AR/VR Optoelectronics Market Insights

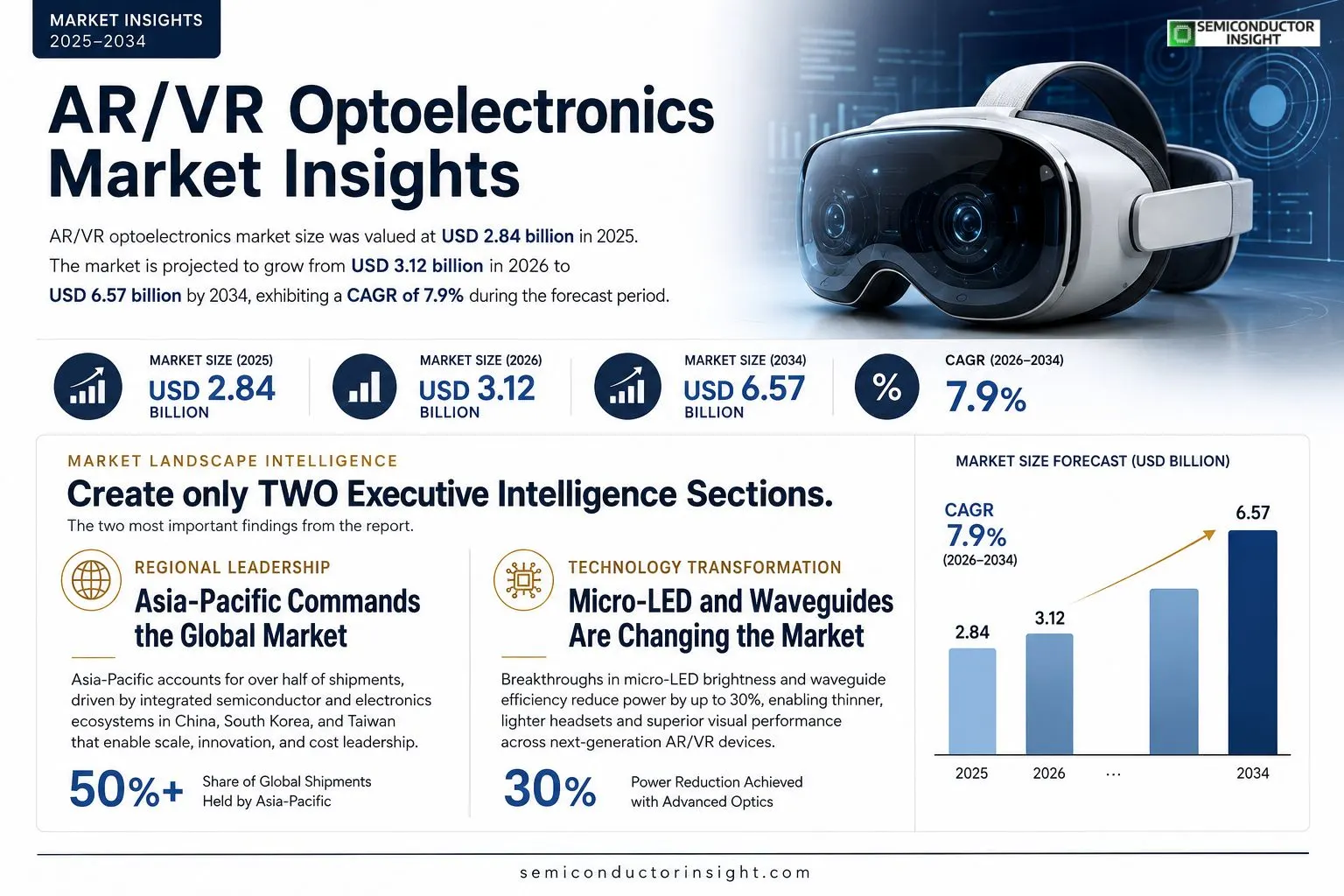

AR/VR Optoelectronics market size was valued at USD 2.84 billion in 2025. The market is projected to grow from USD 3.12 billion in 2026 to USD 6.57 billion by 2034, exhibiting a CAGR of 7.9% during the forecast period.

AR/VR optoelectronics comprise light‑emitting diodes, micro‑LED displays, waveguide modules, holographic optical elements, eye‑tracking sensors and related photonic components that enable immersive visual experiences in head‑mounted displays and mixed‑reality devices.The market is accelerating because of rising consumer demand for high‑resolution mixed‑reality headsets, expanding enterprise adoption of training simulators, and continuous cost reductions in semiconductor photonics. Furthermore, breakthroughs such as Meta’s partnership with Luxexcel on custom prescription lenses (2023) and Sony’s integration of next‑generation micro‑LED panels (2024) are driving component upgrades. Key players,including Apple, Samsung Electro‑Mechanics, Varjo and Lumentum,are investing heavily in R&D and strategic alliances to capture emerging opportunities. Asia‑Pacific accounts for over half of shipments due to dense manufacturing ecosystems in China, South Korea and Taiwan.

MARKET DRIVERS

Rising Demand for Immersive Experiences

AR/VR Optoelectronics Market is being propelled by a surge in consumer and enterprise demand for high‑fidelity immersive content. Worldwide shipments of mixed‑reality headsets reached roughly 15 million units in 2023, reflecting a 12% year‑over‑year growth driven by gaming, remote collaboration, and training applications.

Advancements in Micro‑LED and Waveguide Technologies

Recent breakthroughs in micro‑LED brightness and waveguide efficiency have reduced power consumption by up to 30%, enabling thinner form‑factors and longer battery life. These technical gains are attracting major OEMs and fostering a pipeline of next‑generation devices slated for release by 2025.

➤ Industry analysts project that the total addressable market for AR/VR optoelectronic components could exceed $12 billion by 2030.

Additionally, strategic partnerships between semiconductor firms and optics specialists are accelerating time‑to‑market for integrated solutions, further cementing growth momentum across multiple verticals.

MARKET CHALLENGES

High Development Costs and Regulatory Hurdles

Designing optoelectronic modules that meet stringent latency, resolution, and eye‑safety standards involves substantial R&D investment. For many mid‑size suppliers, the cost barrier exceeds $50 million, limiting scale‑up capabilities and slowing adoption in regulated sectors such as healthcare.

Other Challenges

Supply Chain Vulnerabilities

The reliance on rare‑earth phosphors and advanced lithography equipment creates exposure to geopolitical tensions, which can disrupt component availability and inflate prices by up to 18% during peak demand periods.

MARKET RESTRAINTS

Limited Battery Efficiency for Wearables

Current battery technologies struggle to support prolonged high‑brightness displays without frequent recharging. As a result, many consumer‑grade headsets are confined to session lengths of 45–60 minutes, curbing broader market penetration.

Fragmented Standards Landscape

The coexistence of multiple optical interface standards (e.g., HDMI, DisplayPort, proprietary waveguide protocols) hampers interoperability, forcing developers to design custom solutions that increase time‑to‑market and cost.

MARKET OPPORTUNITIES

Enterprise Training and Simulation

Corporations are increasingly investing in AR/VR training platforms to reduce onsite hazards and improve skill acquisition. The optoelectronics segment stands to gain from contracts worth an estimated $3 billion over the next five years as manufacturers supply high‑resolution, low‑latency displays for these applications.

Automotive Heads‑Up Displays (HUDs)

Automakers are integrating AR overlays into windshields to enhance driver awareness. Projection‑based HUDs require compact, high‑luminance optoelectronic components, presenting a growth avenue estimated at a 14% CAGR through 2032.

Emerging 5G‑Enabled Cloud Rendering

With 5G latency reductions, cloud‑rendered AR/VR experiences become viable, shifting the hardware focus toward lightweight optoelectronic modules. This transition opens opportunities for component manufacturers to supply cost‑effective, high‑bandwidth interfaces.

AR/VR Optoelectronics Market Trends

Rising Consumer Demand for High‑Resolution Mixed‑Reality Displays

AR/VR Optoelectronics Market is being driven by a surge in consumer appetite for head‑mounted displays that deliver true‑to‑life resolution and color fidelity. Advances in micro‑LED and waveguide technologies have lowered the price per pixel, allowing manufacturers to bundle larger, brighter panels into slimmer form factors. As a result, premium mixed‑reality headsets are gaining traction not only among early adopters but also among mainstream gamers and content creators. The reduction in semiconductor photonics cost, combined with improvements in eye‑tracking sensor accuracy, is shortening the gap between prototype and mass‑production cycles, reinforcing the market’s upward trajectory.

Other Trends

Enterprise Training Simulators and Industrial Adoption

Enterprise customers are leveraging AR/VR Optoelectronics Market components to build immersive training simulators for sectors such as aerospace, automotive, and healthcare. High‑definition holographic optical elements enable realistic depth cues, while fast‑response LEDs support low‑latency interactions essential for skill acquisition. Companies report higher retention rates and reduced material waste when replacing physical mock‑ups with virtual environments. This trend is amplified by regional incentives in Asia‑Pacific, where dense manufacturing ecosystems streamline component sourcing and integration, further accelerating deployment across large‑scale training programs.

Strategic Partnerships and Component Innovation

Strategic alliances are reshaping AR/VR Optoelectronics Market landscape. Notable collaborations, such as Meta’s partnership with Luxexcel for custom prescription lenses and Sony’s integration of next‑generation micro‑LED panels, illustrate how OEMs are co‑developing specialized photonic components to meet niche user requirements. Leading players,including Apple, Samsung Electro‑Mechanics, Varjo, and Lumentum,are expanding R&D budgets to pioneer waveguide miniaturization and eye‑tracking sensor miniaturization. In parallel, Asia‑Pacific accounts for more than half of shipments, driven by the region’s advanced wafer fabrication capacity and vertically integrated supply chains. These dynamics collectively foster a competitive environment that rewards rapid innovation and responsive manufacturing.

COMPETITIVE LANDSCAPEKey Industry Players

AR/VR Optoelectronics – Market Competitive Overview

AR/VR Optoelectronics Market is presently anchored by a handful of vertically integrated technology leaders that dominate both device fabrication and component supply chains. Apple leverages its control over custom micro‑LED displays and eye‑tracking sensors to set premium performance benchmarks, while Meta’s rapid scaling of prescription‑lens solutions through its partnership with Luxexcel reinforces its position in consumer head‑mounted displays. Sony’s integration of next‑generation micro‑LED panels and Samsung Electro‑Mechanics’ extensive production of high‑efficiency LEDs and waveguide modules create a duopolistic structure where scale, R&D intensity, and strategic alliances dictate market share. These incumbents benefit from deep semiconductor expertise, securing long‑term contracts with OEMs and influencing pricing dynamics across the value chain.Beyond the marquee names, a diverse set of niche innovators and specialized component manufacturers enrich the competitive landscape. Lumentum supplies high‑power laser sources for eye‑tracking and holographic optics, while Himax and Valeo focus on compact waveguide and diffraction‑grating technologies that enable slimmer form‑factors. Luxexcel continues to expand its custom prescription‑lens platform, and Varjo offers high‑resolution micro‑display modules for enterprise simulators. Asian players such as Goertek, BOE Technology, and Sharp provide cost‑effective micro‑LED and display solutions that fuel the rapid growth of the Asia‑Pacific shipment base. These firms, together with emerging photonics specialists like Sensity Systems and Photonfocus, create a vibrant ecosystem of specialized capabilities that challenge incumbents on innovation, cost, and niche market penetration.

List of Key AR/VR Optoelectronics Companies Profiled

- Apple

- Meta Platforms

- Samsung Electro‑Mechanics

- Sony Corporation

- Lumentum

- Himax Technologies

- Luxexcel

- Varjo

- Goertek

- BOE Technology Group

- Sharp Corporation

- Sensity Systems

- Photonfocus

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Micro‑LED Displays

|

| By Application |

|

Enterprise Training Simulators

|

| By End User |

|

Consumer Segment

|

| By Technology Integration |

|

Standalone Headsets

|

| By Component Functionality |

|

Display Modules

|

Regional Analysis: North America

North America

Significant progress in micro-LED displays and photonic integration is driving enhanced performance and reduced power consumption in AR/VR devices. These advancements are crucial for delivering immersive and comfortable user experiences.

Strategic alliances and mergers among key players are fostering innovation and accelerating the development and deployment of advanced AR/VR optoelectronics solutions. Collaboration is key to navigating the complex technological landscape.

The adoption of AR/VR in enterprise settings, including training, design, and remote collaboration, is creating substantial demand for high-quality optoelectronics components. Businesses are recognizing the transformative potential of this technology.

Continued investment in research and development by both private and public entities is essential for pushing the boundaries of AR/VR optoelectronics and unlocking new possibilities.

Europe

Europe exhibits a steady growth trajectory in AR/VR Optoelectronics Market, underpinned by strong industrial bases and supportive government policies. The automotive and industrial sectors are key drivers of demand, with applications in virtual prototyping, augmented maintenance, and enhanced driver assistance systems. Furthermore, Europe’s focus on sustainable technologies aligns with the energy efficiency benefits offered by advancements in optoelectronics. The region is witnessing increasing collaboration between research institutions and industry players, fostering innovation and accelerating market adoption.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in AR/VR Optoelectronics Market. Driven by burgeoning consumer electronics industries in countries like China and Japan, the demand for advanced display technologies and optical components is surging. The increasing penetration of 5G and the growing popularity of gaming and entertainment applications are further fueling this growth. Government initiatives promoting technological self-sufficiency and investment in digital infrastructure are also contributing to the region’s market expansion. The competitive landscape in Asia-Pacific is intense, with numerous domestic and international players vying for market share.

South America

South America presents a nascent but promising market for AR/VR optoelectronics. The adoption of AR/VR technologies is gradually gaining traction in sectors such as education, healthcare, and retail. While the market size is currently smaller compared to other regions, the potential for growth is significant, particularly with increasing internet penetration and smartphone adoption. Economic development and government investments in technology are expected to drive further market expansion in the coming years.

Middle East & Africa

The Middle East and Africa represent emerging markets with significant growth potential for AR/VR optoelectronics. The region’s growing focus on smart cities, industrial automation, and entertainment is creating demand for advanced AR/VR solutions. Government initiatives promoting technological diversification and investment in infrastructure are also contributing to market growth. While challenges remain in terms of market fragmentation and limited awareness, the long-term outlook for AR/VR optoelectronics in this region is positive.

Report Scope

This market research report provides a comprehensive analysis of the AR/VR Optoelectronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AR/VR Optoelectronics Market?

-> AR/VR Optoelectronics Market was valued at USD 2.84 billion in 2025 and is expected to reach USD 6.57 billion by 2034, with a projected value of USD 3.12 billion in 2026.

Which key companies operate in AR/VR Optoelectronics Market?

-> Key players include Apple, Samsung Electro‑Mechanics, Varjo, and Lumentum, among others.

What are the key growth drivers?

-> Key growth drivers include rising consumer demand for high‑resolution mixed‑reality headsets, expanding enterprise adoption of training simulators, and continuous cost reductions in semiconductor photonics.

Which region dominates the market?

-> Asia‑Pacific accounts for over half of shipments, making it the dominant and fastest‑growing region.

What are the emerging trends?

-> Emerging trends include custom prescription lenses through partnerships such as Meta‑Luxexcel and next‑generation micro‑LED panel integration exemplified by Sony.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...