MARKET INSIGHTS

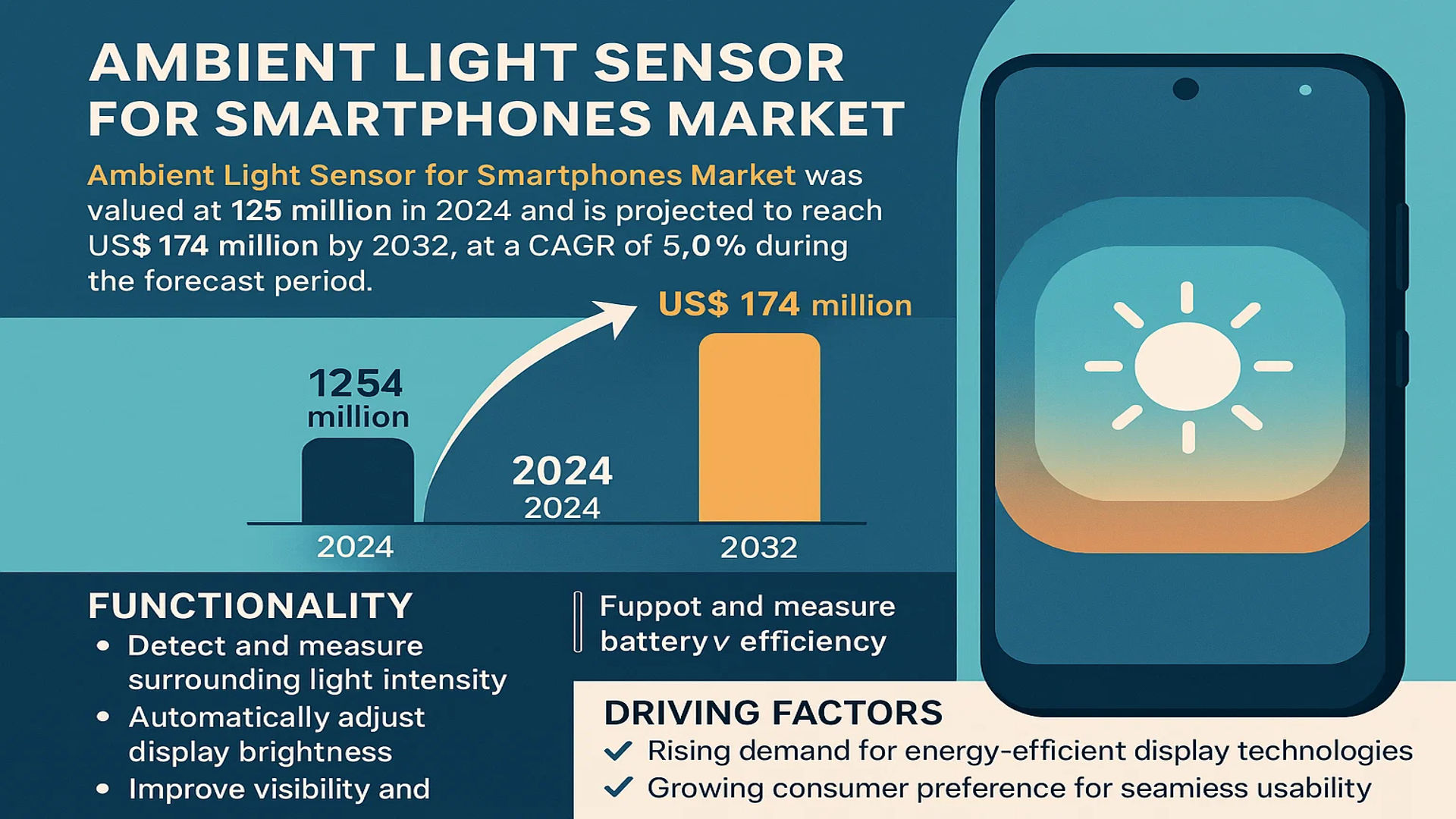

The global Ambient Light Sensor for Smartphones Market was valued at 125 million in 2024 and is projected to reach US$ 174 million by 2032, at a CAGR of 5.0% during the forecast period.

Ambient light sensors for smartphones are critical components that detect and measure the intensity of surrounding light to automatically adjust the device’s display brightness. These sensors enhance user experience by optimizing visibility in varying lighting conditions while improving battery efficiency. In bright environments, such as direct sunlight, the sensor increases screen brightness for readability, whereas in low-light settings, it dims the display to reduce power consumption and minimize eye strain. Modern smartphones increasingly integrate advanced ambient light sensors that support features like adaptive brightness and night mode, further driving their adoption.

The market is fueled by the rising demand for energy-efficient display technologies and the growing consumer preference for seamless usability. Leading manufacturers, including Sensortek, Broadcom, and STMicroelectronics, dominate the market with innovations in multi-functional sensors (e.g., 2-in-1 and 3-in-1 variants). The U.S. and China are key revenue contributors, with smartphone OEMs prioritizing sensor integration to differentiate products in a competitive landscape.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Energy-Efficient Smartphones to Propel Market Growth

The ambient light sensor market is experiencing robust growth due to increasing consumer demand for smartphones with superior battery efficiency. These sensors optimize display brightness based on environmental lighting conditions, significantly reducing power consumption. With smartphone users spending an average of 4-5 hours daily on their devices, manufacturers are prioritizing solutions that extend battery life. The integration of advanced ambient light sensors can reduce display power consumption by up to 30%, making them critical components in modern smartphone design. Leading manufacturers now consider these sensors essential for flagship devices, further accelerating market adoption.

Rising Adoption of AI-Powered Display Optimization to Drive Sensor Integration

Artificial intelligence is revolutionizing smartphone display management by leveraging ambient light sensor data for intelligent brightness adjustment. Modern sensors now incorporate machine learning algorithms that learn user preferences and environmental patterns to optimize display performance. This technology is particularly valuable for high-end smartphones where premium display quality is a key selling point. With over 90% of premium smartphones (priced above $800) now featuring advanced ambient light sensors, the technology is becoming a standard differentiator in competitive markets. The combination of hardware sensors with intelligent software is creating new growth opportunities for sensor manufacturers.

Increasing Smartphone Penetration in Emerging Markets to Expand Sensor Demand

Emerging markets are witnessing accelerated smartphone adoption, with annual growth rates exceeding 8% in regions like Southeast Asia and Africa. This expansion is driving demand for cost-optimized smartphone components, including ambient light sensors. Manufacturers are responding by developing value-engineered sensor solutions that maintain performance while meeting strict price targets for entry-level and mid-range devices. The proliferation of affordable smartphones featuring quality display technologies is making ambient light sensors accessible to broader consumer segments, significantly expanding the total addressable market for sensor providers.

MARKET RESTRAINTS

Cost Pressures in Competitive Smartphone Market to Constrain Sensor Implementation

While ambient light sensors offer significant benefits, their implementation in budget smartphones faces challenges due to intense price competition. Device manufacturers operating in price-sensitive segments often prioritize cost reduction over premium features, sometimes opting for basic sensor solutions or software-based alternatives. This price sensitivity is particularly pronounced in markets with average smartphone selling prices below $200, where component costs are scrutinized. Sensor manufacturers must balance performance with aggressive pricing strategies to remain competitive in these segments.

Technical Limitations in Extreme Lighting Conditions to Challenge Sensor Performance

Ambient light sensors can experience performance limitations in challenging lighting environments, affecting market adoption. Sudden light changes, mixed lighting conditions, and extreme brightness levels can impact sensor accuracy, potentially leading to suboptimal display adjustments. While high-end sensors incorporate advanced calibration and filtering technologies, these solutions increase component costs. The industry continues to face engineering challenges in developing cost-effective sensors that maintain precision across all lighting scenarios, from direct sunlight to dim indoor environments.

MARKET OPPORTUNITIES

Integration with Emerging Display Technologies to Create New Growth Avenues

The development of next-generation display technologies presents significant opportunities for ambient light sensor innovation. Foldable displays, micro-LED screens, and advanced OLED panels require sophisticated light management solutions to optimize power efficiency and viewing quality. Sensor manufacturers that can develop specialized solutions for these emerging display formats will gain first-mover advantages. The growing adoption of adaptive refresh rate technologies in premium smartphones further increases the importance of precise environmental light detection, creating additional integration opportunities for sensor providers.

Expansion of Multi-Function Sensor Solutions to Drive Market Growth

The trend toward sensor fusion presents significant growth potential for ambient light sensor providers. Combining light detection with proximity sensing, color temperature measurement, and other environmental monitoring functions allows for more comprehensive device optimization. Multi-function sensor packages are gaining traction in high-end smartphones, offering space savings and improved system efficiency. Manufacturers investing in integrated sensor solutions are well-positioned to capitalize on the growing demand for sophisticated environmental sensing in mobile devices.

MARKET CHALLENGES

Miniaturization Requirements to Pressure Sensor Design Teams

As smartphone designs become increasingly compact, ambient light sensor manufacturers face mounting pressure to reduce component sizes while maintaining or improving performance. The industry standard for sensor package size has decreased significantly in recent years, with leading manufacturers now offering solutions in packages smaller than 2mm × 2mm. This miniaturization trend presents engineering challenges related to light path optimization, signal-to-noise ratios, and thermal management. Design teams must balance size reduction with performance requirements, often requiring innovative optical designs and advanced packaging technologies.

Supply Chain Disruptions to Impact Sensor Availability

The ambient light sensor market remains vulnerable to global supply chain fluctuations affecting semiconductor components. Geopolitical tensions, material shortages, and manufacturing capacity constraints can disrupt sensor production and delivery timelines. These challenges are particularly acute for specialized optical materials and wafer-level packaging technologies essential for high-performance sensors. Manufacturers must develop resilient supply strategies to mitigate risks while maintaining quality standards and competitive pricing in this dynamic market environment.

AMBIENT LIGHT SENSOR FOR SMARTPHONES MARKET TRENDS

Increasing Demand for Energy-Efficient Smartphones to Drive Market Growth

The global market for ambient light sensors (ALS) in smartphones is experiencing steady growth, fueled by the rising consumer preference for energy-efficient devices. These sensors enable automatic brightness adjustments, which not only enhance user experience but also significantly reduce power consumption. Display brightness is one of the most power-intensive features in smartphones, and the integration of highly sensitive ALS modules has led to a 15-20% improvement in battery life on average. Furthermore, advancements in sensor technology, such as improved infrared (IR) rejection and dynamic response time, are optimizing performance in varying lighting conditions. The growing adoption of OLED and AMOLED displays, which inherently consume less power when brightness is regulated by ALS, further accelerates market expansion.

Other Trends

Expansion of AI-Powered Adaptive Display Technology

Artificial intelligence (AI) is playing a transformative role in enhancing ambient light sensor capabilities. Modern ALS solutions, integrated with machine learning algorithms, now deliver intelligent brightness control by analyzing user behavior, ambient light patterns, and contextual usage. These AI-driven systems go beyond standard threshold-based adjustments, offering smoother transitions that minimize eye strain while maintaining visual clarity. Several premium smartphone brands have already incorporated AI-powered ALS in flagship models, contributing to a 20-25% increase in user satisfaction metrics. As AI adoption continues to rise, sensor manufacturers are also focusing on hybrid solutions combining proximity, color, and ambient light sensing into compact multi-sensor modules.

Rising Smartphone Penetration in Emerging Markets

The rapid proliferation of smartphones in emerging economies is another key driver for the ALS market. Countries in Asia Pacific and Africa are witnessing a 12-15% annual growth in smartphone adoption, increasing the demand for cost-effective yet advanced sensing solutions. Local manufacturers are integrating ambient light sensors even in mid-range devices to offer premium features at competitive prices. Additionally, the shift toward bezel-less and punch-hole display designs necessitates smaller, more efficient sensor placements, pushing R&D investments toward miniaturized ALS components. Market leaders are also developing proprietary technologies to improve low-light sensing accuracy, addressing common challenges in regions with frequent power fluctuations.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Expand Innovations Amid Rising Smartphone Integration

The global ambient light sensor (ALS) market for smartphones remains moderately consolidated, with established semiconductor firms and specialized sensor manufacturers competing for market dominance. ams-OSRAM AG holds a strong position, leveraging its advanced photonics technology and deep partnerships with major smartphone brands, including Apple and Samsung. The company focuses on ultra-low-power sensor designs, a crucial factor as smartphone manufacturers demand greater energy efficiency.

STMicroelectronics follows closely, with its popular VL6180 proximity and ambient light sensor gaining traction in mid-range Android smartphones. The company benefits from its vertically integrated supply chain and emphasis on miniaturization, enabling sleeker smartphone designs without compromising performance. Meanwhile, Broadcom has strengthened its foothold through acquisitions and patents in light-sensing technologies, particularly for high-end smartphone displays.

Other key players, such as Sensortek and Rohm Semiconductor, are gaining recognition by offering cost-competitive solutions for emerging markets. Their multi-sensor modules (e.g., 3-in-1 ALS + proximity + IR sensors) address the growing demand for compact, multi-functional components in budget smartphones. These companies actively invest in R&D to improve accuracy in varied lighting conditions—a persistent industry challenge.

List of Key Ambient Light Sensor Manufacturers Profiled

- ams-OSRAM AG (Austria)

- STMicroelectronics (Switzerland)

- Broadcom Inc. (U.S.)

- Sensortek (Taiwan)

- SILICON LABS (U.S.)

- Vishay Intertechnology, Inc. (U.S.)

- Lite-On Technology (Taiwan)

- Everlight Electronics (Taiwan)

- Melexis (Belgium)

- Sharp Corporation (Japan)

Segment Analysis:

By Type

2-in-1 Sensors Lead the Market Due to Compact Design and Energy Efficiency

The market is segmented based on type into:

- 2-in-1 Sensors

- Features: Combines ambient light sensor (ALS) and proximity detection in a single module

- 3-in-1 Sensors

- Features: Integrates ALS, proximity detection, and gesture recognition

- Standalone Ambient Light Sensors

- Features: Dedicated light sensing for display brightness control

- Others

By Application

Android Smartphones Represent the Largest Application Segment

The market is segmented based on application into:

- iOS Smartphones

- Android Smartphones

- Includes devices from major brands like Samsung, Xiaomi, and Oppo

- Other Smartphone Platforms

By Technology

CMOS-Based Sensors Dominate the Market

The market is segmented based on technology into:

- CMOS-based Sensors

- CCD-based Sensors

- Others

By Sensing Range

Wide Range Sensors Gaining Market Share

The market is segmented based on sensing range into:

- Narrow Range (0-1000 lux)

- Medium Range (0-50,000 lux)

- Wide Range (0-100,000 lux)

Regional Analysis: Ambient Light Sensor for Smartphones Market

Asia-Pacific

The Asia-Pacific region dominates the global ambient light sensor (ALS) market for smartphones, driven by massive smartphone production hubs in China, South Korea, and Taiwan. China alone accounts for over 40% of global smartphone shipments, with brands like Xiaomi, OPPO, and Vivo integrating advanced ALS solutions to enhance user experience. The growing middle-class population and increasing adoption of premium smartphones are fueling demand for 3-in-1 sensors (combining ALS, proximity, and IR sensing). Local manufacturers like Sensortek and Lite-On Technology are capitalizing on cost advantages, while international players like Sharp Corporation and STMicroelectronics expand production facilities in the region. However, price sensitivity remains a challenge for high-end sensor adoption.

North America

North America is a key innovation hub for ambient light sensor technologies, with U.S.-based companies like Broadcom and SILICON LABS leading R&D in low-power consumption sensors. The region shows strong preference for premium smartphones (iPhone adoption exceeds 50% market share), driving demand for high-precision ALS components. Regulatory emphasis on energy-efficient devices aligns with ALS capabilities for battery optimization. The market is transitioning toward miniaturized sensors with AI-powered adaptive brightness features, though higher costs limit penetration in budget devices.

Europe

European smartphone manufacturers prioritize energy-efficient ALS solutions to comply with EU Ecodesign and Energy Labeling regulations. Germany and France are key markets where users value eye-comfort features like auto-dimming in low-light conditions. STMicroelectronics (Switzerland) and ams-OSRAM AG (Austria) supply advanced ALS chips to global brands, with growing focus on automotive-grade sensors for connected devices. Market growth is tempered by slower smartphone replacement cycles compared to Asia, but increasing 5G adoption presents new opportunities.

South America

Brazil and Argentina are emerging markets where affordable Chinese smartphones with basic ALS functionalities are gaining traction. Price competitiveness outweighs advanced features, leading to higher demand for 2-in-1 sensors rather than premium 3-in-1 variants. Local assembly initiatives may boost sensor adoption, but economic instability and import dependencies create supply chain vulnerabilities. The market shows potential as mobile internet penetration grows, particularly for mid-range devices balancing cost and performance.

Middle East & Africa

This region exhibits divergent trends: Gulf countries (UAE, Saudi Arabia) show strong demand for flagship smartphones with advanced ALS features, while African markets prioritize affordability. Turkish manufacturers like HiveMotion are developing cost-optimized sensors for local brands. Challenges include fragmented distribution networks and low consumer awareness about ALS benefits. However, increasing smartphone penetration in Africa (expected to reach 50% by 2025) presents long-term growth avenues, particularly for entry-level sensors.

Technology Spotlight: The shift toward under-display ambient light sensors is gaining momentum, particularly in Asia and North America, as manufacturers pursue bezel-less designs. This innovation is driving partnerships between sensor producers and display manufacturers to maintain accuracy despite panel obstructions, representing the next frontier in smartphone ALS development.

Report Scope

This market research report provides a comprehensive analysis of the global Ambient Light Sensor for Smartphones market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 125 million in 2024 and is projected to reach USD 174 million by 2032, growing at a CAGR of 5.0%.

- Segmentation Analysis: Detailed breakdown by product type (2-in-1, 3-in-1, Others), application (iOS Smartphones, Android Smartphones, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key markets driving growth.

- Competitive Landscape: Profiles of leading market participants including Sensortek, Broadcom, STMicroelectronics, SILICON LABS, ams-OSRAM AG, with analysis of their product portfolios, R&D focus, and market strategies.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with smartphone display systems, and evolving industry standards for light sensing accuracy.

- Market Drivers & Restraints: Evaluation of factors such as growing smartphone adoption, demand for energy-efficient displays, along with challenges like price sensitivity and component miniaturization.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, smartphone OEMs, component suppliers, and investors regarding market opportunities and challenges.

The research employs both primary and secondary methodologies, including interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ambient Light Sensor for Smartphones Market?

-> Ambient Light Sensor for Smartphones Market was valued at 125 million in 2024 and is projected to reach US$ 174 million by 2032, at a CAGR of 5.0% during the forecast period.

Which key companies operate in this market?

-> Key players include Sensortek, Broadcom, STMicroelectronics, SILICON LABS, ams-OSRAM AG, Vishay, Lite-On Technology, and Sharp Corporation.

What are the key growth drivers?

-> Growth is driven by rising smartphone adoption, demand for energy-efficient displays, and increasing integration of advanced sensor technologies.

Which region dominates the market?

-> Asia-Pacific leads in both production and consumption, while North America remains strong in technological innovation.

What are the emerging trends?

-> Emerging trends include multi-functional sensor integration, improved accuracy in low-light conditions, and development of ultra-compact sensor designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...