Building Integrated PV Market Insights

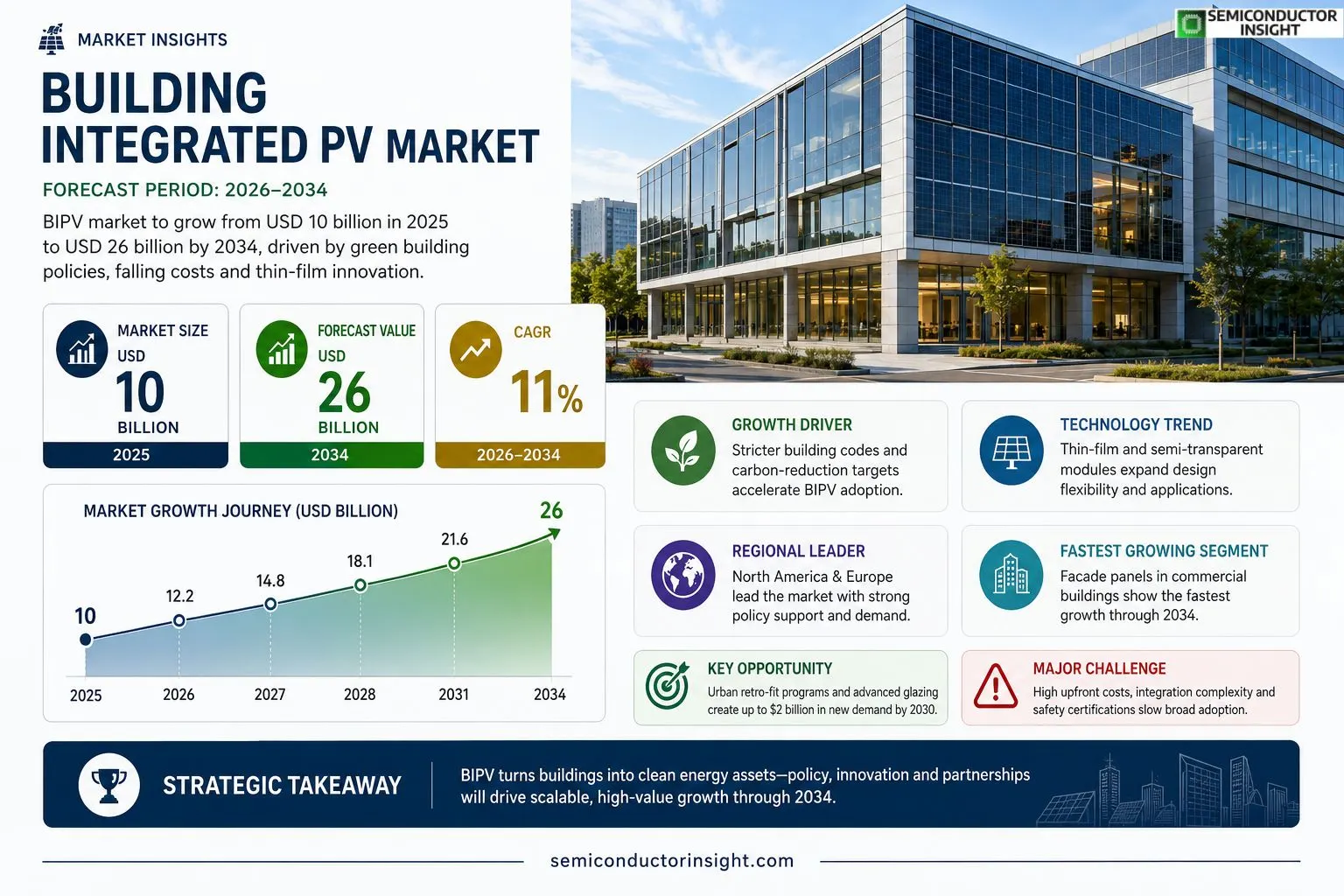

Global Building Integrated PV Market size was valued at USD 10 billion in 2025. The market is projected to grow from USD 10 billion in 2025 to USD 26 billion by 2034, exhibiting a CAGR of 11% during the forecast period.

Building Integrated Photovoltaics (BIPV) are solar energy systems that are seamlessly incorporated into building components such as façades, roofs, windows and shading devices, replacing conventional construction materials while generating electricity on‑site.The market is experiencing rapid growth because governments worldwide are tightening building codes and offering incentives for zero‑carbon construction, while manufacturers benefit from falling module costs and advances in thin‑film technology. Furthermore, high‑profile projects,such as the partnership announced in March 2024 between Panasonic and LIXIL for BIPV glazing,demonstrate strong industry momentum. Leading players including Tesla Energy, SunPower Corporation, Hanwha Q CELLS and Saint‑Gobain are expanding their portfolios through strategic collaborations and innovative product launches.

MARKET DRIVERS

Energy Efficiency and Decarbonization

Building Integrated PV Market is propelled by stringent global carbon‑reduction targets, with many countries aiming for net‑zero emissions by 2050. Integrated photovoltaic facades and rooftops enable commercial and residential buildings to generate up to 30% of their electricity on‑site, dramatically lowering operational carbon footprints.

Policy Incentives and Building Codes

Government incentives such as tax credits, accelerated depreciation, and favorable feed‑in tariffs have increased adoption rates. In regions where building codes now mandate renewable energy integration for new constructions, market penetration is projected to exceed 20% of all new commercial builds by 2027.

➤ Integrated PV can reduce a building’s energy bill by up to 45% while adding aesthetic value that commands higher leasing rates.

Architectural trends favor seamless design, and manufacturers are responding with lightweight, semi‑transparent modules that blend with glazing systems, driving further market expansion.

MARKET CHALLENGES

High Up‑Front Capital Costs

Despite long‑term savings, the initial investment for building‑integrated photovoltaic systems remains substantially higher than conventional roofing solutions, often requiring a 15‑20% premium, which can deter cost‑sensitive developers.

Other Challenges

Technical Integration Complexity

Designing PV‑enabled facades demands close coordination between architects, structural engineers, and electrical specialists, extending project timelines and increasing engineering costs.

MARKET RESTRAINTS

Regulatory and Safety Barriers

Stringent fire‑safety standards and limited certifications for glazing‑integrated modules restrict their use in high‑rise constructions, slowing market entry in several major urban centers.

Supply Chain Limitations

Global shortages of high‑efficiency silicon wafers and specialized framing components have led to lead times of 6‑9 months, constraining project schedules and increasing costs.

MARKET OPPORTUNITIES

Urban Retro‑fit Programs

Municipal retro‑fit initiatives targeting existing office towers present a sizable growth avenue; analysts estimate that retro‑fit installations could account for up to $2 billion in new demand by 2030.

Advancements in Bifacial and Transparent Modules

Emerging bifacial and semi‑transparent technologies are expanding design flexibility, enabling integration into skylights and curtain walls, which opens new revenue streams for commercial real estate developers.

Digital Twin and BIM Integration

Incorporating photovoltaic performance models into Building Information Modeling (BIM) platforms allows stakeholders to forecast energy yields accurately, reducing risk and accelerating approval processes.

Building Integrated PV Market Trends

Regulatory Momentum Drives Adoption

Building Integrated PV Market is being reshaped by a wave of stricter building codes that now require higher energy performance and lower carbon footprints. Governments across Europe, North America, and parts of Asia have introduced incentive programs that subsidize façade‑integrated solar solutions, encouraging developers to replace conventional cladding with photovoltaic glazing. At the same time, municipalities are streamlining permitting processes for BIPV installations, reducing project lead times. These policy shifts create a clear business case for architects and contractors, who can now capture both aesthetic value and on‑site electricity generation without additional structural load. The combined effect of regulation and financial support is accelerating project pipelines and expanding the market reach beyond premium segments.

Other Trends

Cost Reductions via Thin‑Film Advances

Manufacturers are benefiting from continued improvements in thin‑film module efficiency and manufacturing yields, which translate into lower system‑level costs. Lightweight, flexible panels are being integrated into curtain walls and skylights, allowing for larger surface coverage without adding significant dead load. The reduction in material usage, coupled with simplified installation procedures, reduces labor expenses and improves overall project economics. As a result, Building Integrated PV Market is seeing broader adoption in mid‑rise commercial buildings, where cost sensitivity previously limited BIPV uptake. The trend is supported by supply‑chain optimizations that lower the price gap between traditional construction materials and photovoltaic components.

Strategic Partnerships Accelerate Deployment

Recent collaborations between major glazing manufacturers and solar technology firms illustrate a growing ecosystem approach. Joint product development programs focus on integrated solar glass that meets both performance and architectural standards, shortening the time to market for new designs. These alliances also enable shared R&D costs, allowing faster iteration of high‑efficiency cells that blend seamlessly into building envelopes. As a result, Building Integrated PV Market is experiencing an influx of turnkey solutions that combine energy generation, daylighting, and aesthetic appeal, making the technology accessible to a wider range of developers and owners.

COMPETITIVE LANDSCAPEKey Industry Players

Building Integrated Photovoltaics (BIPV) Competitive Overview

In the global Building Integrated PV market, a few large‑scale innovators dominate the landscape by leveraging extensive R&D budgets and vertically integrated supply chains. Tesla Energy commands a strong presence through its Solar Roof, coupling high‑efficiency cells with a sleek, tile‑like aesthetic that appeals to residential developers seeking net‑zero projects. SunPower Corporation differentiates itself with ultra‑high‑efficiency CIGS modules, allowing slimmer façade integrations and higher energy yields per square metre. Hanwha Q CELLS supplies cost‑effective thin‑film and crystalline solutions that have been adopted across large commercial façades in Europe and Asia. Saint‑Gobain, a traditional construction materials leader, has accelerated its BIPV portfolio by embedding photovoltaics into glass and composite panels, targeting the high‑rise market where architectural value is paramount. Panasonic, in partnership with LIXIL, recently announced a BIPV glazing line that blends transparent solar cells with high‑performance window systems, underscoring the trend toward dual‑function building envelopes.Beyond these headline players, a constellation of niche yet technically sophisticated firms enriches the market with specialized form factors and regional expertise. Onyx Solar focuses on high‑transparency glass modules for museum and office projects, while Solaria delivers thin‑film modules optimized for curtain‑wall installations in the United States. Schüco integrates PV‑enabled façades into its aluminium building systems, catering to the German and Scandinavian markets. JinkoSolar’s BIPV line emphasizes economies of scale for large‑scale residential complexes. LIXIL, apart from its Panasonic collaboration, provides modular BIPV roofing tiles for the Japanese market. Sunstyle offers flexible polymer‑based PV films for shading devices, and Dyaqua supplies photovoltaic glazing for commercial skyscrapers in the Middle East. These companies, together with emerging regional manufacturers such as Viurna Solar (France) and Heliatek (Germany), create a diversified ecosystem that supports rapid market growth and fosters innovation across the value chain.

List of Key Building Integrated PV Companies Profiled

- Tesla Energy

- SunPower Corporation

- Hanwha Q CELLS

- Saint‑Gobain

- Panasonic

- Onyx Solar

- Solaria

- Schüco

- JinkoSolar

- LIXIL

- Sunstyle

- Dyaqua

- Viurna Solar

- Heliatek

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Crystalline‑silicon BIPV

|

| By Application |

|

Façade panels

|

| By End User |

|

Commercial buildings

|

| By Technology |

|

Semi‑transparent PV

|

| By Integration Approach |

|

Retrofit projects

|

Regional Analysis: North America

United States

The residential segment remains a key driver for BIPV adoption in the United States. Homeowners are increasingly seeking aesthetically integrated solar solutions that enhance property value and reduce energy bills.

The commercial and industrial sectors are recognizing the long-term cost savings and sustainability benefits of BIPV. Large-scale BIPV projects are being implemented in office buildings, warehouses, and manufacturing facilities.

Ongoing research and development are leading to innovative BIPV materials with enhanced performance characteristics, including improved light absorption and durability.

Government policies and financial incentives play a crucial role in promoting BIPV market growth. Various tax credits, rebates, and net metering programs are available to encourage adoption.

Europe

The European BIPV market exhibits substantial potential, driven by stringent renewable energy targets and a growing focus on sustainable construction. Several countries, including Germany, France, and the United Kingdom, are leading the way in BIPV adoption, supported by favorable government policies and research initiatives. The market is characterized by a diverse range of BIPV technologies, including solar roofing, facades, and windows. Business strategies in Europe often involve collaborations between technology providers, building developers, and energy utilities. The emphasis on energy efficiency standards and green building certifications further contributes to the market’s growth.

Asia-Pacific

Asia-Pacific represents a dynamic and rapidly expanding BIPV market, fueled by increasing urbanization, rising energy demand, and government support for renewable energy. China is the largest BIPV market in the region, with significant investments in residential, commercial, and utility-scale projects. Other key markets include Japan, Australia, and South Korea. The Asia-Pacific BIPV market is characterized by a wide range of technologies and applications, with a growing focus on flexible and transparent solar cells. Business strategies in the region often involve partnerships with local manufacturers and distributors to capitalize on market opportunities.

South America

The BIPV market in South America is gaining momentum, driven by growing awareness of renewable energy and increasing demand for sustainable building solutions. Brazil and Chile are emerging as key markets, with supportive government policies and favorable solar resources. The market is primarily focused on residential and commercial applications, with a growing interest in BIPV for agricultural buildings and infrastructure. Business strategies in South America often involve partnerships with local construction companies and energy providers.

Middle East & Africa

The Middle East and Africa represent a promising growth market for BIPV, driven by abundant solar resources and increasing investments in renewable energy projects. Countries like Saudi Arabia, the United Arab Emirates, and South Africa are actively promoting BIPV adoption through government initiatives and private sector investments. The market is focused on large-scale BIPV projects for commercial buildings, industrial facilities, and infrastructure. Business strategies in the region often involve partnerships with international technology providers and local developers.

Report Scope

This market research report provides a comprehensive analysis of the Building Integrated PV Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Building Integrated PV Market?

-> Building Integrated PV Market was valued at USD 10 billion in 2025 and is expected to reach USD 26 billion by 2034.

Which key companies operate in Building Integrated PV Market?

-> Key players include Tesla Energy, SunPower Corporation, Hanwha Q CELLS and Saint‑Gobain, among others.

What are the key growth drivers?

-> Key growth drivers include tightening building codes and government incentives, falling photovoltaic module costs, and advances in thin‑film technology.

Which region dominates the market?

-> North America and Europe hold dominant market shares, while Asia‑Pacific is emerging as a fast‑growing region.

What are the emerging trends?

-> Emerging trends include strategic partnerships such as Panasonic‑LIXIL for BIPV glazing, integration of thin‑film modules into façades and windows, and increased adoption of BIPV in zero‑carbon building projects.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...