AI Workstation GPU Market Insights

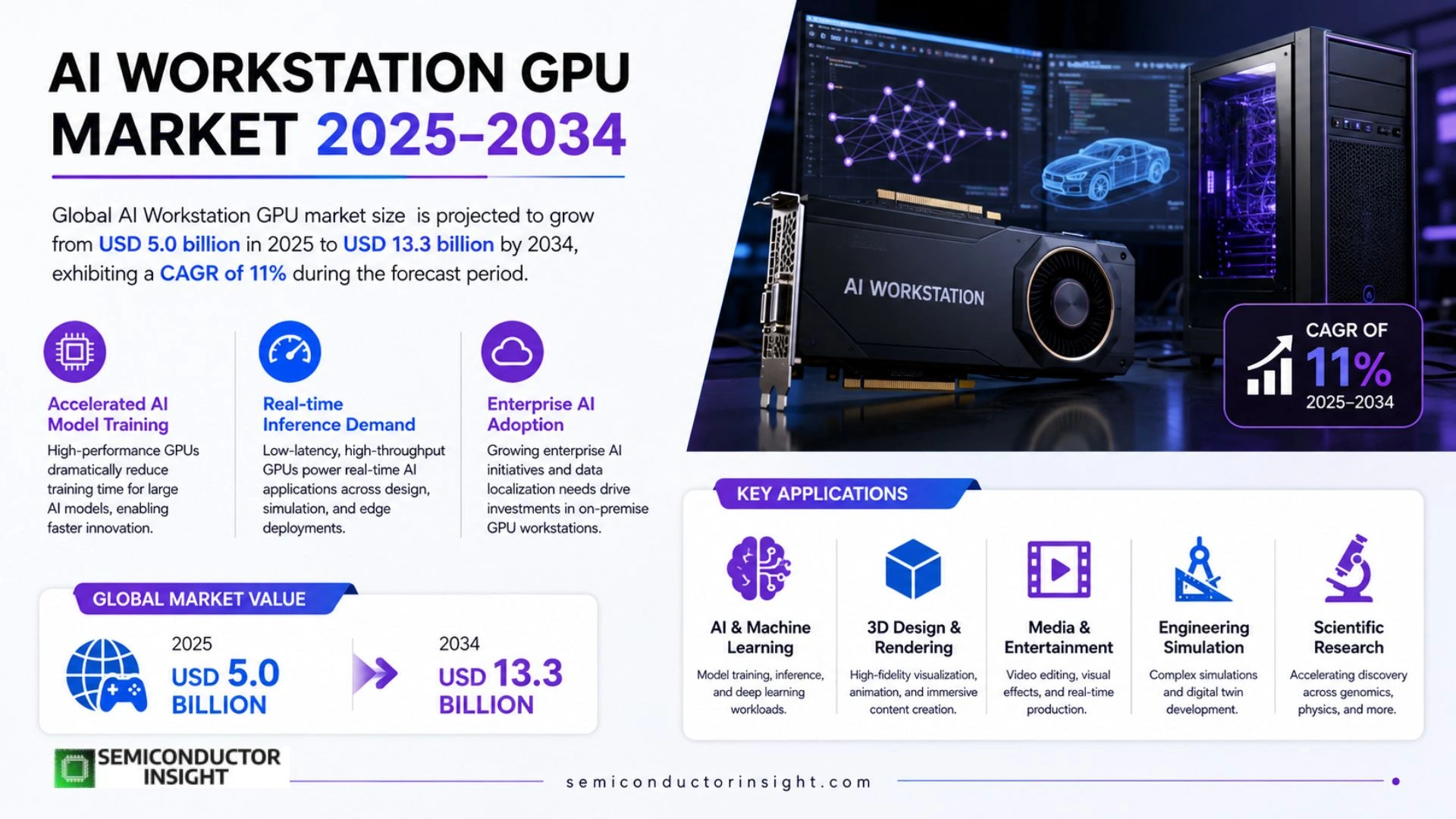

Global AI Workstation GPU market size was valued at USD 5.0 billion in 2025. The market is projected to grow from USD 5.0 billion in 2025 to USD 13.3 billion by 2034, exhibiting a CAGR of 11% during the forecast period.

AI Workstation GPUs are high‑performance graphics processors engineered for professional workloads that demand massive parallelism,deep‑learning model training, inference at scale, scientific simulation, computer‑aided design and real‑time ray tracing.

The expansion is fueled by enterprises scaling generative‑AI projects while creative studios adopt higher‑resolution pipelines; leading vendors such as NVIDIA (RTX A6000, H100), AMD (Radeon Pro W6800) and Intel (Arc A770) are releasing newer silicon that boosts tensor throughput and memory bandwidth.

MARKET DRIVERS

Accelerated AI Model Training

Enterprises are upgrading to purpose‑built GPUs to shorten the training cycle of large language models. By compressing weeks of computation into days, firms can iterate faster, protect talent from burnout, and lock in first‑to‑market advantages. This pressure is reshaping procurement criteria across AI Workstation GPU Market.

Demand for Real‑time Inference

Customer‑facing applications such as autonomous design tools and immersive visualization demand sub‑millisecond latency. GPUs that combine high tensor throughput with low‑power envelopes are becoming indispensable, prompting OEMs to integrate next‑gen silicon into workstation chassis.

➤ Designers who can render photorealistic scenes in seconds are shifting budget allocations from cloud rentals to on‑premise GPU workstations, altering the revenue mix of the sector.

The convergence of edge computing and AI workloads is also nudging midsize firms to invest in on‑site GPU accelerators, expanding the addressable base of AI Workstation GPU Market beyond traditional research labs.

MARKET CHALLENGES

Escalating Power Consumption

State‑of‑the‑art graphics processors consume upwards of 300 W under full load, forcing data‑center operators to reconsider cooling capacity and electricity budgets. Organizations with limited facility upgrades find the incremental cost a deterrent to scaling their GPU fleets.

Other Challenges

Supply Chain Volatility

Recent semiconductor shortages have lengthened lead times for high‑end GPUs, creating a mismatch between demand spikes and inventory availability. Buyers are increasingly negotiating long‑term contracts to hedge against future disruptions, which can lock in pricing structures that may become misaligned with market evolution.

MARKET RESTRAINTS

High Capital Expenditure

Upfront costs for GPU‑powered workstations remain steep, often exceeding $15,000 for top‑tier configurations. Small‑to‑midsize enterprises weigh these outlays against the uncertain ROI of AI projects, leading to a cautious adoption curve.

Financing options are still maturing; many vendors rely on traditional purchase models rather than subscription or as‑a‑service frameworks, limiting flexibility for organizations that prefer operational expenditure over capital spend.

Additionally, the rapid cadence of GPU architecture releases means that a workstation purchased today may be outperformed within 12–18 months, creating a perceived risk of technology obsolescence.

MARKET OPPORTUNITIES

Hybrid Cloud‑Edge Deployments

Enterprises that blend on‑premise GPU workstations with scalable cloud bursting can achieve cost efficiency while preserving data sovereignty. This hybrid model invites service providers to bundle managed GPU workloads, opening a new revenue stream for AI Workstation GPU Market.

Specialized software stacks optimized for workstation GPUs,such as domain‑specific libraries for medical imaging or CAD acceleration,are emerging as differentiators. Companies that co‑develop hardware‑software solutions stand to capture premium pricing and lock in long‑term customer relationships.

AI Workstation GPU Market Trends

Enterprise Scaling of Generative‑AI Workloads

The surge in corporate generative‑AI initiatives is reshaping procurement decisions for compute hardware. Companies that once reserved high‑end GPUs for niche research groups are now allocating them to production‑grade model training, inference, and fine‑tuning pipelines. This shift is not merely a budget line item; it reflects a strategic move to embed AI deeper into product lifecycles, customer service bots, and internal analytics. As model sizes inflate and data sets expand, the need for GPUs that can sustain prolonged tensor operations without throttling becomes a decisive factor in vendor selection. The consequence is a pronounced uptick in demand for devices that combine large VRAM pools with optimized tensor cores, pressuring OEMs to prioritize scalability in their roadmaps.

Other Trends

Hardware Innovation and Architecture Refresh

Leading silicon suppliers have accelerated their release cadence, introducing GPUs such as NVIDIA’s RTX A6000 and H100, AMD’s Radeon Pro W6800, and Intel’s Arc A770. Each generation pushes memory bandwidth past the 1 TB/s mark and expands tensor throughput by double‑digit percentages. These technical gains translate into shorter training epochs and higher inference throughput per watt, a metric that resonates with data‑center operators seeking to control energy costs. The competitive landscape forces manufacturers to differentiate through specialized features,NVLink interconnects, AMD’s Infinity Fabric, and Intel’s Xe‑Core optimizations,thereby enriching the choice set for buyers focused on specific workflow characteristics.

Creative Content Pipeline Evolution

High‑resolution visual production, ranging from cinematic VFX to immersive architectural renderings, is increasingly reliant on AI‑assisted tools. Studios that adopt real‑time ray tracing and AI‑upscaling modules report faster iteration cycles, enabling tighter feedback loops between artists and directors. This operational advantage drives studios to replace legacy workstations with GPU‑centric platforms that can handle both traditional GPU rasterization and AI‑intensive tensor tasks. The convergence of creative and analytical workloads on a single hardware stack creates cross‑industry pressure to standardize driver ecosystems and software SDKs, fostering a more unified development environment.

For vendors and system integrators, these intertwined trends imply a need to balance raw performance with ecosystem support. Pricing strategies must account for the premium that enterprises and studios are willing to pay for reduced time‑to‑insight and time‑to‑market. Meanwhile, software partners are incentivized to deepen integration with AI frameworks, ensuring that emerging GPU capabilities are readily exploitable. The overall trajectory suggests that AI Workstation GPU Market will continue to be a focal point for investment, with success hinging on the ability to align silicon advances with the evolving demands of both data‑intensive and creative workflows.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics of AI Workstation GPUs

NVIDIA continues to shape the AI workstation segment by leveraging its H100 and RTX A6000 families, which combine high tensor‑core density with expansive VRAM. The company’s ecosystem,software stacks like CUDA, cuDNN and a broad partner network,creates a lock‑in effect that smaller rivals find hard to replicate. AMD’s Radeon Pro W6800 line offers a compelling price‑to‑performance alternative, especially for design‑heavy workloads where OpenCL support matters. Intel’s entrance with the Arc A770, bolstered by its Xe‑core architecture, adds a third credible pillar, prompting OEMs to hedge bets across at least two silicon sources. Collectively, these three manufacturers dictate pricing tiers, roadmap cadence, and the pace of feature adoption across the market.

Beyond the tier‑one silicon providers, a constellation of system integrators and specialist vendors extends the market’s reach. Companies such as ASUS, Gigabyte and MSI integrate the top GPUs into workstation‑grade chassis, emphasizing thermal engineering and multi‑display capabilities that appeal to content creators. Enterprise‑focused brands like Dell, HP and Lenovo bundle NVIDIA and AMD GPUs with certified drivers for CAD, VFX and scientific simulation, thereby translating raw silicon performance into turnkey solutions. Niche players including PNY and Qualcomm contribute niche form‑factors or low‑power modules that enable edge‑AI deployments, while Samsung’s memory innovations indirectly influence GPU bandwidth ceilings. This multi‑layered landscape fuels competition on price, support, and value‑added services rather than pure silicon supremacy.

List of Key AI Workstation GPU Companies Profiled

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Discrete AI‑focused GPUs

|

| By Application |

|

Deep‑Learning Model Training

|

| By End User |

|

Automotive Engineering

|

| By Chip Architecture |

|

Tensor‑Core Dominant

|

| By Integration Mode |

|

Hybrid Edge‑Cloud Nodes

|

Regional Analysis: AI Workstation GPU Market

North America

Venture firms allocate a sizable portion of their funds to startups developing AI‑accelerated workstations, recognizing the competitive edge that cutting‑edge GPUs provide for data‑science teams. This financial backing fuels rapid prototype cycles and encourages early adoption among enterprise labs.

A concentration of universities producing graduates skilled in GPU programming and parallel computing underpins the region’s capacity to integrate sophisticated AI workloads into workstation environments, making talent a decisive factor for manufacturers.

Data‑center connectivity, high‑bandwidth memory technologies, and reliable power grids enable firms to deploy high‑performance workstations at scale, reducing operational friction and encouraging broader enterprise uptake.

Clear intellectual‑property safeguards and supportive trade policies provide a predictable environment for hardware innovators, allowing them to focus resources on product differentiation rather than compliance complexities.

Europe

European manufacturers are leveraging strong collaborations between academia and industry to refine GPU‑driven AI workstation solutions. Nations such as Germany and France have introduced incentives for firms that integrate AI accelerators into engineering and design workflows, stimulating demand in automotive and aerospace sectors. The region’s emphasis on data sovereignty encourages local sourcing of hardware, prompting multinational GPU vendors to establish dedicated European design hubs. As regulatory frameworks evolve to address AI ethics, European customers increasingly seek transparent performance benchmarks, driving vendors to highlight real‑world workload efficiencies in their product narratives.

Asia‑Pacific

The Asia‑Pacific landscape is characterized by rapid adoption of AI‑focused workstations in emerging technology hubs across China, Japan, and South Korea. Local enterprises prioritize scalable GPU solutions to support intense model training for language processing and computer‑vision applications. Government initiatives that fund AI research labs create a steady pipeline of demand for high‑end graphics processors. Meanwhile, the region’s manufacturing prowess ensures a cost‑effective supply chain, allowing firms to experiment with next‑generation GPU architectures without prohibitive capital outlays. The convergence of talent, policy support, and production capacity positions the Asia‑Pacific as a formidable challenger in AI Workstation GPU Market.

South America

In South America, adoption of AI workstations is gaining momentum as companies in finance and agritech recognize the value of accelerated analytics. Brazil’s growing startup ecosystem is driving experimental deployments of GPU‑enhanced platforms to extract insights from satellite imagery and market data. Regional trade agreements facilitate import of cutting‑edge hardware, while local universities expand curricula around parallel computing, gradually building a skilled user base. Although infrastructure constraints persist in certain areas, targeted investments in cloud‑based GPU services are mitigating on‑premises limitations, encouraging broader market participation.

Middle East & Africa

The Middle East & Africa region is witnessing early-stage interest in AI workstation capabilities, particularly within oil‑and‑gas analytics and health‑care imaging. Visionary governments are allocating funds to establish AI research centers that require powerful GPU workstations for simulation and modeling tasks. Partnerships with global GPU vendors are delivering training programs that upskill local engineers, laying the groundwork for sustainable demand. While overall market size remains modest, the strategic emphasis on digital transformation suggests an upward trajectory for AI Workstation GPU adoption across the region.

Report Scope

This market research report provides a comprehensive analysis of the AI Workstation GPU Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Workstation GPU Market?

-> AI Workstation GPU Market was valued at USD 6.2 billion in 2025 and is expected to reach USD 12.8 billion by 2034.

Which key companies operate in AI Workstation GPU Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...