Market Insights

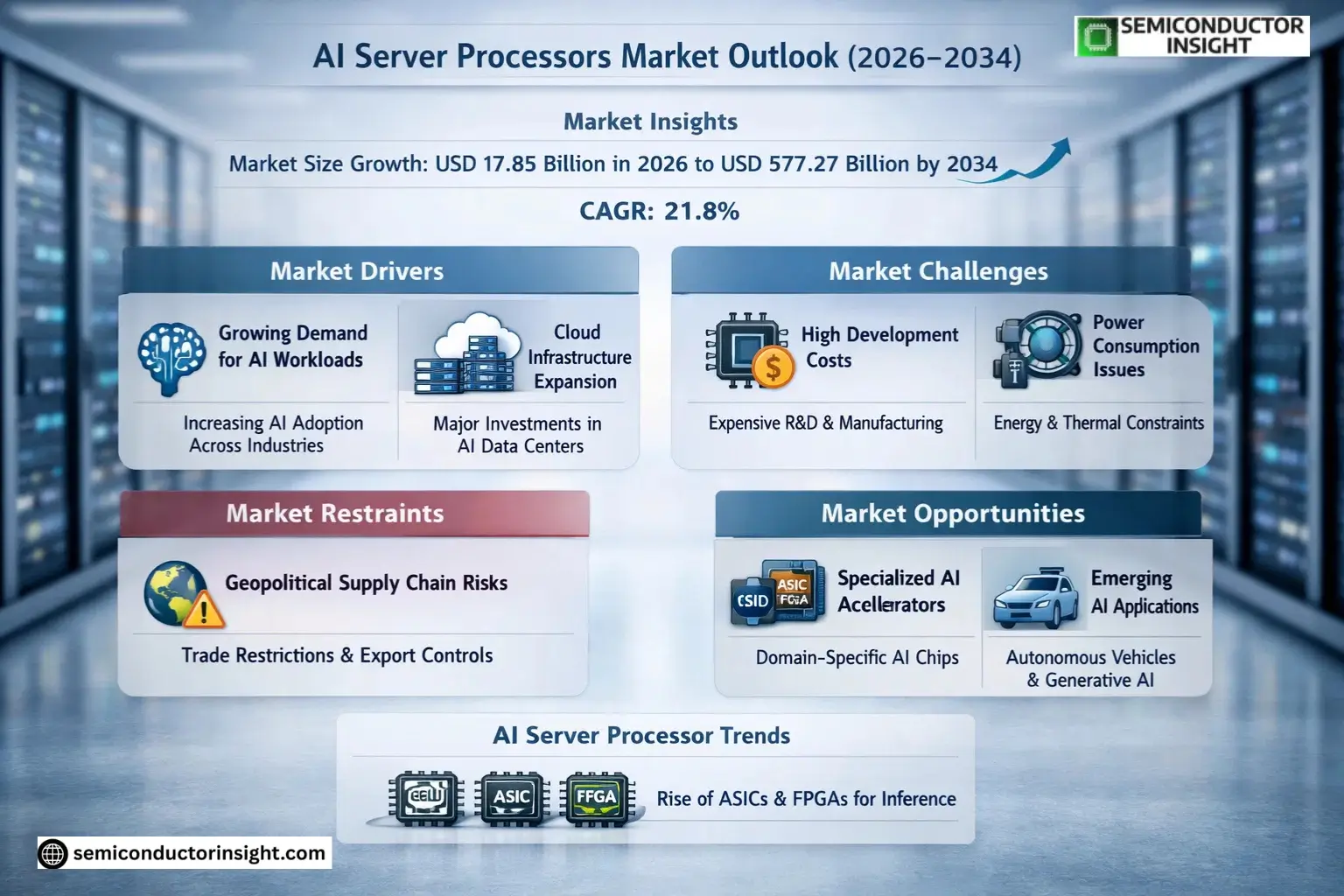

Global AI Server Processors Market size was valued at USD 14.29 billion in 2025. The market is projected to grow from USD 17.85 billion in 2026 to USD 57.27 billion by 2034, exhibiting a CAGR of 21.8% during the forecast period.

AI Server Processors (CPU+GPU+ASIC+FPGA) are specialized semiconductor components designed for high-performance computing workloads in data center environments. These processors combine host CPUs with acceleration chips like GPUs, ASICs, or FPGAs to handle artificial intelligence training and inference tasks through parallel processing architectures. The technology stack includes memory controllers, high-bandwidth interconnects, and optimized software frameworks to maximize computational efficiency for machine learning applications.

The market growth is driven by escalating demand for AI infrastructure across cloud service providers and enterprises deploying large language models. While NVIDIA dominates with its GPU-accelerated platforms, alternative architectures from AMD (Instinct MI300 series) and custom ASICs like Google’s TPU v4 are gaining traction due to their energy efficiency advantages. Recent developments include Intel’s Gaudi3 accelerator launch targeting generative AI workloads and AMD’s acquisition of Mipsology to strengthen its AI software ecosystem.

MARKET DRIVERS

Growing Demand for AI Workloads

Global AI Server Processors Market is witnessing accelerated growth due to the exponential rise in AI workloads across industries. Enterprises are increasingly adopting AI for advanced analytics, natural language processing, and computer vision, driving demand for high-performance AI server processors that can handle complex computations efficiently.

Cloud Service Providers Expanding Infrastructure

Major cloud service providers are significantly investing in AI-optimized data centers, with projected spending on AI server processors expected to exceed USD 18 billion by 2026. This expansion is creating substantial demand for next-generation processors capable of accelerating machine learning and deep learning applications at scale.

Emerging applications in autonomous vehicles and generative AI are pushing the boundaries of processor capabilities, necessitating continuous innovation in AI-optimized silicon architectures.

MARKET CHALLENGES

High Development and Manufacturing Costs

The specialized nature of AI server processor design requires significant R&D investment, with leading-edge 5nm and 3nm fabrication technologies increasing production costs by 40-60% compared to previous nodes. This cost pressure affects both vendors and end-users adopting AI infrastructure.

Other Challenges

Power Consumption Concerns

Advanced AI processors often require 400W+ per chip, creating thermal management challenges in data center environments. Energy efficiency has become a critical selection criterion for enterprise buyers.

MARKET RESTRAINTS

Geopolitical Factors Impacting Supply Chains

Trade restrictions and semiconductor export controls are creating supply chain uncertainties for AI server processor manufacturers. The concentration of advanced chip manufacturing in specific geographic regions presents logistical and political risks to market stability.

MARKET OPPORTUNITIES

Specialized AI Accelerator Adoption

The market is seeing rapid adoption of domain-specific architectures, with AI server processors optimized for particular workloads like transformer models or recommendation systems gaining traction. These specialized solutions offer 2-3x better performance per watt for targeted applications.

AI Server Processors Market Trends

Rise of Specialized AI Accelerators

AI Server Processors Market is witnessing a rapid shift toward specialized accelerators beyond traditional GPUs. ASICs and FPGAs are gaining significant traction for inference workloads due to their superior power efficiency and cost-effectiveness per operation. NVIDIA’s dominance in training workloads continues, but competitors like AMD and Intel are advancing with purpose-built accelerator designs for specific AI tasks.

Other Trends

Supply Chain Constraints Impact Growth

HBM memory shortages and advanced packaging limitations are creating bottlenecks in AI processor production. This has led to increased focus on long-term supply agreements between manufacturers and hyperscalers, with companies like TSMC expanding capacity to meet accelerating demand.

Energy Efficiency Becomes Critical

Data center power constraints are forcing innovation in processor architectures. The market is shifting from pure performance metrics to performance-per-watt evaluations, driving adoption of more efficient designs. This trend favors chipmakers who can deliver breakthrough efficiency gains while maintaining computational throughput for AI workloads.

Vertical Integration Accelerates

Leading players are moving toward full-stack solutions combining processors with networking, cooling systems, and software stacks. NVIDIA’s DGX systems and similar offerings from AMD reflect this shift toward turnkey AI infrastructure solutions that simplify deployment for enterprise customers.

Regional Market Diversification

While North America leads in AI Server Processors adoption, Asia-Pacific markets are growing rapidly, particularly in China and South Korea. Local players are developing competitive alternatives to Western chipmakers, supported by government initiatives and growing domestic AI infrastructure demand.

COMPETITIVE LANDSCAPE

Key Industry Players

NVIDIA Dominates AI Server Processor Market with 70%+ Share in 2025

NVIDIA maintains undisputed leadership in the AI server processor market, capturing over 70% revenue share in 2025 through its GPU and Blackwell platform ecosystem. The company’s vertical integration from silicon to full rack-scale solutions creates significant competitive moats. Intel and AMD follow as strong secondary players, leveraging their x86 server CPUs as host processors combined with discrete GPUs (Intel Ponte Vecchio/AMD Instinct) and AI accelerators. Emerging challengers like Huawei Ascend, Cerebras, and Groq are gaining traction in specialized AI acceleration segments.

The market exhibits a three-tier structure: 1) Full-stack silicon+system providers (NVIDIA/Intel/AMD), 2) Pure-play AI accelerator vendors (Cerebras/Graphcore/Groq), and 3) Regional champions (Huawei/Biren/Enflame in China). Chinese vendors are rapidly developing domestic alternatives, with Huawei Ascend processors now deployed in 20% of China’s AI server installations. FPGA specialists like Lattice and Achronix maintain strong positions in low-latency inference and networking offload applications where reconfigurability provides value.

List of Key AI Server Processor Companies Profiled

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices (AMD)

- Huawei Ascend (Huawei Technologies)

- Qualcomm Technologies

- IBM AI Hardware

- Cerebras Systems

- Ampere Computing

- Graphcore

- Groq

- Cambrian

- Moore Threads

- MetaX

- Shanghai Biren Technology

- Enflame

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GPU-based processors dominate AI training workloads due to their parallel processing capabilities, though constrained by HBM supply. ASICs are gaining traction for inference applications with superior cost efficiency. FPGA adoption grows for specialized low-latency workflows including network offloading and SmartNIC implementations. |

| By Application |

|

Large model training clusters drive the highest processor demand with requirements for massive parallel compute. Inference services show the fastest growth momentum as AI deployment scales, particularly for real-time applications where low-latency FPGA/ASIC solutions gain advantage over traditional GPU approaches. |

| By End User |

|

Cloud service providers represent the most significant buyer segment, driving preferences for rack-scale AI processor solutions. Enterprises show growing adoption for on-premises AI deployments, prioritizing solutions with comprehensive software stacks. Research institutions focus on cutting-edge processor capabilities for experimental AI models. |

| By Technology Focus |

|

Training-focused processors require high memory bandwidth and parallel compute capacity, making GPUs the preferred choice. Inference processors increasingly adopt specialized ASIC architectures for energy efficiency. The market is seeing convergence in architectures that can handle both training and inference workloads efficiently. |

| By Integration Level |

|

Rack-scale systems are gaining prominence as buyers seek optimized AI infrastructure solutions. The trend moves towards bundled offerings integrating processors with networking and cooling solutions. Discrete cards remain important for flexible deployments and upgrade scenarios in existing infrastructure. |

Regional Analysis: North America AI Server Processors Market

AWS, Microsoft Azure, and Google Cloud account for nearly 70% of AI processor deployments in North America. Their hyperscale data centers drive demand for both GPUs and custom AI accelerators like TPUs. Cloud-native AI services create steady processor requirements through ML-as-a-service platforms.

U.S. enterprises show above-average willingness to upgrade server infrastructure for AI workloads. Financial institutions deploy AI processors for fraud detection, while healthcare organizations use them for medical imaging analysis. The trend toward private AI clouds boosts on-premises processor sales.

Silicon Valley’s startup culture fuels specialized AI chip development, with numerous companies working on novel architectures. University partnerships with tech firms produce breakthroughs in processor efficiency. Venture capital flows freely to promising AI hardware startups developing next-generation solutions.

Export controls affect certain high-performance AI processors but stimulate domestic production. Government contracts for defense-related AI applications create specialized processor requirements. Data privacy regulations influence processor design for on-device AI capabilities in certain sectors.

Canada

Canada’s AI Server Processors Market benefits from strong academic research in machine learning and government support for AI development. Toronto, Montreal, and Vancouver emerging as important tech hubs with growing demand for AI-optimized hardware. The market sees increasing adoption in financial technology and healthcare analytics applications. While smaller than the U.S. market, Canada attracts AI investments due to favorable immigration policies for tech talent. Domestic firms collaborate with global chipmakers to implement specialized AI solutions in renewable energy and smart city projects.

Western Europe

European countries show varied adoption patterns for AI server processors influenced by digital infrastructure readiness. The UK, Germany, and France lead in implementing AI hardware, particularly in industrial automation and automotive sectors. Strict data regulations drive demand for processors enabling efficient on-premises AI processing. European tech firms increasingly collaborate with Asian and American chip designers while local semiconductor initiatives aim to reduce import dependence.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market for AI server processors, with China, Japan, and South Korea as primary demand centers. Chinese tech giants aggressively develop domestic AI chips amid trade restrictions, while Japanese firms focus on specialized processors for robotics. Cloud service expansion and 5G deployment across the region create infrastructure opportunities. Government-led AI initiatives in Singapore and India stimulate processor adoption in public sector applications.

Rest of World

Emerging markets show nascent but accelerating demand for AI server processors with middle-east nations investing in smart city projects. Israeli startups contribute innovative processor designs while Gulf states establish AI research centers. Latin American adoption remains limited but shows potential in financial services and agriculture applications. Africa’s market develops through hyperscaler expansions and select government AI programs in key economies.

Report Scope

This market research report provides a comprehensive analysis of the AI Server Processors Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of AI server processors in powering advancements across industries such as data centers, cloud computing, AI training, and inference applications.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (CPU, GPU, FPGA, ASIC), application (training, inference), deployment (cloud, edge, terminal), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Server Processors Market?

-> AI Server Processors Market size was valued at USD 14.29 billion in 2025. The market is projected to grow from USD 17.85 billion in 2026 to USD 57.27 billion by 2034, exhibiting a CAGR of 21.8% during the forecast period.

What is the growth rate of the AI Server Processors Market?

-> The market is expected to grow at a CAGR of 21.8% during the forecast period (2025-2034).

Which key companies operate in AI Server Processors Market?

-> Key players include NVIDIA, Intel, AMD, Huawei Ascend, Qualcomm, IBM, Cerebras, Ampere, Graphcore, Groq, Cambrian, Moore Threads, MetaX, Shanghai Biren Technology, Enflame, Microchip, Lattice, and Achronix, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for AI training clusters, expansion of cloud computing infrastructure, increasing adoption of edge AI solutions, and advancements in high-performance computing.

Which region dominates the market?

-> Asia is the fastest-growing region, driven by China, Japan, and South Korea, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include dedicated AI ASICs for inference workloads, rack-scale integrated solutions, reconfigurable FPGA-based accelerators, and energy-efficient processor designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...