Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market Insights

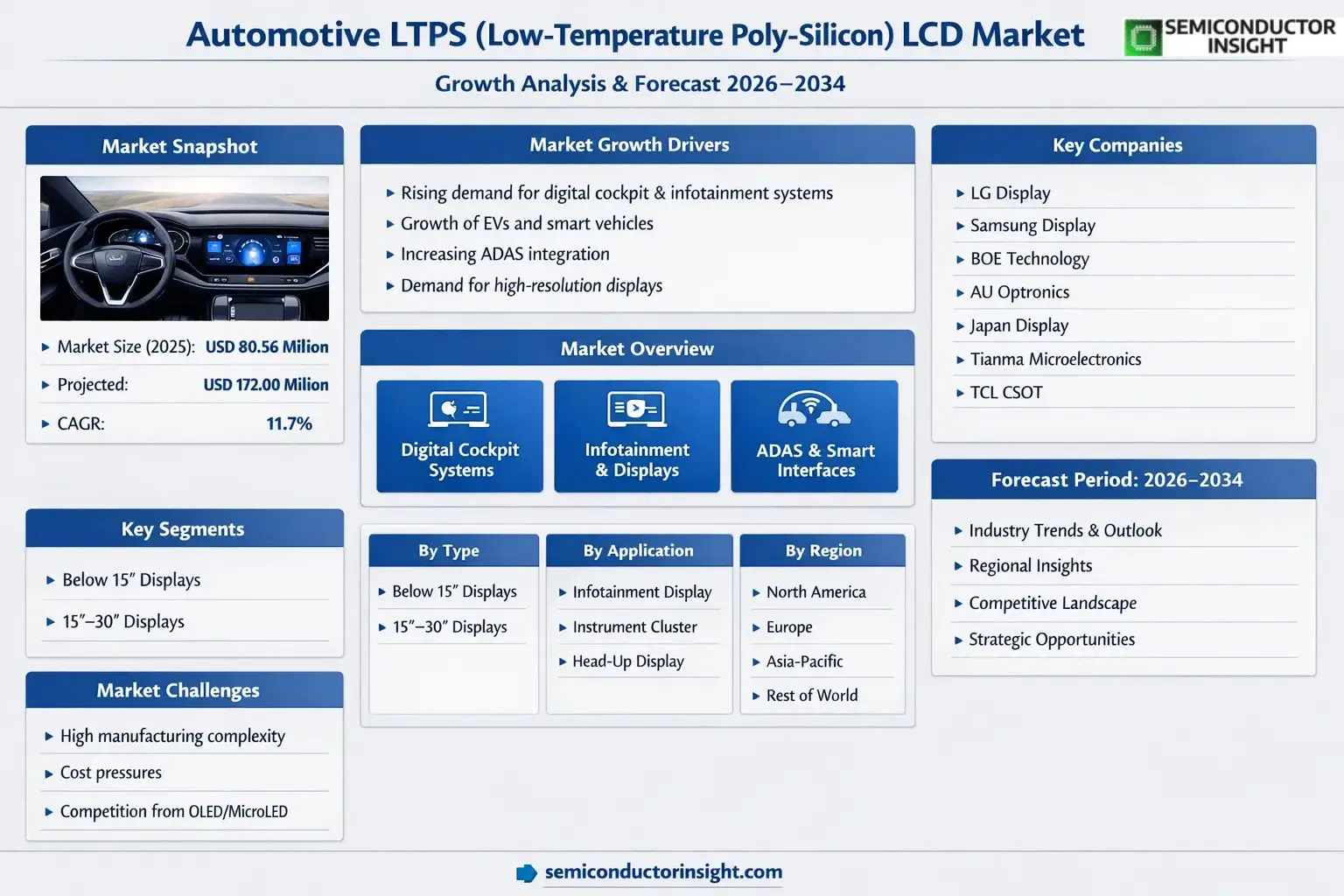

Global Automotive LTPS (Low-Temperature Poly-Silicon) LCD market size was valued at USD 80.56 million in 2025. The market is projected to grow from USD 89.98 million in 2026 to USD 172.00 million by 2034, exhibiting a CAGR of 11.7% during the forecast period.

LTPS (Low-Temperature Poly-Silicon) LCD is an advanced type of liquid crystal display technology that uses low-temperature processed polycrystalline silicon (poly-Si) as the active layer in the thin-film transistor (TFT) array. Unlike conventional amorphous silicon (a-Si) LCDs, LTPS technology enables higher electron mobility, which directly translates into superior display performance characteristics , including higher resolution, enhanced brightness, faster pixel response times, and lower power consumption. These attributes make it particularly well-suited for demanding automotive display environments, where reliability, clarity, and visual performance are critical requirements.

The market is gaining strong momentum driven by the rapid proliferation of in-vehicle infotainment systems, digital instrument clusters, and advanced driver-assistance system (ADAS) interfaces across both passenger and commercial vehicles. The growing consumer preference for premium in-cabin experiences, combined with automakers’ accelerating shift toward fully digitized cockpit architectures, continues to expand the addressable market for automotive-grade LTPS LCD panels. Key manufacturers operating in this space include LG, Samsung, BOE, AU Optronics, Japan Display, Tianma Microelectronics, and TCL CSOT, all of which maintain significant production capabilities and active development pipelines focused on automotive display solutions.

MARKET DRIVERS

Rising Demand for Advanced In-Vehicle Display Systems

Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market is experiencing robust momentum driven by the rapid evolution of in-vehicle infotainment and digital cockpit technologies. Automakers across the globe are increasingly integrating high-resolution, multi-display configurations into passenger vehicles, driven by consumer expectations for seamless connectivity and enhanced user experience. LTPS LCD panels, known for their superior pixel density, faster electron mobility, and lower power consumption compared to conventional amorphous silicon (a-Si) displays, are becoming the preferred choice for instrument clusters, center consoles, and head-up display systems in both premium and mid-segment vehicles.

Electrification and Smart Vehicle Trends Accelerating Adoption

Global transition toward electric vehicles (EVs) and hybrid electric vehicles (HEVs) is a significant driver for the Automotive LTPS LCD Market. EVs inherently require sophisticated digital interfaces to monitor battery status, range estimation, energy consumption, and charging data in real time. LTPS LCD technology, with its ability to support higher refresh rates and finer image clarity, is well-suited for these complex data visualization requirements. Leading EV manufacturers are incorporating large-format LTPS LCD panels as primary driver information displays and secondary touch screens, further reinforcing the technology’s relevance in next-generation automotive architectures.

➤ As automotive OEMs continue to prioritize digital transformation of the vehicle interior, LTPS LCD panels are emerging as a critical enabler of high-fidelity, energy-efficient display ecosystems across EV and connected vehicle platforms.

Regulatory mandates in key markets such as the European Union and North America requiring advanced driver assistance system (ADAS) interfaces, rearview camera displays, and real-time navigation systems are also amplifying demand. These requirements necessitate display solutions that can operate reliably across wide temperature ranges and deliver consistent visual performance,attributes inherent to LTPS LCD technology. The convergence of safety regulations and digital cockpit innovation continues to serve as a foundational growth catalyst for the automotive LTPS LCD segment.

MARKET CHALLENGES

High Manufacturing Complexity and Cost Pressures Limiting Broader Penetration

Despite its technological advantages, the Automotive LTPS LCD Market faces considerable challenges stemming from the inherent complexity of LTPS fabrication processes. The crystallization of amorphous silicon into poly-silicon using excimer laser annealing (ELA) requires precision equipment and controlled environments, resulting in significantly higher production costs compared to standard TFT-LCD or a-Si display manufacturing. These elevated costs create margin pressures for tier-1 automotive display suppliers and can hinder the adoption of LTPS LCD panels in cost-sensitive vehicle segments, particularly in emerging markets where price competitiveness is paramount.

Other Challenges

Competition from Alternative Display Technologies

The Automotive LTPS LCD Market faces intensifying competition from OLED and MicroLED display technologies, which offer superior contrast ratios, thinner form factors, and greater design flexibility. As OLED manufacturing costs gradually decline and automotive-grade OLED panels become more widely available, some OEMs are beginning to evaluate OLED as a viable alternative for premium display applications. This competitive dynamic poses a long-term challenge to LTPS LCD’s market share, particularly in the luxury vehicle segment where differentiated display aesthetics carry significant brand value.

Supply Chain Vulnerabilities and Component Shortages

Global supply chain disruptions, including semiconductor shortages and raw material constraints, have exposed vulnerabilities in the automotive display supply ecosystem. LTPS LCD panels depend on a specialized supply chain for backlight units, driver ICs, and polarizer films, many of which are concentrated in a limited number of geographies. Disruptions in any of these upstream components can create production bottlenecks, extended lead times, and increased procurement costs,all of which challenge automotive display manufacturers seeking to scale LTPS LCD supply in alignment with OEM build schedules.

MARKET RESTRAINTS

Stringent Automotive Qualification Standards Extending Time-to-Market

One of the primary restraints affecting Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market is the rigorous qualification and validation process required before display components can be deployed in production vehicles. Automotive-grade display panels must meet demanding standards such as AEC-Q100 for integrated circuits, ISO 16750 for environmental conditions, and OEM-specific reliability benchmarks covering thermal cycling, vibration resistance, and long-term luminance stability. These qualification cycles can span multiple years and require substantial investment in testing and certification, thereby extending time-to-market and creating barriers to entry for newer or smaller display manufacturers seeking to participate in the automotive LTPS LCD supply chain.

Limited Scalability in Entry-Level Vehicle Segments

While LTPS LCD technology has achieved strong penetration in premium and upper-mid-range vehicles, its scalability into entry-level and economy car segments remains constrained by cost considerations. Automotive OEMs targeting price-sensitive consumers in developing markets such as Southeast Asia, Latin America, and Sub-Saharan Africa continue to favor lower-cost a-Si TFT-LCD solutions for basic instrument cluster and infotainment applications. The inability of LTPS LCD panels to compete on a cost-per-unit basis in these segments limits the addressable market for the technology and restrains overall volume growth in global unit terms. Unless production economies of scale improve substantially, this cost disparity is expected to persist as a structural restraint throughout the forecast period.

MARKET OPPORTUNITIES

Expansion of Digital Cockpit Architecture in Mid-Segment Vehicles

A compelling growth opportunity for the Automotive LTPS LCD Market lies in the accelerating adoption of fully digital cockpit architectures across mid-segment vehicle platforms. As display technology costs gradually normalize and consumer demand for connected, feature-rich interiors extends beyond premium vehicles, automotive OEMs are increasingly incorporating multi-screen LTPS LCD configurations into mainstream models. This democratization of advanced display technology opens a substantially larger addressable market for LTPS panel suppliers and creates volume-driven opportunities to improve manufacturing efficiencies and reduce per-unit costs over time.

Growing Autonomous and Semi-Autonomous Vehicle Development

The progressive development of Level 2 and Level 3 autonomous driving systems presents a significant opportunity for Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market. Autonomous and semi-autonomous vehicles require expanded display real estate to communicate vehicle status, sensor data, navigation guidance, and safety alerts to passengers and drivers. LTPS LCD panels, with their high resolution, wide viewing angles, and compatibility with touch and haptic feedback technologies, are well-positioned to serve these advanced human-machine interface (HMI) requirements. As autonomous vehicle programs mature and transition toward commercialization, demand for high-performance LTPS LCD solutions across passenger, commercial, and shared mobility platforms is expected to expand meaningfully.

Strategic Partnerships and Localized Manufacturing Investments

Opportunities also exist for display manufacturers to leverage strategic partnerships with automotive OEMs and tier-1 suppliers to co-develop customized LTPS LCD display modules tailored to specific vehicle platform requirements. Additionally, government-backed initiatives to localize automotive component manufacturing in regions such as India, Mexico, and Eastern Europe are creating favorable conditions for regional LTPS LCD production investments. Establishing localized supply capabilities would reduce logistics costs, shorten delivery lead times, and improve supply chain resilience,factors that are increasingly prioritized by automotive procurement teams seeking to de-risk their display component sourcing strategies in a post-disruption global manufacturing environment.

MAIN TITLE HERE () Trends

Rising Demand for High-Resolution In-Vehicle Displays Accelerates Automotive LTPS LCD Adoption

Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market is witnessing a significant transformation driven by the rapid integration of advanced display technologies in modern vehicles. As automakers increasingly prioritize digital cockpit experiences, LTPS LCD panels have emerged as a preferred solution owing to their superior resolution, enhanced brightness levels, and faster pixel response times compared to conventional amorphous silicon LCD alternatives. The growing consumer expectation for premium in-cabin infotainment systems, digital instrument clusters, and heads-up display interfaces is directly fueling adoption of LTPS-based panels across both passenger and commercial vehicle segments. Key manufacturers including LG, Samsung, BOE, AU Optronics, Japan Display, Tianma Microelectronics, and TCL CSOT are actively scaling production capabilities to meet rising automotive-grade display requirements.

Other Trends

Expansion of Larger Display Formats in Automotive Interiors

A notable trend shaping Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market is the growing preference for larger display formats, particularly in the 15″ to 30″ segment. Automakers are increasingly incorporating wide-format center console displays and panoramic digital dashboards, pushing demand for high-performance LTPS panels capable of delivering consistent image quality across expanded screen real estate. This shift is especially prominent in electric vehicles and premium car segments where sophisticated human-machine interface design has become a critical differentiator.

Technological Advancement in Polycrystalline Silicon Processing

Continuous innovation in low-temperature polycrystalline silicon processing techniques is enabling display manufacturers to produce thinner, lighter, and more energy-efficient panels suited for automotive environments. Improvements in excimer laser annealing and oxide semiconductor integration are allowing LTPS LCD displays to achieve higher electron mobility, translating to sharper visuals and reduced power consumption , both critical parameters for next-generation vehicle architectures, including those supporting autonomous driving systems.

Regional Manufacturing Dynamics and Supply Chain Developments

Asia remains the dominant production hub for Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market, with China, Japan, and South Korea hosting the majority of display panel manufacturing infrastructure. Chinese manufacturers such as BOE and TCL CSOT are aggressively investing in capacity expansion and process upgrades to strengthen their competitive positioning. Meanwhile, North America and Europe continue to drive demand through robust automotive OEM activity, with suppliers aligning supply chains to meet stringent automotive qualification standards including AEC-Q reliability requirements.

Integration with Smart Cockpit and ADAS Platforms Defining Future Market Direction

The convergence of Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market with smart cockpit ecosystems and advanced driver assistance systems represents a defining long-term trend. Display panels are no longer standalone components but integral elements of connected vehicle platforms that interface with navigation, safety monitoring, and driver behavior analytics systems. As software-defined vehicle architectures gain traction globally, demand for high-fidelity, reliable, and thermally stable LTPS LCD displays is expected to remain on a sustained upward trajectory across all major automotive markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive LTPS LCD Market: Competitive Dynamics, Strategic Positioning, and Leading Manufacturer Profiles

Global Automotive LTPS (Low-Temperature Poly-Silicon) LCD market is characterized by a concentrated yet intensely competitive landscape, dominated by a handful of vertically integrated display manufacturers with deep expertise in advanced thin-film transistor technologies. Leading the competitive hierarchy are major Asian conglomerates , most notably Samsung Display, LG Display, BOE Technology Group, and Japan Display Inc. , which collectively command a substantial share of global automotive-grade LTPS panel supply. These players benefit from massive capital investments in Gen 6 and Gen 8 LTPS fabrication lines, long-standing OEM partnerships with tier-1 automotive suppliers, and proprietary process innovations that enable higher pixel density, superior luminance uniformity, and extended operating temperature ranges required for in-vehicle display applications. As the market advances from a valuation of USD 80.56 million in 2025 toward a projected USD 172 million by 2034, at a CAGR of 11.7%, dominant players are aggressively expanding their automotive display portfolios to capture demand from instrument clusters, center-stack infotainment panels, and heads-up display modules across both passenger and commercial vehicle segments.

Beyond the top-tier incumbents, a growing cohort of specialized and emerging manufacturers is carving out meaningful niches within the automotive LTPS LCD ecosystem. AU Optronics (AUO) and Tianma Microelectronics have established credible automotive-qualified production capabilities, targeting mid-range vehicle platforms with cost-competitive LTPS solutions that meet AEC-Q100 reliability benchmarks. TCL CSOT, leveraging the backing of TCL Technology Group, is rapidly scaling its automotive-grade display capacity and has secured design wins with several Chinese and European automakers. Meanwhile, regional players and joint ventures across South Korea, Japan, China, and Taiwan are investing in next-generation LTPS process nodes to differentiate through ultra-narrow bezels, curved form factors, and integrated touch functionality. Competitive intensity is further amplified by ongoing consolidation activity, cross-licensing agreements, and the strategic pivot of some OLED-focused manufacturers into high-brightness LTPS LCD variants as a bridge technology for automotive interiors demanding cost efficiency without sacrificing display performance.

List of Key Automotive LTPS (Low-Temperature Poly-Silicon) LCD Companies Profiled

- LG Display Co., Ltd.

- Samsung Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp. (AUO)

- Japan Display Inc. (JDI)

- Tianma Microelectronics Co., Ltd.

- TCL CSOT (China Star Optoelectronics Technology)

- Sharp Corporation (a Foxconn Company)

- Innolux Corporation

- Kyocera Display Corporation

- Truly Semiconductors Ltd.

- Visionox Technology Co., Ltd.

- Raystar Optronics Inc.

- Shenzhen China Star Optoelectronics Technology Co., Ltd.

- Panasonic Liquid Crystal Display Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

15″–30″ Displays represent the leading and fastest-growing size segment in the Automotive LTPS LCD market, driven by the widespread adoption of large-format infotainment and cockpit display systems in modern vehicles.

|

| By Application |

|

Infotainment Display remains the dominant application segment for Automotive LTPS LCD, serving as the central hub for connectivity, navigation, media, and vehicle control in both new and existing vehicle models.

|

| By End User |

|

Passenger Vehicle segment leads the Automotive LTPS LCD end-user landscape, owing to the high volume of passenger car production globally and the intensive focus on cabin digitalization among personal vehicle manufacturers.

|

| By Technology Integration |

|

LTPS LCD with In-Cell/On-Cell Touch Integration is emerging as the leading technology integration segment, as automotive display manufacturers focus on delivering thinner, lighter, and more optically efficient display modules for next-generation vehicle cockpits.

|

| By Vehicle Electrification Level |

|

Battery Electric Vehicles (BEV) represent the most dynamic and high-growth segment within the vehicle electrification landscape for Automotive LTPS LCD adoption, as EV manufacturers prioritize digital-first, screen-centric cabin designs as a core brand identity element.

|

Regional Analysis: Automotive LTPS LCD Market

Asia-Pacific

The region’s mature display manufacturing infrastructure supports complex LTPS LCD production with high yield rates. Integrated supply chains from raw materials to finished panels enable cost-effective production. Technology transfer between consumer electronics and automotive applications accelerates innovation cycles. Established quality control processes ensure reliability standards required for automotive applications. Collaborative research between academic institutions and industry partners drives continuous technical improvements.

Strong demand from premium vehicle segments fuels LTPS LCD adoption across passenger and commercial vehicles. Increasing consumer expectations for advanced digital cockpits drive higher display specifications. Regional automakers prioritize local display suppliers for supply chain security and cost advantages. Government policies promoting electric vehicles create additional opportunities for advanced display integration. Competition between display manufacturers leads to rapid technological advancement and price optimization.

The region leads in developing thinner, brighter, and more energy-efficient LTPS LCD designs. Advanced manufacturing techniques enable higher pixel density and better sunlight readability. Integration with touch and haptic feedback technologies enhances user experience. Development of flexible and curved LTPS LCD configurations addresses evolving automotive interior designs. Collaboration with automotive OEMs ensures displays meet stringent reliability and longevity requirements.

Proximity to semiconductor fabrication facilities reduces component costs and lead times. Established logistics networks support just-in-time delivery to automotive assembly plants. Vertical integration among display manufacturers provides control over critical production processes. Access to specialized materials and processing equipment enhances production capabilities. Strong technical support infrastructure facilitates rapid problem-solving and continuous improvement initiatives.

North America

North America demonstrates strong adoption of Automotive LTPS LCD technology in premium vehicle segments. The region’s automotive manufacturers prioritize advanced display systems for luxury and electric vehicles. Stringent safety regulations drive demand for high-visibility, reliable display solutions. Collaboration between technology companies and automotive OEMs fosters innovation in user interface design. The market benefits from high consumer purchasing power and willingness to pay for advanced vehicle technologies.

Europe

Europe maintains significant presence in Automotive LTPS LCD market through premium automotive brands and stringent quality requirements. The region’s focus on driver assistance systems and digital cockpits creates sustained demand for high-performance displays. European automakers emphasize aesthetic integration and functional excellence in display design. Environmental regulations push development of energy-efficient display technologies. Strong supplier relationships ensure reliable technology adoption across vehicle platforms.

South America

South America shows growing interest in Automotive LTPS LCD technology, particularly in premium vehicle imports and local luxury segments. Economic factors influence adoption rates, with focus on cost-effective display solutions. The market demonstrates potential for growth as vehicle electrification trends gain momentum. Regional manufacturing capabilities are developing to support local automotive production requirements. Consumer preferences increasingly favor advanced digital interfaces in vehicles.

Middle East & Africa

Middle East & Africa exhibit selective adoption of Automotive LTPS LCD technology primarily in luxury vehicle segments. The region’s high-temperature environments present unique challenges for display performance and reliability. Market development follows premium vehicle sales patterns and economic conditions. Growing infrastructure development supports increased technology adoption. Regional preferences for vehicle customization drive demand for advanced display options.

Report Scope

This market research report provides a comprehensive analysis of the Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market?

-> Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market was valued at USD 80.56 million in 2025 and is expected to reach USD 172 million by 2034.

Which key companies operate in Automotive LTPS (Low-Temperature Poly-Silicon) LCD Market?

-> Key players include LG, Samsung, BOE, AU Optronics, Japan Display, Tianma Microelectronics, TCL CSOT, among others.

What are the key growth drivers?

-> Key growth drivers include demand for higher resolution, better brightness, faster response times in automotive displays, and advancements over traditional a-Si LCD technology.

Which region dominates the market?

-> Asia is the fastest-growing region with significant contributions from China, Japan, and South Korea, while North America including the U.S. remains a key market.

What are the emerging trends?

-> Emerging trends include adoption in passenger and commercial vehicles, shifts toward LTPS for improved performance in infotainment and instrument clusters, and focus on segments such as <15″, 15″-30″, and others.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...