Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market Insights

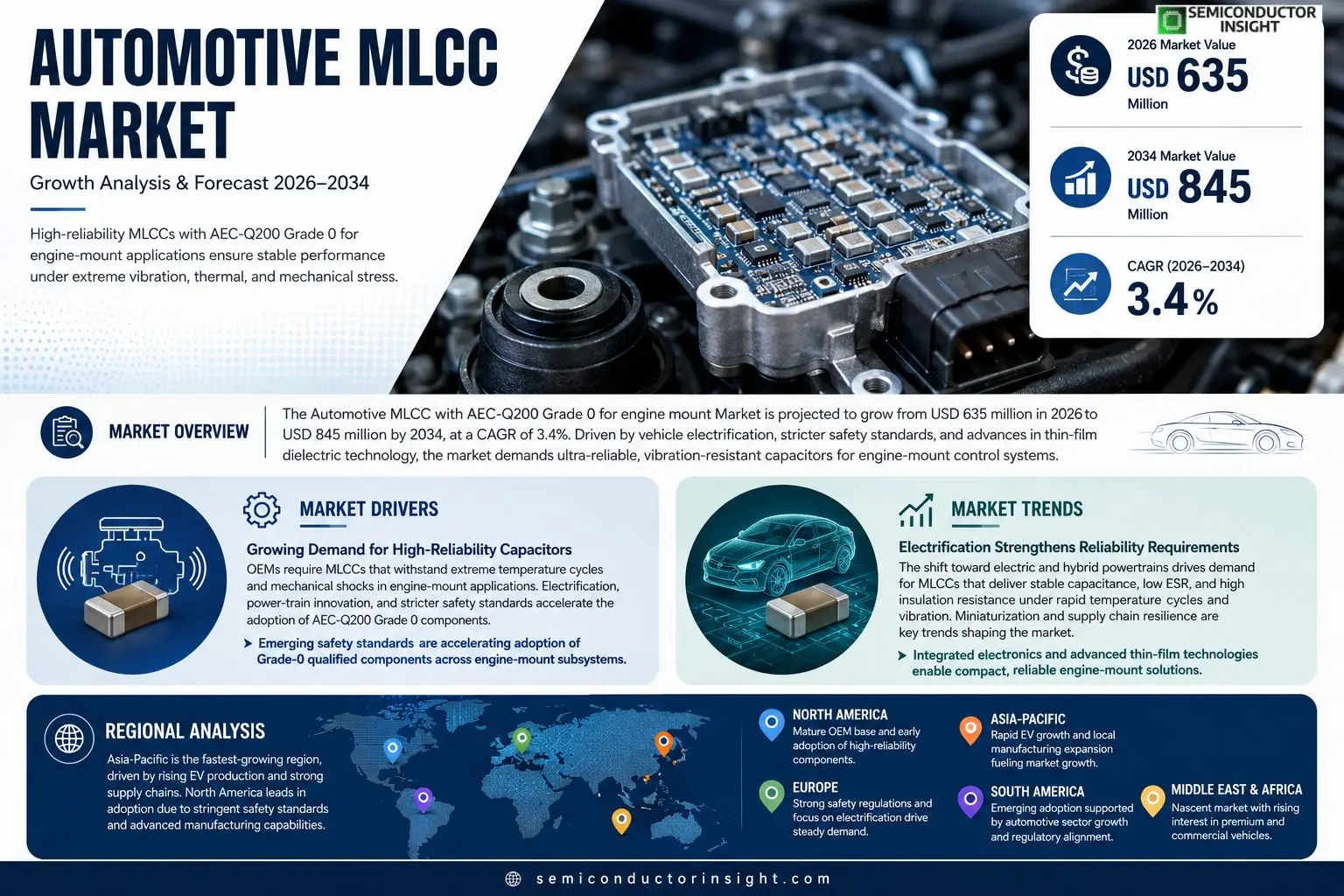

Automotive multilayer ceramic capacitor (MLCC) market segment that meets AEC‑Q200 Grade 0 specifications for engine‑mount applications was valued at USD 620 million in 2025. The market is projected to expand from USD 635 million in 2026 to USD 845 million by 2034, exhibiting a CAGR of approximately 3.4% during the forecast period.

Automotive MLCCs compliant with AEC‑Q200 Grade 0 are high‑reliability components designed to withstand the severe thermal‑mechanical stresses of engine‑mount systems. They provide stable capacitance, low ESR, and robust insulation resistance, ensuring reliable vibration damping and electronic control unit (ECU) performance under harsh operating conditions.The market is gaining momentum because vehicle electrification drives higher demand for precise vibration control, while stricter safety standards push OEMs toward Grade 0 qualified parts. Furthermore, advances in thin‑film dielectric technology reduce package size without compromising durability, encouraging broader adoption across both passenger‑car and commercial‑vehicle platforms.

MARKET DRIVERS

Growing Demand for High‑Reliability Capacitors

Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market is being propelled by OEMs that require capacitors capable of withstanding severe temperature cycles and mechanical shocks typical of engine‑mount applications. Recent vehicle platforms integrate advanced driver‑assist systems that increase the electrical load on engine‑mount electronics, creating a clear need for ultra‑reliable MLCCs.

Electrification and Power‑train Innovation

Electrified powertrains generate higher frequency switching events, driving demand for MLCCs that meet the stringent AEC‑Q200 Grade 0 qualification. Analysts observe that hybrid and mild‑hybrid models now account for a sizable portion of new‑car sales, directly boosting the volume of high‑grade capacitors required for engine‑mount control modules.

➤ Emerging safety standards are accelerating adoption of Grade‑0 qualified components across engine‑mount subsystems.

Furthermore, suppliers are investing in low‑ESR designs that improve energy efficiency, offering manufacturers a tangible route to meet both performance targets and regulatory emissions limits.

MARKET CHALLENGES

Regulatory and Cost Pressures

While the market benefits from stricter safety mandates, the cost premium associated with Grade‑0 certification can strain component budgets, especially for volume‑sensitive engine‑mount applications. Manufacturers must balance compliance with price competitiveness.

Other Challenges

Supply Chain Constraints

A limited number of foundries possess the clean‑room infrastructure required for AEC‑Q200 Grade 0 production, leading to longer lead‑times and occasional shortages during peak demand periods.

MARKET RESTRAINTS

Limited Tier‑One Adoption

Some Tier‑one OEMs remain cautious, preferring legacy capacitor technologies until long‑term reliability data for the new Grade‑0 MLCCs are fully validated across diverse engine‑mount environments. This hesitancy tempers the overall market expansion rate.

MARKET OPPORTUNITIES

Advanced Miniaturization Trends

Engine‑mount control units are trending toward greater integration, presenting opportunities for manufacturers that can deliver ultra‑compact, high‑reliability MLCCs meeting the AEC‑Q200 Grade 0 standard. Companies that innovate in package density while maintaining compliance are well‑positioned to capture emerging demand.

Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market Trends

Electrification Strengthens Reliability Requirements

The shift toward electric and hybrid powertrains is reshaping component requirements across the power‑train. In engine‑mount applications, the need for stable capacitance under rapid temperature cycles has become a decisive factor. Automotive MLCC with AEC‑Q200 Grade 0 for engine mount Market participants are therefore emphasizing designs that retain low equivalent series resistance and high insulation resistance, which together support consistent ECU performance during intense vibration events. Manufacturers are also integrating advanced thin‑film dielectric layers that allow a smaller footprint without sacrificing the mechanical robustness required for mounting locations. This technical direction aligns with OEM specifications that increasingly reference Grade 0 compliance as a baseline for safety‑critical modules.

Other Trends

Supply Chain Resilience

supply chains for high‑reliability ceramic capacitors have been adjusted to mitigate component shortages and lead‑time volatility. Producers are expanding capacity at key foundries while adopting tighter quality‑control loops that certify AEC‑Q200 Grade 0 conformance on each lot. Collaborative forecasting with Automotive OEMs enables more accurate demand planning, reducing buffer inventory while preserving the stringent reliability standards required for engine‑mount installations. At the same time, the push toward regionalized production hubs shortens logistics pathways, which helps maintain the thermal‑mechanical integrity of the capacitors throughout handling and transportation.

Integrated Electronics Strategies

Vehicle architecture trends are encouraging greater integration of power‑train control electronics with vibration‑damping functions. By embedding Automotive MLCC with AEC‑Q200 Grade 0 directly into mounting modules, system designers achieve tighter feedback loops for active vibration control, improving ride comfort and extending the service life of surrounding components. This integration is supported by ongoing advancements in thin‑film dielectric processing that deliver both high reliability and reduced package size, making it feasible to place capacitors in space‑constrained engine compartments. As safety standards evolve, the industry expects further convergence of mechanical and electronic design, reinforcing the role of Grade 0 compliant MLCCs in future power‑train platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive MLCC with AEC‑Q200 Grade 0 for Engine‑Mount Applications

The Automotive multilayer ceramic capacitor (MLCC) segment that satisfies AEC‑Q200 Grade 0 specifications has solidified a clear hierarchy, with Tier‑1 manufacturers such as TDK Corporation and Murata Manufacturing dominating the volume and technology frontier. Their extensive thin‑film dielectric portfolios, combined with deep Automotive‑grade supply chains, allow them to capture the bulk of the USD 620 million market recorded in 2025 and to leverage the projected 3.4 % CAGR through 2034. Both companies have announced dedicated road‑map investments targeting vibration‑damping performance and package miniaturization for engine‑mount ECUs, positioning them as the benchmark for reliability and cost efficiency. The market structure therefore reflects a duopolistic core that drives pricing, standards compliance, and OEM partnership dynamics, while also creating entry barriers for newer entrants that must meet stringent qualification processes.Beyond the duopoly, a cohort of niche yet strategically important players enriches the competitive fabric. Companies such as Kyocera Corporation, Samsung Electro‑Mechanics, and AVX Corporation (now part of KEMET) focus on specialty dielectric formulations that enhance insulation resistance under extreme thermal cycles. Meanwhile, regional specialists including Taiyo Yuden, Vishay Intertechnology, NEC Tokin, and Sumitomo Electric provide tailored form‑factor solutions for commercial‑vehicle platforms where space constraints are paramount. Emerging innovators like NXP Semiconductors’ passive‑component division and Taiwan‑based Yageo are expanding their Automotive portfolios through targeted acquisitions and joint‑development programs, seeking to capture niche market shares in electric‑vehicle power‑train vibration control. This diversified ecosystem ensures continuous technology diffusion while preserving competitive pressure across the value chain.

List of Key Automotive MLCC with AEC‑Q200 Grade 0 Companies Profiled

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Kyocera Corporation

- Samsung Electro‑Mechanics

- AVX Corporation

- Vishay Intertechnology

- Taiyo Yuden Co., Ltd.

- NEC Tokin Corporation

- Sumitomo Electric Industries

- KEMET Corporation

- Yageo Corporation

- NXP Semiconductors (Passive Components Division)

- Panasonic Electronic Devices

- TDK-Lambda (subsidiary focusing on high‑reliability caps)

- ROHM Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thin‑film MLCC

|

| By Application |

|

Engine Mount Vibration Damping

|

| By End User |

|

Passenger Cars

|

| By Technology |

|

High‑Temperature Dielectric

|

| By Vehicle Platform |

|

SUV

|

Regional Analysis: Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market

North America

Major OEMs in the United States and Canada prioritize reliability, prompting a shift toward AEC‑Q200 Grade 0 MLCCs for engine‑mount control units. Their design cycles increasingly allocate early‑stage testing budgets, ensuring component robustness under harsh vibration and temperature conditions.

Silicon Valley and Detroit host advanced fabrication facilities that leverage low‑defect processes. These hubs enable rapid prototyping of high‑performance MLCCs, supporting Automotive suppliers seeking to meet stringent AEC‑Q200 criteria.

Federal safety mandates encourage adoption of Grade 0 components, aligning with FMVSS and SAE standards. Compliance audits drive continuous improvement, reinforcing market confidence in North American offerings.

Strategic stockpiling and diversified sourcing mitigate raw‑material volatility, ensuring uninterrupted supplies of high‑grade MLCCs for engine‑mount applications throughout the forecast horizon.

Europe

European Automotive manufacturers emphasize sustainability and electrification, prompting a gradual transition to high‑reliability MLCCs in engine‑mount control systems. While the region lags slightly behind North America in sheer volume, rigorous UNECE safety directives and strong collaborative networks among German and French OEMs foster steady demand for AEC‑Q200 Grade 0 components. Regional clusters in Germany and the United Kingdom focus on integrating these MLCCs into next‑generation powertrain architectures, reinforcing Europe’s competitive edge in luxury and performance segments.

Asia‑Pacific

Asia‑Pacific exhibits rapid expansion of the Automotive MLCC with AEC‑Q200 Grade 0 for engine mount Market, driven by burgeoning EV production in China, Japan, and South Korea. Manufacturers balance cost considerations with reliability, leading to increased investment in advanced ceramic technologies. Local supply chains benefit from abundant raw‑material sources, yet quality assurance remains a focal point to meet AEC‑Q200 expectations. Collaborative R&D programs between OEMs and semiconductor firms accelerate the introduction of region‑specific solutions.

South America

In South America, market growth is anchored by Brazil’s expanding Automotive sector and Mexico’s role as a manufacturing gateway to North America. While overall volumes are modest, OEMs are progressively adopting AEC‑Q200 Grade 0 MLCCs to comply with emerging safety regulations and to enhance durability in harsh road conditions. Partnerships with North American suppliers facilitate technology transfer, gradually elevating regional expertise in high‑reliability components.

Middle East & Africa

The Middle East & Africa region shows nascent yet promising interest in high‑grade Automotive MLCCs, particularly within premium vehicle segments in the Gulf Cooperation Council nations. Harsh climatic environments underscore the need for robust engine‑mount electronics, encouraging selective adoption of AEC‑Q200 Grade 0 components. Meanwhile, emerging Automotive hubs in South Africa are beginning to align with standards, setting the stage for gradual market maturation over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as Automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market?

-> Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market was valued at USD 620 million in 2025 and is expected to reach USD 845 million by 2034.

Which key companies operate in Automotive MLCC with AEC-Q200 Grade 0 for engine mount Market?

-> Key players include Murata Manufacturing, TDK Corporation, AVX Corporation, Kyocera, Samsung Electro-Mechanics, and Taiyo Yuden, among others.

What are the key growth drivers?

-> Key growth drivers include vehicle electrification demanding precise vibration control, stricter safety standards requiring Grade 0 qualification, and advances in thin‑film dielectric technology enabling smaller, durable packages.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include miniaturization of MLCCs, integration of AI/IoT for smart engine‑mount monitoring, and development of ultra‑low ESR capacitors for high‑frequency applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...