MARKET INSIGHTS

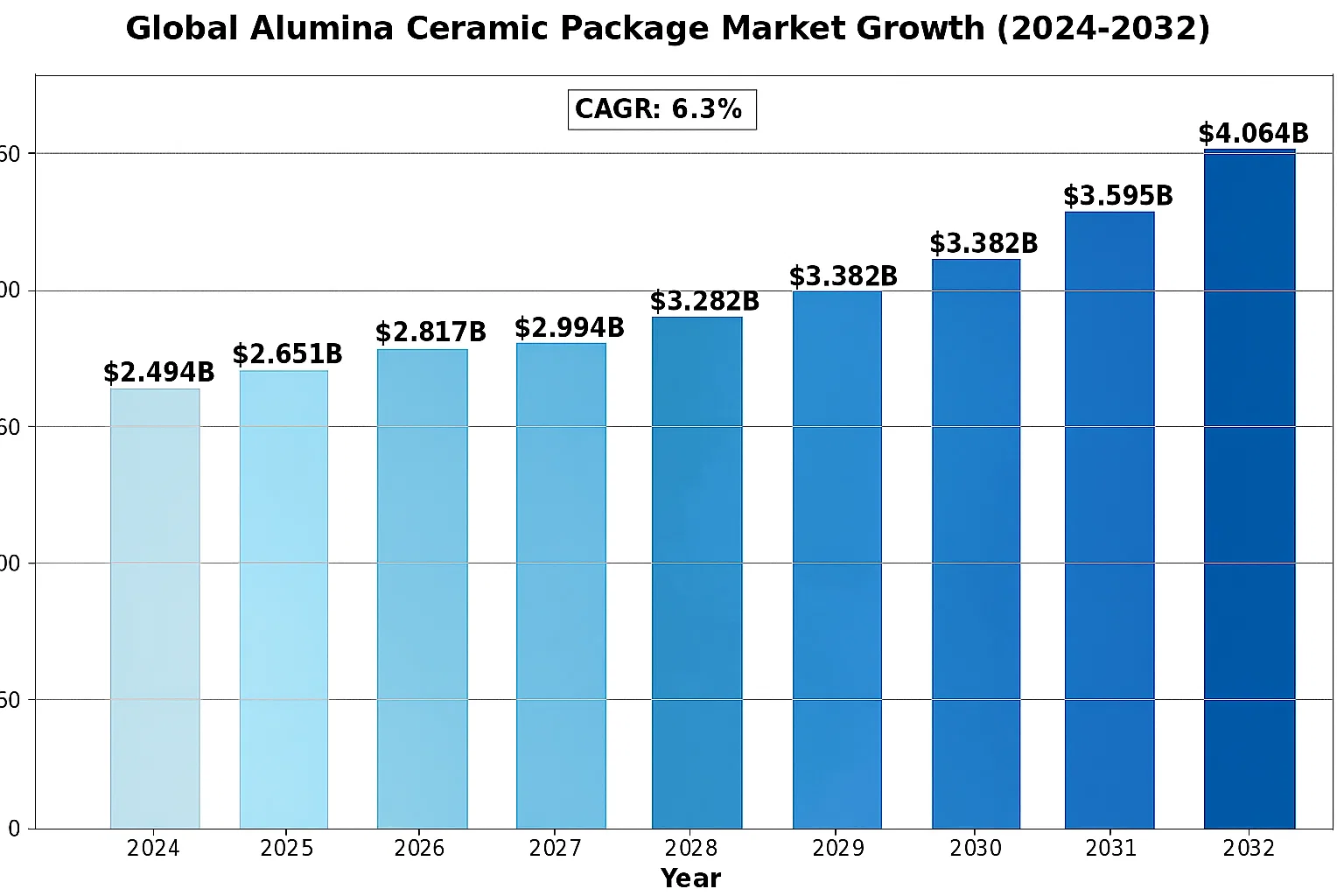

The global Alumina Ceramic Package Market was valued at 2494 million in 2024 and is projected to reach US$ 3782 million by 2032, at a CAGR of 6.3% during the forecast period.

Alumina ceramic packages are advanced packaging solutions known for their exceptional thermal and electrical properties. These packages are manufactured using high-purity alumina (Al2O3) ceramics, which provide superior insulation, high mechanical strength, and excellent thermal conductivity. They are widely used in semiconductor, automotive, and aerospace applications where reliability under extreme conditions is critical.

The market growth is primarily driven by increasing demand from the semiconductor industry, which accounted for USD 579 billion in 2022 and is expected to reach USD 790 billion by 2029. While analog and logic semiconductors continue showing strong growth (20.76% and 14.46% respectively in 2022), the expanding Internet of Things (IoT) ecosystem is creating new opportunities for ceramic packaging solutions. Furthermore, automotive electrification trends and 5G infrastructure development are accelerating adoption across multiple industries. However, competition from alternative materials and complex manufacturing processes remain key challenges for market players.

MARKET DYNAMICS

MARKET DRIVERS

Growing Semiconductor Industry Fuels Demand for High-Reliability Alumina Ceramic Packages

The alumina ceramic package market is experiencing significant growth due to its critical role in semiconductor packaging. With the global semiconductor market projected to reach $790 billion by 2029, growing at a CAGR of 6%, the demand for advanced packaging solutions is accelerating. Alumina ceramic packages offer superior thermal stability, mechanical strength, and electrical insulation compared to plastic or metal alternatives, making them indispensable for high-performance applications. The ability to create multilayer wiring structures with up to 60 layers through thick film technology provides the necessary density for modern semiconductor components. This technical advantage positions alumina ceramics as the packaging material of choice for power devices, microprocessors, and other high-reliability applications.

Automotive Electronics Revolution Creates New Growth Avenues

The automotive industry’s rapid electrification is creating substantial opportunities for alumina ceramic packages. As vehicles incorporate more advanced driver-assistance systems (ADAS), electric powertrains, and in-vehicle networking, the need for robust electronic packaging solutions has increased dramatically. Alumina ceramic packages provide the necessary thermal management for power electronics operating in harsh automotive environments. The market for automotive power electronics is forecast to grow at over 8% annually, driven by the accelerating transition to electric vehicles that require high-voltage power modules typically packaged in alumina ceramics. Furthermore, the push towards autonomous vehicles is generating demand for high-reliability sensor packaging where alumina’s stability and precision are crucial.

5G Infrastructure Deployment Accelerates Market Expansion

The global rollout of 5G networks is significantly boosting demand for alumina ceramic packages in communication applications. These packages provide essential thermal management and signal integrity for high-frequency RF components in 5G base stations. With over 2 million 5G base stations expected to be deployed worldwide by 2025, the market for ceramic packages in communication devices is experiencing robust growth. The material’s low dielectric loss and excellent high-frequency characteristics make it ideal for packaging power amplifiers and other critical components in 5G infrastructure. Additionally, the ongoing development of 6G technologies promises to sustain long-term demand for advanced ceramic packaging solutions.

MARKET RESTRAINTS

High Production Costs Limit Market Penetration

While alumina ceramic packages offer superior performance characteristics, their relatively high production costs compared to plastic alternatives present a significant market restraint. The precise manufacturing processes required to achieve the necessary tolerances (including sintering control within 0.1%) and multilayer wiring integration result in substantially higher production costs. This cost premium makes ceramic packages economically viable primarily for high-reliability applications where performance justifies the expense. However, in consumer electronics and other price-sensitive markets, manufacturers often opt for lower-cost plastic or organic substrates despite their inferior performance characteristics. The cost differential is particularly challenging in emerging markets where price competition is intense.

Supply Chain Vulnerabilities Create Production Bottlenecks

The alumina ceramic package market faces significant challenges from supply chain disruptions affecting raw material availability. High-purity alumina powder, the primary raw material, has experienced price volatility due to geopolitical tensions and trade restrictions. Several key manufacturing facilities concentrated in specific geographic regions create vulnerability to localized disruptions. Recent events have demonstrated how natural disasters, political instability, or pandemic-related restrictions can severely impact the supply of critical materials. Furthermore, the specialized equipment required for ceramic package manufacturing often faces long lead times, delaying capacity expansion efforts during periods of strong demand growth.

MARKET OPPORTUNITIES

Expansion of High-Power LED Applications Presents Growth Potential

The alumina ceramic package market stands to benefit significantly from the expanding applications of high-power LEDs across multiple industries. As solid-state lighting technology advances, higher lumen output LEDs require more robust thermal management solutions that alumina ceramics can provide. The market for high-power LED packaging is anticipated to grow at over 7% annually, driven by applications in automotive headlights, industrial lighting, and specialized horticulture lighting systems. Alumina’s excellent thermal conductivity (~30 W/mK) and electrical insulation properties make it an ideal substrate material for these demanding applications where heat dissipation is critical to performance and longevity.

Emerging Aerospace and Defense Applications Open New Frontiers

The aerospace and defense sector presents promising opportunities for alumina ceramic packages due to their ability to withstand extreme environmental conditions. Modern aircraft increasingly rely on advanced avionics systems that require packaging solutions capable of operating in high-vibration, wide-temperature-range environments. The growing deployment of satellite constellations for global communications and earth observation is generating demand for radiation-hardened electronic packages. Alumina ceramics’ combination of thermal stability, mechanical strength, and radiation resistance positions them well to serve these high-value applications. With global defense spending reaching record levels and commercial space activities expanding rapidly, the market potential for specialized ceramic packages in this sector is substantial.

MARKET CHALLENGES

Intense Competition from Alternative Materials Poses Threat

The alumina ceramic package market faces growing competition from alternative packaging materials that offer different technical and economic advantages. Aluminum nitride and silicon carbide substrates provide higher thermal conductivity, while advanced plastic composites continue to improve their thermal and mechanical properties. The development of glass-based interposers and 3D packaging technologies presents additional competitive pressure. These alternatives are particularly attractive for applications where weight reduction or cost sensitivity outweighs the need for alumina’s specific advantages. Market participants must continually innovate to demonstrate the unique value proposition of alumina ceramics in an increasingly crowded materials landscape.

Technological Complexity Limits Manufacturing Scalability

Meeting the exacting requirements of modern semiconductor packaging with alumina ceramics presents significant technical challenges. The production of multilayer ceramic packages with fine-line circuitry requires precise control of material properties and processing parameters. Variations in sintering behavior, dimensional stability, and metallization quality can impact yields and reliability in large-scale manufacturing. As package designs become more complex to accommodate higher pin counts and finer pitches, maintaining consistent quality becomes increasingly difficult. The industry also faces challenges in developing compatible materials and processes for next-generation applications, requiring substantial R&D investments to stay competitive in the evolving packaging ecosystem.

ALUMINA CERAMIC PACKAGE MARKET TRENDS

Semiconductor Industry Expansion Driving Market Growth

The global semiconductor market, valued at approximately $579 billion in 2022, is projected to reach $790 billion by 2029, growing at a CAGR of 6%. This expansion directly fuels demand for alumina ceramic packages, which are critical for high-reliability semiconductor applications. While memory segments saw a 12.64% decline in 2022, analog, sensor, and logic segments demonstrated strong double-digit growth, underscoring the diverse applications for ceramic packaging. The market is further propelled by IoT adoption, requiring advanced packaging for processors and controllers in smart devices. Alumina ceramics’ ability to maintain dimensional stability within 0.1% during sintering makes them indispensable for multilayer wiring structures in modern chip components.

Other Trends

Automotive Electronics Revolution

Electrification in the automotive sector is creating unprecedented demand for alumina ceramic packages, particularly for power electronics in electric vehicles. With automotive applications accounting for nearly 15% of the market share, packages must withstand high temperatures and provide excellent electrical insulation. The shift towards autonomous driving systems is further accelerating adoption, as ceramic packages ensure reliability for advanced driver-assistance systems (ADAS) operating in harsh environments. Hybrid and electric vehicle production is expected to grow at 29% annually through 2030, directly correlating with increased ceramic packaging requirements.

5G Infrastructure Deployment

The global rollout of 5G networks represents a significant growth vector for alumina ceramic packages in communication devices. These packages provide essential thermal management and signal integrity for high-frequency 5G components. With over 1.3 billion 5G subscriptions projected by 2023, manufacturers are scaling production to meet base station and mobile device requirements. The Asia-Pacific region, leading in 5G adoption, accounts for nearly 45% of ceramic package demand in telecommunications. Furthermore, emerging 6G research initiatives are already driving R&D investments in next-generation ceramic packaging solutions capable of handling terahertz frequencies.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Material Advancements Drive Market Competition

The global alumina ceramic package market exhibits a semi-consolidated competitive structure, with established multinational corporations competing alongside regional specialists. KYOCERA Corporation dominates the market with approximately 18% revenue share in 2024, leveraging its vertically integrated manufacturing capabilities and extensive R&D investments in high-purity alumina formulations. The company’s success stems from its ability to meet stringent aerospace and automotive industry requirements while maintaining cost competitiveness.

NGK/NTK and SCHOTT collectively hold over 25% market share, with their heavy focus on LED packaging solutions and hermetic seals for semiconductor applications. These players have demonstrated consistent growth through strategic partnerships with automotive OEMs and telecommunications equipment manufacturers. Their patented ceramic compositions with thermal conductivity exceeding 24 W/mK give them significant technical advantage in high-power applications.

Regional competitors like ChaoZhou Three-circle (Group) are gaining traction through aggressive pricing strategies and localized supply chains in Asia-Pacific markets. The company reported 12% year-over-year growth in 2023 by expanding production capacity for consumer electronics packaging. Meanwhile, Japanese firm MARUWA differentiates through ultraprecision machining capabilities that enable dimensional tolerances under ±5μm, critical for 5G RF components.

Emerging technological trends are reshaping competition dynamics. Companies are actively developing nano-grained alumina ceramics with improved fracture toughness (>4 MPa·m¹/²) to address the rising demand for thin-walled packages in wearable electronics. AMETEK recently unveiled a new low-temperature co-fired ceramic (LTCC) process that reduces energy consumption by 30% compared to conventional sintering methods.

List of Key Alumina Ceramic Package Companies Profiled

- KYOCERA Corporation (Japan)

- NGK/NTK (Japan)

- ChaoZhou Three-circle (Group) (China)

- SCHOTT (Germany)

- MARUWA (Japan)

- AMETEK (U.S.)

- Hebei Sinopack Electronic Technology Co.Ltd (China)

- NCI (U.S.)

- Yixing Electronic (China)

- LEATEC Fine Ceramics (Taiwan)

- Shengda Technology (China)

Segment Analysis:

By Type

White Ceramic Segment Leads the Market Due to High Thermal Stability and Electrical Insulation Properties

The market is segmented based on type into:

- Black Ceramic

- White Ceramic

By Application

Automotive Electronics Dominates Due to Increased Adoption in Electric Vehicles and Advanced Driver Assistance Systems

The market is segmented based on application into:

- Automotive Electronics

- Communication Devices

- Aeronautics and Astronautics

- High Power LED

- Consumer Electronics

- Others

By End-User

Semiconductor Industry Accounts for Largest Share Owing to Reliability Requirements in Chip Packaging

The market is segmented based on end-user into:

- Semiconductor Manufacturers

- Electronics Component Suppliers

- Research Institutions

- Military and Defense

Regional Analysis: Alumina Ceramic Package Market

North America

The North American alumina ceramic package market benefits from advanced semiconductor manufacturing and strong R&D investments, particularly in the U.S. With key players like KYOCERA Corporation and AMETEK operating in the region, demand is driven by applications in aerospace, defense, and high-power LED industries. The CHIPS and Science Act of 2022, allocating $52.7 billion for domestic semiconductor production, further accelerates adoption. Stringent quality standards and the need for miniaturized components in IoT and automotive electronics sustain market growth. However, high manufacturing costs present a challenge for widespread adoption among smaller enterprises.

Europe

Europe’s market thrives on innovation and regulatory compliance, with Germany leading in automotive electronics and SCHOTT dominating ceramic packaging solutions. The EU’s focus on sustainable electronics manufacturing and growth in 5G infrastructure bolsters demand for high-reliability ceramic packages. While the aerospace sector remains a key consumer, the region faces competition from Asian manufacturers offering cost-competitive alternatives. Investments in wafer-level packaging technologies indicate a shift toward integration with existing semiconductor workflows, balancing performance with environmental considerations under the Circular Economy Action Plan.

Asia-Pacific

Accounting for over 40% of global alumina ceramic package consumption, the Asia-Pacific region is propelled by China’s semiconductor ecosystem and Japan’s precision manufacturing. Companies like ChaoZhou Three-circle and MARUWA leverage local supply chains to serve industries ranging from consumer electronics to telecommunications. Government initiatives like China’s “Made in China 2025” and India’s semiconductor incentives fuel production capacity expansion. Cost efficiency drives adoption, though fluctuating raw material prices and trade tensions occasionally disrupt supply chains. Emerging applications in EV power modules and AI hardware present new opportunities.

South America

The South American market shows gradual growth, with Brazil’s automotive sector being the primary adopter of ceramic packages for engine control units and sensors. Limited local manufacturing capabilities result in heavy reliance on imports from North America and Asia. Economic instability and currency fluctuations hinder large-scale investments in advanced packaging technologies, though increasing foreign partnerships for electronics assembly indicate potential long-term market development. Argentina’s gradual recovery in industrial production presents niche opportunities in medical device packaging applications.

Middle East & Africa

This emerging market exhibits selective growth in countries with developing electronics manufacturing bases, particularly Israel (military applications) and the UAE (aerospace components). While currently representing less than 5% of global demand, increasing FDI in technology parks and special economic zones stimulates local packaging needs. Challenges include limited technical expertise in ceramic processing and dependence on international suppliers. Strategic partnerships with Asian manufacturers are facilitating knowledge transfer, positioning the region for gradual adoption in renewable energy and oil/gas sensor applications.

Report Scope

This market research report provides a comprehensive analysis of the Global Alumina Ceramic Package market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Alumina Ceramic Package market was valued at USD 2494 million in 2024 and is projected to reach USD 3782 million by 2032, growing at a CAGR of 6.3%.

- Segmentation Analysis: Detailed breakdown by product type (Black Ceramic, White Ceramic), application (Automotive Electronics, Communication Devices, Aeronautics and Astronautics, High Power LED, Consumer Electronics, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis of key markets like China, Japan, US, and Germany.

- Competitive Landscape: Profiles of leading market participants including KYOCERA Corporation, NGK/NTK, ChaoZhou Three-circle (Group), SCHOTT, and MARUWA, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of advanced ceramic packaging technologies, integration with semiconductor devices, and emerging applications in 5G and IoT sectors.

- Market Drivers & Restraints: Evaluation of factors such as growing semiconductor industry (projected to reach USD 790 billion by 2029), demand for high-reliability packaging, alongside challenges like material costs and supply chain constraints.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, investors, and policymakers regarding market opportunities in the evolving electronics packaging ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Alumina Ceramic Package Market?

-> Alumina Ceramic Package Market was valued at 2494 million in 2024 and is projected to reach US$ 3782 million by 2032, at a CAGR of 6.3%.

Which key companies operate in Global Alumina Ceramic Package Market?

-> Key players include KYOCERA Corporation, NGK/NTK, ChaoZhou Three-circle (Group), SCHOTT, MARUWA, AMETEK, and Hebei Sinopack Electronic Tecnology Co.Ltd, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand in semiconductor packaging, expansion of 5G infrastructure, automotive electronics growth, and increasing adoption in aerospace applications.

Which region dominates the market?

-> Asia-Pacific holds the largest market share, driven by semiconductor manufacturing in China, Japan, and South Korea, while North America shows significant growth in advanced packaging solutions.

What are the emerging trends?

-> Emerging trends include development of ultra-thin ceramic packages, integration with advanced semiconductor designs, and increasing use in high-power LED applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...