MARKET INSIGHTS

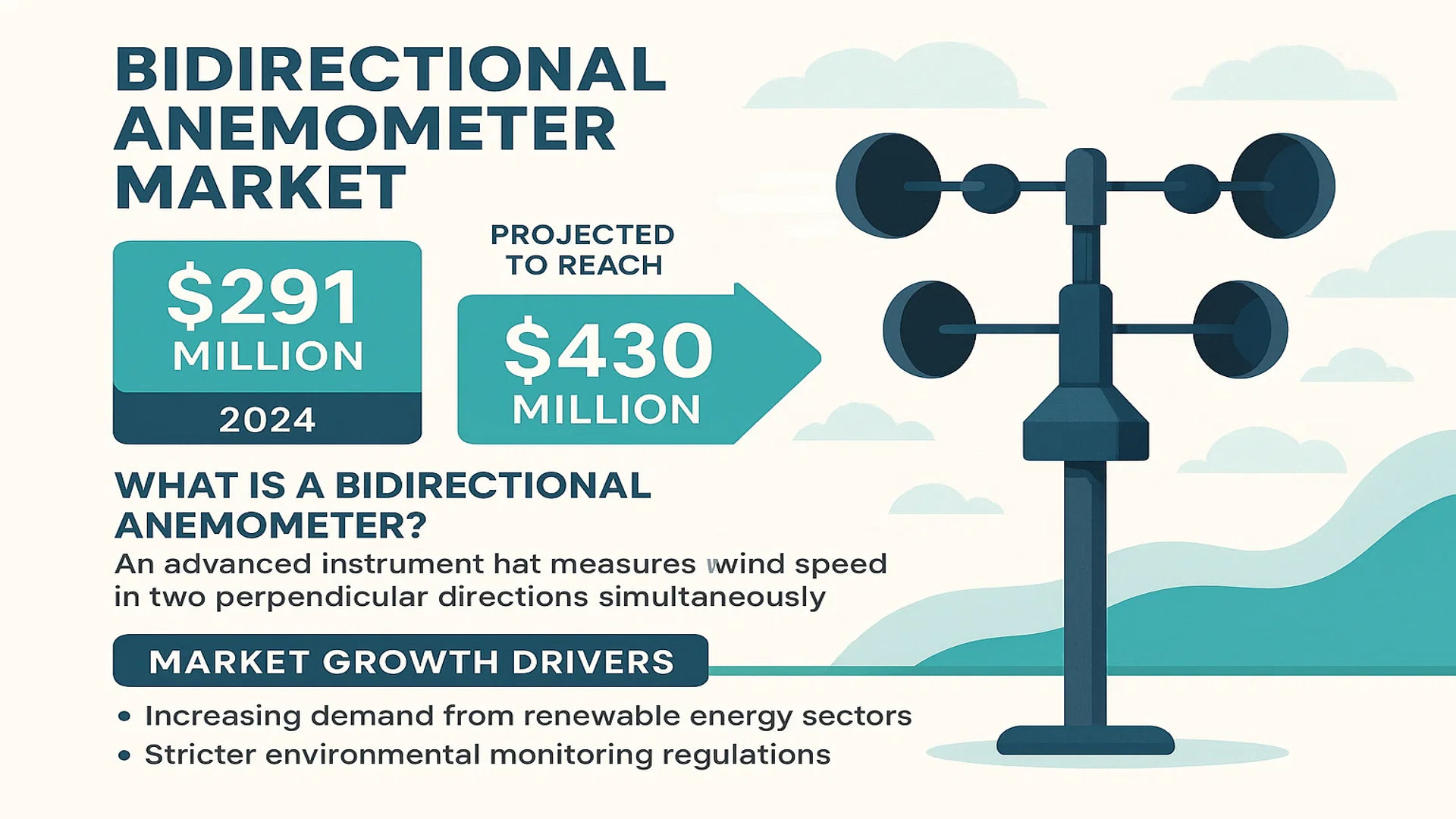

The global Bidirectional Anemometer Market was valued at 291 million in 2024 and is projected to reach US$ 430 million by 2032, at a CAGR of 5.8% during the forecast period.

A bidirectional anemometer is an advanced instrument capable of measuring wind speed in two perpendicular directions simultaneously. These devices utilize dual independent sensors or specialized vane configurations to capture horizontal and vertical airflow components, enabling precise calculation of composite wind speed and direction. This functionality is critical for applications requiring multidimensional wind analysis, including meteorological monitoring, aerospace testing, environmental studies, and industrial ventilation optimization.

Market growth is driven by increasing demand from renewable energy sectors and stricter environmental monitoring regulations. The U.S. currently represents a significant market share, while China demonstrates strong growth potential with expanding infrastructure projects. Key industry players including TSI, Gill Instruments, and OMEGA Engineering continue innovating with ultrasonic and thermal measurement technologies to enhance accuracy and reliability across diverse operational conditions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Accurate Meteorological Data to Boost Market Growth

The increasing need for precise wind measurement across industries is driving significant growth in the bidirectional anemometer market. With climate change intensifying weather patterns, meteorological agencies worldwide are investing heavily in advanced monitoring equipment. Bidirectional anemometers, capable of measuring horizontal and vertical wind vectors simultaneously, provide critical data for weather forecasting, aviation safety, and environmental studies. The global meteorological observation segment accounted for over 35% of the total market share in 2024, reflecting the technology’s importance in weather monitoring applications.

Expansion of Renewable Energy Sector Accelerates Adoption

The rapid growth of wind energy installations globally is creating substantial demand for advanced wind measurement technologies. Bidirectional anemometers play a crucial role in wind farm site assessment, turbine performance monitoring, and energy output optimization. With global wind energy capacity expected to grow by 60% between 2024-2032, the need for accurate wind profiling instruments is increasing exponentially. Energy companies are particularly adopting ultrasonic bidirectional anemometers for their durability and lack of moving parts in harsh wind farm environments.

Technological Advancements in Sensor Technology Propel Market Forward

Recent innovations in ultrasonic and thermal anemometry are enhancing product capabilities while reducing costs. Modern bidirectional anemometers now feature IoT connectivity, real-time data transmission, and improved weather resistance. Leading manufacturers have introduced models with measurement accuracy within ±1% and wind speed ranges up to 60 m/s. The ultrasonic segment is projected to grow at 7.2% CAGR through 2032, faster than mechanical variants, due to these technological improvements and lower maintenance requirements.

MARKET RESTRAINTS

High Initial Costs Limit Widespread Adoption

While offering superior functionality, bidirectional anemometers typically command premium pricing compared to conventional wind measurement devices. Advanced ultrasonic models can cost 3-5 times more than basic mechanical anemometers, creating adoption barriers in price-sensitive markets and applications. The initial investment for professional-grade systems, including installation and calibration, often exceeds $5,000, restricting usage to well-funded organizations and large-scale projects.

Technical Complexities in Extreme Environments Challenge Reliability

Bidirectional anemometers face performance limitations in harsh weather conditions that can impact data accuracy. Icing conditions, heavy rain, and extreme temperatures affect sensor reliability, particularly for ultrasonic models. In polar regions and high-altitude installations, specialized (and more expensive) heated versions are required to maintain functionality. These environmental challenges increase total cost of ownership and complicate deployment in critical applications like aviation weather stations and offshore wind farms.

Regulatory Compliance Adds Implementation Costs

Stringent certification requirements for wind measurement instruments in aviation and energy applications create additional market barriers. Obtaining certifications like ISO 16622 for meteorological measurements or IEC 61400 for wind turbine applications involves lengthy testing procedures and significant documentation. These compliance processes can delay product launches by 6-12 months and increase development costs by 15-20%, particularly for manufacturers targeting global markets with differing regional standards.

MARKET OPPORTUNITIES

Smart City Initiatives Create New Application Areas

Urban wind monitoring for smart city infrastructure presents a growing opportunity for bidirectional anemometer manufacturers. Modern cities are deploying networked wind sensors for building ventilation optimization, pollution dispersion tracking, and urban microclimate studies. The global smart city market is projected to reach $1 trillion by 2030, with environmental monitoring solutions representing a fast-growing segment that increasingly incorporates advanced wind measurement technologies.

Integration with AI and IoT Opens New Possibilities

The combination of bidirectional anemometers with artificial intelligence and IoT platforms is enabling predictive analytics for various industries. Energy companies are using AI-powered wind forecasting systems that integrate data from multiple anemometers to optimize turbine performance. Similarly, port authorities and aviation facilities employ networked wind monitoring for operational safety. These advanced applications command higher margins and create recurring revenue streams through data services and analytics.

Emerging Markets Offer Significant Growth Potential

Developing nations investing in renewable energy and modern meteorological infrastructure represent an untapped market. Countries in Southeast Asia, Latin America, and Africa are establishing new weather monitoring networks and wind farms, driving demand for cost-effective yet accurate wind measurement solutions. Manufacturers developing localized products with regional certifications and language support are well-positioned to capture this growth, particularly as governments implement stricter environmental monitoring regulations.

MARKET CHALLENGES

Intense Competition from Alternative Technologies

Bidirectional anemometers face competition from lower-cost alternatives like unidirectional anemometers and emerging remote sensing technologies. Lidar-based wind measurement systems, while more expensive, offer advantages for certain applications by measuring wind profiles at multiple altitudes. Additionally, some industries are adopting predictive models using historical data instead of continuous monitoring, potentially reducing demand for physical anemometers in non-critical applications.

Supply Chain Disruptions Impact Manufacturing

The specialized components required for high-precision bidirectional anemometers, particularly ultrasonic sensors and calibration equipment, remain vulnerable to supply chain interruptions. Semiconductor shortages affecting sensor manufacturing and trade disputes impacting specialized alloys have caused delivery delays and cost increases. These disruptions complicate production planning for manufacturers and can lead to extended lead times for end-users, particularly for customized or high-specification models.

Data Standardization and Integration Hurdles

The lack of universal data protocols for wind measurement creates integration challenges in multi-sensor systems. Various manufacturers use proprietary output formats and communication protocols, requiring custom interfaces for data aggregation platforms. This fragmentation increases implementation costs and limits interoperability between equipment from different vendors, slowing adoption in large-scale monitoring networks where standardization is critical for effective data analysis.

BIDIRECTIONAL ANEMOMETER MARKET TRENDS

Rising Demand for Precise Wind Measurement in Renewable Energy Fuels Market Growth

The global bidirectional anemometer market is experiencing significant growth, driven by increasing applications in the renewable energy sector, particularly wind farms. As governments worldwide push for sustainable energy solutions, the installation of wind turbines has surged, requiring highly accurate wind measurement tools to optimize performance and ensure safety. Bidirectional anemometers, with their ability to measure wind speed in both horizontal and vertical planes, are becoming indispensable in assessing wind patterns for turbine placement and efficiency. Reports indicate that investments in wind energy projects grew by approximately 23% in 2023, further propelling the demand for these devices.

Other Trends

Advancements in Ultrasonic Anemometer Technology

Ultrasonic bidirectional anemometers are gaining traction due to their precision, durability, and lack of moving parts compared to traditional mechanical variants. The adoption of ultrasonic models has increased by nearly 15% annually, attributed to their superior performance in extreme weather conditions. Leading manufacturers are integrating IoT and AI capabilities into these devices, enabling real-time data analytics and predictive maintenance, which is revolutionizing wind monitoring in industries such as aviation and meteorological research.

Expansion of Environmental Monitoring Applications

Environmental monitoring agencies are increasingly deploying bidirectional anemometers to track air quality and pollutant dispersion patterns. With stricter environmental regulations being enforced globally, the need for accurate wind data in urban and industrial areas has amplified. Cities with high pollution levels, such as Beijing and Delhi, are investing heavily in air quality monitoring systems, where bidirectional anemometers play a critical role. Additionally, the growing emphasis on climate change studies is driving research institutions to adopt these instruments for atmospheric research, further expanding their market reach.

Challenges in Adoption for Small-Scale Industries

Despite their advantages, high costs associated with advanced bidirectional anemometers remain a barrier for small-scale industries and developing regions. While ultrasonic variants offer superior accuracy, their price point is approximately 30% higher than mechanical alternatives, limiting their adoption among budget-constrained sectors. Furthermore, the complexity of integrating these devices with existing infrastructure poses operational challenges, particularly in regions with limited technical expertise. However, manufacturers are gradually introducing cost-effective models to address these concerns and expand their customer base.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Technological Advancements Drive Market Competition

The global bidirectional anemometer market features a mix of established players and emerging competitors, with the top five manufacturers accounting for a significant revenue share in 2024. The market is characterized by continuous technological advancements as companies invest in R&D to enhance the accuracy, durability, and application scope of their devices.

TSI Incorporated leads the market, leveraging its strong brand recognition and extensive distribution network across North America, Europe, and Asia. The company’s product portfolio includes high-precision ultrasonic and thermal anemometers tailored for industrial and environmental applications. Meanwhile, OMEGA Engineering has strengthened its position through strategic acquisitions and partnerships, expanding its reach in the aerospace and energy sectors.

Asian manufacturers like Dongguan Wanchuang Electronics and Shenzhen Huayi Instruments are gaining traction with cost-effective solutions for meteorological and environmental monitoring applications. While they currently hold smaller market shares compared to global leaders, their focus on local market needs and competitive pricing strategies position them for future growth.

The competitive landscape continues to evolve as smaller specialized players carve out niches in vertical markets. For example, Gill Instruments maintains a strong presence in marine and renewable energy applications, while KIMO Instruments focuses on HVAC and building ventilation systems. This segmentation of applications helps moderate competition within specific market subsets.

List of Key Bidirectional Anemometer Manufacturers

- TSI Incorporated (U.S.)

- Kanomax (Japan)

- Gill Instruments (UK)

- METEOOM (France)

- OMEGA Engineering (U.S.)

- KIMO Instruments (France)

- Fluke International (U.S.)

- Dongguan Wanchuang Electronics (China)

- Ulead Group (China)

- Shenzhen Huayi Instruments (China)

- Shenzhen Jumaoyuan Technology (China)

- Lanju Intelligent Technology (China)

- Shandong Renke Measurement and Control Technology (China)

- Shandong Jingdao Optoelectronics Technology (China)

- Beijing Huakong Xingye Technology Development (China)

- Shenzhen Fengtu Technology (China)

- Shanghai Huatu Instruments (China)

- Suzhou Yushan Sensing Technology (China)

- Guangli Technology Group (China)

- Shandong Dingmei Intelligent Equipment (China)

Market leaders are increasingly shifting their focus toward smart, connected anemometers with IoT capabilities, while mid-sized players differentiate through application-specific designs and localized customer support. The emergence of Chinese manufacturers brings new dynamics to pricing strategies and regional market penetration. Although the market remains fragmented by application and geography, consolidation through mergers and acquisitions appears likely as companies seek to broaden their technological capabilities and geographic footprints.

Segment Analysis:

By Type

Mechanical Segment Leads Due to High Reliability and Cost-Effectiveness in Diverse Environments

The market is segmented based on type into:

- Mechanical

- Subtypes: Cup anemometers, vane anemometers, and others

- Ultrasonic

- Thermal

- Subtypes: Hot-wire sensors, thermal dispersion sensors, and others

By Application

Meteorological Observation Segment Dominates Due to Critical Role in Weather Forecasting and Climate Studies

The market is segmented based on application into:

- Meteorological Observation

- Aerospace

- Environmental Monitoring

- Energy Industry

- Others

By End-User

Commercial and Industrial Sector Leads Due to Growing Demand for Airflow Measurement in HVAC and Manufacturing

The market is segmented based on end-user into:

- Government & Research Institutes

- Commercial & Industrial

- Energy & Utilities

- Others

Regional Analysis: Bidirectional Anemometer Market

Asia-Pacific

The Asia-Pacific region dominates the global bidirectional anemometer market, accounting for the largest revenue share in 2024. China leads regional demand due to extensive infrastructure development and government-backed meteorological research initiatives. The country’s ambitious renewable energy targets, including 1,200 GW of installed wind and solar capacity by 2030, necessitate advanced wind measurement solutions. India follows closely with growing investments in smart cities and environmental monitoring systems. Japan maintains a stable demand for high-precision ultrasonic anemometers in aerospace and automotive testing applications. The region benefits from concentrated manufacturing hubs of key players like Shenzhen Huayi Instruments and Dongguan Wanchuang Electronics, optimizing supply chains.

North America

North America represents the second-largest market, driven by stringent EPA air quality monitoring requirements and advanced aerospace applications. The U.S. accounts for over 75% of regional demand, with particular strength in thermal anemometers for HVAC optimization in commercial buildings. Recent FAA mandates for airport wind shear detection systems have created new opportunities. Canada’s focus on Arctic climate research and wind farm development in Alberta continues to spur demand. Local manufacturers like TSI and OMEGA Engineering lead innovation in ruggedized designs for harsh environments, though high product costs somewhat limit market penetration.

Europe

Europe shows steady growth fueled by renewable energy expansion and EU environmental directives. Germany remains the largest market, with its thriving wind energy sector requiring precise wind resource assessment tools. The UK’s offshore wind ambitions, targeting 50 GW by 2030, create sustained demand for marine-grade anemometers. Scandinavia contributes significantly through its specialized meteorological institutes and cold climate research programs. European manufacturers like KIMO Instruments emphasize energy-efficient ultrasonic models, though competition from Asian producers intensifies price pressures. The region’s mature market sees replacement demand outpacing new installations.

South America

The South American market remains nascent but shows promise, particularly in Brazil’s expanding wind power sector which reached 30 GW capacity in 2024. Argentina’s renewable energy auctions stimulate intermittent demand peaks. However, economic instability and currency fluctuations limit capital investments in advanced monitoring equipment. Most countries rely on imported Chinese models due to cost advantages, though this creates challenges with maintenance and calibration. Mining applications in Chile and Peru generate steady demand for explosion-proof variants, but the overall market remains price-sensitive with slow adoption of premium technologies.

Middle East & Africa

This emerging market benefits from large-scale renewable energy projects in the GCC countries, particularly solar-wind hybrid installations requiring microclimate analysis. Saudi Arabia’s NEOM smart city project represents a major demand driver. Africa’s market grows slowly but steadily, with South Africa leading in wind farm development and Morocco expanding its meteorological infrastructure. The lack of local manufacturing necessitates imports, creating logistical challenges. Dust and extreme temperatures necessitate frequent sensor replacements, though this also drives aftermarket opportunities. The region shows long-term potential but requires infrastructure development to unlock growth.

Report Scope

This market research report provides a comprehensive analysis of the Global Bidirectional Anemometer Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 291 million in 2024 and is projected to reach USD 430 million by 2032, growing at a CAGR of 5.8%.

- Segmentation Analysis: Detailed breakdown by product type (Mechanical, Ultrasonic, Thermal), application (Meteorological Observation, Aerospace, Environmental Monitoring, Energy Industry, Others), and end-user industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis for key markets like the U.S., China, Germany, and Japan.

- Competitive Landscape: Profiles of leading market participants including TSI, Kanomax, Gill Instruments, OMEGA Engineering, and Fluke International, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, IoT integration, and advanced materials in bidirectional anemometer design.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand for precise wind measurement in renewable energy projects versus challenges like high equipment costs.

- Stakeholder Analysis: Strategic insights for manufacturers, suppliers, research institutions, and government agencies operating in the wind measurement sector.

The research employs both primary and secondary methodologies, including interviews with industry experts, manufacturer data analysis, and verification through multiple authoritative sources to ensure data accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Bidirectional Anemometer Market?

->Bidirectional Anemometer Market was valued at 291 million in 2024 and is projected to reach US$ 430 million by 2032, at a CAGR of 5.8% during the forecast period.

Which key companies operate in Global Bidirectional Anemometer Market?

-> Key players include TSI, Kanomax, Gill Instruments, OMEGA Engineering, Fluke International, KIMO Instruments, and METEOOM, among others.

What are the key growth drivers?

-> Major growth drivers include increasing renewable energy projects, stricter environmental monitoring regulations, and advancements in aerospace technology requiring precise wind measurement.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include integration of IoT capabilities, development of low-power wireless anemometers, and increasing adoption in smart city infrastructure projects.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...