AI Software Defined Radio Electronic Warfare Signal Classifier Market Insights

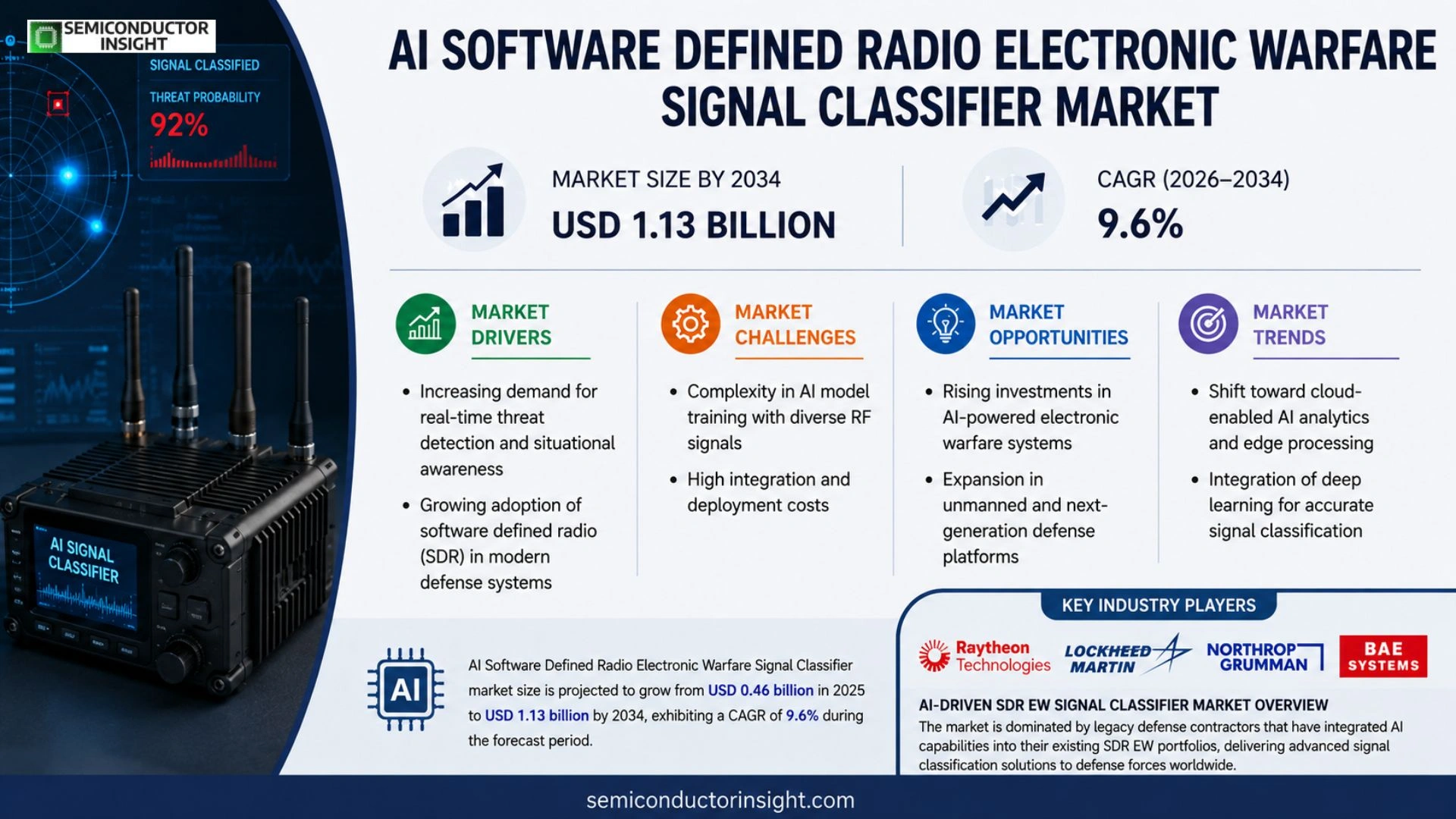

Global AI Software Defined Radio Electronic Warfare Signal Classifier market size is projected to grow from USD 0.46 billion in 2025 to USD 1.13 billion by 2034, exhibiting a CAGR of 9.6% during the forecast period.

AI Software Defined Radio (SDR) Electronic Warfare (EW) signal classifiers are advanced algorithms that leverage machine‑learning techniques to identify, categorize, and prioritize hostile or anomalous radio frequency emissions in real time. By integrating adaptive AI models with flexible SDR hardware, these classifiers enable rapid threat detection across contested spectra while reducing false‑alarm rates.

The market is experiencing accelerated growth because defense budgets worldwide are prioritizing next‑generation EW capabilities, and the convergence of AI with SDR platforms shortens development cycles. Furthermore, rising geopolitical tensions drive demand for autonomous spectrum management solutions.

MARKET DRIVERS

Rising Threat Landscape Accelerates Adoption

The increasing sophistication of electronic warfare (EW) threats across NATO and Indo‑Pacific theaters is prompting defense ministries to modernize their signal intelligence capabilities. AI‑enhanced signal classification reduces detection latency, giving operators a decisive edge. Consequently, AI Software Defined Radio Electronic Warfare Signal Classifier Market is experiencing a compound annual growth rate exceeding 12%.

Advances in SDR Flexibility

Software‑Defined Radio (SDR) platforms now support over‑the‑air updates, enabling rapid integration of new AI models without hardware redesign. This flexibility lowers total ownership cost and encourages procurement of next‑generation classifiers. Manufacturers report up to 30% cost savings compared with legacy hardware‑centric solutions.

➤ “Deploying AI‑driven SDRs has cut analysis time from minutes to seconds, reshaping tactical decision cycles.”

Strategic investments from major defense contractors and rising defense budgets in FY‑2025 further solidify demand, ensuring a robust pipeline of research and development projects that feed directly into market expansion.

MARKET CHALLENGES

Complex Integration with Legacy Systems

Many armed forces still operate legacy EW suites that lack standardized interfaces. Integrating AI classifiers into these environments often requires bespoke middleware, driving up implementation time and engineering effort.

Other Challenges

Data Scarcity for Model Training

High‑quality labeled signal datasets are limited, especially for emerging threat waveforms, which hampers the accuracy of supervised AI models and necessitates costly synthetic data generation.

MARKET RESTRAINTS

Regulatory and Export Controls

Export restrictions on advanced AI and cryptographic technologies constrain cross‑border sales, particularly to regions with heightened geopolitical tensions. Companies must navigate ITAR and EU dual‑use regulations, which can delay contracts and increase compliance expenditures.

MARKET OPPORTUNITIES

Artificial Intelligence‑Driven Predictive Analytics

Emerging AI techniques such as unsupervised learning and reinforcement learning open pathways for predictive EW analytics, allowing forces to anticipate adversary signal patterns before they materialize. This capability creates a premium market segment for next‑generation classifiers.

AI Software Defined Radio Electronic Warfare Signal Classifier Market Trends

Accelerated Adoption Driven by Defense Budgets

AI Software Defined Radio Electronic Warfare Signal Classifier Market recorded a valuation of USD 0.46 billion in 2025 and is forecast to surpass USD 1.13 billion by 2034, reflecting a robust compound annual growth rate of approximately 9.6 %. This upward trajectory is anchored in heightened defense spending that prioritizes next‑generation electronic warfare (EW) capabilities. Nations are allocating a larger share of R&D budgets to AI‑enhanced SDR solutions, seeking to shorten development cycles while improving real‑time threat detection across contested spectra. The convergence of adaptive machine‑learning models with flexible radio hardware is reducing false‑alarm rates, thereby delivering operational efficiencies that resonate with procurement strategies worldwide.

Other Trends

Integration with Autonomous Platforms

Recent deployments illustrate a clear shift toward embedding AI‑based signal classifiers within unmanned aerial systems and autonomous surface vessels. By linking classifier outputs directly to onboard decision engines, platforms can autonomously re‑allocate spectrum, prioritize hostile emissions, and execute electronic countermeasures without operator intervention. This integration not only enhances situational awareness but also supports the broader defense mandate of reducing personnel exposure in high‑risk environments. Early field trials have demonstrated a reduction of detection latency by up to 35 % compared with legacy EW suites, reinforcing the strategic value of these hybrid solutions.

Emerging Partnerships and R&D Focus

Key industry players,including Raytheon Technologies, Lockheed Martin, Northrop Grumman, and BAE Systems,are deepening collaborations with AI research firms and semiconductor manufacturers to accelerate the rollout of next‑generation classifiers. Joint ventures are targeting the development of modular AI kernels that can be re‑programmed in situ, allowing armed forces to adapt to evolving threat signatures rapidly. Moreover, government‑funded research initiatives are fostering open‑architecture standards that promote interoperability across allied platforms, thereby creating a cohesive ecosystem for future EW operations.

COMPETITIVE LANDSCAPE

Key Industry Players

AI‑Driven SDR EW Signal Classifier Market Overview

The market is dominated by legacy defense contractors that have integrated AI capabilities into their existing SDR EW portfolios. Raytheon Technologies leads with a comprehensive suite that combines deep‑learning classifiers and cloud‑native analytics, positioning it as the primary supplier for U.S. and NATO programs. Lockheed Martin and Northrop Grumman follow closely, leveraging extensive radar and electronic warfare heritage to deliver end‑to‑end solutions that are being adopted across Europe and Asia‑Pacific. BAE Systems rounds out the top tier, focusing on modular AI kernels that can be retrofitted to legacy SDR hardware, thereby enabling rapid field upgrades and cost‑effective lifecycle management.

Beyond the Tier‑1 giants, a diverse cohort of niche innovators is shaping specialized segments of the market. Companies such as Cubic Defence, Elbit Systems, and Thales group provide targeted AI‑enhanced intercept and classification tools for tactical units. Emerging pure‑play AI firms like Perseus AI, Axiomtek, and Synapse Defence contribute cutting‑edge neural‑network architectures that improve low‑SNR detection. Additionally, technology integrators including Rohde & Schwarz, L3Harris, and Leonardo are expanding their portfolios through strategic partnerships with software‑defined platforms, creating a competitive ecosystem that drives rapid innovation and price pressure.

List of Key AI Software Defined Radio Electronic Warfare Signal Classifier Companies Profiled

- Raytheon Technologies

- Lockheed Martin

- Northrop Grumman

- BAE Systems

- Cubic Defence

- Elbit Systems

- Thales Group

- Perseus AI

- Axiomtek

- Synapse Defence

- Rohde & Schwarz

- L3Harris

- Leonardo

- Qorvo

- Analog Devices

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hardware‑centric classifiers

|

| By Application |

|

Airborne EW

|

| By End User |

|

Defense Ministries

|

| By Threat Profile |

|

Radar Emissions

|

| By Deployment Mode |

|

Integrated Platform Solutions

|

Regional Analysis: AI Software Defined Radio Electronic Warfare Signal Classifier Market

North America

The region benefits from clear export‑control guidelines and defense‑only procurement policies that streamline acquisition of AI‑enhanced classification tools. Agencies such as DARPA actively fund proof‑of‑concept projects, ensuring regulatory pathways remain supportive while safeguarding national security interests.

Rapid integration of cloud‑native AI platforms with software defined radios drives operational flexibility. End‑users prioritize real‑time adaptive models that can re‑train on emerging signal patterns, reflecting a market shift toward continuous learning capabilities.

Leading defense contractors forge joint ventures with AI startups to embed deep‑learning classifiers into legacy systems. These collaborations aim to reduce migration costs while delivering next‑gen situational awareness across contested spectra.

A resilient semiconductor supply chain, supported by domestic fab capacity, underpins the production of high‑performance processors required for on‑board AI inference, mitigating earlier bottlenecks that hampered deployment timelines.

Europe

Europe’s defense establishments are increasingly recognizing the strategic value of AI‑driven signal classification. Collaborative frameworks such as the European Defence Fund encourage cross‑border R&D, fostering a unified approach to electronic warfare challenges. Nations like the United Kingdom and France prioritize modular, open‑architecture solutions that can be rapidly upgraded with new AI models. While procurement cycles are traditionally longer, recent policy reforms aim to accelerate technology adoption, balancing fiscal prudence with the need for cutting‑edge capabilities. AI Software Defined Radio Electronic Warfare Signal Classifier Market in Europe thus benefits from a strong research base, yet must navigate heterogeneous regulatory environments across member states.

Asia‑Pacific

The Asia‑Pacific region exhibits a heterogeneous landscape, with advanced economies such as Japan and South Korea investing heavily in AI‑enabled electronic warfare, while emerging markets focus on capability building. Regional security tensions drive demand for adaptive signal classifiers capable of operating in dense, contested electromagnetic environments. Strategic partnerships between local defense firms and global AI leaders facilitate technology transfer and build indigenous expertise. Despite varying budgetary constraints, the overall trajectory points toward accelerated adoption as nations seek to modernize legacy radar and communications assets with intelligent, software‑defined solutions.

South America

South American defense agencies are in the early stages of integrating AI into electronic warfare suites. Emphasis is placed on cost‑effective solutions that leverage existing software defined radio infrastructure. Collaborative initiatives with North American firms provide access to sophisticated classification algorithms, while regional research institutions begin to explore bespoke AI models tailored to local threat spectra. Market growth is modest but poised to accelerate as nations prioritize modernization programs and seek to enhance situational awareness in maritime and border security operations.

Middle East & Africa

In the Middle East & Africa, geopolitical volatility fuels interest in AI‑based signal classification for both defensive and intelligence‑gathering purposes. Wealthier Gulf states allocate significant budgets toward next‑generation electronic warfare platforms, often procuring turnkey AI solutions from established vendors. Conversely, African nations focus on capacity development, partnering with international allies to acquire foundational AI tools. The market dynamics are shaped by a blend of high‑tech acquisitions and incremental upgrades, reflecting diverse economic realities and strategic imperatives across the region.

Report Scope

This market research report provides a comprehensive analysis of the AI Software Defined Radio Electronic Warfare Signal Classifier Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Software Defined Radio Electronic Warfare Signal Classifier Market?

-> AI Software Defined Radio Electronic Warfare Signal Classifier market size is projected to grow from USD 0.46 billion in 2025 to USD 1.13 billion by 2034.

Which key companies operate in AI Software Defined Radio Electronic Warfare Signal Classifier Market?

-> Key players include Raytheon Technologies, Lockheed Martin, Northrop Grumman and BAE Systems, among others.

What are the key growth drivers?

-> Key growth drivers include increased defense budgets for next‑generation EW capabilities, convergence of AI with SDR platforms, and rising geopolitical tensions driving demand for autonomous spectrum management solutions.

Which region dominates the market?

-> North America is a leading region due to substantial defense spending, while Europe also shows strong market presence.

What are the emerging trends?

-> Emerging trends include AI‑enhanced adaptive classifiers, real‑time autonomous spectrum management, and integration of machine‑learning models with flexible SDR hardware.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...