MARKET INSIGHTS

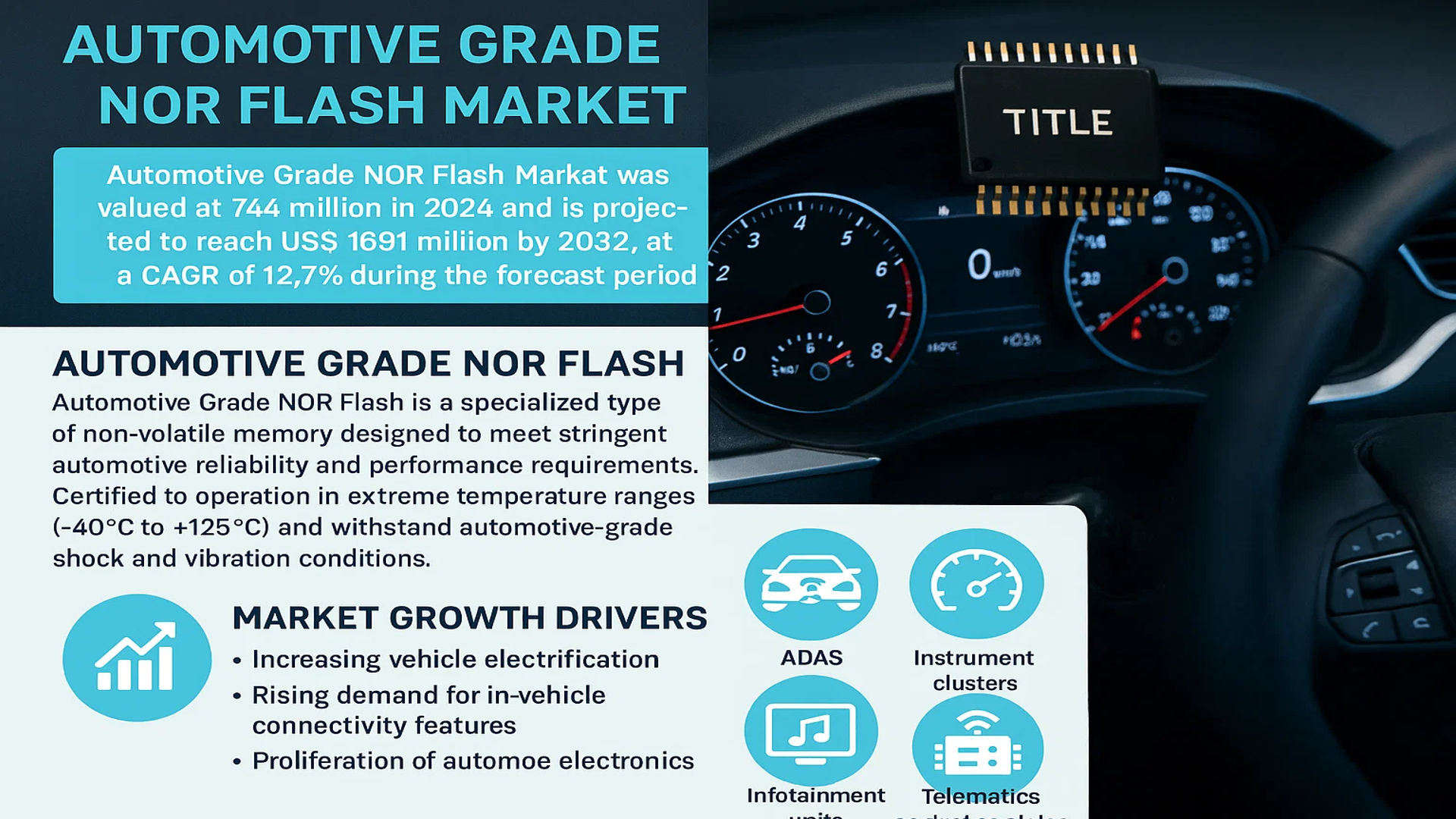

The global Automotive Grade NOR Flash Market was valued at 744 million in 2024 and is projected to reach US$ 1691 million by 2032, at a CAGR of 12.7% during the forecast period.

Automotive Grade NOR Flash refers to a specialized type of non-volatile memory designed to meet stringent automotive reliability and performance requirements. These components are certified to operate in extreme temperature ranges (-40°C to +125°C) and withstand automotive-grade shock and vibration conditions. The technology is primarily used for storing critical firmware in advanced driver assistance systems (ADAS), instrument clusters, infotainment units, and telematics control modules.

The market growth is being driven by increasing vehicle electrification, rising demand for in-vehicle connectivity features, and the proliferation of automotive electronics. The 3.3V segment currently dominates the market due to its compatibility with legacy automotive systems, while the 1.8V segment is gaining traction for power-sensitive applications. Key players like Micron, Infineon Technologies, and Winbond are expanding their production capacity to meet the growing demand from automakers transitioning to software-defined vehicle architectures.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Adoption of Advanced Driver Assistance Systems (ADAS) to Accelerate Market Expansion

The automotive industry is witnessing a rapid shift toward autonomous and semi-autonomous vehicles, which is driving demand for Automotive Grade NOR Flash memory. Advanced driver assistance systems (ADAS) rely heavily on high-reliability storage solutions for real-time data processing, sensor fusion, and firmware execution. The global ADAS market is projected to grow significantly due to regulatory mandates for vehicle safety and consumer demand for enhanced driving experiences. These systems require NOR Flash to store critical boot code and firmware in extreme temperature conditions, ensuring instantaneous access to data during vehicle operation, unlike NAND alternatives that suffer from slower read speeds.

Proliferation of Electric Vehicles (EVs) and Connected Car Technologies to Fuel Market Growth

The surge in electric vehicle production directly impacts the demand for Automotive Grade NOR Flash, as EVs depend on sophisticated electronic control units (ECUs) that require fail-safe memory solutions. EV sales have been increasing at a remarkable rate, supported by government incentives and advancements in battery technology. Additionally, connected car ecosystems—encompassing 5G-enabled telematics, over-the-air (OTA) updates, and infotainment systems—are expanding rapidly. These applications demand NOR Flash for its reliability in storing configuration data and executing code directly from memory, particularly in safety-critical environments where data integrity is non-negotiable.

Furthermore, stringent automotive safety standards such as ISO 26262 and AEC-Q100 compliance have become critical purchasing criteria for automakers. NOR Flash manufacturers are responding by developing products with extended temperature ranges (-40°C to +125°C) and enhanced endurance cycles, further solidifying the technology’s role in next-generation automotive architectures.

MARKET RESTRAINTS

High Cost Structure and Extended Qualification Cycles to Limit Market Penetration

While Automotive Grade NOR Flash offers superior reliability compared to industrial-grade alternatives, its adoption is constrained by significantly higher costs. The rigorous qualification processes required for automotive components—including prolonged testing under extreme environmental conditions—drive up production expenses. Automotive memory solutions can cost 2-3 times more than their consumer-grade counterparts, creating pricing pressures for OEMs trying to balance performance with budget constraints. This challenge is particularly acute in emerging markets where price sensitivity remains a dominant factor in purchasing decisions.

Supply Chain Constraints and Geopolitical Factors

The semiconductor industry continues to face supply-demand imbalances, with automotive-grade components experiencing longer lead times than other sectors. Geopolitical tensions affecting semiconductor trade flows have exacerbated these challenges, creating uncertainty in component availability. Automakers are forced to maintain larger safety stocks or engage in long-term contracts with suppliers, increasing inventory carrying costs and reducing flexibility in responding to market fluctuations.

MARKET CHALLENGES

Technical Limitations in Density Scaling to Impede Next-Generation Applications

NOR Flash technology faces inherent limitations in achieving the higher density requirements of modern automotive systems without compromising reliability. While 3.3V NOR Flash currently dominates applications requiring 256Mb capacities or below, the industry struggles to scale beyond 1Gb densities with the same cost-effectiveness as NAND solutions. This creates architectural challenges for automakers developing systems with increasing data storage needs, such as autonomous driving platforms requiring extensive neural network parameters. The technology’s cell structure makes high-density integration more complex compared to NAND alternatives.

Competition from Emerging Non-Volatile Memory Technologies

Emerging memory technologies like MRAM (Magnetoresistive RAM) and ReRAM (Resistive RAM) are gaining traction as potential alternatives to NOR Flash in certain automotive applications. These technologies offer near-infinite endurance and faster write speeds, making them attractive for frequent data logging applications. While currently more expensive than NOR Flash, continued R&D investments could make them viable competitors in mission-critical automotive applications within the next decade.

MARKET OPPORTUNITIES

Development of Autonomous Vehicle Architectures to Create New Growth Vectors

The progression toward higher levels of vehicle autonomy (L3-L5) presents substantial opportunities for Automotive Grade NOR Flash providers. Autonomous driving systems require multiple layers of redundancy in their memory subsystems, with NOR Flash being ideal for storing safety-critical boot code and real-time operating systems. As automakers implement heterogeneous computing architectures combining MCUs, GPUs and AI accelerators, the demand for reliable, instant-on memory solutions will grow exponentially across sensor fusion hubs, domain controllers and fail-operational systems.

Emerging Markets and Localization Strategies to Open New Revenue Streams

Growth in automotive production within emerging economies—particularly in Southeast Asia and Latin America—is creating opportunities for memory suppliers to establish localized support networks. Regional automakers are increasingly adopting international safety standards while seeking cost-optimized solutions, prompting NOR Flash manufacturers to develop tailored product portfolios. Partnerships with regional tier-1 suppliers and investments in local testing facilities are becoming strategic imperatives to capture this growth while navigating trade policy complexities.

➤ Industry consolidation is accelerating as major players acquire specialized IP and manufacturing capabilities to address the automotive sector’s unique requirements.

AUTOMOTIVE GRADE NOR FLASH MARKET TRENDS

Advanced Vehicle Electronics Driving Demand for High-Performance NOR Flash

The automotive industry’s rapid shift toward electrification, connectivity, and autonomous driving is significantly boosting the demand for Automotive Grade NOR Flash. This non-volatile memory solution is critical for storing firmware and real-time execution code in modern vehicle systems, including advanced driver-assistance systems (ADAS), infotainment, and telematics. With over 90% of new vehicles now incorporating some form of digital display and connectivity feature, the need for reliable, high-speed memory that can withstand harsh automotive conditions has never been greater. Furthermore, the introduction of vehicle-to-everything (V2X) communication standards in smart cities is pushing memory requirements even higher, with an estimated 30% year-on-year growth in NOR Flash adoption for automotive edge computing applications.

Other Trends

Safety and Functional Reliability Standards

Stringent automotive safety certifications like AEC-Q100 are reshaping the NOR Flash market landscape, with manufacturers investing heavily in radiation-hardened designs and extended temperature-range products. Compliance with ISO 26262 functional safety standards for ASIL-rated applications has become a key differentiator, particularly for memory solutions deployed in autonomous vehicle systems. Leading suppliers now offer -40°C to +125°C operational range memories with built-in error correction code (ECC) to meet these requirements, with the safety-critical segment expected to account for nearly 45% of total Automotive NOR Flash revenue by 2026.

Integration Challenges in Next-Generation Vehicle Architectures

The transition to zone-based E/E architectures and domain controllers presents both opportunities and challenges for Automotive NOR Flash adoption. While these new architectures require higher-density memory solutions (typically 256Mb to 1Gb) for centralized computing modules, they also demand lower power consumption and faster read performance. Manufacturers are responding with innovative serial peripheral interface (SPI) NOR Flash solutions offering 400MHz clock speeds and deep power-down modes below 1μA. The industry is witnessing a notable shift from parallel to serial interfaces, with SPI NOR expected to capture over 75% of the automotive memory market by 2030, particularly in cost-sensitive electric vehicle applications where space and power efficiency are paramount.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Memory Leaders Invest in Reliability and Innovation to Secure Market Position

The global Automotive Grade NOR Flash market exhibits a moderately consolidated structure, dominated by semiconductor giants while also featuring specialized memory manufacturers. Infineon Technologies and Micron Technology collectively held approximately 38% market share in 2024, owing to their extensive automotive-qualified memory portfolios and entrenched relationships with Tier-1 automotive suppliers.

The competitive intensity has increased with the growing demand for reliable code storage solutions in advanced driver-assistance systems (ADAS) and vehicle electrification. Macronix has emerged as a strong contender, particularly in the Asian market, by focusing on high-temperature resistant NOR Flash solutions that meet AEC-Q100 Grade 1 specifications.

Market players are aggressively expanding their product lines to address evolving automotive requirements. Winbond recently introduced a new series of 1.8V automotive NOR Flash devices with enhanced security features for vehicle-to-everything (V2X) applications, while Microchip Technology strengthened its position through strategic partnerships with European automakers.

Innovation remains crucial as the industry transitions toward autonomous driving capabilities. Companies like GigaDevice are investing heavily in reliability testing and qualification processes, recognizing that automotive applications demand exceptional endurance and data retention compared to consumer-grade memory products.

List of Key Automotive Grade NOR Flash Manufacturers

- Infineon Technologies AG (Germany)

- Macronix International Co., Ltd. (Taiwan)

- Micron Technology, Inc. (U.S.)

- Winbond Electronics Corporation (Taiwan)

- GigaDevice Semiconductor Inc. (China)

- Ingenic Semiconductor (China)

- Microchip Technology Inc. (U.S.)

Segment Analysis:

By Type

3.3V Segment Leads the Market Due to High Compatibility with Automotive Electronics

The market is segmented based on type into:

- 3.3V

- 1.8V

- Others

By Application

Passenger Cars Segment Dominates with Widespread Adoption in Infotainment and ADAS Systems

The market is segmented based on application into:

- Passenger Cars

- Commercial Cars

By Memory Density

High-Density Solutions Gain Traction for Advanced Automotive Applications

The market is segmented based on memory density into:

- Low Density (≤ 256Mb)

- Medium Density (257Mb – 1Gb)

- High Density (> 1Gb)

By End Use

OEM Integration Drives Market Growth for Automotive Grade NOR Flash

The market is segmented based on end use into:

- OEM (Original Equipment Manufacturer)

- Aftermarket

Regional Analysis: Automotive Grade NOR Flash Market

Asia-Pacific

Dominating the global market with over 40% revenue share in 2024, Asia-Pacific is the largest consumer of Automotive Grade NOR Flash, primarily driven by China’s booming automotive sector and semiconductor manufacturing capabilities. The region benefits from strong government support for electric vehicle adoption and increasing investments in autonomous driving technologies. Japan and South Korea remain key hubs for automotive semiconductor innovation, with major OEMs integrating advanced NOR Flash solutions into next-generation vehicles. While cost-sensitive markets still favor conventional memory solutions, tier-1 suppliers are gradually shifting toward higher-density Automotive Grade NOR Flash to support advanced driver-assistance systems (ADAS) and connected car features.

North America

The North American market, led by the U.S., is characterized by stringent automotive safety standards and rapid adoption of vehicular connectivity solutions. Automotive Grade NOR Flash demand is growing at a CAGR of 13.2% (2024-2032) as domestic automakers incorporate more sophisticated infotainment and telematics systems. The region’s strong R&D ecosystem, with major players like Micron and Microchip Technology headquartered here, drives innovation in high-temperature resistant memory solutions. However, supply chain disruptions and trade restrictions continue to pose challenges for regional manufacturers attempting to secure stable semiconductor supplies.

Europe

European automakers are accelerating their transition toward electric vehicles, creating sustained demand for reliable Automotive Grade NOR Flash in battery management systems and safety-critical applications. Germany remains the technology hub, with Infineon Technologies leading development of AEC-Q100 compliant memory solutions. The region’s emphasis on functional safety (ISO 26262) and data security in connected cars favors high-reliability NOR Flash adoption. However, increasing competition from Asian suppliers and the complexity of automotive supply chains are testing European manufacturers’ ability to maintain competitive pricing while meeting stringent quality requirements.

South America

While representing a smaller portion of the global market, the South American Automotive Grade NOR Flash sector shows promising growth potential, particularly in Brazil’s emerging electric vehicle sector. The region faces infrastructure challenges in semiconductor distribution networks and relies heavily on imports. Domestic automotive production focuses mainly on entry-level vehicles, limiting demand for premium memory solutions. However, increasing foreign investments in local auto manufacturing and gradual modernization of vehicle fleets are expected to drive moderate market growth through 2032.

Middle East & Africa

This region presents a developing market for Automotive Grade NOR Flash, with growth concentrated in Gulf Cooperation Council (GCC) countries adopting advanced vehicle technologies. UAE and Saudi Arabia are leading the charge in smart mobility initiatives that require robust memory solutions. The African continent shows limited current demand due to predominance of used vehicle imports, but increasing local assembly operations suggest long-term growth potential. Market expansion faces hurdles including limited technical expertise in automotive electronics and preference for lower-cost aftermarket solutions among regional consumers.

Report Scope

This market research report provides a comprehensive analysis of the global Automotive Grade NOR Flash market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Automotive Grade NOR Flash market was valued at USD 744 million in 2024 and is projected to reach USD 1,691 million by 2032, growing at a CAGR of 12.7%.

- Segmentation Analysis: Detailed breakdown by product type (3.3V, 1.8V, Others), application (Passenger Cars, Commercial Cars), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants including Infineon Technologies, Macronix, Micron, Winbond, GigaDevice, Ingenic Semiconductor, and Microchip Technology, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in NOR Flash memory, integration with automotive systems, and evolving industry standards for reliability and performance.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing automotive electronics content and electrification, along with challenges like supply chain constraints and stringent automotive certification requirements.

- Stakeholder Analysis: Insights for semiconductor manufacturers, automotive OEMs, tier-1 suppliers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Grade NOR Flash Market?

-> Automotive Grade NOR Flash Market was valued at 744 million in 2024 and is projected to reach US$ 1691 million by 2032, at a CAGR of 12.7% during the forecast period.

Which key companies operate in Global Automotive Grade NOR Flash Market?

-> Key players include Infineon Technologies, Macronix, Micron, Winbond, GigaDevice, Ingenic Semiconductor, and Microchip Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing automotive electronics content, vehicle electrification trends, and demand for reliable memory solutions in advanced driver assistance systems (ADAS) and infotainment systems.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by automotive production in China and Japan, while North America remains a significant market due to advanced vehicle technologies.

What are the emerging trends?

-> Emerging trends include higher density NOR Flash solutions, integration with automotive microcontrollers, and development of memory solutions for autonomous vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...