Aluminum polymer SMD capacitor for server motherboards Market Insights

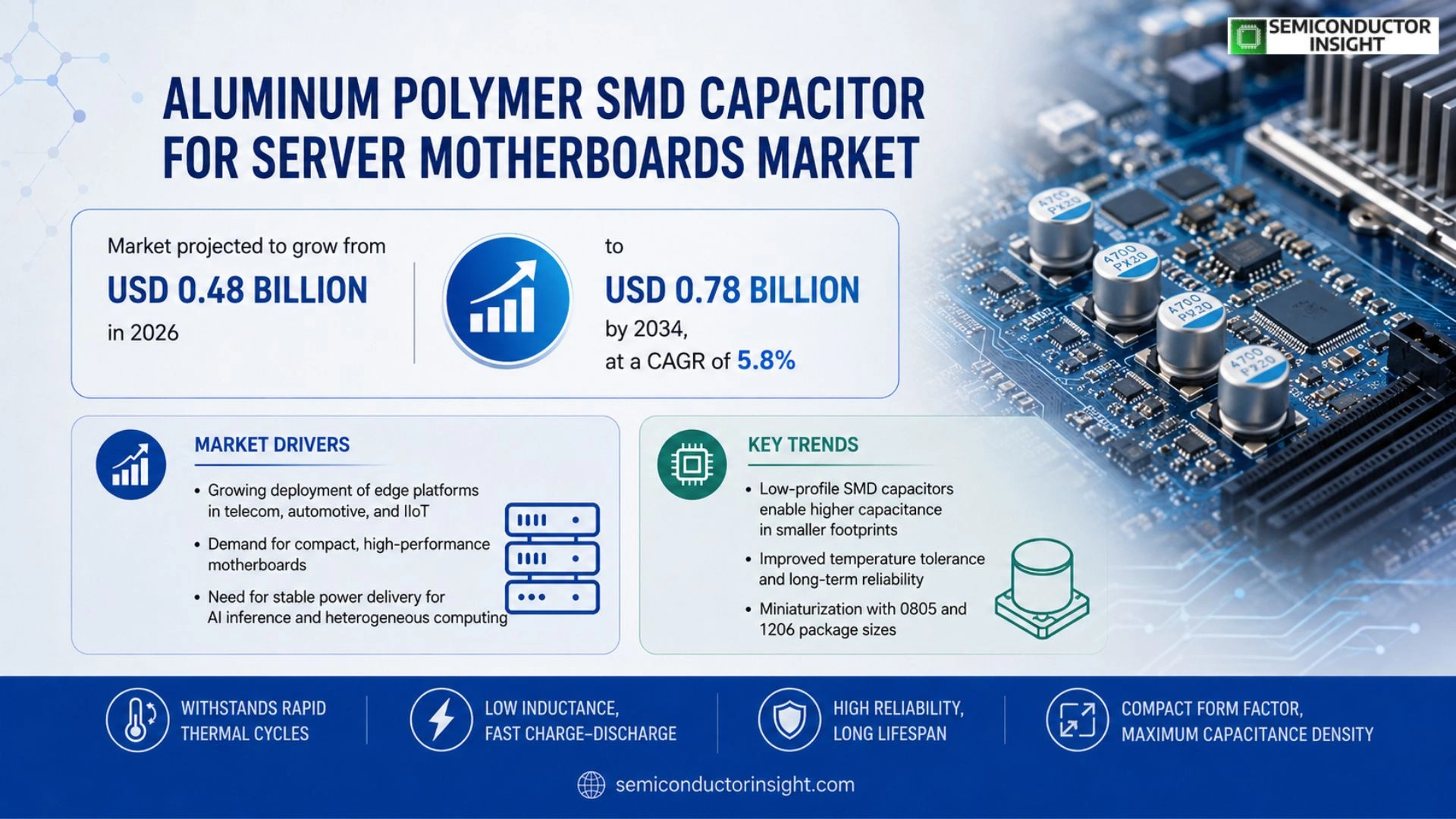

Global Aluminum polymer SMD capacitor for server motherboards market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period.

Aluminum polymer surface‑mount device (SMD) capacitors are low‑ESR components that combine the high capacitance density of aluminum electrolytic technology with the reliability of solid‑polymer electrolytes. Designed specifically for high‑density server motherboards, they provide stable voltage regulation under heavy computational loads and support rapid thermal cycling typical of data‑center environments.

The market is experiencing robust growth because cloud‑computing expansion and AI‑driven workloads increase power‑density requirements on servers. Furthermore, rising adoption of edge‑computing platforms pushes manufacturers toward compact yet high‑performance passive components.

MARKET DRIVERS

Increasing Data Center Power Efficiency Demands

The surge in hyperscale data centers has intensified the need for components that reduce power loss. Aluminum polymer SMD capacitors provide lower equivalent series resistance (ESR) compared with traditional electrolytic types, directly supporting Aluminum polymer SMD capacitor for server motherboards Market growth as manufacturers chase higher efficiency ratios.

Growth of High‑Performance Computing (HPC) Platforms

HPC workloads demand stable voltage regulation on server motherboards. The superior thermal conductivity of polymer electrolytes enables designers to place capacitors closer to power‑intensive chips, shortening loop lengths and improving overall system reliability. This technical advantage is a primary catalyst for market adoption.

➤ “The shift to polymer‑based SMD capacitors is reducing motherboard thermal hotspots by up to 15 %,” says an industry analyst.

Broad industry standards such as DDR5 and PCIe 5.0 further tighten voltage tolerances, making the reliability of Aluminum polymer SMD capacitor for server motherboards Market solutions a decisive factor in component selection for new server platforms.

MARKET CHALLENGES

Cost Sensitivity in Tier‑1 Server Segments

While performance benefits are clear, the premium pricing of polymer SMD capacitors compared with traditional alternatives poses budgeting challenges for large‑scale OEMs, especially in price‑competitive server tiers where margin pressures remain high.

Other Challenges

Supply Chain Volatility

Fluctuations in raw material availability for polymer electrolytes can lead to lead‑time extensions, complicating just‑in‑time manufacturing models common in the server industry.

MARKET RESTRAINTS

Limited Design Familiarity

Design engineers accustomed to conventional aluminum electrolytic capacitors often lack extensive experience with polymer formulations, resulting in longer validation cycles and a cautious approach to integrating these components into server motherboards.

MARKET OPPORTUNITIES

Emerging Edge‑Computing Deployments

Edge servers operate in constrained environments where space, thermal management, and power efficiency are critical. The compact footprint and high ripple current capability of aluminum polymer SMD capacitors position them as a strategic component for next‑generation edge infrastructure, opening a new growth corridor for the market.

Aluminum polymer SMD capacitor for server motherboards Market Trends

Rising Power‑Density Demands in Data‑Center Servers

The acceleration of cloud‑computing services and AI‑driven workloads is forcing server manufacturers to pack more processing power into each board. This shift creates a pronounced need for passive components that can sustain higher ripple currents while keeping equivalent series resistance (ESR) low. Aluminum polymer SMD capacitors meet these requirements by delivering a dense capacitance profile combined with the reliability of solid‑polymer electrolytes. Their ability to regulate voltage under heavy computational loads reduces the risk of power instability, which is critical for maintaining uptime in hyperscale data‑center environments. In addition, the solid‑polymer matrix provides superior leakage‑current characteristics compared with traditional wet electrolytes, extending service life under continuous high‑temperature operation. Manufacturers also benefit from the relatively simple reflow soldering profile of these components, which aligns with existing assembly lines and minimizes production bottlenecks. Consequently, data‑center OEMs are increasingly specifying aluminum polymer SMD capacitors as standard building blocks for next‑generation server platforms.

Other Trends

Edge‑Computing Adoption Accelerates Component Miniaturization

Edge platforms demand compact, high‑performance boards that can survive rapid thermal cycles and fluctuating power profiles. The low‑profile form factor of aluminum polymer SMD capacitors aligns with these constraints, enabling designers to shrink board footprints without sacrificing capacitance density. As edge deployments proliferate in telecom, autonomous vehicles, and industrial IoT, the market sees a steady increase in orders for capacitors that balance size, temperature tolerance, and long‑term reliability. Furthermore, the latency‑sensitive nature of edge AI inference requires power‑stable environments, prompting designers to prioritize capacitors with low inductance and fast charge‑discharge cycles. The growing trend toward heterogeneous computing, where GPUs and ASICs share the same motherboard, further amplifies the demand for capacitors capable of handling diverse load transients. Suppliers responding with smaller package sizes, such as 0805 and 1206, are helping OEMs meet the aggressive form‑factor targets of edge servers.

Advancements in Polymer Electrolyte Formulations

Leading manufacturers such as Murata, TDK, AVX, and KEMET are rolling out next‑generation polymer electrolytes that extend operating temperature ranges and boost ripple‑current capability. These innovations reduce failure rates during rapid thermal cycling and support the higher power‑density architectures emerging in next‑generation servers. Sustainability considerations are also shaping development, as manufacturers adopt lead‑free polymer formulations and improve material recyclability. Industry roadmaps indicate a shift toward ultra‑high‑frequency (UHF) operating capabilities to support emerging 400‑Gb/s Ethernet and PCIe 5.0 standards. Analysts anticipate that ongoing R&D will further narrow the performance gap between aluminum polymer SMD devices and traditional solid‑capacitor technologies, reinforcing their position as the preferred choice for high‑density server motherboards.

COMPETITIVE LANDSCAPE

Key Industry Players

Aluminum Polymer SMD Capacitor for Server Motherboards – Competitive Overview

The market is anchored by a handful of large‑scale manufacturers that control the majority of volume shipments to server‑board OEMs. Murata Manufacturing leads the segment with its Ultra‑Low‑ESR series, leveraging an extensive global supply chain and aggressive pricing that aligns with the projected CAGR of 5.8 % through 2034. TDK Corporation follows closely, differentiating on high‑temperature tolerance and ripple‑current capability, which are critical for AI‑driven workloads. Both firms benefit from deep R&D investments that enable rapid iteration of polymer electrolyte formulations, allowing them to capture the bulk of contracts from hyperscale data‑center builders and edge‑computing platform vendors.

Beyond the dominant tier, a diverse cohort of niche and regional players sustains competitive pressure and drives incremental innovation. AVX Corp. and KEMET Corporation have introduced extended‑life product lines targeting rugged enterprise environments, while Vishay Intertechnology focuses on compact form‑factor solutions for space‑constrained motherboards. Companies such as Taiyo Yuden, Samsung Electro‑Mechanics, and Panasonic Electronic Components add depth with specialty capacitance‑density offerings, and newer entrants like Yageo Corporation and Kyocera Corporation are expanding their polymer‑capacitor portfolios to address emerging thermal‑cycling challenges. This fragmented tail of manufacturers ensures a steady pipeline of differentiated technologies that collectively enhance reliability and performance across the server motherboard ecosystem.

List of Key Aluminum Polymer SMD Capacitor for Server Motherboards Companies Profiled

- Murata Manufacturing

- TDK Corporation

- AVX Corp.

- KEMET Corporation

- Vishay Intertechnology

- Taiyo Yuden

- Samsung Electro‑Mechanics

- Yageo Corporation

- Panasonic Electronic Components

- Kyocera Corporation

- Illinois Capacitor Corp.

- Cornell Dubilier

- Rohm Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Low‑ESR Aluminum Polymer

|

| By Application |

|

Server Motherboard Power Decoupling

|

| By End User |

|

Data Center Operators

|

| By Performance Requirement |

|

High Ripple Current Capability

|

| By Technology Trend |

|

Solid‑Polymer Electrolyte Innovations

|

Regional Analysis: Aluminum polymer SMD capacitor for server motherboards Market

North American fabs have integrated aluminum polymer SMD capacitor production lines with advanced automation, enabling shorter cycle times and higher yield. Collaboration between material suppliers and tier‑1 capacitor makers accelerates the rollout of thin‑film polymer dielectrics, supporting the demand for compact, high‑reliability server boards. The region’s supply chain resilience further consolidates its leading position.

Data‑center operators and hyperscale cloud providers dominate the demand curve, valuing the low ESR and high temperature stability of polymer SMD capacitors. High‑performance computing clusters and AI training rigs also rely on these components to maintain signal integrity under intensive workloads, reinforcing North America’s sectoral advantage.

Stringent RoHS compliance and expanding safety certifications drive manufacturers to adopt lead‑free polymer formulations. North American standards emphasize reliability testing for server‑grade components, prompting vendors to implement rigorous qualification protocols. This regulatory focus ensures market participants maintain high quality, further strengthening the region’s reputation.

Collaborative R&D programs between universities and capacitor firms accelerate the development of ultra‑low‑inductance polymer dielectrics. Emerging 3D‑stacked server architectures stimulate interest in form‑factor‑optimized SMD designs, positioning North America at the forefront of next‑generation capacitor innovation.

Europe

Europe remains a critical hub for Aluminum polymer SMD capacitor for server motherboards Market, with a strong emphasis on sustainability and energy efficiency. Germany’s engineering expertise drives the integration of polymer capacitors into high‑density server platforms, while the United Kingdom focuses on advanced materials research to enhance dielectric performance. The region benefits from unified regulatory frameworks that promote eco‑friendly manufacturing, encouraging manufacturers to adopt lead‑free polymer technologies. Collaborative initiatives across the EU foster standardization, enabling smoother cross‑border supply chains and reinforcing Europe’s position as a key supplier of high‑reliability components for enterprise data centers.

Asia‑Pacific

Asia‑Pacific is emerging as a fast‑growing market for Aluminum polymer SMD capacitor for server motherboards Market, propelled by rapid digital transformation and expanding cloud infrastructure. China’s massive server production capacity creates strong demand for polymer‑based SMD solutions that can endure high thermal stress. Japan’s long‑standing expertise in precision electronics supports the development of ultra‑reliable capacitor modules, while South Korea’s emphasis on 5G and edge computing drives innovation in compact form factors. The region’s cost‑effective manufacturing capabilities, combined with increasing focus on environmentally compliant processes, position Asia‑Pacific as a vital contributor to the global supply chain.

South America

South America contributes niche yet valuable insights to Aluminum polymer SMD capacitor for server motherboards Market, with Brazil leading regional adoption through its growing data‑center ecosystem. Local manufacturers are beginning to integrate polymer SMD capacitors to meet the reliability expectations of multinational server OEMs operating in the continent. Emerging markets such as Argentina and Chile are investing in telecom infrastructure upgrades, which indirectly stimulate demand for high‑performance server components. Although the market share remains modest, the region’s focus on cost‑efficient production and increasing technical expertise supports a gradual expansion of polymer capacitor usage.

Middle East & Africa

Middle East & Africa presents a developing landscape for Aluminum polymer SMD capacitor for server motherboards Market, driven by expanding cloud services and increasing data‑center investments in the Gulf Cooperation Council states. The United Arab Emirates and Saudi Arabia are establishing technology hubs that prioritize energy‑efficient server designs, creating a niche for polymer‑based SMD capacitors known for thermal resilience. African markets, led by South Africa, are gradually upgrading telecommunications infrastructure, prompting early adoption of reliable server components. While the overall demand is still in its infancy, sustained governmental support for digital transformation projects underpins a steady upward trajectory for polymer capacitor integration in the region.

Report Scope

This market research report provides a comprehensive analysis of the Aluminum polymer SMD capacitor for server motherboards Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Aluminum polymer SMD capacitor for server motherboards Market?

-> Aluminum polymer SMD capacitor for server motherboards market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034.

Which key companies operate in Aluminum polymer SMD capacitor for server motherboards Market?

-> Key players include Murata Manufacturing, TDK Corporation, AVX Corp., and KEMET, among others.

What are the key growth drivers?

-> Key growth drivers include cloud‑computing expansion, AI‑driven workloads, and rising edge‑computing adoption.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include higher ripple‑current capability, extended temperature range designs, and integration of solid‑polymer technology for improved reliability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...