Automotive Grade Digital Isolation Chip Market Insights

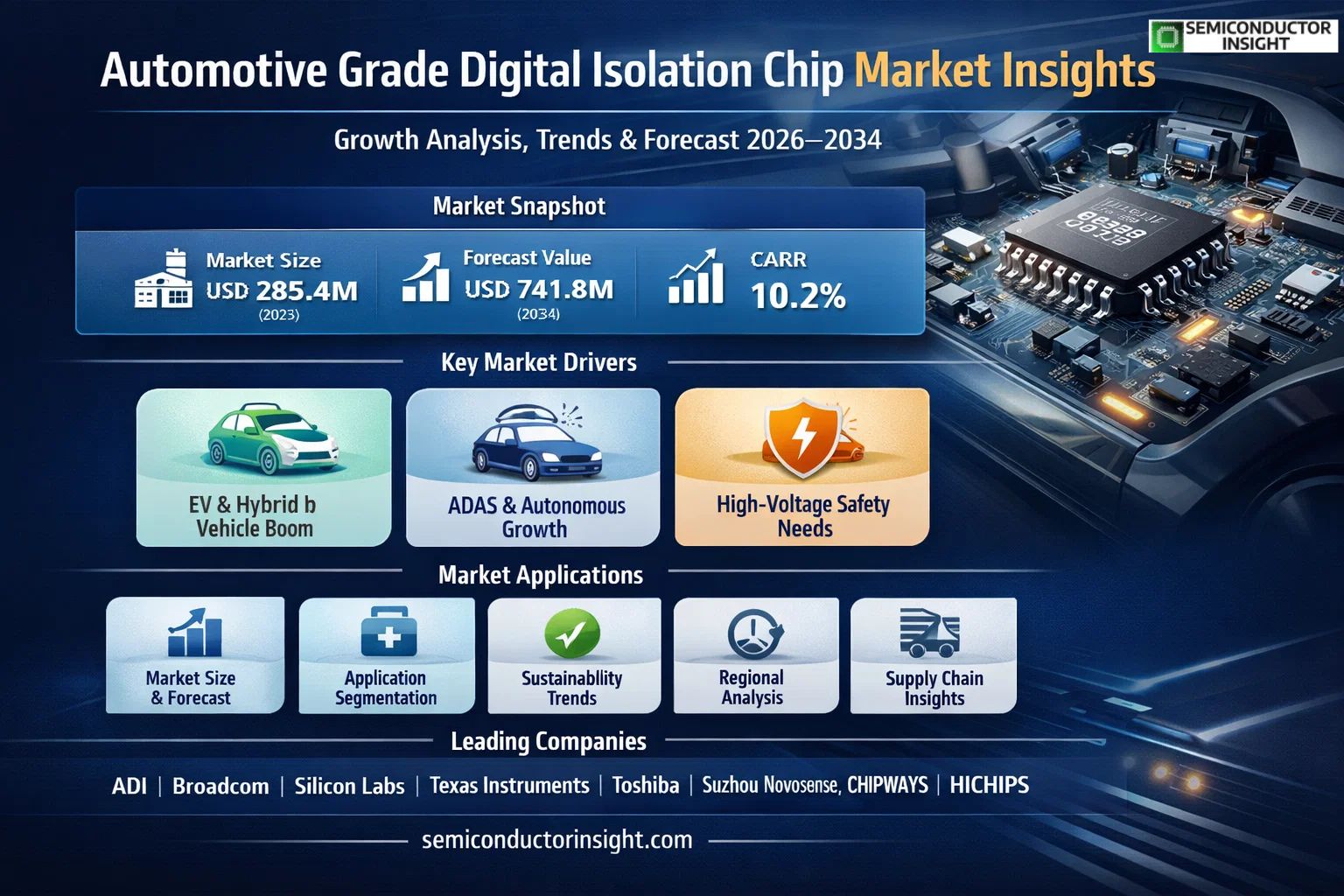

Global Automotive Grade Digital Isolation Chip market size was valued at USD 285.4 million in 2025. The market is projected to grow from USD 312.6 million in 2026 to USD 741.8 million by 2034, exhibiting a CAGR of 10.2% during the forecast period.

Automotive grade digital isolation chip is a specialized semiconductor device used in vehicle electronic systems to achieve safe and reliable communication between sensitive low-voltage components and fast transient high-voltage circuits. By effectively isolating high-voltage and low-voltage domains, these chips protect critical control units from voltage spikes, electromagnetic interference, and ground loops. The primary isolation technologies employed include magnetic coupling and capacitive (tolerant) coupling, each offering distinct performance advantages depending on the application environment. These chips are designed to meet stringent automotive qualification standards such as AEC-Q100, ensuring long-term reliability across extreme temperature ranges and harsh operating conditions.

The market is experiencing robust growth driven by the accelerating electrification of automobiles and the rapid advancement of vehicle intelligence. As electric vehicles (EVs), hybrid electric vehicles (HEVs), and advanced driver-assistance systems (ADAS) become increasingly mainstream, the demand for high-performance digital isolation solutions continues to expand significantly. Furthermore, the proliferation of in-vehicle communication protocols and the integration of battery management systems (BMS) in EVs have created substantial new application opportunities for automotive-grade digital isolation chips. ADI, Broadcom, Silicon Labs, Texas Instruments (TI), Toshiba, Suzhou Novosense, CHIPWAYS, and HICHIPS are among the key players operating in this market with diversified and competitive product portfolios.

MARKET DRIVERS

Rising Electrification of Vehicles Accelerating Demand for Robust Isolation Solutions

The rapid transition toward electric vehicles (EVs) and hybrid electric vehicles (HEVs) is one of the most significant forces shaping utomotive Grade Digital Isolation Chip Market. As high-voltage battery systems, onboard chargers, and traction inverters become standard components in modern powertrains, the need for reliable galvanic isolation between high-voltage and low-voltage domains has intensified considerably. Automotive grade digital isolators play a critical role in safeguarding sensitive microcontrollers and communication interfaces from potentially damaging voltage transients, making them indispensable in next-generation vehicle architectures. The sustained growth in EV adoption across major markets in Asia-Pacific, Europe, and North America continues to generate strong procurement demand from Tier-1 automotive suppliers and OEMs alike.

Expansion of Advanced Driver Assistance Systems (ADAS) and Autonomous Driving Technologies

The proliferation of Advanced Driver Assistance Systems (ADAS) and the incremental advancement toward higher levels of vehicle autonomy are directly fueling the consumption of automotive grade digital isolation chips. These systems rely on an increasing number of electronic control units (ECUs), LiDAR modules, radar sensors, and camera interfaces that require noise-free, isolated communication channels to function reliably in electrically noisy vehicle environments. Digital isolators that comply with AEC-Q100 qualification standards are particularly well-positioned to serve these demanding applications, offering superior electromagnetic interference (EMI) immunity and longer operational lifespans compared to traditional optocoupler-based solutions.

➤ Automotive grade digital isolation chips are increasingly replacing legacy optocouplers in safety-critical ECU designs, offering up to 10x faster data rates and significantly improved reliability across extended temperature ranges required by automotive qualification standards.

Furthermore, the growing integration of vehicle-to-everything (V2X) communication infrastructure and the expansion of in-vehicle networking protocols such as CAN FD, LIN, and automotive Ethernet are creating additional application nodes where digital isolation is essential. As software-defined vehicle architectures gain traction, centralized compute platforms with domain controllers require isolation at multiple interface points, broadening the addressable scope of utomotive Grade Digital Isolation Chip Market beyond powertrain applications into the broader vehicle electronics ecosystem.

MARKET CHALLENGES

Stringent AEC-Q100 Qualification Requirements Posing Technical and Commercial Barriers

One of the foremost challenges confronting participants in utomotive Grade Digital Isolation Chip Market is the rigorous qualification process mandated by the AEC-Q100 stress test standard for integrated circuits used in automotive applications. Achieving and maintaining this certification demands extensive reliability testing across wide temperature ranges, typically spanning -40°C to +125°C or beyond, as well as compliance with electrostatic discharge (ESD) and latch-up performance criteria. For emerging semiconductor companies and new market entrants, the time and capital investment required to complete AEC-Q100 qualification can represent a significant barrier, often extending product development cycles by 12 to 24 months and increasing non-recurring engineering costs substantially. This dynamic tends to concentrate competitive advantages among established suppliers with pre-existing automotive certification infrastructure.

Other Challenges

Supply Chain Complexity and Semiconductor Sourcing Constraints

The automotive semiconductor supply chain has demonstrated notable vulnerability to disruption, as evidenced by Global chip shortage that significantly impacted vehicle production schedules in recent years. Automotive grade digital isolation chips, while individually lower in volume than microcontrollers or memory devices, are subject to the same long-lead-time procurement dynamics and allocation pressures that characterize the broader automotive IC ecosystem. OEMs and Tier-1 suppliers are increasingly requiring multi-sourcing strategies and safety stock arrangements, which in turn place operational and inventory management burdens on component distributors and chipmakers operating within this segment of utomotive Grade Digital Isolation Chip Market.

Integration with Evolving Functional Safety Standards

Meeting ISO 26262 functional safety requirements adds a layer of design complexity that presents ongoing challenges for developers of digital isolation solutions targeting safety-critical automotive subsystems. Demonstrating the required Automotive Safety Integrity Level (ASIL) compliance through hardware and software diagnostic measures demands close collaboration between chip designers, system integrators, and OEM safety engineering teams. This requirement elevates the engineering expertise threshold for participation in the market and may slow adoption cycles for new isolation chip architectures that have not yet accumulated the operational field data required to support robust ASIL certification arguments.

MARKET RESTRAINTS

High Design-In Complexity and Extended Automotive Product Lifecycle Commitments

A meaningful restraint on the growth trajectory of utomotive Grade Digital Isolation Chip Market is the inherently long and complex design-in process associated with automotive electronic components. Unlike consumer or industrial electronics applications where product refresh cycles may span two to three years, automotive platform programs typically commit to specific component selections for seven to ten years or longer, encompassing production and aftermarket service requirements. This extended lifecycle expectation makes OEMs and Tier-1 suppliers highly conservative in qualifying new digital isolation chip vendors or adopting novel isolation technologies, even when performance and cost advantages are evident. The result is a market where incumbent suppliers with established design wins enjoy significant revenue stability, but new entrants face prolonged ramp timelines before capturing meaningful market share.

Cost Sensitivity in Volume Automotive Applications Limiting Premium Product Penetration

While the performance attributes of advanced automotive grade digital isolation chips are well recognized within the engineering community, persistent cost sensitivity at the vehicle system level represents a tangible restraint on market expansion, particularly in high-volume, cost-competitive vehicle segments. Procurement teams at major OEMs apply considerable pressure on component pricing across all electronic subsystems, and digital isolators are not immune to this dynamic. In applications where the isolation performance requirements do not necessitate the full capability set of premium-tier devices, buyers may default to lower-specification alternatives or delay upgrades to more advanced isolation solutions, moderating the overall revenue growth potential for higher-margin products within utomotive Grade Digital Isolation Chip Market.

MARKET OPPORTUNITIES

Growing Adoption of 800V Battery Architectures Opening New High-Performance Isolation Design Windows

The industry-wide shift toward 800-volt battery platform architectures in premium and performance electric vehicles represents a compelling growth opportunity for utomotive Grade Digital Isolation Chip Market. Higher system voltages place more demanding requirements on isolation barrier performance, including higher working voltage ratings, improved partial discharge resistance, and tighter creepage and clearance specifications. Digital isolation chips engineered to address these elevated voltage environments offer OEMs and Tier-1 suppliers a technically superior alternative to legacy isolation approaches, and the qualification of such devices into high-voltage powertrain programs could unlock substantial design win value as 800V platforms become more prevalent across mid-market vehicle segments over the coming years.

Expansion into Emerging Markets and Localized EV Supply Chains Creating New Demand Centers

The accelerated development of domestic automotive manufacturing ecosystems in markets such as India, Southeast Asia, and Latin America presents a meaningful incremental opportunity for suppliers active in utomotive Grade Digital Isolation Chip Market. As these regions scale up local EV production and develop indigenous automotive electronic supply chains, demand for AEC-Q100 qualified components, including digital isolators, is expected to grow from a relatively modest base. Suppliers that proactively establish application engineering support, local distribution partnerships, and regionally tailored product portfolios in these emerging automotive hubs may achieve early positioning advantages that translate into durable, long-term design win pipelines as local vehicle production volumes mature.

Integration of Isolation Functionality into Multi-Function Automotive SoCs Enabling Co-Design Opportunities

An evolving architectural trend toward greater semiconductor integration within automotive electronic systems presents a nuanced but strategically significant opportunity for digital isolation chip developers. As automotive system-on-chip (SoC) vendors and microcontroller suppliers explore the integration of isolation capability alongside processing, communication, and power management functions within unified device platforms, there is a growing need for co-design and co-development collaboration between isolation specialists and broader semiconductor ecosystem participants. Companies with deep expertise in automotive grade digital isolation technology that can effectively engage in such collaborative engagements — whether through IP licensing, chiplet-based architectures, or joint reference design programs — stand to access revenue streams that extend beyond traditional standalone component sales within the evolving Automotive Grade Digital Isolation Chip Market.

Trends

Electrification and Intelligence as Core Demand Drivers

Automotive Grade Digital Isolation Chip Market is experiencing significant momentum driven by the accelerating electrification of Global automotive industry. As vehicles increasingly incorporate high-voltage powertrains, battery management systems, and advanced driver-assistance systems (ADAS), the need for reliable electrical isolation between high-voltage and low-voltage circuits has become critical. Automotive grade digital isolation chips serve as essential semiconductor components that enable safe signal transmission across these voltage domains, protecting sensitive electronics from potentially damaging transient voltages. The continued global push toward electric vehicles (EVs) and hybrid electric vehicles (HEVs) is reinforcing sustained demand for these chips across both passenger car and commercial vehicle segments.

Other Trends

Rising Adoption in Battery Management and Charging Systems

One of the prominent application trends within utomotive Grade Digital Isolation Chip Market is the growing integration of these devices in battery management systems (BMS) and onboard charging units. As EV battery packs operate at increasingly higher voltages to extend driving range and improve efficiency, robust isolation solutions have become a non-negotiable design requirement. Digital isolation chips based on magnetic coupling technology are gaining traction in this application area due to their high immunity to electromagnetic interference and reliable performance under harsh automotive operating conditions. Key manufacturers including ADI, Texas Instruments (TI), Silicon Labs, and Suzhou Novosense are actively developing AEC-Q100-qualified isolation devices tailored for these demanding environments.

Expansion of ADAS and Functional Safety Requirements

The rapid proliferation of ADAS features — including automatic emergency braking, lane-keeping assist, and radar-based sensing — is creating additional growth avenues for utomotive Grade Digital Isolation Chip Market. These safety-critical systems require high-speed, low-latency data communication with guaranteed isolation to meet ISO 26262 functional safety standards. Chipmakers are responding by introducing isolation solutions with enhanced data rates, reinforced insulation ratings, and integrated diagnostics. Compliance with stringent automotive-grade qualification standards is becoming a key competitive differentiator among suppliers such as Broadcom, Toshiba, CHIPWAYS, and HICHIPS.

Localization and Supply Chain Diversification Reshaping Competitive Dynamics

Geopolitical considerations and supply chain disruptions experienced in recent years have prompted automotive OEMs and Tier-1 suppliers to actively diversify their sourcing strategies for semiconductor components, including digital isolation chips. This has accelerated the growth of domestic chip manufacturers in Asia, particularly in China, where companies such as Suzhou Novosense and CHIPWAYS are scaling production capacity to serve regional automotive customers. Meanwhile, established global players are investing in regional manufacturing and qualification programs to ensure supply continuity. This trend toward supply chain localization is expected to introduce greater competition and innovation within utomotive Grade Digital Isolation Chip Market over the coming years, ultimately benefiting automotive manufacturers seeking resilient and cost-effective sourcing options.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Grade Digital Isolation Chip Market – Competitive Dynamics, Strategic Positioning, and Leading Manufacturer Profiles

Global Automotive Grade Digital Isolation Chip market is characterized by a moderately consolidated competitive landscape, with a handful of established semiconductor giants commanding a significant share of total revenue. Analog Devices, Inc. (ADI) stands out as a dominant force in this space, leveraging its deep expertise in signal processing and isolation technology to deliver AEC-Q100-qualified digital isolators tailored for electric vehicle (EV) powertrains, battery management systems (BMS), and onboard charging modules. Texas Instruments (TI) and Broadcom similarly maintain strong footholds, offering robust automotive-grade isolation portfolios that address the stringent reliability, electromagnetic compatibility (EMC), and functional safety (ISO 26262) requirements demanded by Tier-1 automotive suppliers and OEMs. Silicon Labs further distinguishes itself through its proprietary CMOS-based isolation technology, enabling high-speed data transmission across isolation barriers with low power consumption — a critical attribute as vehicle electrification and ADAS integration intensify across global automotive platforms.

Beyond Global incumbents, a growing cohort of specialized and regional players is reshaping the competitive dynamics of utomotive Grade Digital Isolation Chip Market. Toshiba’s Semiconductor & Storage division contributes photocoupler and digital isolator solutions with strong traction in Asia-Pacific automotive supply chains, particularly in Japan and South Korea. Chinese domestic manufacturers such as Suzhou Novosense Microelectronics, CHIPWAYS, and HICHIPS have emerged as strategically significant competitors, benefiting from government-backed semiconductor self-sufficiency initiatives and the rapid localization of EV component sourcing within China — now one of the world’s largest and fastest-growing automotive electronics markets. These companies are actively expanding their AEC-Q100-certified product lines to compete on performance, cost, and supply chain resilience, making them increasingly relevant not only in China but also in broader emerging market automotive ecosystems. The competitive intensity in this market is expected to escalate as automakers accelerate the transition to software-defined vehicles, 800V EV architectures, and integrated intelligent cockpit systems — all of which demand advanced, high-performance digital isolation solutions.

List of Key Automotive Grade Digital Isolation Chip Companies Profiled

- Analog Devices, Inc. (ADI)

- Broadcom Inc.

- Silicon Laboratories (Silicon Labs)

- Texas Instruments (TI)

- Toshiba Electronic Devices & Storage Corporation

- Suzhou Novosense Microelectronics Co., Ltd.

- CHIPWAYS Technology Co., Ltd.

- HICHIPS Technology Co., Ltd.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Skyworks Solutions, Inc.

- ROHM Semiconductor

- Renesas Electronics Corporation

- Shanghai Chipanalog Microelectronics Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Magnetic Coupling is the leading segment in utomotive Grade Digital Isolation Chip Market, driven by its robust performance characteristics and superior reliability in demanding automotive environments.

|

| By Application |

|

Passenger Car represents the dominant application segment for automotive grade digital isolation chips, propelled by the accelerating global transition toward battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs).

|

| By End User |

|

Original Equipment Manufacturers (OEMs) constitute the leading end-user segment, as they directly govern the design specifications and component selection processes for new vehicle platforms at scale.

|

| By Isolation Channel |

|

Multi-Channel (4-Channel and above) isolation chips are emerging as the fastest-growing sub-segment, driven by the increasing complexity of modern automotive electronic architectures that require simultaneous isolation of multiple signal paths within a compact form factor.

|

| By Voltage Rating |

|

1000V – 2500V rated digital isolation chips represent the leading voltage rating segment, aligning with the high-voltage requirements of contemporary electric vehicle battery packs and powertrain systems that typically operate within this range.

|

Regional Analysis: Automotive Grade Digital Isolation Chip Market

Asia-Pacific

Asia-Pacific’s rapid transition toward electrified transportation is a primary catalyst for automotive grade digital isolation chip adoption. The surging volume of battery electric vehicles and plug-in hybrids across the region demands highly reliable isolation components that safeguard low-voltage control circuits from high-voltage power trains, creating a consistent and expanding demand environment for isolation chip manufacturers operating in this space.

The region hosts some of the world’s most advanced semiconductor fabrication facilities, giving Asia-Pacific a structural advantage in producing automotive grade digital isolation chips at scale. Taiwan, South Korea, and Japan lead in process technology, enabling local chip designers to deliver solutions that meet stringent AEC-Q100 qualification standards required for automotive-grade components deployed in safety-critical vehicle subsystems.

Proactive government policies across China, Japan, South Korea, and India are reshaping the automotive semiconductor landscape. Subsidies for EV adoption, mandates for domestic chip production, and investments in smart mobility infrastructure collectively strengthen the demand for automotive grade digital isolation chips. These policies reduce dependence on foreign supply chains and accelerate the commercialization of locally developed isolation technologies.

Asia-Pacific serves as a leading innovation hub for automotive electronics, with extensive R&D investment flowing into ADAS, vehicle electrification, and in-vehicle networking technologies. These developments necessitate advanced digital isolation solutions capable of operating in high-noise, thermally demanding automotive environments, positioning regional chip suppliers to develop next-generation products that align with global safety and performance benchmarks.

North America

North America represents a mature and technologically sophisticated market for automotive grade digital isolation chips, characterized by strong demand from established automotive OEMs and a growing base of electric vehicle startups. The United States leads regional consumption, underpinned by significant investments in EV infrastructure, domestic semiconductor production through initiatives like the CHIPS Act, and the presence of influential technology-driven automakers advancing software-defined vehicle architectures. The region’s stringent automotive safety standards, including compliance with functional safety norms such as ISO 26262, drive automakers and suppliers to adopt high-reliability digital isolation components. Canada and Mexico contribute through integrated supply chain participation within the broader North American automotive manufacturing corridor. The increasing complexity of power electronics in EVs and HEVs, combined with growing adoption of advanced driver assistance systems, sustains robust demand for automotive grade digital isolation chip solutions across the region through the forecast period.

Europe

Europe occupies a strategically important position in Global automotive grade digital isolation chip market, supported by the continent’s legacy of automotive engineering excellence and its accelerated pivot toward vehicle electrification. Germany, France, Sweden, and the United Kingdom house some of the world’s premier automotive brands and tier-1 electronics suppliers, all of whom require advanced isolation technologies to meet the demands of modern EV powertrains and high-voltage battery systems. European Union regulations mandating reduced carbon emissions and the phased elimination of internal combustion engine vehicles are compelling automakers to transition at pace, directly amplifying demand for automotive grade digital isolation chips. The region also places particular emphasis on cybersecurity and functional safety within vehicle electronics, encouraging investment in isolation solutions that provide both signal integrity and robust protection against electromagnetic interference in increasingly connected vehicle platforms.

South America

South America presents a developing yet progressively relevant market for automotive grade digital isolation chips, with Brazil serving as the primary demand center due to its large automotive manufacturing base and growing interest in electrified mobility. While the region’s adoption of fully electric vehicles remains at an earlier stage compared to North America, Europe, and Asia-Pacific, the gradual modernization of vehicle electronics and the increasing integration of safety-oriented systems are beginning to drive localized demand for isolation chip technologies. Multinational automotive manufacturers operating production facilities in Brazil and Argentina are transferring advanced electronic architectures into regionally assembled vehicles, which necessitates sourcing automotive grade digital isolation components. Government incentives aimed at promoting green transportation and reducing fuel dependency are expected to incrementally support market growth through the 2026 to 2034 forecast period.

Middle East & Africa

The Middle East and Africa region currently represents a nascent stage of development within utomotive Grade Digital Isolation Chip Market, yet several structural factors suggest meaningful long-term potential. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are investing substantially in smart city infrastructure and sustainable transportation, with electric vehicle adoption receiving policy-level encouragement. South Africa serves as the continent’s primary automotive manufacturing hub, with established assembly operations for global brands that increasingly incorporate advanced electronic systems. As regional automakers and distributors align vehicle specifications more closely with international standards, demand for automotive grade digital isolation chips is expected to rise steadily. The gradual expansion of EV charging infrastructure and growing consumer awareness of electrified vehicles across select urban centers in the region are anticipated to provide incremental momentum for utomotive Grade Digital Isolation Chip Market over the coming years.

Report Scope

This market research report provides a comprehensive analysis of utomotive Grade Digital Isolation Chip Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive Grade Digital Isolation Chip Market?

->Global Automotive Grade Digital Isolation Chip market size was valued at USD 285.4 million in 2025.The market is projected to grow from USD 312.6 million in 2026 to USD 741.8 million by 2034, exhibiting a CAGR of 10.2% during the forecast period.

Which key companies operate in Automotive Grade Digital Isolation Chip Market?

-> Key players include ADI, Broadcom, Silicon Labs, TI, Toshiba, Suzhou Novosense, CHIPWAYS, and HICHIPS, among others. In 2025, Global top five players held approximately % of the market in terms of revenue.

What are the key growth drivers?

-> Key growth drivers include the electrification of automobiles, the rising trend of vehicle intelligence and connectivity, increasing demand for safe communication between high-voltage and low-voltage electronic components, and expanding adoption of automotive-grade semiconductor devices across passenger cars and commercial vehicles.

Which region dominates the market?

-> Asia-Pacific is a significant region in utomotive Grade Digital Isolation Chip Market, with China projected to reach USD million by 2034. North America also holds a notable share, with the U.S. market estimated at USD million in 2025.

What are the emerging trends?

-> Emerging trends include growing adoption of magnetic coupling and tolerant coupling isolation technologies, increasing integration of digital isolation chips in EV powertrains and ADAS systems, advancements in semiconductor fabrication for automotive-grade reliability, and expanding applications across both passenger cars and commercial vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...