AI Server Power Management IC Market Insights

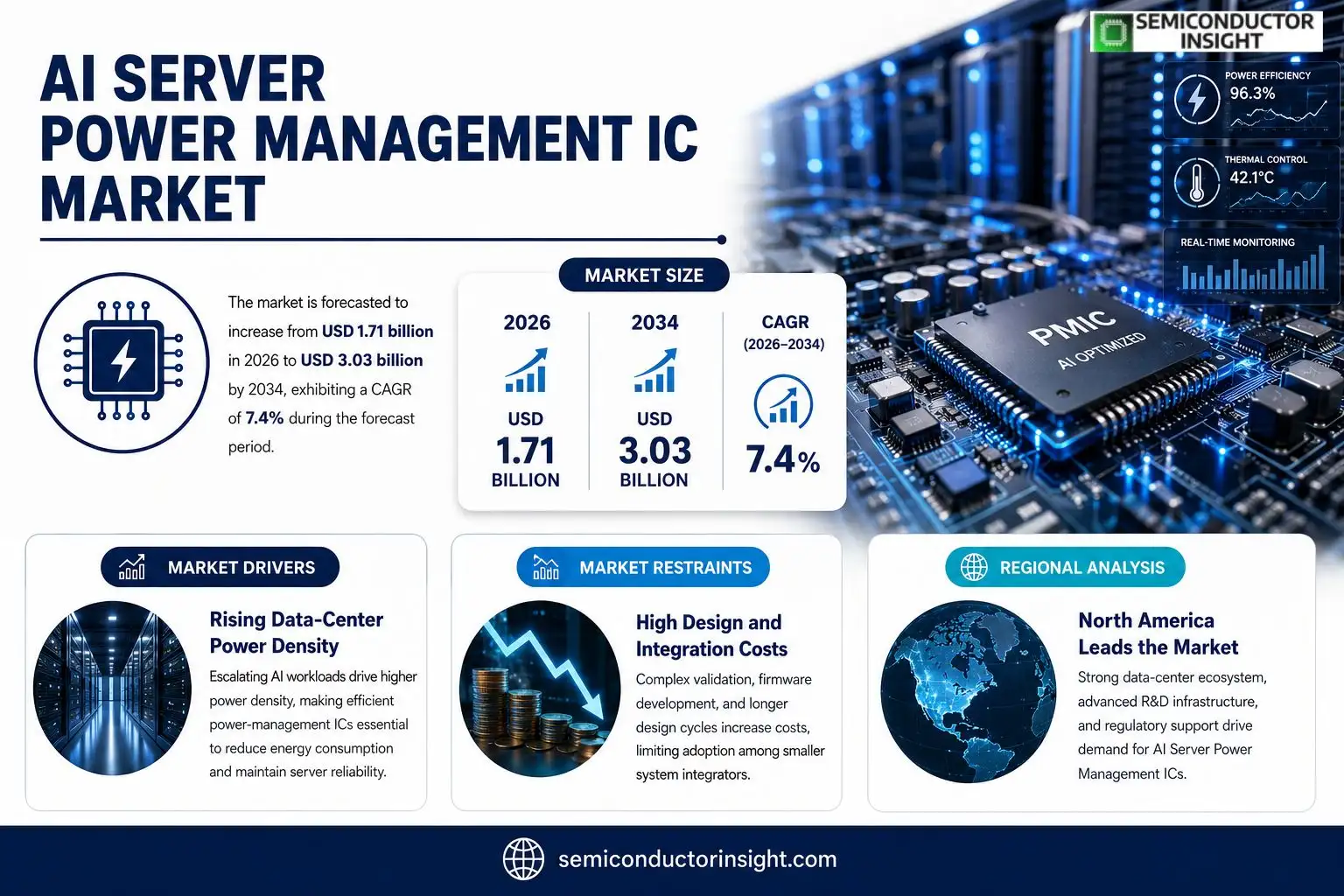

AI Server Power Management IC market size was valued at USD 1.62 billion in 2025. The market is forecasted to increase from USD 1.71 billion in 2026 to USD 3.03 billion by 2034, exhibiting a CAGR of 7.4 % during the forecast period.

AI Server Power Management ICs are specialized integrated circuits that monitor and control voltage rails, current limits, and thermal thresholds for high‑performance AI accelerators within data‑center servers. They enable dynamic scaling of power delivery while preserving computational stability and energy efficiency.The expansion is because of escalating AI model complexity, which pushes data‑center operators toward tighter power budgets and lower operating costs. Additionally, regulatory pressure on energy consumption encourages adoption of advanced power‑management silicon. Recent collaborations such as Intel’s partnership with Schneider Electric in early 2024 and Texas Instruments’ launch of a low‑latency PMIC platform illustrate how leading vendors are addressing these demands.

MARKET DRIVERS

Rising Data‑Center Power Density

Modern AI workloads push servers toward the limits of power delivery, forcing operators to confront thermal hotspots and escalating electricity bills. Efficient power‑management ICs become the linchpin for maintaining uptime while curbing waste, a reality that has already prompted many hyperscale operators to retrofit existing racks with smarter control chips.

Regulatory Pressure on Energy Consumption

Legislation across North America and Europe now mandates measurable reductions in data‑center carbon footprints. Facilities that can demonstrate precise power throttling and real‑time reporting gain a competitive edge in procurement cycles, encouraging vendors to prioritize low‑loss architectures in their product roadmaps.

➤ “Power‑management ICs that combine adaptive voltage scaling with on‑chip intelligence are reshaping cost structures for AI‑driven servers.”

The convergence of tighter power budgets and stricter compliance creates a fertile environment for AI Server Power Management IC Market to expand its addressable base, especially as AI inference workloads proliferate at the edge.

MARKET CHALLENGES

Thermal Management Complexity

As server density climbs, dissipating heat without compromising performance becomes a delicate balancing act. Power‑management ICs must now interface with advanced cooling solutions, yet many legacy designs lack the granularity to modulate power in sub‑millisecond intervals, limiting overall efficiency gains.

Other Challenges

Supply Chain Volatility

Component shortages and geopolitical tensions have stretched lead times for specialty semiconductors, forcing OEMs to hold larger inventories or accept delayed product launches, thereby dampening short‑term market momentum.

MARKET RESTRAINTS

High Design and Integration Costs

Embedding sophisticated power‑management functions requires extensive validation and firmware development, inflating bill‑of‑materials for new server platforms. Smaller system integrators, in particular, hesitate to adopt cutting‑edge ICs until economies of scale deliver affordable pricing.

MARKET OPPORTUNITIES

AI‑Driven Power Monitoring and Predictive Control

Embedding machine‑learning algorithms directly into power‑management ICs enables predictive load shifting and anomaly detection, translating into measurable reductions in operational expenditure. Early adopters report up to a 12% drop in energy costs, positioning this capability as a high‑value differentiator for AI Server Power Management IC Market.Edge‑located AI accelerators, which operate under constrained power envelopes, present another growth vector. Manufacturers that can deliver ultra‑low‑dropout regulators and adaptive buck‑boost converters within a single silicon footprint will capture a sizable share of forthcoming deployments.

AI Server Power Management IC Market Trends

Rising Demand for Energy‑Efficient Power Delivery in AI Servers

The surge in AI model complexity has forced data‑center operators to scrutinize every watt consumed by high‑performance accelerators. Power‑management ICs now act as the critical interface between power supplies and AI chips, translating fluctuating workload requirements into precise voltage and current adjustments. This capability not only safeguards computational stability but also curtails operating expenditures by trimming unnecessary energy draw. Consequently, end‑users are prioritizing platforms that embed intelligent regulation, prompting silicon vendors to embed more granular monitoring and faster response times into their designs.

Other Trends

Regulatory Influence on Power Consumption

Governments across North America and Europe have tightened reporting obligations for data‑center energy use, linking compliance to tax incentives. As a result, operators are compelled to adopt power‑management solutions that can demonstrate measurable efficiency gains. The pressure has accelerated the migration from legacy linear regulators to digital PMICs capable of real‑time adaptation, a shift that vendors are exploiting to differentiate their product portfolios.

Strategic Partnerships Accelerate Innovation

Collaboration between chip manufacturers and infrastructure providers is reshaping the development cycle. Early 2024 saw Intel align with Schneider Electric to co‑engineer a power‑delivery framework that integrates AI‑aware monitoring directly into rack‑level power distribution units. Meanwhile, Texas Instruments introduced a low‑latency PMIC platform designed for next‑generation AI accelerators, emphasizing rapid fault detection and seamless scaling. These alliances illustrate a broader industry trend: hardware designers are seeking ecosystem partners that can validate power‑management performance at scale, thereby shortening time‑to‑market and reducing integration risk for server OEMs.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of AI Server Power Management IC Market

Intel dominates the upper‑tier segment, leveraging its deep integration with data‑center architectures to bundle power‑management silicon with its Xeon and Habana accelerator families. The company’s strategic alliance with Schneider Electric accelerates adoption of its PMICs in hyperscale facilities, where fine‑grained voltage control translates directly into operational expense reductions. Texas Instruments follows closely, positioning a low‑latency PMIC platform that addresses the tight timing windows of AI inference workloads. Its broad portfolio and established OEM relationships enable it to capture a sizable share of the market’s growth, especially among vendors seeking multi‑phase buck‑boost solutions for mixed‑precision compute engines.Beyond the two titans, several specialized firms carve out niches by targeting specific design constraints. Analog Devices focuses on high‑precision current‑sense and thermal‑monitoring blocks that complement demanding AI accelerators. Maxim Integrated (now part of Analog Devices) continues to supply compact, automotive‑grade regulators that are increasingly repurposed for edge‑server modules. ON Semiconductor and NXP Semiconductors offer silicon that emphasizes low‑noise performance, appealing to customers building inference racks with strict signal‑integrity requirements. Meanwhile, Renesas, STMicroelectronics, Infineon, Microchip Technology, Rohm Semiconductor and Skyworks Solutions round out the competitive set, each delivering differentiated features—such as integrated digital twins, extended temperature ranges, or ultra‑fast response times—that allow system integrators to fine‑tune power envelopes for varied AI workloads.

List of Key AI Server Power Management IC Companies Profiled

- Intel Corporation

- Texas Instruments

- Analog Devices, Inc.

- Maxim Integrated

- ON Semiconductor

- NXP Semiconductors

- Renesas Electronics Corporation

- STMicroelectronics

- Infineon Technologies AG

- Microchip Technology Inc.

- Rohm Semiconductor

- Skyworks Solutions, Inc.

- Dialog Semiconductor (Renesas)

- Power Integrations, Inc.

- Vicor Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Switching Power Management ICs

|

| By Application |

|

AI Accelerator Power Delivery

|

| By End User |

|

Cloud Service Providers

|

| By Power Architecture |

|

Point‑of‑Load Architecture

|

| By Integration Level |

|

System‑on‑Chip Integrated PMICs

|

Regional Analysis: AI Server Power Management IC Market

North America

Large‑scale operators are redesigning power distribution networks to embed AI‑aware ICs that fine‑tune consumption per rack. The shift from static to dynamic power budgets reduces operating expense and extends hardware refresh cycles, prompting OEMs to prioritize these modules in next‑gen server platforms.

Edge locations, from telecom hubs to autonomous‑vehicle depots, demand compact power‑management solutions that reconcile limited cooling capacity with bursty inference workloads. Vendors that offer tight integration with low‑latency AI accelerators gain a distinct competitive advantage in this emerging segment.

Clusters around Silicon Valley and Boston foster collaborative R&D between chip designers and AI algorithm specialists. This proximity accelerates co‑design cycles, allowing power‑management ICs to anticipate workload patterns generated by transformer‑based models.

Energy‑efficiency standards enacted by the EPA and state agencies pressure data‑center operators to adopt smarter power controls, driving demand for ICs that can certify compliance without sacrificing performance.

Europe

European data‑center operators are navigating a regulatory landscape that emphasizes carbon accounting, prompting a strategic pivot toward power‑management ICs capable of granular metering. Nations such as Germany and France provide subsidies for retrofitting legacy servers with energy‑aware silicon, encouraging OEMs to tailor their product lines for the region’s stringent reporting requirements. Meanwhile, the Nordics leverage abundant renewable power, which raises expectations for hardware that can dynamically align compute intensity with green‑energy availability. This combination of policy pressure and abundant clean power creates a niche where power‑management ICs become pivotal in achieving both cost savings and ESG objectives.

Asia‑Pacific

The Asia‑Pacific market blends rapid data‑center expansion with a cost‑sensitive manufacturing base. China’s aggressive AI infrastructure roll‑out and India’s burgeoning cloud services sector generate a sustained appetite for power‑management ICs that can sustain high density while keeping thermal footprints low. Local semiconductor firms are increasingly embedding AI‑driven power‑control loops directly into ASIC designs, reducing the bill of materials and shortening time‑to‑market. Cross‑border collaborations, especially between Japanese precision‑engineers and Korean memory producers, are elevating the sophistication of these ICs, positioning the region as a hotbed of innovative, cost‑effective solutions.

South America

In South America, market momentum is anchored by Brazil’s expanding cloud footprint and the region’s reliance on intermittent renewable sources. Power‑management ICs that can adapt to fluctuating grid conditions are gaining traction, as operators seek to avoid costly downtime caused by voltage instability. Local OEMs are partnering with South‑American utilities to pilot adaptive power‑saving algorithms that align server workloads with periods of excess solar generation, thereby lowering operating expenses and reinforcing grid resilience.

Middle East & Africa

The Middle East’s high‑temperature environments compel data‑center owners to prioritize thermal efficiency, making intelligent power‑management ICs essential for maintaining server reliability. Investments from sovereign wealth funds into AI‑focused data hubs have accelerated demand for components that can balance performance with aggressive cooling constraints. In Africa, nascent cloud infrastructures rely heavily on energy‑efficient hardware to offset limited power infrastructure, prompting early adopters to source ICs that enable fine‑grained power scaling and reduce overall capital outlay.

Report Scope

This market research report provides a comprehensive analysis of the AI Server Power Management IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Server Power Management IC Market?

-> AI Server Power Management IC Market was valued at USD 1.62 billion in 2025 and is expected to reach USD 3.03 billion by 2034.

Which key companies operate in AI Server Power Management IC Market?

-> Key players include Intel, Texas Instruments, Schneider Electric, among others.

What are the key growth drivers?

-> Key growth drivers include escalating AI model complexity, tighter power budgets, and regulatory pressure on energy consumption.

Which region dominates the market?

-> North America leads the market, while Asia‑Pacific shows rapid growth.

What are the emerging trends?

-> Emerging trends include low‑latency PMIC platforms, AI‑optimized power management, and strategic partnerships such as Intel‑Schneider Electric.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...