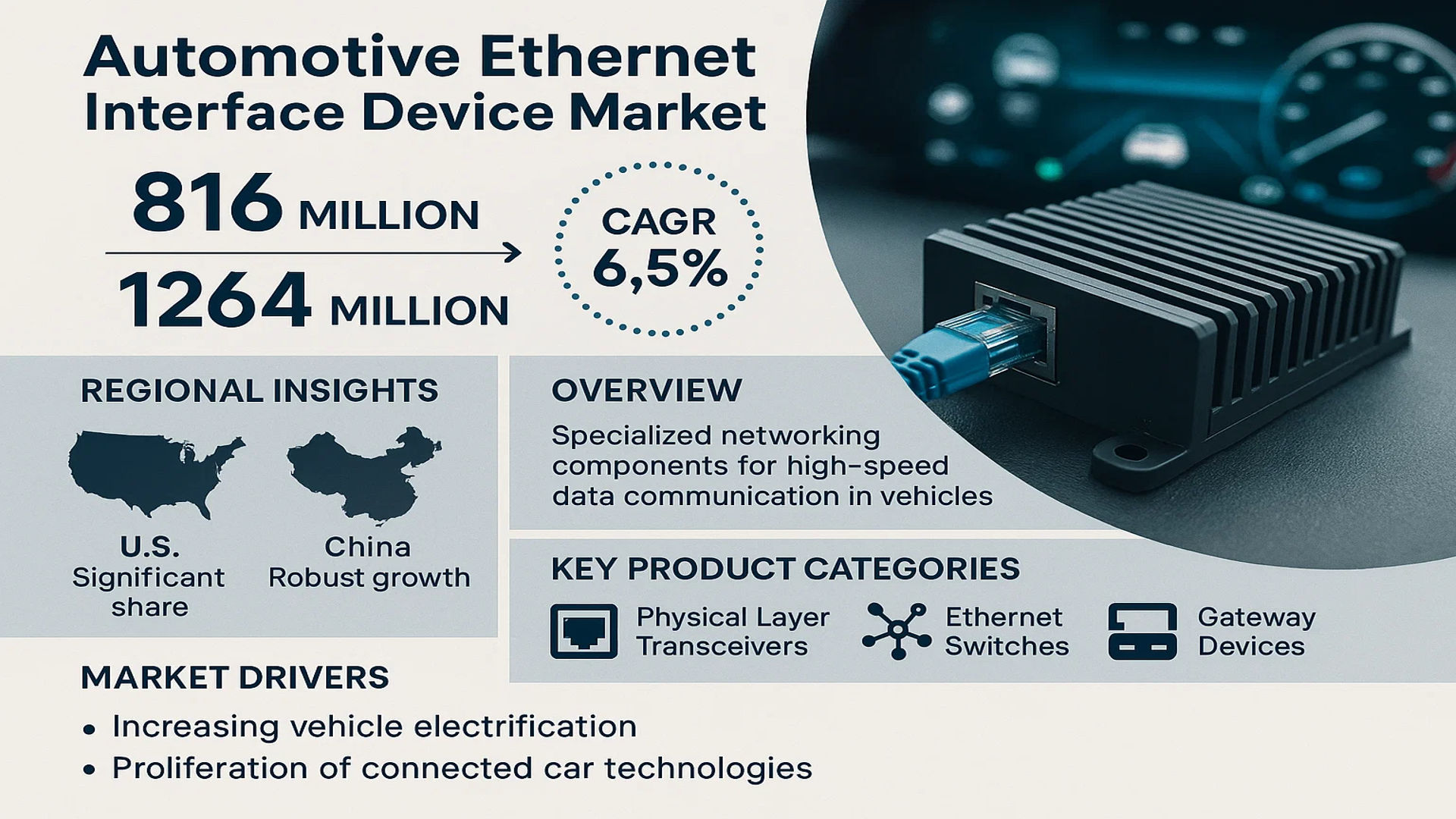

MARKET INSIGHTS

The global Automotive Ethernet Interface Device Market was valued at 816 million in 2024 and is projected to reach US$ 1264 million by 2032, at a CAGR of 6.5% during the forecast period. The U.S. market is estimated to account for a significant share, while China is expected to witness robust growth, reflecting the increasing demand for advanced automotive networking solutions.

Automotive Ethernet interface devices are specialized networking components designed to meet the high-speed data communication requirements of modern vehicles. These devices integrate traditional Ethernet technology with automotive-specific protocols like IEEE 802.3 (100BASE-T1, 1000BASE-T1) and AUTOSAR standards to enable reliable, low-latency connectivity between electronic control units (ECUs). Key product categories include physical layer transceivers (PHY), Ethernet switches, and gateway devices that support advanced driver-assistance systems (ADAS) and in-vehicle infotainment.

The market growth is primarily driven by increasing vehicle electrification and the proliferation of connected car technologies. While automotive manufacturers are accelerating the adoption of Ethernet-based architectures to support bandwidth-intensive applications, challenges remain in standardization and cybersecurity. Leading players like Broadcom, NXP Semiconductors, and Texas Instruments are investing heavily in developing next-generation solutions, with recent advancements focusing on multi-gigabit automotive Ethernet for autonomous driving systems.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced Driver Assistance Systems (ADAS) Accelerates Market Growth

The global proliferation of ADAS technologies is acting as a primary catalyst for automotive Ethernet interface device adoption. These systems require ultra-reliable, high-bandwidth networks to process massive data flows from numerous sensors including radars, cameras, and LiDAR units. Modern vehicles now incorporate up to 20+ ADAS functions, with each autonomous level increase demanding exponentially more data transmission capacity. This has spurred automakers to transition from traditional CAN buses to automotive Ethernet, which can deliver the required 1Gbps+ bandwidth while meeting stringent automotive-grade reliability standards. The ADAS market itself is projected to grow substantially, further driving demand for robust in-vehicle networking solutions that Ethernet interface devices provide.

Vehicle Electrification Trends Create New Networking Demands

The rapid shift toward electric vehicles (EVs) is reshaping automotive networking architectures. EVs require sophisticated battery management systems and power electronics that generate vast amounts of real-time data needing precise synchronization. Automotive Ethernet’s ability to support both power and data transmission over single cabling (Power over Data Line) makes it particularly suitable for EV applications. With global EV sales projected to account for over 30% of all vehicle sales by 2030, this represents a significant growth vector for Ethernet interface devices. Major OEMs are redesigning vehicle electrical/electronic architectures around Ethernet backbones to accommodate electrification needs while reducing wiring complexity and weight.

Standardization Efforts and Cost Reductions Drive Mainstream Adoption

Recent standardization of automotive-specific Ethernet variants (100BASE-T1, 1000BASE-T1) through IEEE 802.3 and OPEN Alliance has reduced implementation barriers. These standards address automotive requirements like electromagnetic compatibility, while maintaining compatibility with conventional Ethernet. Simultaneously, economies of scale have driven per-port costs down by approximately 40% over the past five years, making automotive Ethernet increasingly cost-competitive with legacy networks. This cost-performance improvement is accelerating Ethernet’s penetration beyond premium vehicles into mass-market segments. The growing availability of AUTOSAR-compliant software stacks further simplifies integration, encouraging broader ecosystem participation.

MARKET RESTRAINTS

Legacy Vehicle Architectures and Retrofit Challenges Limit Immediate Adoption

Despite strong growth prospects, automotive Ethernet faces inertia from entrenched vehicle architectures. Many current production vehicles utilize electrical systems designed around Controller Area Network (CAN) and FlexRay protocols, with development cycles spanning 5-7 years. Retrofitting Ethernet into these legacy architectures requires extensive redesign of electronic control units (ECUs) and wiring harnesses, creating cost and complexity barriers. This is particularly challenging for lower-tier suppliers operating on tight margins. Additionally, many existing automotive applications don’t yet require Ethernet’s bandwidth capabilities, allowing legacy networks to maintain relevance in cost-sensitive segments.

Network Security Concerns Present Implementation Hurdles

As vehicles become increasingly connected, Ethernet’s expanded attack surface raises cybersecurity concerns. While traditional automotive networks were physically isolated, Ethernet enables potential external access points that could be exploited. Implementing robust security measures like MACsec encryption adds complexity and cost to Ethernet deployments. The industry is still developing standardized approaches to automotive network security, with competing solutions creating interoperability challenges. These security considerations slow adoption as automakers balance innovation with risk management, particularly for safety-critical systems.

MARKET OPPORTUNITIES

Domain Consolidation and Zonal Architectures Create New Implementation Paradigms

The industry’s shift toward domain-based and zonal E/E architectures presents significant opportunities for Ethernet interface devices. These new architectures consolidate functions into high-performance computing modules connected via Ethernet backbones, replacing distributed ECU networks. A single zonal gateway might replace dozens of discrete ECUs, dramatically increasing Ethernet port requirements per vehicle. This architectural transformation could multiply the average Ethernet interface device content per vehicle by 3-5x compared to current implementations. Early adopters among premium automakers are demonstrating the feasibility of these approaches, paving the way for broader market expansion.

Emerging In-Vehicle Applications Demand Higher Network Performance

Next-generation vehicle features like autonomous driving, advanced infotainment, and vehicle-to-everything (V2X) communication are creating unprecedented networking demands. These applications require both high bandwidth and deterministic latency that only automotive Ethernet can provide at scale. For example, centralized high-definition mapping systems may require continuous multi-gigabit data flows from various sensors to processing units. The upcoming transition to 2.5G/5G/10G automotive Ethernet standards will further expand the addressable market for interface devices. These technological advances coincide with growing consumer expectations for connected vehicle features, ensuring sustained demand growth.

MARKET CHALLENGES

Supply Chain Complexity and Component Shortages Impact Production

The automotive semiconductor supply chain faces ongoing challenges that directly affect Ethernet interface device availability. These components require specialized manufacturing processes combining high-performance networking capabilities with automotive-grade reliability. Recent disruptions have created lead times exceeding 12 months for certain Ethernet PHY chips, forcing automakers to redesign or delay vehicle programs. The situation is compounded by the concentrated nature of the supplier base, with just a handful of companies capable of producing compliant devices at scale. As Ethernet becomes more pervasive in vehicles, ensuring stable component supply will be critical to market growth.

Interoperability and Testing Requirements Increase Development Costs

Validating Ethernet interface devices across diverse vehicle systems presents significant technical and financial challenges. Unlike consumer Ethernet, automotive implementations must operate flawlessly across temperature extremes, vibration, and electromagnetic interference. Comprehensive conformance testing to IEEE and OEM-specific standards can account for 20-30% of development budgets. Moreover, the lack of universal test methodologies creates redundant validation efforts across the supply chain. These factors contribute to extended product development cycles and higher per-unit costs, particularly for smaller suppliers entering the market.

AUTOMOTIVE ETHERNET INTERFACE DEVICE MARKET TRENDS

Rising Demand for High-Speed In-Vehicle Networking Solutions

The automotive industry is undergoing a significant transformation as vehicles become increasingly connected and autonomous. This shift is fueling demand for high-speed, reliable communication networks within vehicles, propelling the adoption of Automotive Ethernet Interface Devices. The global market, valued at $816 million in 2024, is projected to reach $1.26 billion by 2032, growing at a CAGR of 6.5%. This growth is attributed to the rising complexity of automotive electronic control units (ECUs) and the need for efficient data transfer between advanced driver-assistance systems (ADAS), infotainment systems, and sensors. Additionally, the evolution towards 1000BASE-T1 and Multi-Gig Ethernet standards is enabling faster and more stable in-vehicle communication, making these interface devices indispensable.

Other Trends

Standardization and Compliance with AUTOSAR & IEEE 802.3

The push for standardization is reshaping the market as automotive manufacturers and suppliers prioritize compliance with IEEE 802.3 (100BASE-T1, 1000BASE-T1) and AUTOSAR specifications. These standards ensure interoperability and robustness in vehicle networking architectures, reducing development costs and improving system reliability. With leading players like NXP Semiconductors, Broadcom, and Texas Instruments introducing compliant solutions, the market is witnessing an acceleration in protocol harmonization. Moreover, regulatory bodies and industry consortia are actively working to enhance Ethernet’s scalability for next-gen vehicles, ensuring seamless integration with emerging technologies like Vehicle-to-Everything (V2X) communication.

Increased Adoption in Autonomous and Electric Vehicles

The rapid expansion of autonomous (L3-L5) and electric vehicle (EV) production is a major catalyst for market growth. These vehicles rely heavily on high-bandwidth networks to process real-time data from multiple sensors, cameras, and lidar systems. Automotive Ethernet interface devices, such as PHY transceivers and switches, play a crucial role in managing this data flow efficiently. Manufacturers are also emphasizing lightweight cabling solutions to reduce vehicle weight, enhancing the appeal of single-pair Ethernet (SPE) in EVs. With China and the U.S. leading in EV adoption, regional demand for these components is expected to surge, contributing significantly to market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

High Demand for Connected Vehicles Drives Strategic Competition Among Automotive Ethernet Leaders

The global Automotive Ethernet Interface Device Market features a dynamic competitive landscape where established semiconductor giants compete with specialized automotive solution providers. This segmentation reflects the dual nature of the market, where both traditional automotive suppliers and telecom/networking companies are converging to serve the growing demand for in-vehicle high-speed data networks.

Broadcom currently leads the market with its comprehensive portfolio of automotive Ethernet PHY chips and switches. The company’s dominance stems from early investments in automotive-grade Ethernet solutions and strategic partnerships with major automakers. Following closely is NXP Semiconductors, whose recent acquisition of Marvell’s automotive Ethernet business has significantly strengthened its position in advanced driver assistance systems (ADAS) and in-vehicle networking applications.

The landscape is further shaped by companies like Texas Instruments and Microchip Technology, which have leveraged their analog and mixed-signal expertise to develop cost-effective Ethernet interface solutions for mid-range vehicles. Meanwhile, test and measurement specialists such as Keysight Technologies and Rohde & Schwarz play a crucial role in validating Ethernet implementations, ensuring compliance with stringent automotive reliability standards.

Recent market developments indicate an increasing focus on multi-gigabit automotive Ethernet solutions. Companies are racing to develop chipsets supporting the emerging 2.5G, 5G and 10G BASE-T1 standards, which will be critical for next-generation connected and autonomous vehicles. This technological arms race is driving both innovation and consolidation across the industry.

List of Leading Automotive Ethernet Interface Device Companies

- Broadcom Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- Texas Instruments (U.S.)

- Microchip Technology (U.S.)

- Keysight Technologies (U.S.)

- Rohde & Schwarz (Germany)

- Spirent Communications (U.K.)

- Vector Informatik (Germany)

- TE Connectivity (Switzerland)

- Semtech Corporation (U.S.)

Segment Analysis:

By Type

Basic Communication Segment Leads Due to Widespread Adoption in ADAS and Infotainment Systems

The market is segmented based on type into:

- Basic Communication

- Protocol Conversion

By Application

Automobile Manufacturing Segment Dominates Market Due to Increasing Vehicle Electrification

The market is segmented based on application into:

- Automobile Manufacturing

- Aftermarket Services

- Automotive Testing & Validation

- Others

By Component

PHY Chips Lead the Market Due to Critical Role in Signal Transmission

The market is segmented based on component type into:

- Ethernet Switches

- PHY Chips

- Subtypes: 100BASE-T1, 1000BASE-T1, Others

- Gateways

- Connectors

By Vehicle Type

Passenger Vehicles Segment Dominates Due to Higher Technology Adoption Rates

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

Regional Analysis: Automotive Ethernet Interface Device Market

North America

North America dominates the Automotive Ethernet Interface Device market, with the United States accounting for the largest share, driven by robust automotive innovation and high adoption of advanced vehicle networking technologies. The region benefits from strong OEM partnerships with semiconductor leaders like Broadcom and Texas Instruments, ensuring rapid integration of high-speed Ethernet solutions into next-generation vehicles. Key factors fueling growth include stringent cybersecurity mandates for connected cars and substantial R&D investments in autonomous driving. The U.S. government’s push for V2X (vehicle-to-everything) communication standards further accelerates demand. However, premium pricing of Ethernet-enabled components remains a challenge for mass-market penetration.

Europe

Europe’s Automotive Ethernet Interface Device market is propelled by the region’s leadership in luxury and electric vehicle (EV) production. Germany, home to automakers like BMW and Mercedes-Benz, prioritizes high-bandwidth in-vehicle networks for infotainment and ADAS (Advanced Driver Assistance Systems). Compliance with EU’s GDPR for data security and the ISO/SAE 21434 cybersecurity standard shapes product development. Collaboration between automotive suppliers (e.g., NXP Semiconductors) and OEMs drives innovation, though fragmented regulations across member states occasionally slow standardization. The shift toward software-defined vehicles presents long-term opportunities for Ethernet interface providers.

Asia-Pacific

Asia-Pacific is the fastest-growing market, led by China, Japan, and South Korea. China’s booming EV sector and government initiatives for smart transportation (e.g., “Made in China 2025”) fuel demand. Local manufacturers favor cost-optimized Ethernet solutions while global players like Rohde & Schwarz and Vector Informatik expand testing infrastructure. Japan’s automotive giants leverage Ethernet for lightweight wiring in hybrid vehicles, whereas India’s price-sensitive market shows gradual uptake. Challenges include uneven adoption rates and intellectual property concerns, but the region’s manufacturing scale ensures long-term dominance.

South America

South America’s market is nascent, with Brazil and Argentina as focal points. Economic volatility and reliance on conventional vehicle architectures limit Ethernet adoption, though partnerships with global Tier-1 suppliers are increasing. Fleet modernization projects and emerging telematics applications offer niche opportunities. The lack of localized manufacturing for Ethernet components results in dependency on imports, inflating costs.

Middle East & Africa

The region shows slow but steady growth, driven by luxury vehicle sales in the UAE and Saudi Arabia. Infrastructure for connected vehicles remains underdeveloped, but smart city initiatives in Dubai and Riyadh signal future potential. Local players face hurdles such as limited technical expertise and low consumer awareness, though partnerships with European and Asian suppliers could bridge gaps.

Asia-Pacific: The Growth Epicenter

With a CAGR exceeding 8% (2024–2032), Asia-Pacific surpasses other regions due to its automotive production scale and technological partnerships. China’s State Council policies encourage domestic Ethernet chipset development, reducing reliance on foreign suppliers. Meanwhile, Southeast Asia’s expanding middle class drives demand for connected vehicles. Japanese automakers’ expertise in reliability engineering ensures Ethernet’s seamless integration, though tariff disputes occasionally disrupt supply chains.

Report Scope

This market research report provides a comprehensive analysis of the global Automotive Ethernet Interface Device market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 816 million in 2024 and is projected to reach USD 1264 million by 2032, growing at a CAGR of 6.5%.

- Segmentation Analysis: Detailed breakdown by product type (Basic Communication, Protocol Conversion), application (Automobile Manufacturing, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Keysight Technologies, Broadcom, NXP Semiconductors, Texas Instruments, and Microchip, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging standards (IEEE 802.3, AUTOSAR), high-speed communication protocols (100BASE-T1, 1000BASE-T1), and integration with automotive electronic systems.

- Market Drivers & Restraints: Evaluation of factors such as increasing vehicle connectivity demands, ADAS adoption, and challenges related to automotive-grade reliability requirements.

- Stakeholder Analysis: Strategic insights for automotive OEMs, component suppliers, and technology providers regarding the evolving ecosystem and business opportunities.

The research employs both primary and secondary methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Ethernet Interface Device Market?

-> Automotive Ethernet Interface Device Market was valued at 816 million in 2024 and is projected to reach US$ 1264 million by 2032, at a CAGR of 6.5% during the forecast period.

Which key companies operate in this market?

-> Key players include Keysight Technologies, Rohde & Schwarz, Broadcom, NXP Semiconductors, Texas Instruments, Microchip, and TE Connectivity.

What are the key growth drivers?

-> Growth is driven by increasing vehicle connectivity requirements, autonomous driving technologies, and adoption of high-bandwidth in-vehicle networks.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America and Europe lead in technology adoption and market share.

What are the emerging trends?

-> Emerging trends include multi-gigabit automotive Ethernet, cybersecurity solutions, and integration with vehicle-to-everything (V2X) communication.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...