Analog & Power Wafer Foundry Market Insights

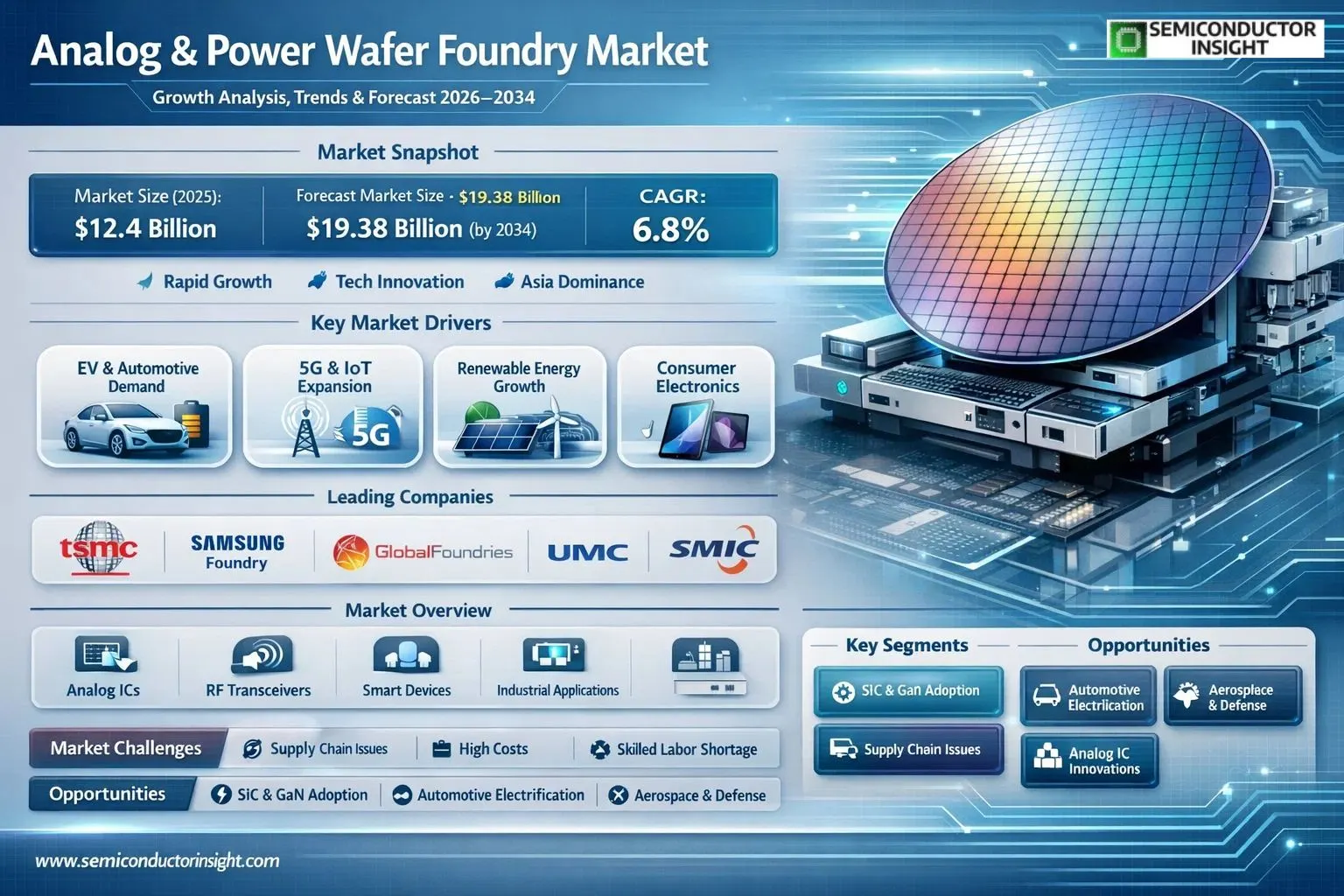

Global Analog & Power Wafer Foundry market size was valued at USD 12.4 billion in 2025. The market is projected to grow from USD 13.2 billion in 2026 to USD 19.38 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

Analog & Power Wafer Foundries are specialized semiconductor manufacturing facilities that produce analog and power integrated circuits (ICs) on silicon wafers for fabless companies and integrated device manufacturers (IDMs). These foundries are critical for fabricating chips that manage real-world signals like sound, temperature, and power, encompassing a wide range of components such as Power Management ICs (PMICs), data converters, amplifiers, and radio frequency (RF) transceivers. Their performance is fundamental to the functionality of end systems in applications ranging from smartphones and automotive systems to industrial equipment and IoT devices.

The market is experiencing steady growth driven by several key factors, including the proliferation of electric vehicles, which require sophisticated power management systems, and the exponential expansion of the 5G infrastructure and IoT ecosystems, which demand a vast quantity of analog and RF chips. Furthermore, the increasing complexity of consumer electronics and a strategic shift by major IDMs toward a fab-lite or fabless model are creating significant outsourcing opportunities for foundries. Recent developments, such as the acquisition of Tower Semiconductor by Intel Foundry Services, highlight the intense strategic focus and consolidation within this sector to capture this growing demand. Key players that dominate this fragmented but vital market include TSMC, GlobalFoundries, United Microelectronics Corporation (UMC), and SMIC.

MARKET DRIVERS

Rising Demand in Electric Vehicles and Automotive Sector

Analog & Power Wafer Foundry Market is propelled by the surge in electric vehicle (EV) adoption, where efficient power management solutions are critical. Analog and power semiconductors handle high-voltage requirements for battery systems and inverters, with global EV sales projected to reach 17 million units by 2028, driving foundry capacity expansions.

Expansion in Renewable Energy and Industrial Applications

Renewable energy integration, including solar inverters and wind turbine controls, boosts demand for robust power wafers. The market benefits from industrial automation trends, where analog ICs ensure precise signal processing, contributing to a steady 8.5% annual growth in wafer fabrication needs.

➤ Analysts forecast Analog & Power Wafer Foundry Market to expand at a 9.2% CAGR through 2030, fueled by electrification trends.

Additionally, 5G infrastructure and IoT devices rely on specialized analog components for connectivity and sensing, further accelerating investments in dedicated foundry technologies.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Shortages

Geopolitical tensions and semiconductor shortages have disrupted Analog & Power Wafer Foundry Market, leading to delays in wafer production. Foundries face wafer fab utilization rates dropping to 75% in peak crisis periods, impacting delivery timelines for automotive and consumer electronics clients.

Other Challenges

Technological Complexity in Advanced Nodes

Shrinking process nodes for analog and power devices introduce yield challenges, with defect densities rising by 15-20% during transitions, straining R&D budgets and extending time-to-market.

Competition from integrated device manufacturers (IDMs) intensifies pressure on pure-play foundries, forcing continuous process improvements amid rising operational costs estimated at $10-15 billion for new 200mm facilities.

Skilled labor shortages in wafer processing further complicate scaling, with vacancy rates in engineering roles hovering around 12% globally.

MARKET RESTRAINTS

High Capital Expenditures and Cyclical Demand

Analog & Power Wafer Foundry Market is restrained by enormous upfront investments, often exceeding $5 billion for state-of-the-art facilities focused on 150-300mm wafers tailored for power applications. These capex barriers limit new entrants and expansions.

Market cyclicality tied to automotive and consumer cycles results in volatile order books, with capacity utilization fluctuating between 65% and 95%, deterring long-term commitments.

Regulatory compliance for environmental standards in wafer fabrication adds ongoing costs, particularly for chemical handling and emissions control in analog power processes.

MARKET OPPORTUNITIES

Adoption of Wide Bandgap Materials like SiC and GaN

Shifting towards silicon carbide (SiC) and gallium nitride (GaN) wafers opens vast opportunities in Analog & Power Wafer Foundry Market, enabling higher efficiency in EVs and data centers. SiC adoption is expected to grow 25% annually, requiring specialized foundry capabilities.

Automotive electrification and AI-driven power management create demand for custom analog solutions, with foundries investing in 8-inch SiC lines projected to capture 30% market share by 2027.

Emerging applications in aerospace and defense further diversify revenue streams, as these sectors prioritize reliable power semiconductors amid global supply diversification efforts.

Analog & Power Wafer Foundry Market Trends

Rising Demand for 12-Inch Wafer Production

Analog & Power Wafer Foundry Market is experiencing a notable shift toward larger wafer sizes, particularly the 12-inch segment, which is gaining prominence due to enhanced production efficiency and cost advantages. This trend aligns with the increasing complexity of analog and power ICs used in power management and signal chain applications. Foundries are investing in 12-inch capabilities to meet the demands of high-volume manufacturing for consumer electronics, automotive systems, and telecommunications, where performance hinges on precise analog components like converters and RF transceivers.

Other Trends

Expansion in Power Management ICs Applications

Demand for Analog & Power Wafer Foundry services is surging in power management ICs (PMICs), driven by the proliferation of energy-efficient devices in smartphones, modems, and WiFi routers. These ICs optimize power delivery, enabling longer battery life and compact designs, which are critical in the fragmented analog market serving diverse customer needs across countless applications.

Regional Growth in Asia-Pacific

Asia, particularly China, Taiwan, Japan, and South Korea, dominates Analog & Power Wafer Foundry Market, fueled by robust semiconductor ecosystems and proximity to end-user industries. Local foundries are scaling operations to support regional demand in analog signal chain ICs, while North America and Europe focus on specialized high-performance nodes, fostering balanced global supply chains.

Intensifying Competition Among Key Players

Leading foundries such as TSMC, Samsung Foundry, GlobalFoundries, UMC, and SMIC are shaping Analog & Power Wafer Foundry Market through capacity expansions and technological innovations. The top players maintain significant revenue shares by specializing in mature processes for 8-inch and 6-inch wafers alongside advanced 12-inch lines. This competitive dynamic encourages mergers, acquisitions, and R&D in materials engineering, ensuring sustained market fragmentation and opportunities for niche providers like Tower Semiconductor and VIS. Overall, these trends underscore a resilient Analog & Power Wafer Foundry Market poised for steady evolution amid rising IC integration needs.

COMPETITIVE LANDSCAPE

Key Industry Players

Dominating Analog & Power Wafer Foundry Manufacturers and Strategic Market Positions

Analog & Power Wafer Foundry Market is led by a few dominant pure-play foundries that command significant market share through advanced process technologies and high-volume production capabilities. TSMC stands out as Global leader, leveraging its cutting-edge nodes and extensive analog/power IP portfolio to serve diverse applications like power management ICs and signal chain components. Samsung Foundry and GlobalFoundries follow closely, capturing substantial revenue portions with specialized Bipolar-CMOS-DMOS (BCD) processes tailored for automotive and industrial power devices. United Microelectronics Corporation (UMC) and SMIC round out the top five, collectively holding a major share of the fragmented market, which features hundreds of players but is increasingly consolidated around 12-inch wafer capacities projected to drive growth through 2034.

Beyond the frontrunners, a robust ecosystem of niche foundries excels in specialized analog and power technologies, catering to customized needs in RF transceivers, low-noise amplifiers, and converters for smartphones, modems, and WiFi systems. Companies like Tower Semiconductor, PSMC, and VIS (Vanguard International Semiconductor) differentiate through mature 8-inch and 6-inch platforms, enabling cost-effective production for mid-tier PMICs and analog signal chains. Emerging players such as Hua Hong Semiconductor, HLMC, X-FAB, and DB HiTek focus on high-voltage processes for power applications, while others including Nexchip, Intel Foundry Services, and Polar Semiconductor provide regional strengths in Asia and North America, fostering innovation amid challenges like supply chain dynamics and technological shifts.

List of Key Analog & Power Wafer Foundry Companies Profiled

- TSMC

- Samsung Foundry

- GlobalFoundries

- United Microelectronics Corporation (UMC)

- SMIC

- Tower Semiconductor

- PSMC

- VIS (Vanguard International Semiconductor)

- Hua Hong Semiconductor

- HLMC

- X-FAB

- DB HiTek

- Nexchip

- Intel Foundry Services (IFS)

- Polar Semiconductor, LLC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

12-inch Analog & Power Wafer Foundry

|

| By Application |

|

Power Management ICs (PMIC)

|

| By End User |

|

Consumer Electronics

|

| By Voltage Range |

|

Medium Voltage

|

| By Process Technology |

|

BCDMOS

|

Regional Analysis: Analog & Power Wafer Foundry Market

Asia-Pacific

Key fabrication centers in Taiwan and China lead wafer production for analog and power ICs, leveraging mature ecosystems for high-volume output. These hubs excel in 8-inch and 12-inch processes, optimizing for power density and thermal management critical to automotive and industrial sectors.

Prominent foundries drive Analog & Power Wafer Foundry Market with specialized capabilities in BCD and trench technologies. Strategic alliances with fabless firms enhance portfolio diversity, from low-voltage analog to high-power discretes.

Innovations in silicon carbide and gallium nitride processes elevate efficiency in power conversion. Advanced lithography and etching refine analog signal integrity, supporting next-gen applications in renewables and smart grids.

Surging adoption of EVs and data centers fuels demand for robust power wafers. Policy support and export incentives strengthen regional dominance in Analog & Power Wafer Foundry Market supply chain.

North America

North America plays a vital role in Analog & Power Wafer Foundry Market, emphasizing design innovation and niche high-performance fabrication. Home to leading fabless companies, the region relies on specialized foundry partnerships for prototyping advanced analog and power semiconductors. Focus areas include RF analog for telecommunications and wide-bandgap materials for aerospace applications. Robust intellectual property frameworks and R&D investments foster breakthroughs in mixed-signal integration. While domestic capacity is limited, strategic outsourcing to global partners ensures access to mature processes. Growing emphasis on supply chain resilience drives initiatives for localized wafer production, particularly for defense and medical sectors. Collaborative ecosystems between academia and industry accelerate commercialization of energy-efficient power devices, positioning North America as a hub for high-margin, customized solutions in Analog & Power Wafer Foundry Market.

Europe

Europe advances steadily in Analog & Power Wafer Foundry Market, prioritizing sustainability and automotive-grade semiconductors. Foundries here specialize in high-reliability power wafers for electric drivetrains and industrial automation. Stringent regulatory standards propel innovations in lead-free processes and eco-friendly fabrication. Regional strengths lie in compound semiconductors like silicon-on-insulator for precision analog sensing. Cross-border collaborations enhance process optimization, meeting demands from renewable energy inverters and smart manufacturing. Investments in digital twins and AI-driven yield management bolster competitiveness. As the push for carbon-neutral supply chains intensifies, Europe’s foundries integrate green manufacturing practices, securing a prominent position in Analog & Power Wafer Foundry Market through quality and compliance excellence.

South America

South America emerges as a growing contender in Analog & Power Wafer Foundry Market, driven by expanding electronics assembly and renewable projects. Limited local capacity leads to heavy reliance on imports, but initiatives in Brazil and Mexico aim to develop foundational wafer capabilities for power management in agrotech and solar applications. Cost-competitive labor and natural resources support backend processing, with gradual shifts toward front-end analog fabrication. Partnerships with Asian foundries transfer technology for basic power discretes. Rising urbanization boosts demand for efficient consumer power ICs, encouraging ecosystem maturation. South America’s strategic location facilitates nearshoring trends, enhancing its trajectory in Analog & Power Wafer Foundry Market amid global diversification efforts.

Middle East & Africa

The Middle East & Africa region shows potential in Analog & Power Wafer Foundry Market, leveraging energy sector demands for high-voltage power wafers in oil, gas, and desalination plants. Emerging hubs in the UAE and Israel focus on analog ICs for smart infrastructure and defense. Investments in fabrication facilities prioritize ruggedized devices for harsh environments. Technology transfers from established players build local expertise in power MOSFETs and analog drivers. Africa’s solar boom drives needs for cost-effective wafers, spurring public-private ventures. Geopolitical stability in key areas attracts foreign direct investment, positioning the region for expanded participation in Analog & Power Wafer Foundry Market through specialized, resilient solutions.

Report Scope

This market research report provides a comprehensive analysis of the Analog & Power Wafer Foundry Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Analog & Power Wafer Foundry Market?

-> Global Analog & Power Wafer Foundry market was valued at USD 12,400 million in 2025 and is expected to reach USD 19,380 million by 2034, at a CAGR of 6.8% during the forecast period.

Which key companies operate in Analog & Power Wafer Foundry Market?

-> Key players include TSMC, Samsung Foundry, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, among others.

What are the key growth drivers?

-> Key growth drivers include demand for analog chips in applications such as analog-to-digital converters, RF transceivers, modems, smartphones, and WiFi routers, along with market expansion and innovation opportunities in materials engineering.

Which region dominates the market?

-> Asia dominates the market, driven by key players in China, Taiwan, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include growth in 12-inch wafer technology, increasing adoption of Power Management ICs (PMIC) and Analog Signal Chain ICs, and continued fragmentation providing innovation in analog IC performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...