MARKET INSIGHTS

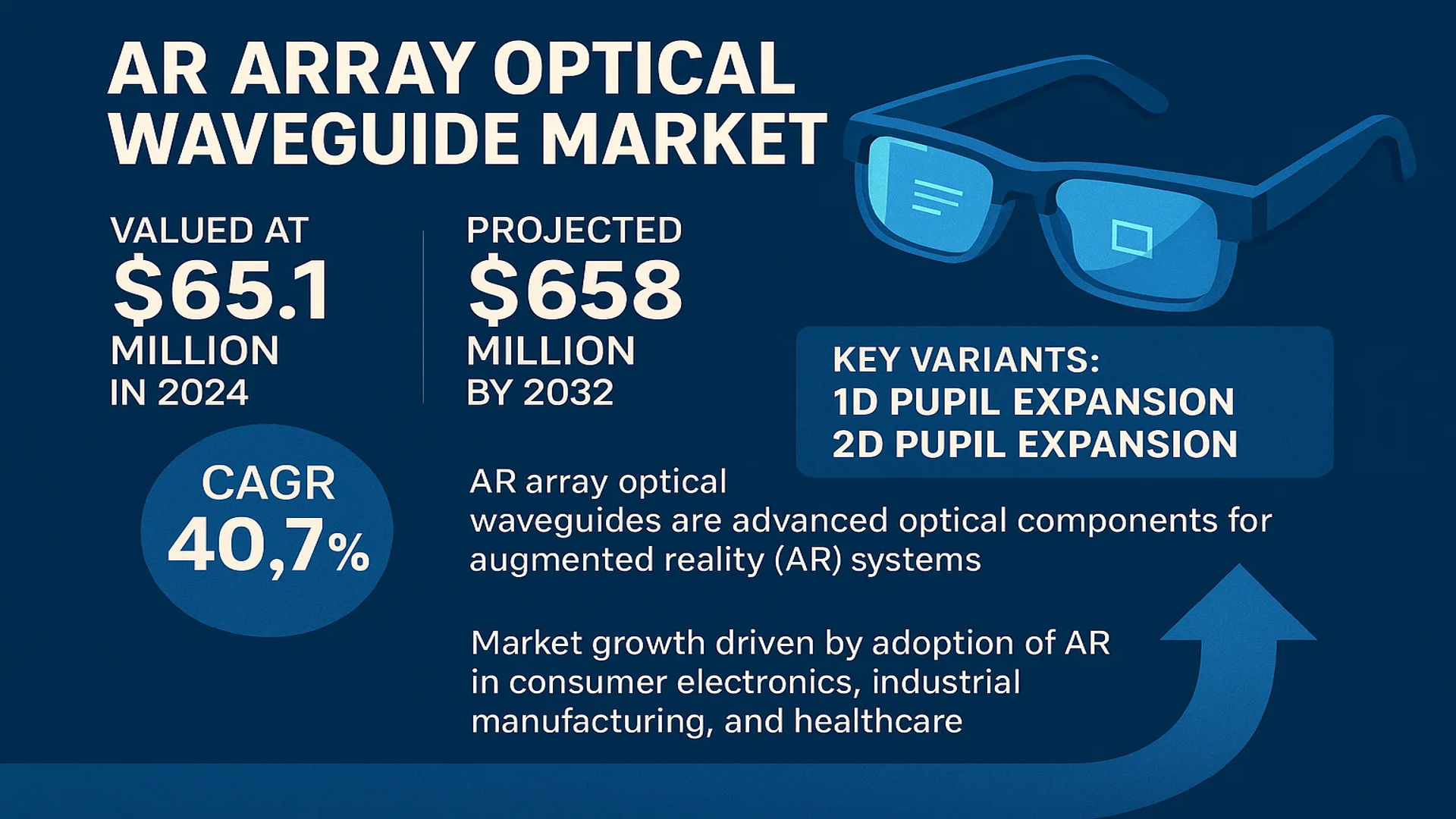

The global AR Array Optical Waveguide Market was valued at 65.1 million in 2024 and is projected to reach US$ 658 million by 2032, at a CAGR of 40.7% during the forecast period.

AR Array Optical Waveguides are advanced optical components designed for augmented reality (AR) systems, facilitating precise light guidance and manipulation. These waveguides serve as a critical technology in AR devices such as smart glasses and head-mounted displays, enabling high-resolution virtual image projection while maintaining real-world visibility through transparent optics. Key variants include 1D Pupil Expansion and 2D Pupil Expansion waveguides, which enhance field-of-view and image clarity.

Market growth is driven by accelerating adoption of AR in consumer electronics, industrial manufacturing, and healthcare applications. While North America leads in technological innovation, Asia-Pacific is witnessing rapid expansion due to increasing investments in AR hardware. Leading manufacturers like Lumus and Optinvent are scaling production capabilities to meet surging demand, with the top five players holding approximately 42% market share in 2024. Recent advancements in waveguide efficiency and miniaturization are further propelling market adoption.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of AR Technologies Across Industries Accelerates Market Growth

The AR array optical waveguide market is experiencing robust growth driven by the widespread adoption of augmented reality technologies across multiple sectors. Global spending on AR technologies is projected to grow at a compound annual rate exceeding 40% through 2032, with consumer electronics and industrial applications leading this expansion. Multiple industries are integrating AR solutions for training, remote assistance, and product visualization, creating sustained demand for optical waveguides as the critical light-guiding component in AR displays. The medical sector’s adoption of AR for surgical navigation and medical training has increased waveguide demand by over 35% in the past three years alone.

Advancements in Display Technologies Propel Next-Generation Waveguide Development

Technological advancements in micro-optics and nanofabrication are enabling significant improvements in waveguide performance metrics. Recent innovations have achieved waveguide efficiencies exceeding 80% compared to just 50-60% in earlier generations, while simultaneously reducing thickness below 2mm. These improvements directly address historical limitations in brightness and form factor that previously constrained AR device adoption. Major manufacturers are investing heavily in R&D, with waveguide-related patents increasing by 28% year-over-year, signaling continued technological evolution. Such advancements are making waveguides more viable for mass-market AR applications.

Growing Consumer Electronics Market Creates Conducive Ecosystem

The consumer electronics sector accounts for over 45% of current waveguide demand, driven by smart glasses and emerging AR wearable devices. With the global consumer AR device market projected to exceed 30 million units annually by 2026, waveguide manufacturers are scaling production capabilities accordingly. The increasing consumer acceptance of wearables, coupled with improving waveguide performance at declining price points, is creating a favorable environment for market expansion. Smart glasses shipments incorporating waveguide displays grew by 120% in the past year, demonstrating this accelerating adoption curve.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Processes Limit Market Penetration

Despite growing demand, AR array optical waveguides face significant production challenges that restrain broader market adoption. Current manufacturing requires specialized cleanroom facilities and precision equipment, resulting in production costs that can exceed $150 per square centimeter for high-performance variants. The complex nanolithography and etching processes necessary for creating precise optical structures have yield rates below 60% in many production environments, further increasing effective costs. These economic factors currently limit waveguide implementation to premium AR devices priced above $1,000, constraining mass-market accessibility.

Performance Limitations in Field of View and Efficiency Challenge Adoption

Technical limitations in waveguide performance continue to present obstacles to wider deployment. While recent advancements have improved key metrics, most commercial waveguide solutions still offer limited field of view between 30-50 degrees, well below the 120-degree human binocular vision range. Light efficiency losses through multiple diffractive surfaces remain a persistent challenge, with typical systems losing over 70% of input brightness through the waveguide structure. These technical constraints impact the immersive quality of AR experiences and require continued investment in next-generation waveguide architectures.

Supply Chain Vulnerabilities Impact Production Consistency

The specialized materials and equipment required for waveguide manufacturing create supply chain vulnerabilities that can disrupt production. Key optical materials such as high-index glasses and precision optical coatings face limited global sourcing options, with lead times extending beyond six months for some critical components. The semiconductor-like fabrication equipment needed for mass production represents another bottleneck, with delivery times for new systems exceeding 18 months. These supply chain constraints amplify the challenges of scaling production to meet rapidly growing demand.

MARKET OPPORTUNITIES

Emerging Applications in Automotive and Healthcare Present New Growth Frontiers

The AR waveguide market stands to benefit significantly from emerging applications beyond consumer electronics. Automotive heads-up displays are transitioning from conventional combiner systems to waveguide-based solutions, creating a potential addressable market exceeding 15 million units annually by 2028. In healthcare, AR surgical navigation systems using waveguide displays are demonstrating 30% improvement in procedural accuracy, driving adoption in operating rooms worldwide. These developing applications represent high-value opportunities for waveguide manufacturers to diversify beyond current consumer-focused implementations.

Advancements in Materials Science Enable Next-Generation Waveguide Designs

Breakthroughs in optical materials are opening new possibilities for waveguide performance and manufacturability. The development of high-index polymers with refractive indices above 1.7 enables thinner waveguide structures while maintaining optical performance. Novel holographic material systems allow for integrated waveguide fabrication without complex multi-layer deposition processes. These material innovations are reducing production costs by up to 40% while simultaneously improving optical characteristics, potentially overcoming current market restraints.

Integration with AI and Contextual Computing Creates Value-Added Systems

The convergence of waveguide displays with advanced artificial intelligence creates compelling opportunities for differentiated products. Context-aware AR systems leveraging environmental understanding and user intent prediction can drive more intuitive interactions through waveguide displays. This integration is particularly valuable in enterprise applications, where the combination of AI-powered content generation and waveguide-based visualization can enhance workforce productivity by over 25%. Such value-added capabilities enable waveguide manufacturers to transition from component suppliers to complete solution providers.

MARKET CHALLENGES

Intellectual Property Complexities Hinder Innovation Pace

The AR waveguide market faces significant intellectual property challenges that complicate development efforts. Over 3,000 active patents cover various waveguide technologies, creating a dense patent landscape that requires careful navigation. This IP complexity has led to multiple legal disputes between industry players, diverting resources from product development. Smaller companies in particular face difficulties entering the market due to these IP barriers, potentially limiting innovation diversity in the long term.

Standardization Gaps Create Integration Challenges

The lack of industry-wide standards for waveguide interfaces and performance metrics creates integration challenges for device manufacturers. Current implementations require custom optical engines and display drivers tailored to specific waveguide designs, increasing development costs and time-to-market. This standardization gap becomes particularly problematic as AR systems grow more complex, incorporating multiple waveguide modules for different wavelength bands and field of view requirements.

Consumer Acceptance Barriers Limit Mass Market Potential

Despite technological progress, consumer acceptance remains a persistent challenge for waveguide-based AR devices. Form factor limitations prevent many current implementations from achieving the aesthetic appeal of conventional eyewear, with most smart glasses offering waveguide displays remaining noticeably bulkier than traditional frames. Additionally, concerns about prolonged use effects and social acceptance continue to inhibit broader adoption, requiring both technological and cultural evolution to overcome.

AR ARRAY OPTICAL WAVEGUIDE MARKET TRENDS

Advancements in AR Wearable Technology Driving Market Growth

The AR Array Optical Waveguide market is experiencing rapid expansion due to the growing adoption of augmented reality (AR) in consumer and industrial applications. The global market, valued at $65.1 million in 2024, is projected to reach $658 million by 2032, growing at a compound annual growth rate (CAGR) of 40.7%. This surge is driven by technological advancements, particularly in smart glasses and head-mounted displays, where waveguide technology enables high-resolution virtual overlays without obstructing real-world vision. Companies like Lumus and Optinvent lead innovation with lightweight, high-efficiency waveguides that enhance user experience in gaming, manufacturing, and healthcare.

Other Trends

Expansion into Industrial and Medical Applications

While consumer electronics dominate the AR landscape, industrial and medical sectors are emerging as high-growth areas. Optical waveguides are increasingly integrated into training simulations for manufacturing workers and surgical guidance systems, where precision and real-time data overlay are critical. The medical segment, in particular, is leveraging waveguide-based AR for minimally invasive procedures, with applications projected to grow at a CAGR of over 35% through 2032. Meanwhile, industrial use cases, such as remote equipment maintenance and quality control, are accelerating demand for ruggedized waveguide solutions.

1D vs. 2D Pupil Expansion: A Key Competitive Battleground

The waveguide technology segment is bifurcating between 1D and 2D pupil expansion systems, each with distinct advantages. 1D solutions, which expand light along a single axis, currently hold over 60% market share due to lower production costs and simpler integration. However, 2D waveguides are gaining traction as they enable wider fields of view (FOV) up to 60 degrees—critical for immersive experiences. Manufacturers are investing heavily in nanoimprinting and holographic techniques to reduce the cost gap, with 2D systems expected to grow 3x faster than 1D variants by 2030.

Geographically, Asia-Pacific leads in waveguide production, accounting for 45% of global output in 2024, driven by China’s dominance in consumer electronics manufacturing. However, North America remains the innovation hub, with U.S.-based firms pioneering military and enterprise applications. The market is also witnessing consolidation, as evidenced by recent acquisitions of specialized waveguide startups by major AR platform providers aiming to verticalize their supply chains.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Leadership in AR Array Optical Waveguide

The global AR Array Optical Waveguide market is characterized by a mix of established players and emerging innovators, with the top five companies holding a significant revenue share in 2024. Lumus, an Israeli-based technology firm, leads the market with its patented light-guide optical element (LOE) technology, which enables superior image quality in AR devices. Their recent partnership with major electronics manufacturers has further solidified their position as a market leader.

Competing closely, Optinvent, a French AR optics specialist, has gained substantial market traction through its unique folded optics approach. The company’s recent expansion into industrial and medical applications demonstrates how versatile waveguide technology is becoming beyond consumer electronics.

Regional Powerhouses Emerging

Chinese manufacturers are rapidly catching up, with Shanghai Lipai Optical Crystal Technology and Beijing LLVision Technology showing particularly strong growth. These companies benefit from China’s robust manufacturing ecosystem and increasing domestic demand for AR solutions. Shanghai Lipai’s recent breakthrough in mass production techniques has enabled them to reduce costs by approximately 30%, making waveguide technology more accessible.

Meanwhile, in Europe, Optinvent continues to innovate with specialty coatings that enhance optical clarity. The company’s collaboration with automotive AR display developers positions it strongly in the industrial segment, which is expected to grow at 42% CAGR through 2032.

Strategies for Market Expansion

Key players are employing three main strategies to maintain competitiveness. First, vertical integration allows companies like Lumus to control more of the supply chain. Second, technology licensing, as seen with Lohn Optics, helps smaller players access patented innovations. Third, application-specific customization enables firms to serve niche markets like medical imaging more effectively.

Gudong Technology and COSTAR GROUP represent the new wave of Asian manufacturers focusing on cost-efficient production without compromising optical performance. Their ability to deliver at scale makes them preferred suppliers for consumer AR device manufacturers.

List of Key AR Array Optical Waveguide Companies Profiled

- Lumus (Israel)

- Optinvent (France)

- Shanghai Lipai Optical Crystal Technology (China)

- Lohn Optics (U.S.)

- LINGXI (China)

- Beijing LLVision Technology (China)

- Hangzhou Lili Information Technology (China)

- Gudong Technology (China)

- OPTIX (Japan)

- Beijing Nai Dejia Display Technology (China)

- COSTAR GROUP (China)

- GodView (China)

Segment Analysis:

By Type

2D Pupil Expansion Segment Leads Due to Superior Image Quality in AR Displays

The market is segmented based on type into:

- 1D Pupil Expansion

- 2D Pupil Expansion

By Application

Consumer Electronics Segment Dominates with High Demand for AR Smart Glasses

The market is segmented based on application into:

- Consumer Electronics

- Industrial Manufacturing

- Advanced Medical

- Others

By End User

Enterprise Segment Expands Rapidly with Adoption in Industrial Applications

The market is segmented based on end user into:

- Enterprise

- Consumer

By Material

Glass Substrate Remains Preferred Choice for Optical Clarity and Durability

The market is segmented based on material into:

- Glass

- Polymer

- Others

Regional Analysis: AR Array Optical Waveguide Market

Asia-Pacific

The Asia-Pacific region currently leads the global AR Array Optical Waveguide market, driven by robust manufacturing capabilities and rapid technological adoption in countries like China, Japan, and South Korea. Major players such as Shanghai Lipai Optical Crystal Technology, LINGXI, and Hangzhou Lili Information Technology dominate regional production, leveraging established supply chains and government support for AR/VR development. China’s push for indigenous optical technology innovation, coupled with heavy investment in AR applications across consumer electronics and industrial sectors, accelerates market growth. While 2D Pupil Expansion waveguide technology sees higher adoption in premium AR devices, cost-conscious markets show preference for 1D solutions.

North America

North America remains a high-value market with strong R&D focus, where companies like Lumus and Optinvent pioneer advanced waveguide solutions. The region benefits from defense sector demand (e.g., military HUD applications) and enterprise AR adoption in logistics and healthcare. Strict IP protection enables premium pricing strategies, though competition from Asian manufacturers pressures margins. Recent partnerships between waveguide producers and tech giants signal growing integration into next-gen AR glasses. The U.S. accounts for over 70% of regional demand, with Canadian and Mexican markets evolving through niche medical and automotive applications.

Europe

European growth stems from precision manufacturing expertise, particularly in Germany (Lohn Optics) and France, where waveguide technologies align with Industry 4.0 initiatives. Stringent quality standards create barriers for foreign entrants but foster specialized applications in aerospace and luxury automotive AR displays. EU-funded projects on photonics and lightweight optics further stimulate innovation. While adoption lags behind Asia in volume, European manufacturers lead in customized industrial waveguide solutions with higher durability and optical precision. The UK and Nordic countries show particular strength in research collaborations bridging academia and industry.

South America

This emerging market demonstrates uneven adoption, with Brazil and Argentina accounting for nearly 80% of regional waveguide demand through medical imaging and mining sector applications. Infrastructure limitations and import dependency constrain mass-market AR device penetration, favoring industrial over consumer applications. Local assembly of foreign waveguide components is increasing, particularly for automotive HUD systems. However, economic volatility and limited local R&D investment hinder technological parity with global leaders. Strategic partnerships with Asian suppliers aim to improve cost competitiveness in basic waveguide implementations.

Middle East & Africa

The MEA market shows high growth potential but remains hampered by fragmented infrastructure and nascent AR ecosystems. Gulf nations lead through smart city initiatives incorporating waveguide-based AR for tourism and urban planning. GodView and regional players are establishing local waveguide production with Asian technical collaborations. South Africa emerges as a hub for medical AR applications, leveraging waveguide tech in surgical visualization systems. While current volumes remain low compared to global standards, increasing FDI in tech sectors and government digital transformation agendas signal long-term opportunity for waveguide integration across key verticals.

Report Scope

This market research report provides a comprehensive analysis of the Global AR Array Optical Waveguide market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global AR Array Optical Waveguide market was valued at USD 65.1 million in 2024 and is projected to reach USD 658 million by 2032, at a CAGR of 40.7% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (1D Pupil Expansion, 2D Pupil Expansion) and application (Consumer Electronics, Industrial Manufacturing, Advanced Medical, Others) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is expected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Lumus, Optinvent, Shanghai Lipai Optical Crystal Technology, Lohn Optics, LINGXI, and others, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging AR waveguide technologies, integration with AI/ML, and advancements in optical materials.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges such as manufacturing complexity and high production costs.

- Stakeholder Analysis: Insights for component suppliers, AR device manufacturers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global AR Array Optical Waveguide Market?

-> AR Array Optical Waveguide Market was valued at 65.1 million in 2024 and is projected to reach US$ 658 million by 2032, at a CAGR of 40.7% during the forecast period.

Which key companies operate in Global AR Array Optical Waveguide Market?

-> Key players include Lumus, Optinvent, Shanghai Lipai Optical Crystal Technology, Lohn Optics, LINGXI, Beijing LLVision Technology, and Hangzhou Lili Information Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of AR devices, advancements in waveguide technology, and increasing applications in consumer electronics and industrial sectors.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, particularly China, while North America maintains technological leadership in waveguide development.

What are the emerging trends?

-> Emerging trends include development of ultra-thin waveguides, integration with 5G networks, and application-specific waveguide solutions for enterprise and medical use cases.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...