimize staffing, while manufacturers monitor production line efficiency through vision analytics. These secondary applications provide 20-30% additional ROI on surveillance investments, making the technology more attractive to cost-conscious buyers. The integration of POS data with video analytics is creating particularly strong opportunities in the retail and hospitality sectors.

Strategic Partnerships Between Security and IT Providers

As surveillance systems become more network-dependent, manufacturers are forming alliances with cybersecurity firms and IT infrastructure providers. These partnerships enable bundled solutions that address key customer concerns about integration complexity and data protection. Joint offerings have demonstrated 40-50% faster deployment times compared to piecemeal implementations. The trend toward converged physical and cybersecurity solutions is particularly strong in banking and healthcare sectors where regulatory compliance is critical.

BUILDING SECURITY SURVEILLANCE SYSTEM MARKET TRENDS

Integration of AI and IoT Driving Smart Surveillance Systems

The adoption of artificial intelligence (AI) and Internet of Things (IoT) in building security surveillance systems has significantly enhanced real-time monitoring and threat detection capabilities. AI-powered video analytics enable automatic recognition of suspicious activities, reducing human intervention and improving response times. Smart surveillance systems now incorporate facial recognition, license plate recognition, and behavioral analysis to identify security threats more effectively. The global demand for AI-powered security solutions is rising, with smart surveillance deployments increasing by approximately 25% annually in commercial buildings and public infrastructure.

Other Trends

Cloud-Based Surveillance Solutions

Cloud-based surveillance systems are gaining traction due to their scalability, remote accessibility, and lower upfront infrastructure costs. Businesses are increasingly shifting from traditional on-premises solutions to cloud-hosted surveillance, which allows centralized management and real-time data access from multiple locations. The adoption of cloud storage for security footage has grown by over 30% in the past two years, driven by the need for cost-effective, high-capacity storage solutions.

Heightened Demand for High-Resolution and Thermal Imaging

Security surveillance systems are increasingly leveraging 4K Ultra HD cameras and thermal imaging technology to enhance situational awareness. High-resolution cameras improve identification accuracy, particularly in crowded environments, while thermal imaging provides reliable detection in low-light or adverse weather conditions. Surveillance systems now integrate both technologies, with thermal camera adoption growing by approximately 15% annually in critical infrastructure applications. Additionally, the rise of edge computing allows cameras to process data locally, reducing bandwidth requirements and latency in security monitoring.

Increased Focus on Cybersecurity in Surveillance Networks

As surveillance systems become more connected, cybersecurity has emerged as a critical concern. Companies are investing in encrypted data transmission protocols, multi-factor authentication, and regular firmware updates to prevent unauthorized access to surveillance networks. Recent vulnerabilities discovered in IP-based cameras highlight the need for robust security measures, prompting manufacturers to strengthen device-level protection. Security compliance certifications, such as ISO 27001, are now common requirements for surveillance system vendors in government and enterprise contracts.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Security Firms Intensify AI and Cloud-Based Solutions to Gain Market Dominance

The global building security surveillance system market exhibits a highly competitive environment, characterized by the presence of multinational corporations, regional players, and niche solution providers. While the market remains somewhat fragmented, major technology-driven players continue to consolidate their positions through aggressive R&D investments and strategic acquisitions. Hikvision and Honeywell currently dominate market share, collectively accounting for approximately 25% of global revenue in 2024. Their leadership stems from comprehensive product ecosystems spanning hardware, software, and analytics platforms.

Axis Communications and Bosch Security Systems maintain strong positions in the European and North American markets, primarily due to their focus on high-quality network video solutions and open-platform integrations. Both companies have recently shifted toward AI-powered video analytics, recognizing the growing demand for intelligent surveillance that goes beyond basic monitoring functions.

Mid-sized innovators like Avigilon Corporation (a Motorola Solutions company) are gaining traction through specialized offerings. Avigilon’s recent launch of high-definition analytics cameras with self-learning capabilities demonstrates how agility and technological differentiation can challenge larger competitors.

List of Key Building Security Surveillance Providers Profiled

- Hikvision (China)

- Honeywell International Inc. (U.S.)

- Axis Communications AB (Sweden)

- Bosch Security Systems (Germany)

- Dahua Technology (China)

- Johnson Controls (Ireland)

- Panasonic i-PRO Sensing Solutions (Japan)

- Huawei Technologies (China)

- NXP Semiconductors (Netherlands)

- Agent Video Intelligence (Israel)

Market competition continues to intensify as enterprises increasingly demand integrated solutions combining physical security with cybersecurity measures. Recent developments show most major players expanding their partner networks to provide seamless integration with access control, fire safety, and building management systems—a critical factor for winning large commercial and government contracts.

Segment Analysis:

By Type

Network Surveillance System Segment Leads Due to High Integration with AI and IoT Technologies

The market is segmented based on type into:

- Analog Surveillance System

- Subtypes: CCTV cameras, DVR systems, and others

- Digital Surveillance System

- Subtypes: IP cameras, NVR systems, and others

- Network Surveillance System

- Subtypes: Cloud-based solutions, AI-powered analytics, and others

- Hybrid Surveillance System

By Application

Commercial Building Segment Dominates Due to High Security Requirements in Corporate Environments

The market is segmented based on application into:

- Residential

- Commercial Building

- School

- Hospital

- Government Facilities

By Component

Video Surveillance Equipment Segment Holds Major Share Due to Continuous Technological Advancements

The market is segmented based on component into:

- Video Surveillance Equipment

- Subtypes: Cameras, monitors, storage devices, and others

- Access Control Systems

- Alarm Systems

- Software Solutions

By Technology

AI-Based Surveillance Gains Traction Due to Enhanced Analytics and Automation Capabilities

The market is segmented based on technology into:

- Traditional Surveillance

- IP-Based Surveillance

- AI-Based Surveillance

- Subtypes: Facial recognition, behavior analysis, and others

- Cloud-Based Surveillance

Regional Analysis: Building Security Surveillance System Market

North America

The North American market for building security surveillance systems is the most advanced globally, driven by strict regulatory standards and high adoption of smart security technologies. The U.S. leads with robust demand across commercial, residential, and institutional sectors, supported by increasing security budgets and widespread AI-based surveillance integration. Key players like Honeywell and Johnson Controls dominate the market with advanced offerings in network and cloud-based surveillance solutions. The region also experiences growing demand for cybersecurity-integrated surveillance due to rising data protection concerns. Although analog systems persist in cost-conscious segments, the shift toward IP-based surveillance is accelerating, particularly in smart city projects.

Europe

Europe maintains a strong focus on compliance with GDPR and other data privacy laws, which influence the deployment of surveillance systems. Countries like Germany and the U.K. emphasize AI-driven analytics and cloud storage solutions to enhance security while ensuring regulatory adherence. The market benefits from increased investments in public infrastructure security and the retrofitting of older buildings with modern surveillance technologies. However, high costs associated with premium solutions and resistance to perceived privacy intrusions present challenges. Despite this, key players such as Bosch Security Systems and Axis Communications continue to drive innovation in this space.

Asia-Pacific

Asia-Pacific is the fastest-growing region, propelled by rapid urbanization, infrastructure development, and heightened security concerns in densely populated areas. China and India are major contributors, leveraging local manufacturers like Dahua Technology and Hikvision to provide cost-effective surveillance solutions. While analog and low-cost digital systems dominate in emerging economies, there is a steady shift toward AI-powered network surveillance, particularly in commercial and government applications. Challenges include fragmented regulations and inconsistent enforcement, but the push for smart city initiatives across the region ensures continued market expansion.

South America

The market in South America is evolving, with Brazil and Argentina leading adoption due to increasing crime rates and investments in commercial real estate. Budget constraints and economic instability, however, limit widespread adoption of high-end systems. Most demand comes from urban centers deploying hybrid analog-digital solutions. While cybersecurity and cloud integration remain underdeveloped compared to North America and Europe, regional players are gradually introducing more sophisticated offerings to meet growing security needs.

Middle East & Africa

This region shows uneven growth, with Gulf countries like the UAE and Saudi Arabia investing heavily in smart surveillance for mega-projects and critical infrastructure. Advanced AI and facial recognition systems are increasingly adopted in high-security zones. Conversely, African markets lag due to limited infrastructure and funding, relying predominantly on entry-level analog systems. Nonetheless, long-term opportunities exist as urban development accelerates and governments prioritize security modernization.

Report Scope

This market research report provides a comprehensive analysis of the Global Building Security Surveillance System market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 689 million in 2024 and is projected to reach USD 954 million by 2032, growing at a CAGR of 5.2%.

- Segmentation Analysis: Detailed breakdown by product type (Analog, Digital, Network Surveillance Systems), application (Residential, Commercial, Healthcare, Education), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of 16 leading market participants including Hikvision, Bosch Security Systems, Honeywell, Axis Communications, and Dahua Technology, with analysis of their market share, product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of AI-powered analytics, cloud-based surveillance, IoT integration, and advanced video management systems transforming the industry.

- Market Drivers & Restraints: Evaluation of factors including rising security concerns, smart city initiatives, regulatory compliance requirements, alongside challenges like data privacy concerns and high implementation costs.

- Stakeholder Analysis: Strategic insights for security system providers, building operators, technology vendors, and investors regarding emerging opportunities in the security ecosystem.

The report employs rigorous primary and secondary research methodologies, including expert interviews, company financial analysis, and verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Building Security Surveillance System Market?

-> Building Security Surveillance System Market was valued at 689 million in 2024 and is projected to reach US$ 954 million by 2032, at a CAGR of 5.2% during the forecast period.

Which key companies operate in this market?

-> Major players include Hikvision, Dahua Technology, Axis Communications, Bosch Security Systems, Honeywell, Johnson Controls, and Panasonic.

What are the key growth drivers?

-> Growth is driven by increasing security concerns, smart city development, regulatory mandates, and technological advancements in surveillance systems.

Which region dominates the market?

-> Asia-Pacific leads in market share, while North America shows strong adoption of advanced surveillance technologies.

What are the emerging trends?

-> Key trends include AI-powered video analytics, cloud-based surveillance solutions, integration with building automation systems, and cybersecurity enhancements.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...