Market Insights

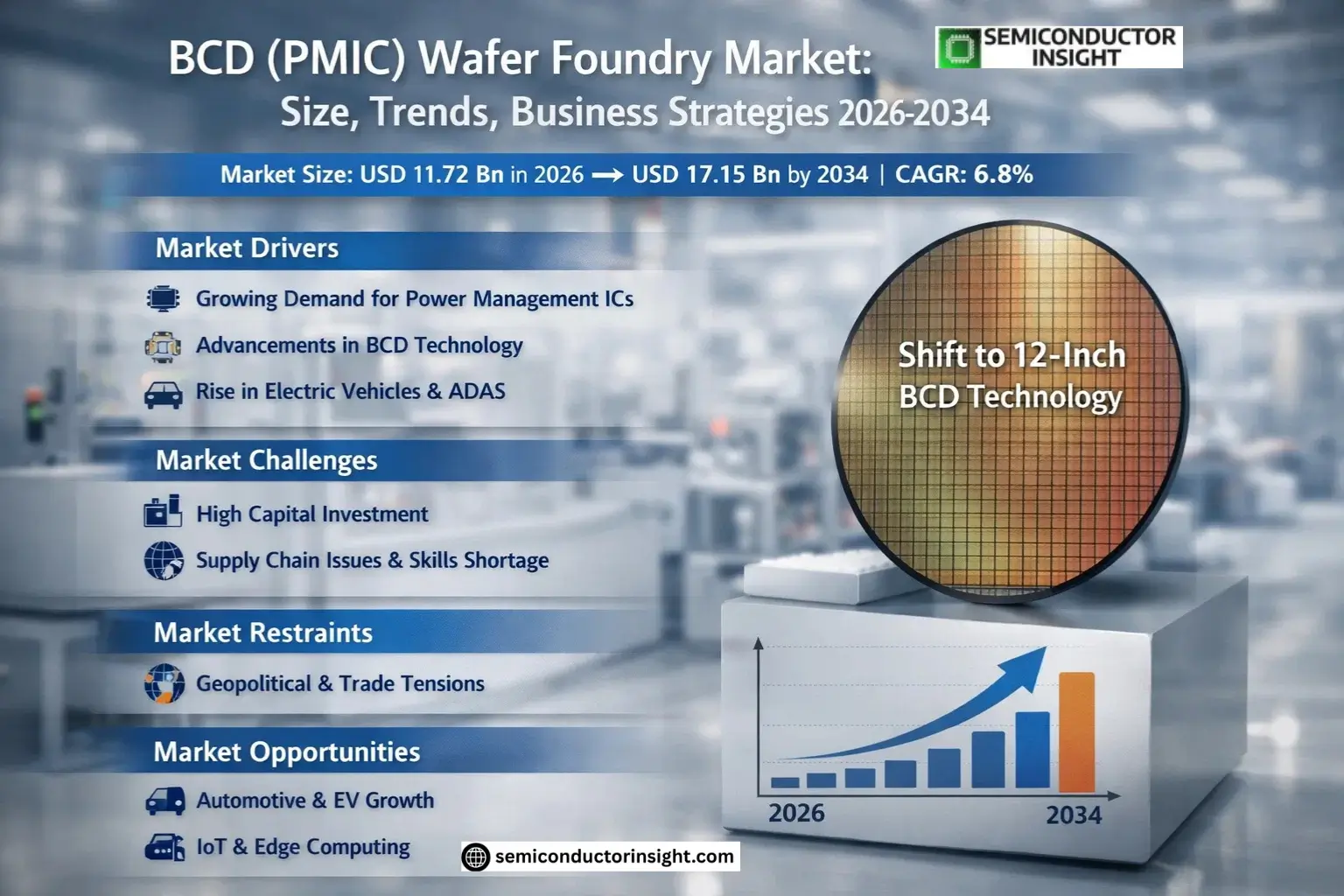

Global BCD (PMIC) Wafer Foundry Market size was valued at USD 10.96 billion in 2025. The market is projected to grow from USD 11.72 billion in 2026 to USD 17.15 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

BCD (Bipolar-CMOS-DMOS) technology is a specialized semiconductor manufacturing process that integrates bipolar, CMOS, and DMOS components on a single chip, enabling high-performance power management integrated circuits (PMICs). These wafers are critical for applications requiring efficient power conversion, voltage regulation, and signal processing in compact form factors.

The market growth is driven by increasing demand for energy-efficient electronics across industries such as automotive, consumer electronics, and industrial automation. The rise of electric vehicles and IoT devices has particularly accelerated adoption of BCD-based PMICs due to their superior thermal performance and power density. Leading foundries like TSMC and Samsung are expanding production capacity to meet this demand while developing advanced node technologies for next-generation applications.

MARKET DRIVERS

Growing Demand for Power Management ICs

BCD (PMIC) Wafer Foundry Market is experiencing strong growth due to increasing demand for power management integrated circuits in consumer electronics, automotive, and industrial applications. The widespread adoption of 5G and IoT devices has further accelerated the need for efficient BCD (PMIC) solutions.

Advancements in BCD Technology

Technological innovations in BCD (PMIC) wafer fabrication, including smaller node processes and improved power efficiency, are driving market expansion. Foundries are investing heavily in R&D to meet the growing complexity of power management requirements across various industries.

The automotive sector’s shift towards electric vehicles and advanced driver-assistance systems (ADAS) is creating significant demand for high-performance BCD (PMIC) solutions from specialized wafer foundries.

MARKET CHALLENGES

High Capital Investment Requirements

Establishing and maintaining BCD (PMIC) wafer foundries requires substantial capital investment in specialized equipment and cleanroom facilities. This creates high barriers to entry for new market participants.

Other Challenges

Supply Chain Complexities

BCD (PMIC) Wafer Foundry Market faces challenges from global semiconductor supply chain disruptions and material shortages, impacting production timelines and costs.

Technical Expertise Shortage

There is a growing shortage of skilled professionals with specialized knowledge in BCD (PMIC) process technology, creating bottlenecks in capacity expansion.

MARKET RESTRAINTS

Geopolitical and Trade Tensions

Regional trade restrictions and geopolitical tensions are impacting the global BCD (PMIC) Wafer Foundry Market , particularly affecting technology transfers and equipment procurement between major semiconductor-producing regions.

MARKET OPPORTUNITIES

Expansion in Automotive Applications

The automotive industry presents significant growth opportunities for BCD (PMIC) wafer foundries, with increasing demand for power management solutions in electric vehicles, infotainment systems, and advanced safety features.

Emerging IoT and Edge Computing

The proliferation of IoT devices and edge computing architectures is creating new opportunities for BCD (PMIC) wafer foundries to provide specialized power management solutions for low-power, high-efficiency applications.

BCD (PMIC) Wafer Foundry Market Trends

Shift Toward 12-inch BCD Technology Dominance

BCD (PMIC) Wafer Foundry Market is witnessing accelerated adoption of 12-inch BCD (Bipolar-CMOS-DMOS) technology, driven by superior cost efficiencies and higher productivity. This transition is reshaping manufacturing strategies among leading foundries, with capacity expansions focusing primarily on larger wafer sizes to meet automotive and industrial application demands.

Other Trends

Automotive Electronics Driving Market Growth

Automotive applications account for over 30% of BCD (PMIC) Wafer Foundry demand, fueled by increasing vehicle electrification and advanced driver-assistance systems (ADAS). Semiconductor manufacturers are prioritizing automotive-grade BCD processes to ensure reliability under harsh operating conditions.

Geographic Expansion in Asia-Pacific

China’s semiconductor self-sufficiency initiatives are driving significant investments in domestic BCD (PMIC) Wafer Foundry capabilities. SMIC and Hua Hong Semiconductor are expanding 8-inch and 12-inch BCD production lines to reduce reliance on imported power management ICs, with Southeast Asia emerging as a strategic manufacturing hub.

Technological Integration Challenges

While BCD technology offers advantages in power efficiency, foundries face integration challenges with advanced nodes below 40nm. The industry is developing hybrid solutions combining BCD with FinFET technologies to address performance requirements in advanced PMIC applications.

Supply Chain Diversification

GlobalFoundries and UMC are establishing redundant BCD (PMIC) Wafer Foundry capacity across multiple regions to mitigate geopolitical risks. This strategy responds to increasing demand for localized semiconductor supply chains in North America and Europe following recent chip shortages.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominance of Top Foundries in BCD (PMIC) Wafer Production

TSMC and Samsung Foundry lead the BCD (PMIC) Wafer Foundry Market with advanced 12-inch BCD technology nodes and significant capacity allocations. These top two players accounted for over 45% of global production capacity in 2025, serving major power management IC designers across automotive, smartphone and industrial sectors. GlobalFoundries and UMC follow as strong second-tier competitors with specialized 8-inch BCD lines, particularly strong in automotive PMIC production.

China’s SMIC and Hua Hong Semiconductor have rapidly expanded their BCD foundry capabilities to serve local PMIC designers, leveraging government support and domestic demand. Specialty foundries like Tower Semiconductor (now owned by Intel) and X-FAB maintain strong positions in niche applications requiring high-voltage BCD processes. Emerging players like Nexchip and GTA Semiconductor are investing heavily to capture growing demand from Chinese EV and consumer electronics markets.

List of Key BCD (PMIC) Wafer Foundry Companies Profiled

- TSMC

- Samsung Foundry

- GlobalFoundries

- United Microelectronics Corporation (UMC)

- SMIC

- Tower Semiconductor

- PSMC

- VIS (Vanguard International Semiconductor)

- Hua Hong Semiconductor

- HLMC

- X-FAB

- DB HiTek

- Nexchip

- Intel Foundry Services (IFS)

- GTA Semiconductor Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

12-inch BCD dominates due to higher production efficiency and superior performance characteristics:

|

| By Application |

|

Automotive Electronics shows the strongest growth potential:

|

| By End User |

|

Fabless Semiconductor Companies represent the fastest-growing segment:

|

| By Technology Node |

|

90nm-40nm remains most widely adopted:

|

| By Integration Level |

|

System-on-Chip Solutions gaining traction:

|

Regional Analysis: Asia-Pacific BCD (PMIC) Wafer Foundry Market

Taiwanese foundries developed 0.18μm BCD platforms with ultra-low RDS(on) for automotive PMICs, combined with AI-assisted thermal simulation tools that optimize chip layouts. These advancements enable higher power density solutions demanded by EV manufacturers worldwide.

With IATF 16949 certified facilities, Taiwan’s foundries supply AEC-Q100 qualified BCD PMICs to global Tier 1 suppliers. The region’s earthquake-resistant wafer fabs ensure supply chain resilience for mission-critical automotive power management applications.

Machine learning algorithms analyze wafer test data across multiple BCD lots to identify process variations. This AI integration reduces defect rates by correlating electrical parameters with fab metrology data, crucial for high-voltage PMIC production.

Taiwanese foundries lead in 3D stacking of BCD PMICs with CMOS logic, developing through-silicon-via solutions. This enables compact power delivery networks for AI accelerators and 5G RF modules, creating new market opportunities through 2034.

China

China is rapidly expanding its BCD (PMIC) foundry capabilities through domestic champions like SMIC and Hua Hong Semiconductor. Government subsidies under the “Made in China 2025” initiative target self-sufficiency in power management ICs. New 200mm BCD lines focus on consumer electronics PMICs, though lag behind Taiwan in automotive-grade processes. Local design houses benefit from preferential foundry access, creating a resilient regional supply chain for power ICs.

South Korea

Korean foundries excel in high-performance BCD processes for display driver PMICs and smartphone power management. Samsung Foundry’s 90nm BCD platform incorporates FinFET elements for ultra-low power applications. The region leads in PMIC-panel integration for foldable displays, though faces challenges in establishing automotive qualification at scale compared to Taiwanese counterparts.

Japan

Japan maintains strong capabilities in high-reliability BCD processes through Renesas’ in-house fabs. The region specializes in industrial-grade PMICs with extreme temperature tolerance, leveraging decades of power semiconductor expertise. Aging 200mm facilities present modernization challenges, but Japanese foundries remain critical for aerospace and railway power management solutions.

Rest of Asia-Pacific

Singapore and Malaysia host important BCD (PMIC) back-end operations with advanced test/packaging facilities. These nations benefit from Western IDMs outsourcing power IC manufacturing, offering geopolitical supply chain diversification. Emerging Indian foundries are entering the BCD market through government-supported analog semiconductor initiatives.

Report Scope

This market research report provides a comprehensive analysis of the BCD (PMIC) Wafer Foundry Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of BCD (PMIC) Wafer Foundry Market?

-> BCD (PMIC) Wafer Foundry Market size was valued at USD 10.96 billion in 2025. The market is projected to grow from USD 11.72 billion in 2026 to USD 17.15 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

What is the growth rate (CAGR) of BCD (PMIC) Wafer Foundry Market?

-> The market is expected to grow at a CAGR of 6.8% during the forecast period (2025-2034).

Which key companies operate in BCD (PMIC) Wafer Foundry Market?

-> Key players include TSMC, Samsung Foundry, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, PSMC, VIS (Vanguard International Semiconductor), Hua Hong Semiconductor, HLMC, among others.

Which region dominates the market?

-> Asia dominates the market with significant contributions from China, Japan, and South Korea.

What are the key applications of BCD (PMIC) Wafer Foundry?

-> Major applications include Smart Phone, Automotive Electronics, Consumer Electronics, and Industrial sectors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...