AI-Specific Design-for-Test Market Insights

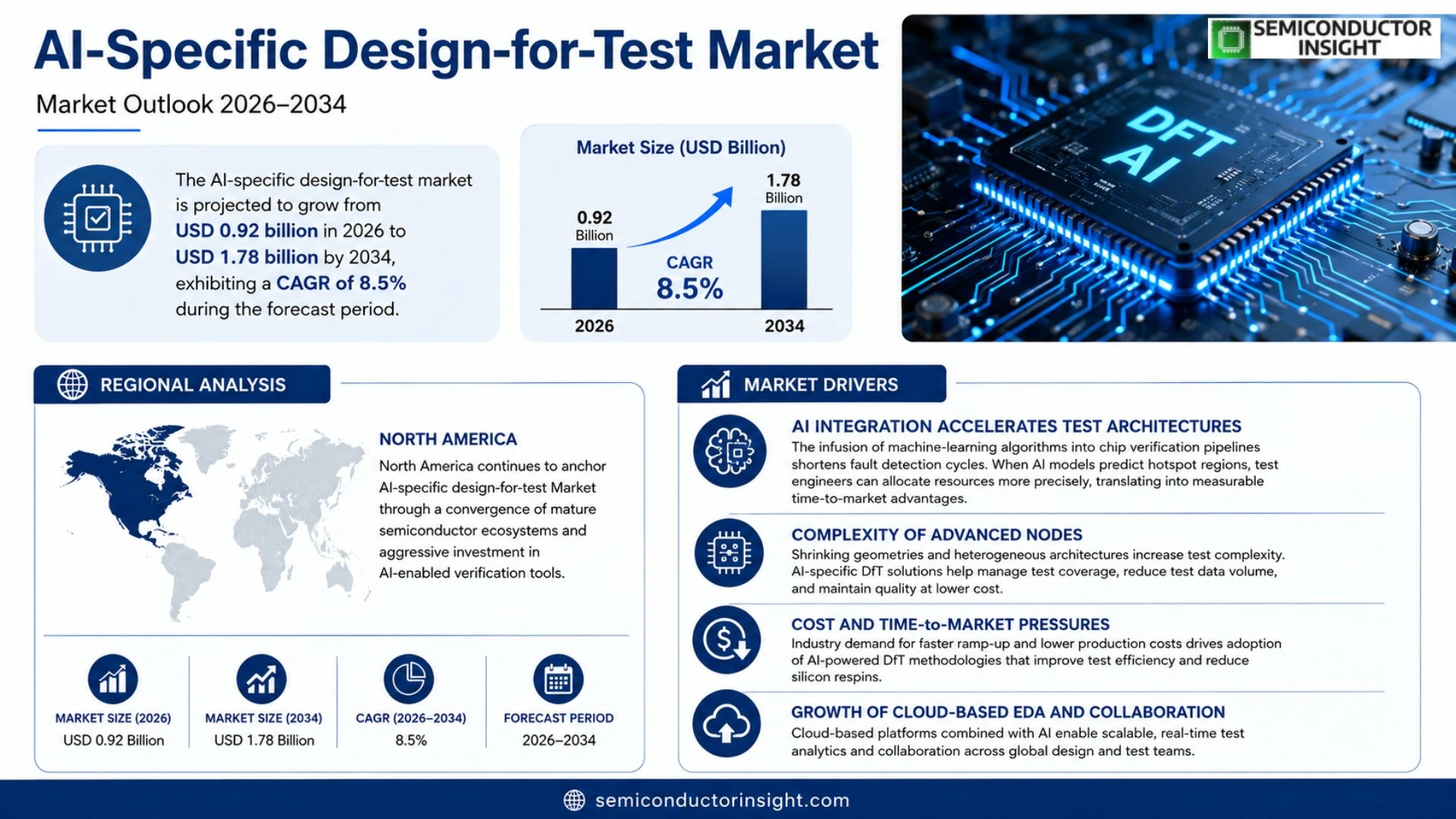

Global AI-specific design-for-test market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.78 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period.

AI-specific design‑for‑test encompasses methodologies and tools that embed testability features directly into artificial‑intelligence hardware and software pipelines. It includes built‑in self‑test circuits for neural accelerators, automated generation of test vectors for deep‑learning models, and runtime monitoring mechanisms that detect inference anomalies.

The market is experiencing accelerated expansion because AI chip architectures are becoming increasingly heterogeneous and power‑dense. Moreover, regulatory scrutiny over algorithmic safety pushes manufacturers toward comprehensive verification suites. In March 2023, Cadence announced a collaboration with NVIDIA to deliver end‑to‑end DFT solutions for next‑generation GPUs, illustrating how strategic alliances are shaping adoption. Established vendors such as Synopsys, Siemens EDA (formerly Mentor Graphics), and Intel’s verification division continue to broaden their portfolios, further reinforcing demand.

MARKET DRIVERS

AI Integration Accelerates Test Architectures

The infusion of machine‑learning algorithms into chip verification pipelines shortens fault detection cycles. When AI models predict hotspot regions, test engineers can allocate resources more precisely, translating into measurable time‑to‑market advantages. Companies that embed AI early are witnessing a shift from reactive debugging to proactive defect avoidance.

Rising System‑Level Complexity

System‑on‑chip (SoC) designs now embed heterogeneous cores, high‑speed interconnects, and specialized accelerators. This architectural density forces a reevaluation of traditional test strategies. By leveraging AI‑specific design‑for‑test (DfT) methodologies, firms can reconcile the need for exhaustive coverage with realistic test budgets.

➤ “AI‑enabled DfT reduces test pattern count by up to 30 % while preserving fault‑coverage targets,”

The economic impact is evident: reduced pattern storage eases memory constraints, and lower power consumption during test improves overall yield. As manufacturers prioritize cost efficiency, the AI‑Specific Design‑for‑Test Market becomes a strategic lever for competitive differentiation.

MARKET CHALLENGES

Data Quality Constraints

Effective AI models demand extensive, high‑fidelity simulation data. In practice, many design houses lack standardized datasets, leading to models that overfit or misinterpret rare fault scenarios. The result is a paradox where sophisticated algorithms cannot reach their full potential due to insufficient training inputs.

Other Challenges

Skill Shortage

The intersection of AI expertise and legacy test engineering creates a talent gap. Organizations often find themselves hiring data scientists who lack deep semiconductor knowledge, while existing test engineers may not be versed in machine‑learning workflows. This mismatch inflates project timelines and budget overruns.

High Up‑Front Investment

Deploying AI‑specific DfT platforms involves capital outlay for compute infrastructure, licensing, and integration services. For mid‑size fabs, the return horizon can extend beyond standard product cycles, prompting cautious adoption.

MARKET RESTRAINTS

Regulatory and Security Concerns

Stringent export controls on AI technologies and growing cybersecurity expectations impose additional validation steps. Test suites that incorporate AI must demonstrate traceability and resistance to adversarial manipulation, adding layers of compliance work that can deter rapid rollout.

Legacy Infrastructure Inertia

Many fab environments still rely on decades‑old test equipment that cannot interface directly with modern AI analytics platforms. Retrofitting or replacing such hardware entails downtime that manufacturers are reluctant to accommodate, especially when production schedules are tight.

Consequently, the market experiences a measured pace of adoption, with early adopters often confined to greenfield projects where the risk profile is more manageable.

MARKET OPPORTUNITIES

Edge‑AI Validation Services

The proliferation of AI inference at the edge creates a niche for test solutions that can validate low‑power, high‑throughput designs on the fly. Service providers that bundle AI‑specific DfT with remote diagnostics stand to capture a growing slice of the market.

AI‑Powered Security Testing

As AI accelerators become integral to critical applications, ensuring they are resilient against tampering is paramount. Companies that embed adversarial testing within their DfT flow can differentiate themselves and command premium pricing.

Finally, the shift toward subscription‑based analytics platforms lowers the barrier for smaller players to experiment with AI‑specific DfT, expanding the overall addressable market and fostering a more heterogeneous ecosystem.

AI-Specific Design-for-Test Market Trends

Heterogeneous AI Chip Architectures Elevate Test Demands

AI-specific design-for-test Market is being reshaped by the rapid diversification of AI accelerator designs. Engineers now integrate compute units, memory hierarchies, and specialized interconnects on a single die, which raises the probability of latent defects escaping traditional verification. As a result, vendors are embedding built‑in self‑test (BIST) blocks directly into neural processing units, allowing manufacturers to execute exhaustive pattern checks without external equipment. This shift reduces time‑to‑volume and aligns test strategies with the power‑dense reality of modern AI silicon, where every milliwatt saved translates into competitive advantage.

Other Trends

Strategic Alliances Accelerate Tool Adoption

In early 2023, a partnership between a leading EDA firm and a premier GPU producer introduced an end‑to‑end verification suite tailored for deep‑learning inference engines. The collaboration demonstrated how joint development can compress integration cycles, delivering test‑generation automation that matches the pace of AI model evolution. Subsequent moves by established players,expanding verification portfolios and integrating runtime monitoring,signal a broader industry consensus that comprehensive testability is no longer optional but a baseline expectation for high‑performance AI products.

Regulatory Pressure Fuels Comprehensive Verification

Regulators across major economies are tightening requirements around algorithmic safety, mandating traceable evidence that AI decisions remain within defined error bounds. This regulatory climate compels manufacturers to adopt systematic test‑vector generation and anomaly‑detection mechanisms embedded within the design flow. Companies that can demonstrate a closed‑loop verification process, from model training through silicon deployment, gain a defensible market position and mitigate the risk of costly product recalls or compliance penalties.

COMPETITIVE LANDSCAPE

Key Industry Players

AI‑Specific Design‑for‑Test Market Competitive Overview

Cadence Design Systems occupies the forefront of the AI‑specific DFT arena, largely because of its 2023 partnership with NVIDIA that couples Cadence’s verification platform with NVIDIA’s next‑generation GPU architectures. This alliance illustrates how the market is concentrating around firms that can deliver end‑to‑end testability solutions for heterogeneous AI silicon. The ecosystem is shaped by a handful of heavyweight EDA providers that bundle IP protection, built‑in self‑test circuitry, and runtime anomaly detection into a single workflow. Their scale enables deep integration with chip designers, while the high cost of developing AI‑centric test suites creates a barrier for newcomers, reinforcing the hierarchical structure of the market.

Beyond the dominant trio, a diverse set of specialists is carving out niche positions. Synopsys expands its portfolio with AI‑oriented verification IP, while Siemens EDA (formerly Mentor Graphics) leverages its system‑level verification heritage to address power‑dense neural accelerators. Intel’s verification division supplies in‑house DFT capabilities for its own AI processors and offers services to external fabs. Arm’s ecosystem partners, such as Qualcomm and AMD/Xilinx, embed lightweight test‑generation kernels directly into their IP blocks. Smaller innovators,including Analog Devices, Marvell, Broadcom, IBM, and TSMC‑affiliated design houses,focus on custom self‑test macros or runtime monitoring solutions that appeal to OEMs seeking differentiated safety guarantees.

List of Key AI‑Specific Design‑for‑Test Companies Profiled

- Cadence Design Systems

- NVIDIA Corporation

- Synopsys Inc.

- Siemens EDA

- Intel Corporation

- Arm Ltd.

- Qualcomm Technologies, Inc.

- AMD/Xilinx

- Analog Devices, Inc.

- Marvell Technology Group Ltd.

- Broadcom Inc.

- IBM Corporation

- TSMC Design Services

- Google Cloud AI (TensorFlow Verification)

- Samsung Electronics (AI Chip Verification)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Neural Accelerator DFT

|

| By Application |

|

Edge AI Devices

|

| By End User |

|

Chip Designers

|

| By Architecture |

|

Heterogeneous Multi‑Core

|

| By Regulatory Influence |

|

Safety Certification

|

Regional Analysis: AI-Specific Design-for-Test Market

North America

The U.S. and Canada maintain coordinated standards that encourage AI model transparency while safeguarding IP. This balance accelerates adoption of AI‑specific test suites without imposing prohibitive compliance costs, making the market more receptive to innovative solutions.

Universities in Massachusetts, Ontario, and Texas produce graduates fluent in both machine learning and test engineering, feeding a talent pool that can bridge algorithmic research with production‑grade verification.

Leading adopters include automotive semiconductor firms seeking safety‑critical validation, and data‑center chip makers that require high‑throughput pattern generation powered by AI inference.

Cloud‑based AI test platforms, coupled with flexible licensing models, lower entry barriers for midsize designers, expanding the market beyond traditional large incumbents.

Europe

European stakeholders leverage a diverse regulatory mosaic that, while fragmented, encourages cross‑border collaboration on AI‑specific verification standards. Nations such as Germany and France invest heavily in public‑private research hubs, where AI specialists co‑develop test algorithms with chip manufacturers. The region’s emphasis on sustainability influences test methodologies that optimize power consumption during verification, aligning product development with broader environmental goals. These dynamics position Europe as a fertile ground for differentiated AI‑driven test solutions that meet both performance and compliance expectations.

Asia‑Pacific

In Asia‑Pacific, a surge of domestic AI research centers located in Singapore, Japan, and South Korea fuels rapid prototyping of design‑for‑test frameworks. Local semiconductor giants are integrating AI inference engines directly into test equipment to shorten cycle times and reduce reliance on external software providers. Government incentives geared toward advanced manufacturing create a supportive backdrop for AI‑specific testing ventures, while the region’s cost‑effective engineering talent pool accelerates implementation at scale.

South America

South American markets are beginning to address the latency between AI algorithm development and test deployment by forming strategic alliances with North American EDA firms. Brazil’s emerging AI research community contributes localized expertise in language processing and sensor integration, which in turn informs test pattern generation for region‑specific applications such as agricultural technology. Although the ecosystem is still maturing, the focus on collaborative innovation signals a gradual rise in AI‑specific design‑for‑test activities.

Middle East & Africa

The Middle East & Africa region is capitalizing on sovereign technology initiatives that prioritize AI capabilities within semiconductor testing. Visionary programs in the United Arab Emirates and Israel promote the establishment of AI test labs that operate alongside traditional verification teams. Meanwhile, African tech hubs are cultivating a new generation of engineers versed in machine learning, hinting at future contributions to the global AI‑Specific Design-for-Test Market as these talent pools become more integrated into multinational supply chains.

Report Scope

This market research report provides a comprehensive analysis of the AI-Specific Design-for-Test Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Specific Design-for-Test Market?

-> AI-specific design-for-test market is projected to grow from USD 0.92 billion in 2026 to USD 1.78 billion by 2034.

Which key companies operate in AI-Specific Design-for-Test Market?

-> Key players include Cadence, NVIDIA, Synopsys, Siemens EDA, Intel, among others.

What are the key growth drivers?

-> Key growth drivers include increasing heterogeneity of AI chip architectures, rising power density requirements, and heightened regulatory scrutiny on algorithmic safety.

Which region dominates the market?

-> North America remains the largest market due to the concentration of leading semiconductor designers and early adoption of AI verification solutions.

What are the emerging trends?

-> Emerging trends include built‑in self‑test circuits for neural accelerators, automated generation of test vectors for deep‑learning models, and runtime monitoring mechanisms that detect inference anomalies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...