MARKET INSIGHTS

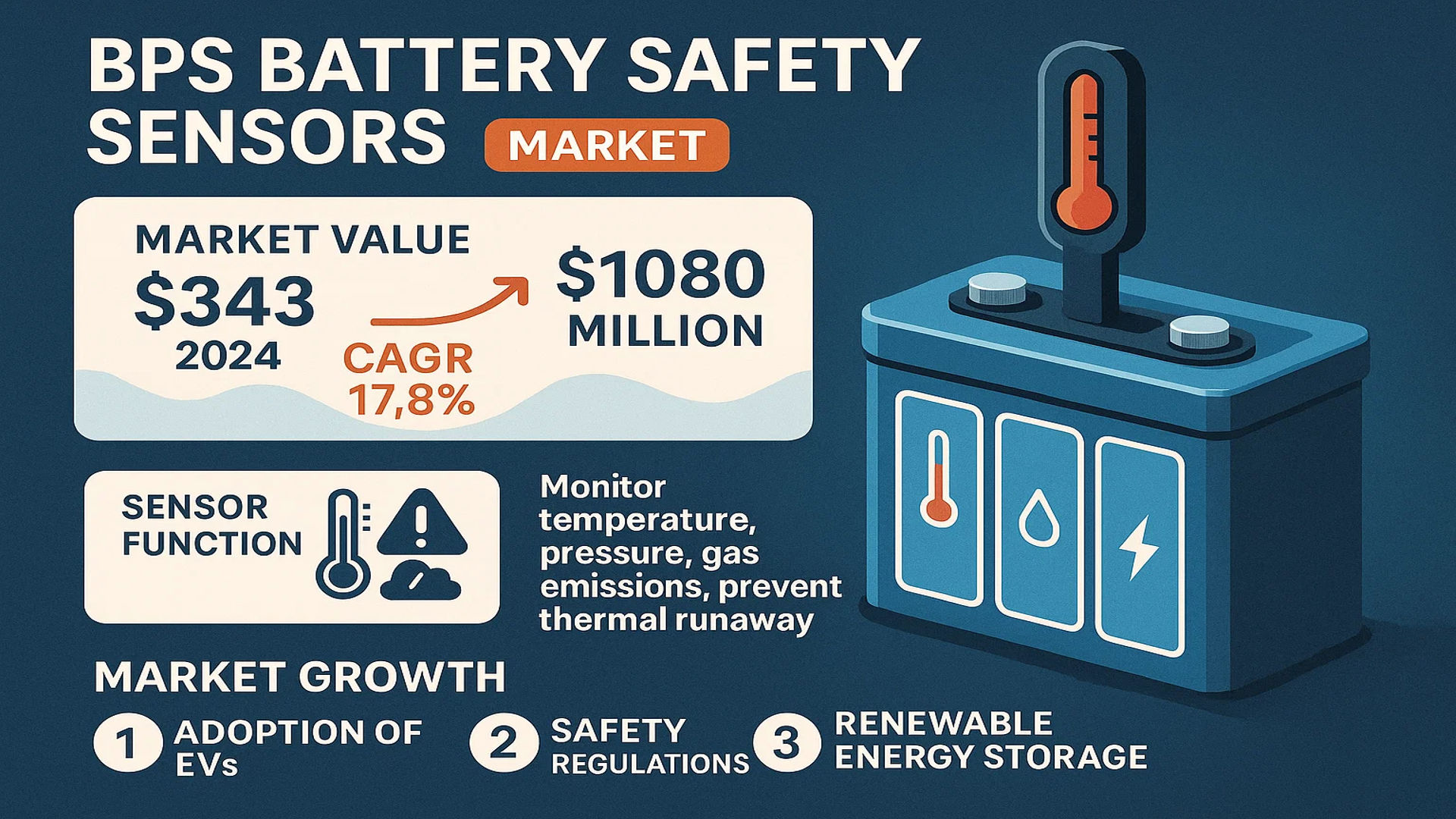

The global BPS Battery Safety Sensors market was valued at 343 million in 2024 and is projected to reach US$ 1080 million by 2032, at a CAGR of 17.8% during the forecast period.

BPS Battery Safety Sensors are specialized devices designed to monitor critical parameters in battery systems, including temperature, pressure, and gas emissions. These sensors play a vital role in preventing thermal runaway and ensuring operational safety across applications such as electric vehicles (EVs), energy storage systems (ESS), and industrial battery solutions.

Market growth is primarily driven by the rapid adoption of EVs, stricter safety regulations, and increasing investments in renewable energy storage. While Asia-Pacific dominates demand due to expanding EV production, North America and Europe follow closely with advanced battery technologies. Key players like Valeo, Honeywell, and Metis Engineering are accelerating innovation through strategic partnerships, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Electric Vehicles Accelerates Adoption of BPS Battery Safety Sensors

The rapid global shift toward electric mobility is creating unprecedented demand for advanced battery safety solutions. With electric vehicle sales projected to grow at a compound annual growth rate of over 26% through 2030, the need for reliable battery protection systems has become critical. Battery safety sensors play a vital role in preventing thermal runaway incidents, which have been responsible for several high-profile EV recalls in recent years. These sensors monitor critical parameters including temperature, voltage, and gas emissions, enabling real-time threat detection and proactive safety measures. Major automotive manufacturers are now making battery safety systems mandatory, with some OEMs allocating up to 15% of their total battery management budget specifically for advanced monitoring solutions.

Stringent Safety Regulations Fueling Market Expansion

Governments worldwide are implementing rigorous safety standards for battery-powered applications, driving widespread adoption of BPS sensors. New regulations now require comprehensive battery monitoring systems in all energy storage installations above 5kWh capacity, with specific mandates for real-time thermal monitoring and automated shutdown capabilities. The energy storage sector, which is expected to triple its global capacity within the next five years, represents a significant growth avenue for safety sensor providers. Regulatory bodies have begun classifying battery safety components as critical infrastructure, with some regions offering subsidies for advanced sensor integration.

Furthermore, international standardization efforts are creating a unified framework for battery safety across applications.

➤ For instance, recent updates to transportation safety guidelines now require multi-point sensor arrays in all EV battery packs exceeding 20kWh capacity.

The combination of regulatory mandates and voluntary safety certifications is creating a compliance-driven market where advanced sensor technology becomes a competitive differentiator rather than just a safety feature.

MARKET RESTRAINTS

High Implementation Costs Restrict Widespread Adoption

While battery safety sensors offer critical protection, their relatively high cost presents a significant barrier to market penetration, particularly in price-sensitive segments. Advanced multi-parameter sensor arrays can increase total battery system costs by 8-12%, creating resistance among cost-conscious manufacturers. The sophistication required for accurate thermal runaway prediction drives up both development expenses and unit costs, with some high-end sensors costing several times more than basic temperature monitors. This pricing disparity is particularly challenging in emerging EV markets where manufacturers operate on slim margins.

Other Restraints

Integration Complexity

The deployment of comprehensive safety systems requires extensive battery pack redesigns in many applications. Retrofitting existing battery systems with advanced monitoring capabilities often proves technically challenging and economically unviable, forcing manufacturers to delay upgrades until next-generation designs.

Standardization Issues

The lack of universal communication protocols between sensor systems and battery management units creates compatibility challenges. This fragmentation increases development costs and limits the plug-and-play potential of safety solutions across different battery architectures.

MARKET CHALLENGES

Technical Limitations in Early Detection Capabilities

The industry faces significant technological hurdles in developing sensors capable of reliably predicting impending battery failures with adequate lead time. Current systems can detect active thermal events but struggle with early-stage anomaly identification, often providing warnings only minutes before critical failure. Research indicates that improving prediction windows from the current 2-5 minute range to 15+ minutes could reduce battery-related incidents by over 70%. However, achieving this requires breakthroughs in sensor sensitivity and data interpretation algorithms that haven’t yet reached commercial viability.

The dynamic nature of battery degradation patterns further complicates detection algorithms. Unlike mechanical components with predictable wear patterns, lithium-ion batteries exhibit highly variable failure modes depending on usage conditions, manufacturing variances, and environmental factors. Developing sensor systems that account for these variables without excessive false positives remains an unsolved engineering challenge for the industry.

MARKET OPPORTUNITIES

Emergence of AI-Enhanced Predictive Safety Systems Creates New Growth Avenues

The integration of artificial intelligence with battery sensor networks presents transformative potential for the market. Advanced machine learning algorithms can analyze complex sensor data patterns to predict failure events with greater accuracy and lead time than conventional threshold-based systems. Early implementations have demonstrated 40% improvements in detection reliability while reducing false alarms by up to 60%. This technology convergence is creating opportunities for sensor providers to transition from component suppliers to comprehensive safety solution partners.

Expansion of Energy Storage Applications Opens New Markets

The rapid growth of grid-scale and residential energy storage systems represents a major growth opportunity for safety sensor providers. Unlike automotive applications where space and weight are critical constraints, stationary storage systems can accommodate more comprehensive monitoring solutions. This allows for sophisticated sensor arrays that monitor not just temperature and voltage, but also electrolyte composition, internal pressure, and mechanical stress. With the global energy storage market projected to expand fivefold by 2030, safety system providers have an opportunity to establish new standards for comprehensive battery monitoring in stationary applications.

Emerging battery technologies such as solid-state and sodium-ion chemistries will require specialized sensor solutions, creating additional opportunities for suppliers capable of adapting their technologies to new electrochemical profiles.

BPS BATTERY SAFETY SENSORS MARKET TRENDS

Growing Adoption in Electric Vehicles to Drive Market Expansion

The BPS Battery Safety Sensors market is experiencing robust growth, largely fueled by the accelerating adoption of electric vehicles (EVs) worldwide. As governments push for sustainable transportation solutions through incentives and stricter emission regulations, EV production has surged, increasing the demand for advanced battery monitoring systems. The global EV market is forecasted to grow at a CAGR of 22% from 2024 to 2032, directly influencing the adoption of battery safety sensors. These sensors are critical in detecting thermal runaway risks, pressure anomalies, and gas emissions in lithium-ion batteries, ensuring compliance with stringent safety standards. Major automotive manufacturers are increasingly integrating these sensors as standard components, further boosting market penetration.

Other Trends

Advancements in Sensor Technology

Recent innovations in multi-parameter sensing and IoT-enabled battery monitoring are transforming the BPS sensor landscape. Modern sensors now combine temperature, pressure, and gas detection into compact, highly reliable modules, reducing system complexity in battery packs. These improvements enhance real-time data accuracy while lowering power consumption, a key factor for energy efficiency in EVs and grid storage systems. Moreover, AI-driven predictive analytics are being integrated with these sensors, enabling early fault detection and extending battery lifespan—a critical advantage given battery replacement costs can account for 40-50% of total EV maintenance expenses.

Expansion into Energy Storage Systems (ESS)

The rapid deployment of renewable energy infrastructure is creating substantial opportunities for BPS sensor adoption in grid-scale and residential energy storage applications. With global investments in energy storage projected to exceed $120 billion annually by 2030, safety remains a top priority for utility operators and homeowners alike. Battery safety sensors help mitigate fire risks in high-capacity lithium-ion installations, particularly in regions prone to extreme temperatures. Regulatory bodies in North America and Europe now mandate third-party safety certifications for ESS installations—a policy shift that has accelerated sensor integration across commercial and industrial projects. Additionally, the growing need for backup power solutions in data centers and telecom networks further diversifies the demand pipeline.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Competition in Battery Safety Monitoring

The global BPS battery safety sensors market exhibits a moderately competitive structure with multinational corporations dominating revenue share while regional players compete through cost-effective solutions. Valeo and Honeywell collectively accounted for approximately 28% market share in 2024, leveraging their established automotive supply networks and precision sensing expertise. These industry leaders continue expanding their EV safety portfolios through strategic partnerships with battery manufacturers.

Mid-sized innovators like Metis Engineering and Cubic Sensor and Instrument are gaining traction through specialized solutions for thermal runaway detection, capturing nearly 15% of the professional installations segment. Their growth stems from patented gas detection technologies that outperform conventional temperature monitoring systems in early fault identification.

Chinese manufacturers including Zhengzhou Weisheng Electronic Technology and Yangzhou Ruikong Automotive Electronics demonstrate rapid market penetration with competitively priced integrated sensors, particularly in Asia-Pacific markets. These companies benefit from localized production capabilities and government incentives supporting domestic EV component suppliers.

Recent industry developments highlight intensifying R&D focus, with Volt Electronics launching a new generation of wireless BPS sensors in Q1 2024 and Dong Guan Churod Electronics securing three major contracts with European energy storage providers. Such advancements indicate the market’s progression toward more sophisticated, connected safety monitoring ecosystems.

List of Key BPS Battery Safety Sensor Manufacturers

- Valeo (France)

- Honeywell International Inc. (U.S.)

- Metis Engineering Ltd. (U.K.)

- Cubic Sensor and Instrument Co., Ltd. (China)

- Zhengzhou Weisheng Electronic Technology Co., Ltd. (China)

- Yangzhou Ruikong Automotive Electronics Co., Ltd. (China)

- Shenzhen Kemin Sensor Technology Co. (China)

- Dong Guan Churod Electronics Co., Ltd. (China)

- Volt Electronics (Turkey)

Segment Analysis:

By Type

Integrated Segment Leads Due to High Demand for Compact and Energy-Efficient Solutions

The market is segmented based on type into:

- Integrated

- Non-integrated

By Application

Electric Vehicles Segment Dominates Owing to Rising Adoption of Battery Safety Regulations

The market is segmented based on application into:

- Energy Storage

- Electric Vehicles

- Others

By End User

Automotive OEMs Hold Significant Share Due to Mandatory Safety Requirements

The market is segmented based on end user into:

- Automotive OEMs

- Battery Manufacturers

- Energy Storage System Providers

By Technology

Thermal Runaway Detection Technology Gains Prominence for Enhanced Safety

The market is segmented based on technology into:

- Thermal Runaway Detection

- Gas Detection

- Pressure Monitoring

- Voltage Monitoring

Regional Analysis: BPS Battery Safety Sensors Market

Asia-Pacific

Asia-Pacific dominates the BPS Battery Safety Sensors market, primarily driven by rapid EV adoption in China, Japan, and South Korea. China alone accounts for over 60% of global EV battery production, mandating stringent safety standards. Government initiatives like China’s NEV policy and India’s FAME II subsidies accelerate sensor demand. Local manufacturers (Zhengzhou Weisheng Electronic Technology, Shenzhen Kemin Sensor) benefit from cost-competitive solutions, though international players like Honeywell and Valeo maintain strong positions through joint ventures. The region’s battery production capacity expansion—projected to reach 4,500 GWh by 2030—ensures sustained sensor demand.

North America

The North American market thrives on strict safety regulations and EV infrastructure investments. The U.S. Infrastructure Bill allocates $7.5 billion for EV charging networks, indirectly boosting battery safety component demand. Domestic players like Honeywell collaborate with automakers to develop integrated sensor solutions for Tesla and Ford models. Canada’s focus on lithium-ion battery recycling further propels sensor adoption to monitor second-life battery performance. However, higher costs of advanced sensor technologies compared to Asian alternatives remain a challenge for widespread adoption.

Europe

Europe’s market is shaped by EU battery directives enforcing comprehensive safety monitoring across the battery lifecycle. Germany leads in innovation with companies like Volt Electronics developing gas detection sensors for thermal runaway prevention. The region’s emphasis on sustainable energy storage systems (ESS) drives demand for high-accuracy pressure and temperature sensors. However, reliance on imported battery cells from Asia creates supply chain vulnerabilities. Recent collaborations between Metis Engineering and European automakers aim to localize sensor production, enhancing supply stability.

South America

South America shows emerging potential in battery safety sensors, particularly in Brazil’s growing ESS sector for renewable energy projects. The lack of local manufacturing necessitates imports, with Chinese suppliers capturing 70% of the regional market. Argentina’s lithium mining boom may stimulate downstream battery production, creating future sensor opportunities. Current adoption is limited to industrial applications, as EV penetration remains below 2% regionally. Regulatory frameworks for battery safety are still under development, slowing market maturation.

Middle East & Africa

The MEA market focuses on energy storage for solar projects, with UAE and Saudi Arabia leading sensor adoption in utility-scale battery systems. Limited EV adoption restricts automotive applications, though Gulf nations’ planned EV infrastructure investments (e.g., Saudi’s 30% EV target by 2030) show promise. Most sensors are imported via distributors, with Cubic Sensor and Israel-based startups exploring localized solutions. Africa’s market remains nascent due to infrastructure gaps, although mining operations in DRC and Zambia present niche opportunities for industrial battery monitoring.

Report Scope

This market research report provides a comprehensive analysis of the Global BPS Battery Safety Sensors Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 343 million in 2024 and is projected to reach USD 1080 million by 2032 at a CAGR of 17.8%.

- Segmentation Analysis: Detailed breakdown by product type (integrated and non-integrated), application (energy storage, electric vehicles, and others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants, including Valeo, Honeywell, Metis Engineering, and Cubic Sensor And Instrument, covering their product portfolios, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with battery management systems (BMS), and advancements in thermal runaway detection.

- Market Drivers & Restraints: Evaluation of factors such as rising EV adoption, stringent safety regulations, and supply chain challenges impacting market growth.

- Stakeholder Analysis: Strategic insights for battery manufacturers, automotive OEMs, sensor suppliers, and investors to capitalize on market opportunities.

The report employs primary and secondary research methodologies, including expert interviews and data from verified industry sources, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global BPS Battery Safety Sensors Market?

-> BPS Battery Safety Sensors market was valued at 343 million in 2024 and is projected to reach US$ 1080 million by 2032, at a CAGR of 17.8% during the forecast period.

Which key companies operate in Global BPS Battery Safety Sensors Market?

-> Key players include Valeo, Honeywell, Metis Engineering, Cubic Sensor And Instrument, Zhengzhou Weisheng Electronic Technology, and Yangzhou Ruikong Automotive Electronics.

What are the key growth drivers?

-> Growth is driven by rising EV production, increasing energy storage deployments, and stringent battery safety regulations.

Which region dominates the market?

-> Asia-Pacific leads the market due to high EV adoption in China and growing battery manufacturing, while North America shows significant growth potential.

What are the emerging trends?

-> Emerging trends include AI-enabled predictive safety analytics, miniaturization of sensors, and integration with IoT-based battery monitoring systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...