Automotive Grade Flash Memory Market Insights

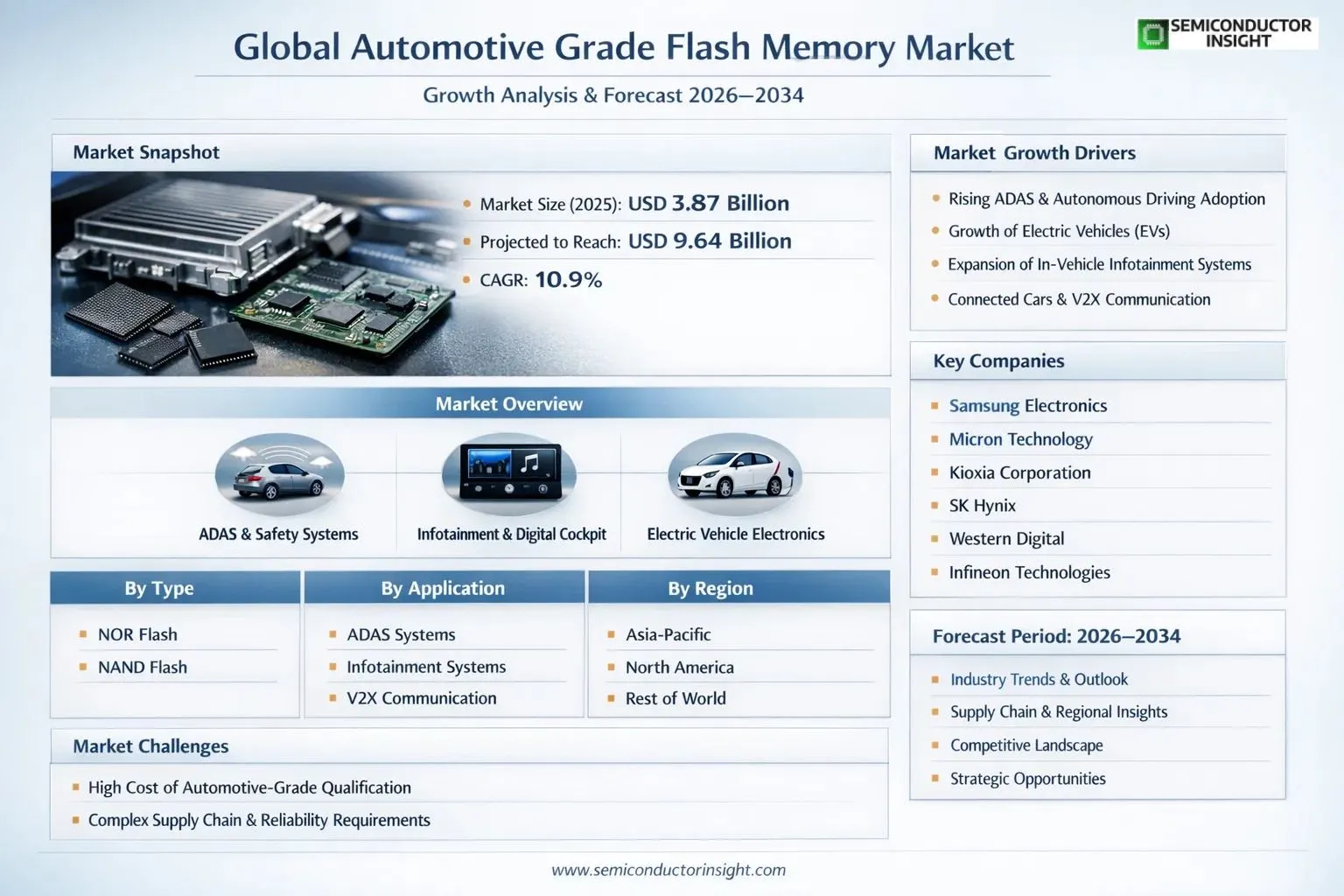

Global Automotive Grade Flash Memory market size was valued at USD 3.87 billion in 2025. The market is projected to grow from USD 4.21 billion in 2026 to USD 9.64 billion by 2034, exhibiting a CAGR of 10.9% during the forecast period.

Automotive Grade Flash Memory refers to flash memory solutions specifically designed and manufactured to meet the stringent requirements of the automotive industry. These memory products are built to withstand the harsh environmental conditions and unique operational demands encountered in automotive applications, including extreme temperature ranges typically from -40°C to +125°C, high vibration, electromagnetic interference, and long operational lifespans. The primary product types encompass NOR Flash and NAND Flash, each serving distinct functions across advanced driver-assistance systems (ADAS), instrument clusters, infotainment systems, and vehicle-to-everything (V2X) communication modules.

The market is experiencing robust growth driven by accelerating vehicle electrification, the rapid proliferation of ADAS features, and the increasing software-defined vehicle architecture adopted by global automakers. Furthermore, the surging demand for in-vehicle infotainment and connected car technologies is compelling automakers and Tier-1 suppliers to integrate higher-capacity, high-reliability flash memory solutions across vehicle platforms. Key manufacturers operating in this market with broad product portfolios include Samsung, Micron, Kioxia, SK Hynix, Western Digital, Infineon Technologies, Macronix, Winbond, GigaDevice, Ingenic Semiconductor, and Microchip Technology.

MARKET DRIVERS

Rising Adoption of Advanced Driver Assistance Systems (ADAS) and In-Vehicle Infotainment

The automotive grade flash memory market is experiencing robust growth, primarily driven by the accelerating integration of Advanced Driver Assistance Systems (ADAS) and sophisticated in-vehicle infotainment (IVI) platforms across modern vehicle architectures. As automakers transition toward software-defined vehicles, the demand for high-density, high-reliability non-volatile memory solutions has intensified considerably. Automotive-grade flash memory, engineered to withstand extreme temperature ranges, vibration, and electromagnetic interference, has become indispensable in storing critical firmware, maps, sensor calibration data, and multimedia content. The proliferation of connected vehicle technologies is further amplifying this demand, compelling Tier 1 suppliers and OEMs to source memory components that comply with stringent automotive qualification standards such as AEC-Q100.

Electrification of Vehicles and Growth of Electric Vehicle Platforms

Global shift toward vehicle electrification represents one of the most significant structural drivers for the automotive grade flash memory market. Electric vehicles (EVs) rely heavily on sophisticated battery management systems (BMS), powertrain control units, and over-the-air (OTA) update capabilities , each of which demands reliable, high-endurance flash memory components. As EV adoption accelerates across North America, Europe, and Asia-Pacific, automakers are designing platforms that require greater volumes of embedded flash and managed NAND solutions. The increasing complexity of EV software stacks, often comprising tens of millions of lines of code, necessitates high-capacity automotive-grade NOR and NAND flash memory to store and execute these systems efficiently.

➤ The convergence of electrification, connectivity, and autonomous driving is fundamentally reshaping memory architecture requirements within the automotive ecosystem, positioning automotive grade flash memory as a mission-critical enabling technology for next-generation mobility platforms.

Furthermore, the rapid advancement of autonomous driving technologies across SAE Levels 2 through 4 is generating substantial incremental demand for automotive-grade flash memory. Autonomous systems depend on real-time processing of vast sensor data from LiDAR, radar, and camera arrays, requiring flash memory solutions with low latency, high read/write endurance, and functional safety compliance aligned with ISO 26262 standards. This trend is expected to sustain long-term demand momentum across the automotive grade flash memory market throughout the forecast period.

MARKET CHALLENGES

Stringent Automotive Qualification Standards and Extended Product Lifecycle Requirements

One of the most pronounced challenges confronting participants in the automotive grade flash memory market is the complexity and cost associated with meeting rigorous automotive qualification standards. Unlike consumer-grade memory components, automotive-grade flash must satisfy AEC-Q100 stress test qualifications, JEDEC standards, and ISO 26262 functional safety requirements , processes that involve extensive validation cycles spanning multiple years. Memory manufacturers must invest substantially in testing infrastructure, process development, and reliability engineering, which significantly elevates the time-to-market and overall cost structure. Additionally, the automotive industry’s expectation of 10 to 15-year product lifecycle support creates ongoing supply chain commitments that are difficult to reconcile with the rapid cadence of semiconductor process node migrations.

Other Challenges

Supply Chain Complexity and Geopolitical Risks

The automotive grade flash memory market is exposed to considerable supply chain vulnerabilities, exacerbated by the geographic concentration of advanced semiconductor manufacturing capacity in East Asia. Geopolitical tensions, trade policy uncertainties, and periodic capacity constraints at leading foundries have underscored the fragility of automotive memory supply chains. OEMs and Tier 1 suppliers have faced procurement disruptions that highlighted the risks of single-source dependencies and the challenge of qualifying alternative suppliers within the compressed timelines demanded by vehicle production schedules.

Thermal and Reliability Constraints in Harsh Operating Environments

Automotive applications subject flash memory components to extreme operational stressors, including wide temperature fluctuations typically ranging from -40°C to +150°C, mechanical vibration, and humidity exposure. Ensuring consistent data integrity, endurance, and retention under these conditions requires specialized memory cell designs and advanced error correction algorithms, adding engineering complexity and cost. As vehicles incorporate more electronic control units (ECUs) in thermally challenging locations such as engine compartments and brake systems, the reliability demands placed on automotive grade flash memory continue to intensify.

MARKET RESTRAINTS

High Cost Premiums Associated with Automotive-Grade Memory Qualification

A significant restraint on the automotive grade flash memory market is the substantial cost premium that automotive-qualified components command relative to their industrial or commercial counterparts. The extensive qualification processes, extended reliability testing, and long-term supply commitments inherent to automotive-grade components translate into higher bill-of-materials costs for vehicle manufacturers. In an industry environment where automakers are simultaneously managing cost pressures from electrification investments and intensifying competition, procurement teams face challenges justifying the price differentials associated with fully automotive-qualified flash memory, particularly in cost-sensitive vehicle segments. This dynamic can slow adoption rates among smaller OEMs and emerging EV manufacturers operating under tight capital constraints.

Technological Transition Risks Associated with NAND Flash Scaling

The ongoing transition to advanced 3D NAND flash memory architectures presents both opportunity and restraint within the automotive grade flash memory market. While 3D NAND offers superior density and cost economics, the technology’s inherent characteristics , including reduced endurance per cell and greater sensitivity to data retention under high-temperature conditions , create qualification challenges for automotive applications requiring multi-decade reliability. Memory manufacturers must invest in specialized automotive-optimized 3D NAND variants and robust firmware management solutions, adding development complexity. The qualification timelines for new process nodes within the automotive segment can extend well beyond those applicable to consumer markets, creating technology lag that may limit the market’s ability to rapidly capitalize on advancements in flash memory density and performance.

MARKET OPPORTUNITIES

Expansion of Over-the-Air Update Capabilities Driving High-Endurance Flash Demand

The widespread adoption of over-the-air (OTA) software update architectures across modern vehicle platforms is creating a compelling growth opportunity for automotive grade flash memory suppliers. As automakers implement OTA capabilities to remotely update vehicle firmware, navigation maps, ADAS algorithms, and infotainment systems, the endurance and write-cycle specifications for onboard flash memory must be significantly elevated. This architectural shift is driving OEM procurement toward higher-endurance automotive-grade NAND and NOR flash solutions capable of sustaining frequent write operations throughout the vehicle’s operational lifespan. Memory suppliers that can demonstrate superior endurance profiles combined with AEC-Q100 qualification are well-positioned to capture growing design-win opportunities across both established automakers and emerging EV-native brands.

Growth of Zonal and Centralized Vehicle Electrical Architecture Creating New Memory Design Opportunities

The automotive industry’s transition from distributed electronic control unit architectures to zonal and centralized computing platforms represents a transformative opportunity for the automotive grade flash memory market. Next-generation vehicle electrical architectures consolidate control functions into fewer, more powerful domain controllers and vehicle computers, each requiring substantially greater flash memory capacity to store consolidated software stacks, application data, and functional safety partitions. This architectural evolution is accelerating demand for high-density automotive-grade managed NAND solutions, embedded MultiMediaCards (eMMC), and Universal Flash Storage (UFS) components qualified to automotive standards. Memory suppliers capable of delivering scalable, high-capacity solutions with robust functional safety features aligned to ISO 26262 ASIL-B and ASIL-D requirements are positioned to benefit significantly as automakers accelerate their adoption of centralized vehicle computing platforms throughout the forecast period.

MAIN TITLE HERE () Trends

Rising Demand for Advanced Driver Assistance Systems Fueling Automotive Grade Flash Memory Adoption

The automotive grade flash memory market is witnessing robust growth driven by the rapid proliferation of advanced driver assistance systems (ADAS) across passenger and commercial vehicles. Modern ADAS platforms require high-speed, high-reliability memory solutions capable of processing large volumes of real-time sensor data, including inputs from cameras, radar, and LiDAR systems. Automotive grade flash memory, engineered to operate reliably across wide temperature ranges and under mechanical stress conditions, has become a foundational component in these safety-critical applications. As automakers worldwide accelerate the integration of Level 2 and Level 3 autonomous driving features, demand for NOR and NAND flash memory solutions certified to automotive standards continues to strengthen significantly.

Other Trends

Infotainment and Instrument Cluster Upgrades Driving NOR Flash Consumption

The ongoing transformation of in-vehicle infotainment systems and digital instrument clusters is generating sustained demand for automotive grade flash memory, particularly NOR flash. Consumers increasingly expect seamless connectivity, high-resolution displays, and over-the-air update capabilities in their vehicles. NOR flash memory, valued for its fast random read performance and execute-in-place capability, is extensively deployed in infotainment control units and instrument cluster microcontrollers. Automotive-qualified NOR flash devices from manufacturers such as Macronix, Winbond, and Infineon Technologies are seeing increased design-in activity as automakers refresh interior electronics across multiple vehicle platforms.

Vehicle-to-Everything (V2X) Communication Expanding Flash Memory Use Cases

The emergence of Vehicle-to-Everything (V2X) communication technology is creating new demand vectors for automotive grade flash memory. V2X systems require reliable, low-latency memory to store and process communication protocols, security certificates, and real-time traffic data. As regulatory frameworks supporting V2X deployment advance across North America, Europe, and Asia, automotive flash memory suppliers are developing purpose-built solutions optimized for connected vehicle applications. This trend is expected to broaden the addressable market for automotive grade flash memory beyond traditional storage applications into active communication and edge computing roles within modern vehicle architectures.

Competitive Landscape and Regional Manufacturing Trends

The automotive grade flash memory market features a concentrated competitive landscape, with leading global semiconductor manufacturers including Samsung, Micron, Kioxia, SK Hynix, and Western Digital holding significant combined revenue share. These players are investing in automotive-qualified production lines and expanding their product portfolios to address the full spectrum of automotive memory requirements, from entry-level microcontrollers to high-performance ADAS processors. Regionally, Asia-Pacific remains the dominant production and consumption hub, with China and Japan representing key markets. North America and Europe are also experiencing growing demand, supported by local automotive OEM investments in electrification and autonomous vehicle programs. Supply chain resilience and AEC-Q100 qualification standards continue to shape procurement strategies across the industry.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Grade Flash Memory Market – Competitive Dynamics, Strategic Positioning, and Leading Manufacturer Profiles

Global Automotive Grade Flash Memory market is characterized by intense competition among a concentrated group of technologically advanced semiconductor manufacturers. Samsung and Micron Technology collectively command a significant share of the market, leveraging their extensive R&D capabilities, large-scale fabrication facilities, and vertically integrated supply chains to maintain dominant positions. Samsung’s automotive-qualified NOR and NAND flash solutions are widely deployed across ADAS, infotainment, and instrument cluster applications, while Micron’s AEC-Q100-qualified memory portfolio caters to the growing demands of connected and autonomous vehicle platforms. Kioxia and SK Hynix have also established strong footholds, with their automotive-grade NAND flash offerings gaining traction in high-bandwidth applications such as Advanced Driver Assistance Systems (ADAS) and Vehicle-to-Everything (V2X) communication modules. The top five players collectively accounted for a substantial portion of global revenues in 2025, reflecting the oligopolistic nature of this specialized memory segment.

Beyond the dominant tier-one suppliers, several niche and regional players contribute meaningfully to the competitive ecosystem of the Automotive Grade Flash Memory market. Infineon Technologies, with its robust NOR flash lineup qualified for automotive functional safety standards (ISO 26262), holds a prominent position in the European and North American automotive supply chains. Macronix and Winbond are recognized for their automotive-grade NOR flash solutions, particularly favored for instrument cluster and embedded control unit (ECU) applications due to their reliability and low power consumption profiles. GigaDevice and Ingenic Semiconductor represent the growing influence of Chinese semiconductor firms, increasingly qualifying their flash products to AEC-Q100 Grade 1 and Grade 0 standards to penetrate global OEM supply chains. Western Digital and Microchip Technology further diversify the competitive landscape, offering automotive storage and memory solutions optimized for the evolving requirements of software-defined vehicles, electrification, and in-vehicle networking architectures.

List of Key Automotive Grade Flash Memory Companies Profiled

- Samsung Electronics

- Micron Technology

- Kioxia Corporation

- SK Hynix

- Western Digital Corporation

- Infineon Technologies

- Macronix International Co., Ltd.

- Winbond Electronics Corporation

- GigaDevice Semiconductor Inc.

- Ingenic Semiconductor Co., Ltd.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- STMicroelectronics

- ISSI (Integrated Silicon Solution Inc.)

- Cypress Semiconductor (a Infineon Company)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

NOR Flash holds a dominant position in the automotive grade flash memory market, driven by its superior read speeds and execute-in-place (XIP) capability, which are critical for code storage and real-time execution in safety-critical automotive systems.

|

| By Application |

|

ADAS (Advanced Driver Assistance Systems) emerges as the most strategically significant application segment, reflecting the automotive industry’s accelerating shift toward semi-autonomous and autonomous vehicle architectures.

|

| By End User |

|

OEMs (Original Equipment Manufacturers) represent the primary and most influential end-user segment, as they dictate the memory specifications embedded across entire vehicle platforms during the design and production phase.

|

| By Vehicle Type |

|

Electric Vehicles (EVs) are rapidly establishing themselves as the most transformative and high-growth vehicle type for automotive-grade flash memory adoption, driven by the proliferation of sophisticated electronic architectures unique to electrified powertrains.

|

| By Interface/Technology Standard |

|

eMMC / UFS is emerging as the leading technology standard for next-generation automotive flash memory deployments, particularly as vehicle architectures evolve toward centralized computing platforms and zonal electronic designs.

|

Regional Analysis: Automotive Grade Flash Memory Market

Asia-Pacific

China’s rapid electrification of its automotive fleet has created an expansive and growing demand base for automotive grade flash memory. Government mandates around vehicle intelligence, combined with robust domestic EV production from both legacy automakers and emerging players, are fostering strong adoption of advanced memory solutions embedded within vehicle control units, navigation systems, and ADAS modules. The sheer scale of China’s automotive sector makes it the single largest sub-market within the Asia-Pacific region.

Japan’s automotive industry is synonymous with engineering precision, and this philosophy extends to its adoption of automotive grade flash memory. Japanese OEMs demand components that consistently exceed functional safety requirements, making the region a critical market for AEC-Q100 compliant memory solutions. The country’s deep semiconductor expertise also supports localized development of next-generation flash products tailored specifically for automotive environments involving extreme temperature variation and long operational lifespans.

South Korea’s globally dominant semiconductor manufacturers are strategically expanding their automotive-grade product portfolios to capture growing demand from both domestic automakers and international OEM clients. The convergence of South Korea’s memory fabrication expertise with the rising complexity of in-vehicle electronics positions the country as a vital contributor to the regional automotive grade flash memory supply chain, particularly for NAND flash solutions deployed in infotainment and telematics applications.

Taiwan’s advanced semiconductor foundries and packaging ecosystem provide critical support for the regional automotive grade flash memory market, enabling rapid scaling of production to meet surging demand. Meanwhile, Southeast Asian nations are emerging as important assembly and testing hubs for automotive electronics, gradually building capabilities that strengthen the broader regional supply chain. These markets are expected to play an increasingly prominent role as automotive electrification spreads across developing Asian economies through the forecast period.

North America

North America represents a highly significant market for automotive grade flash memory, anchored by the United States’ position as a global center of automotive innovation and technology development. The region’s prominent role in advancing autonomous vehicle research, software-defined vehicle architectures, and electrification programs has substantially elevated the demand for high-performance, reliable flash memory components. American automotive OEMs and technology firms are increasingly embedding sophisticated electronic systems into vehicles, from advanced driver assistance to connected infotainment platforms, all of which depend on automotive-qualified flash memory. Canada’s growing electric vehicle manufacturing footprint and Mexico’s expanding role as an automotive production hub further reinforce North American demand dynamics. Regulatory frameworks encouraging vehicle safety and connectivity standards are also contributing to accelerated adoption of automotive grade flash memory solutions across the region throughout the 2026 to 2034 period.

Europe

Europe occupies a critical position in Global automotive grade flash memory market, underpinned by its world-renowned automotive heritage and stringent vehicle safety and emissions regulations. Germany, France, Sweden, and Italy host some of the world’s most technologically advanced automotive manufacturers, all of whom are aggressively transitioning toward electrified and digitally connected vehicle platforms. The European Union’s regulatory environment around vehicle safety, data integrity, and emissions is compelling automakers to integrate increasingly sophisticated electronic systems, thereby driving sustained demand for automotive grade flash memory. Europe’s emphasis on functional safety standards, particularly ISO 26262 compliance, ensures that memory components deployed in the region must meet exceptional reliability thresholds. The region’s commitment to achieving ambitious carbon neutrality targets is also accelerating EV adoption, creating substantial incremental demand for automotive-grade flash memory solutions embedded in battery management and powertrain control systems.

South America

South America represents a developing yet progressively important market within Global automotive grade flash memory landscape. Brazil leads the region as the largest automotive production and consumption market, with growing interest in vehicle electrification and modernization of fleet electronics gradually increasing demand for automotive-qualified memory components. While the pace of adoption may be comparatively measured relative to more mature markets, South American automotive manufacturers are increasingly sourcing vehicles equipped with advanced infotainment and connectivity features that incorporate automotive grade flash memory. Government initiatives supporting local automotive production and energy transition, particularly in Brazil and Argentina, are expected to gradually elevate the regional market’s significance over the forecast horizon. Infrastructure development and rising consumer demand for technologically equipped vehicles further support a positive long-term demand outlook for the region’s automotive grade flash memory market.

Middle East & Africa

The Middle East and Africa region currently represents an emerging frontier in the automotive grade flash memory market, characterized by rising vehicle imports, expanding urban mobility infrastructure, and a growing appetite for technologically advanced vehicles among consumers in Gulf Cooperation Council nations. Countries such as the United Arab Emirates and Saudi Arabia are witnessing increased penetration of premium and connected vehicles, which inherently incorporate sophisticated flash memory-dependent electronic systems. Africa’s broader automotive market remains at an earlier stage of development, though long-term urbanization trends and infrastructure investment create a foundation for future growth. The Middle East’s ambitions around smart city development and sustainable transportation solutions may serve as a meaningful catalyst for automotive-grade electronics adoption over the coming decade, gradually positioning the region as a more active participant in Global automotive grade flash memory market through 2034.

Report Scope

This market research report provides a comprehensive analysis of the Automotive Grade Flash Memory Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Automotive Grade Flash Memory Market?

-> Global Automotive Grade Flash Memory Market was valued at USD 3.87 billion in 2025 and is expected to reach USD 9.64 billion by 2034, growing at a CAGR of 10.9%during the forecast period.

Which key companies operate in the Automotive Grade Flash Memory Market?

-> Key players include Samsung, Micron, Kioxia, SK Hynix, Western Digital, Infineon Technologies, Macronix, Winbond, GigaDevice, Ingenic Semiconductor, and Microchip Technology, among others. In 2025, Global top five players held a share of approximately % in terms of revenue.

What are the key growth drivers?

-> Key growth drivers include rising demand for ADAS and autonomous driving technologies, growth in connected vehicle platforms, expansion of infotainment systems, increasing adoption of V2X communication, and the need for high-reliability memory solutions capable of withstanding harsh automotive environments.

Which region dominates the Automotive Grade Flash Memory Market?

-> Asia represents a significant share of Global market, with China projected to reach USD million and the U.S. market estimated at USD million in 2025. North America and Europe also hold substantial market positions driven by advanced automotive manufacturing ecosystems.

What are the emerging trends in the Automotive Grade Flash Memory Market?

-> Emerging trends include the proliferation of NOR Flash and NAND Flash memory in automotive applications, integration of flash memory in ADAS, Instrument Clusters, and Infotainment Systems, and increasing deployment in V2X communication platforms. The NOR Flash segment is projected to reach USD million by 2034, with a CAGR of % over the next six years.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...