Automotive Analog IC Market Insights

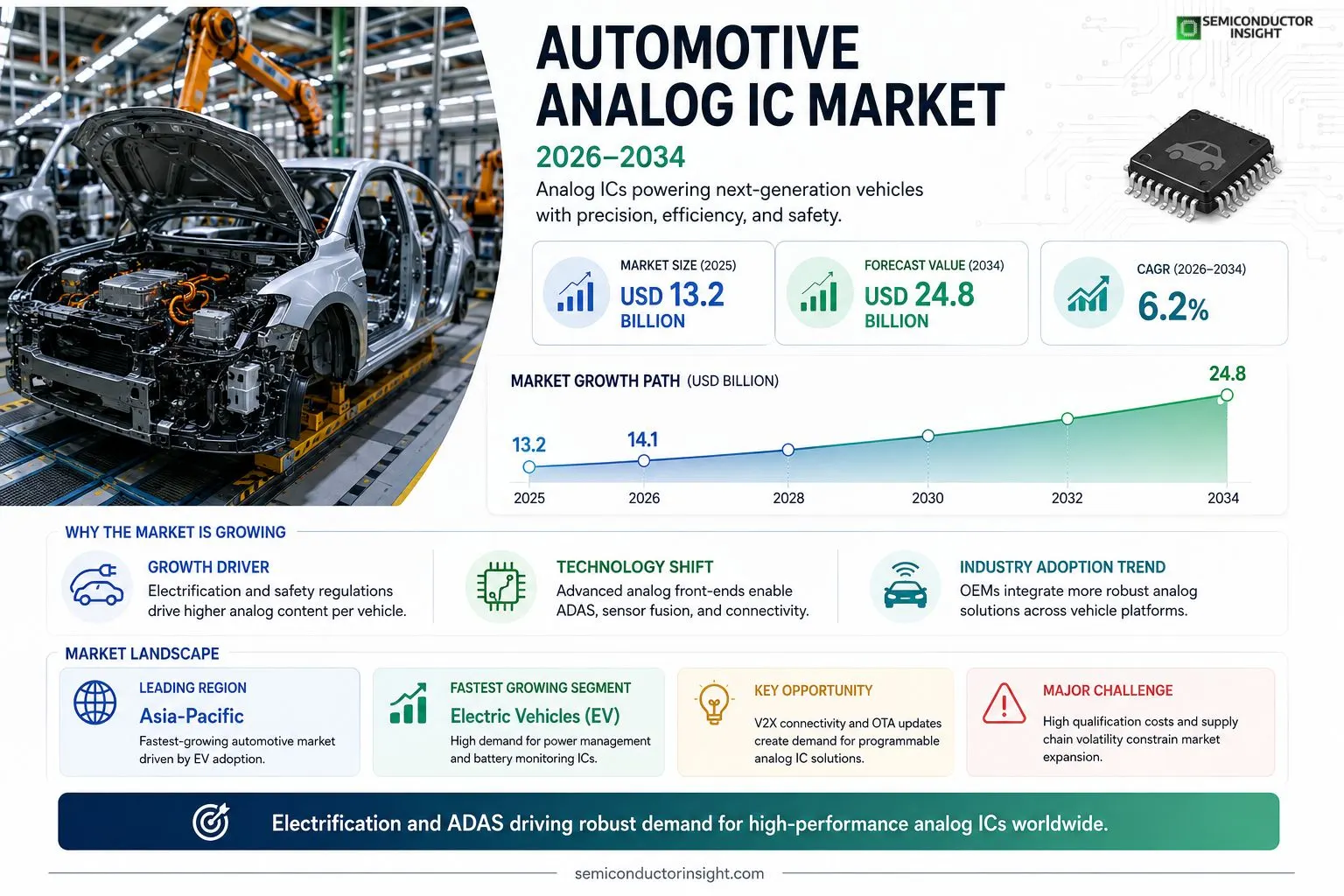

automotive analog IC market size was valued at USD 13.2 billion in 2025. The market is projected to grow from USD 14.1 billion in 2026 to USD 24.8 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period.

Automotive analog integrated circuits are semiconductor components that process continuous signals for vehicle systems such as power‑train control, infotainment, ADAS, and battery management. These ICs include voltage regulators, operational amplifiers, comparators, sensor interfaces, and signal‑conditioning devices that enable precise monitoring and actuation across harsh automotive environments.The market is experiencing rapid growth because electrification, autonomous‑driving functions, and stricter safety standards are driving higher demand for robust analog solutions. Furthermore, increasing vehicle connectivity and the shift toward electric powertrains are prompting OEMs to adopt more sophisticated analog front‑ends. Key players such as Texas Instruments, Infineon Technologies, NXP Semiconductors, and Renesas Electronics are expanding their portfolios through strategic acquisitions and advanced process technologies.

MARKET DRIVERS

Increasing Electrification of Vehicles

The rapid shift toward electric and hybrid powertrains is driving a significant rise in demand for high‑performance analog components that manage power distribution, sensor interfacing, and battery‑management functions within modern automobiles. Automotive Analog IC Market benefits from manufacturers integrating more sophisticated analog front‑ends to support regenerative braking and fast‑charging systems.

Stringent Emission and Safety Regulations

ly enforced emission standards and advanced safety mandates compel OEMs to deploy precise analog signal conditioning for air‑bag sensors, radar, and LiDAR modules. Compliance pressures thus stimulate the adoption of robust analog ICs that deliver low‑noise performance and high reliability under automotive temperature ranges.

➤ Analyst insight: The convergence of electrification and regulatory compliance is expected to double the analog IC content per vehicle within the next five years.

In addition, the proliferation of cabin‑level infotainment and driver‑assistance features creates new analog signal paths for audio, video, and touch interfaces, further expanding the scope of Automotive Analog IC Market across premium and mass‑market segments.

MARKET CHALLENGES

Supply Chain Volatility for Semiconductor Materials

Fluctuations in the availability of silicon wafers and specialized substrates lead to longer lead times and higher production costs for analog IC manufacturers, making it difficult to meet the aggressive launch schedules of automotive programs.

Other Challenges

Design Complexity

Advanced driver‑assistance systems (ADAS) require multi‑channel analog front‑ends that must be co‑designed with digital processors, increasing development cycles and validation requirements.

MARKET RESTRAINTS

High Qualification Costs

Automotive qualification processes such as AEC‑Q100 and ISO‑26262 demand extensive testing and documentation, inflating the upfront investment for analog IC suppliers. Smaller players often lack the resources to achieve these certifications, limiting market entry.

MARKET OPPORTUNITIES

Emerging Vehicle‑to‑Everything (V2X) Connectivity

The rollout of V2X communication systems creates demand for analog front‑ends that handle RF signal conditioning, power‑efficient transceiver interfaces, and precise timing control. Companies that can integrate these functions onto single‑chip solutions are positioned to capture a growing share of Automotive Analog IC Market.Additionally, the rise of over‑the‑air (OTA) updates for vehicle firmware encourages the development of programmable analog blocks, offering flexibility and reducing the need for hardware redesigns across model years.

Automotive Analog IC Market Trends

Rise of Electrified Powertrains

Automotive Analog IC Market is being reshaped by the rapid adoption of electric and hybrid propulsion systems. Analog front‑ends now handle higher voltage domains, regenerative‑brake energy flow, and precise battery‑state monitoring. Designers require voltage regulators and operational amplifiers that tolerate wider temperature ranges and sustain reliability over longer vehicle lifecycles. As OEMs standardize high‑voltage architectures, suppliers are consolidating their analog portfolios to provide integrated solutions that reduce board count and improve system efficiency. This shift fuels a steady increase in demand for robust analog components that support power‑train control while meeting automotive‑grade qualification standards.

Other Trends

Advanced Driver Assistance Systems (ADAS) Integration

ADAS functions such as adaptive cruise control, lane‑keeping assist, and collision detection rely on high‑precision sensor signal conditioning. Automotive Analog IC Market sees growing utilization of low‑noise amplifiers, comparators, and sensor‑interface circuits that translate radar, lidar, and camera outputs into clean, digitizable signals. Tight integration of these analog blocks with microcontroller units enables faster data processing and reduces latency, which is critical for safety‑critical decision making. Manufacturers are also embedding diagnostic features within analog ICs to facilitate predictive maintenance and comply with emerging safety regulations.

Increasing Connectivity and Sensor Fusion

Vehicle connectivity platforms demand analog front ends that can interface with a diverse set of communication protocols while preserving signal integrity. The trend toward sensor fusion,combining data from temperature, pressure, and motion sensors,requires analog ICs with flexible gain settings and programmable filtering. These capabilities help streamline the electrical architecture of connected cars, allowing continuous over‑the‑air updates and real‑time telemetry. As automotive networks become more complex, the analog segment of the market is focusing on scalable designs that support multi‑channel input and low‑power operation, ensuring that the overall vehicle system remains efficient and reliable.

COMPETITIVE LANDSCAPEKey Industry Players

Automotive Analog IC Market: Competitive Overview 2025‑2034

Automotive Analog IC Market is dominated by a handful of large semiconductor firms that leverage deep analog expertise and extensive automotive-grade process libraries. Texas Instruments remains a cornerstone player, supplying voltage regulators, op‑amps and sensor interfaces across almost every vehicle platform, while Infineon Technologies capitalizes on its power‑semiconductor heritage to deliver robust front‑end solutions for electrified power‑trains. NXP Semiconductor and Renesas Electronics complement these strengths with integrated mixed‑signal portfolios that address ADAS, infotainment and battery‑management requirements. These four companies command a combined market share exceeding 55 %, shaping product roadmaps through aggressive R&D investment and strategic acquisitions that broaden both performance envelopes and compliance capabilities for emerging safety standards.Beyond the tier‑one leaders, a diverse set of niche players adds depth and specialization to the ecosystem. Analog Devices focuses on high‑precision instrumentation amplifiers and data converters for sensor‑fusion tasks, whereas STMicroelectronics offers a broad analog front‑end suite tightly integrated with its microcontroller families. ON Semiconductor, Microchip Technology and Maxim Integrated (now part of Analog Devices) supply cost‑effective regulators and isolation devices for mass‑market models. Smaller yet influential contributors such as Skyworks Solutions, ROHM Semiconductor, Cypress Semiconductor (now part of Infineon), and Renesas’ rival, Nuvoton, deliver targeted solutions for connectivity, lighting and power‑stage applications, ensuring a competitive pressure that drives continuous innovation across the analog spectrum.

List of Key Automotive Analog IC Companies Profiled

- Texas Instruments

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Analog Devices

- STMicroelectronics

- ON Semiconductor

- Microchip Technology

- Maxim Integrated

- Skyworks Solutions

- ROHM Semiconductor

- Cypress Semiconductor

- Nuvoton Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Power‑Management ICs

|

| By Application |

|

Advanced Driver‑Assistance Systems (ADAS)

|

| By End User |

|

Original Equipment Manufacturers (OEMs)

|

| By Technology |

|

Integrated Mixed‑Signal Solutions

|

| By Vehicle Architecture |

|

Electric Vehicles (EV)

|

Regional Analysis: North America

North America

The demand for analog ICs in powertrain applications, encompassing engine control units (ECUs) and transmission control units (TCUs), remains substantial. Manufacturers are increasingly seeking analog components offering enhanced precision, temperature resilience, and power efficiency to optimize fuel economy and reduce emissions. The rise in hybrid and electric vehicle powertrains adds further complexity and opportunities for innovative analog solutions.

The expansion of Advanced Driver-Assistance Systems (ADAS), including features like adaptive cruise control, lane departure warning, and automatic emergency braking, is driving significant demand for automotive analog ICs. These systems rely heavily on analog components for sensor signal processing and data acquisition. Reliability and security are critical factors in this segment, leading to a focus on robust and tamper-resistant analog IC designs.

The growing integration of infotainment systems, connected car features, and advanced connectivity solutions is fueling demand for analog ICs used in audio processing, display interfaces, and communication modules. The increasing complexity of these systems necessitates higher-performance and power-efficient analog components to meet the evolving demands of consumers.

Analog ICs play a crucial role in body electronics, including lighting systems, door control modules, and comfort features. The increasing sophistication of these systems and the trend towards greater electrification are creating new opportunities for analog IC manufacturers. Enhanced reliability and integration capabilities are key considerations in this segment.

Europe

Europe represents a mature and highly regulated automotive market, with a strong emphasis on sustainability and technological innovation. The region is experiencing strong growth in electric vehicle adoption, which is translating into increased demand for automotive analog ICs supporting battery management, motor control, and charging infrastructure. European manufacturers are prioritizing energy efficiency and reducing carbon emissions, driving demand for analog solutions that optimize power consumption. The stringent safety regulations in Europe also necessitate advanced ADAS systems, further boosting the demand for specialized analog components. The integration of connected car technologies and the rise of autonomous driving are additional factors contributing to market growth. The European market is characterized by a high level of technological sophistication and a focus on quality and reliability. Companies operating in this region are actively investing in research and development to meet the evolving needs of the automotive industry.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing automotive market ly, driven by robust economic growth and increasing vehicle production, particularly in China and India. The region is witnessing a rapid shift towards electric vehicles, which presents significant opportunities for automotive analog IC manufacturers. The demand for ADAS systems is also growing rapidly in Asia-Pacific, fueled by increasing urbanization and stricter safety regulations. The region is characterized by a highly competitive market landscape with a mix of domestic and international players. Focus on cost optimization and localized supply chains are key strategies for success in this market. The growth of the automotive industry in Asia-Pacific is expected to continue in the coming years, driven by increasing disposable incomes and rising demand for personal transportation. Analog ICs are crucial for supporting the development of advanced automotive technologies in this dynamic region.

South America

South America’s automotive market is characterized by moderate growth, driven by increasing urbanization and rising disposable incomes. While the market is less mature than North America or Europe, it presents significant potential for automotive analog IC manufacturers. The region is seeing a gradual adoption of electric vehicles, with government initiatives promoting EV adoption. Demand for ADAS is slowly increasing, largely driven by higher-end vehicle segments. Cost sensitivity remains a key factor in this market, necessitating a focus on competitive pricing strategies. The automotive industry in South America is relatively concentrated in Brazil and Argentina, providing opportunities for regional partnerships and localized manufacturing. Analog ICs are essential for supporting the increasing complexity of vehicles sold in this region.

Middle East & Africa

The Middle East & Africa automotive market presents a mixed outlook, with varying growth rates across different countries. The region is witnessing increasing vehicle sales, driven by rising disposable incomes and government investments in infrastructure. The demand for automotive analog ICs is growing, particularly in countries like Saudi Arabia and the United Arab Emirates, where significant investments are being made in autonomous driving and connected vehicle technologies. The region faces challenges related to infrastructure development and economic instability, which can impact market growth. Analog components for power management and sensor systems are in high demand due to the region’s challenging climate conditions. As the automotive industry continues to evolve, so too will the demand for cutting-edge analog IC solutions in this dynamic region.

Report Scope

This market research report provides a comprehensive analysis of the Automotive Analog IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive Analog IC Market?

-> Automotive Analog IC Market was valued at USD 13.2 billion in 2025 and is expected to reach USD 24.8 billion by 2034.

Which key companies operate in Automotive Analog IC Market?

-> Key players include Texas Instruments, Infineon Technologies, NXP Semiconductors, and Renesas Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include electrification of vehicles, autonomous‑driving functions, stricter safety standards, increasing vehicle connectivity, and the shift toward electric powertrains.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include advanced analog front‑ends for AI/IoT integration, higher‑performance voltage regulators, and innovative semiconductor process technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...