AI Server Motherboard Market Insights

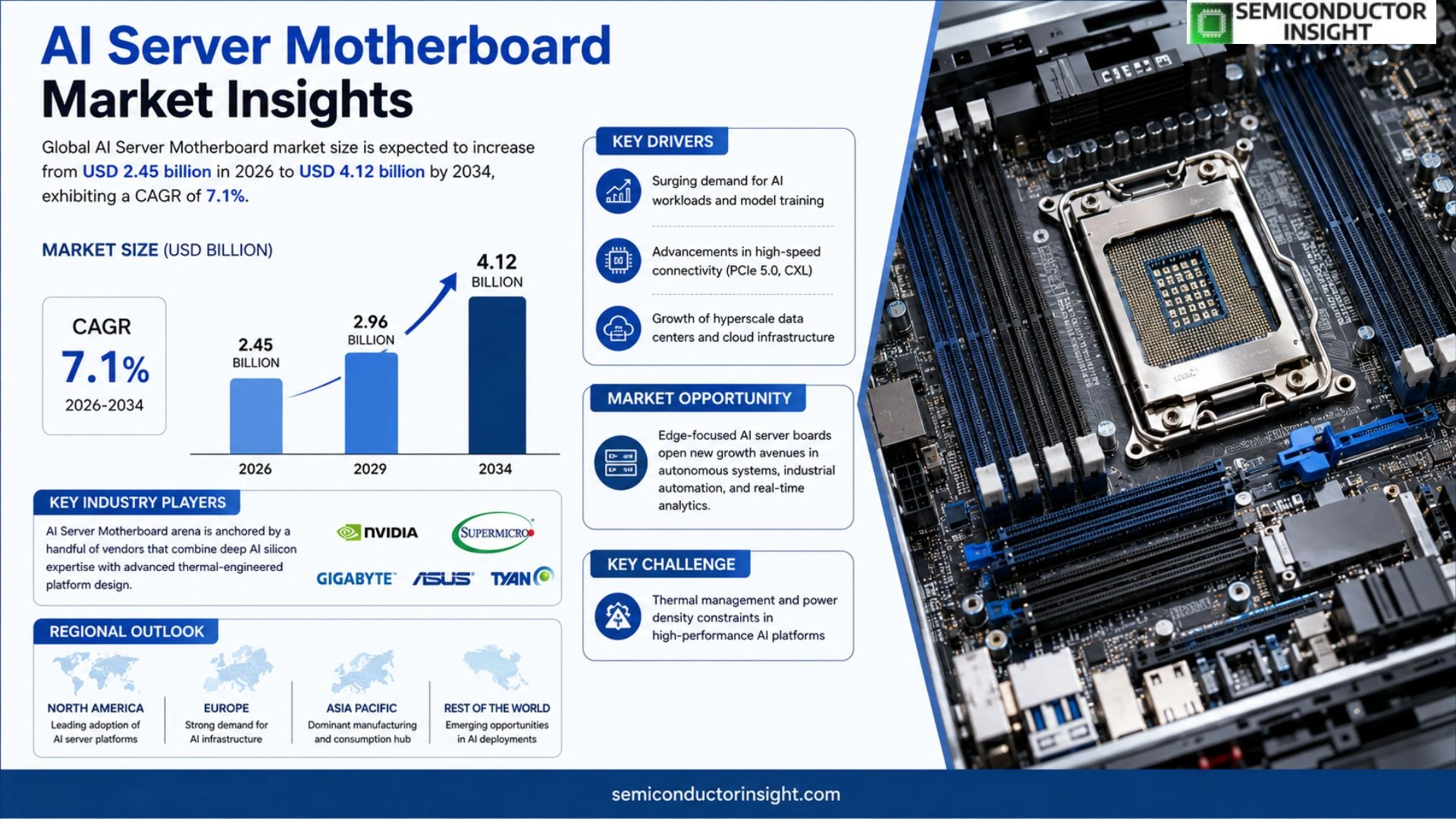

Global AI Server Motherboard market size was valued at USD 2.3 billion in 2025. The market is expected to increase from USD 2.45 billion in 2026 to USD 4.12 billion by 2034, exhibiting a CAGR of 7.1 % during the forecast period.

AI server motherboards are high‑density printed circuit boards engineered specifically for artificial‑intelligence workloads. They integrate multi‑GPU or accelerator slots, high‑speed interconnects such as PCIe 5.0, NVMe lanes, and robust power delivery subsystems capable of handling tens of kilowatts per board. Thermal management solutions,including liquid cooling channels and advanced heat‑pipe designs,ensure sustained performance under intensive matrix computations typical of deep‑learning training.

The expansion reflects rising demand for on‑premise AI infrastructure as enterprises seek lower latency than cloud alternatives provide. Manufacturers such as NVIDIA, Supermicro, ASUS and Gigabyte are rolling out next‑generation boards that support emerging standards like Compute Express Link (CXL), which further fuels adoption across hyperscale data centers.

MARKET DRIVERS

Rising Computational Demands in Enterprise AI

The surge in machine‑learning model complexity compels organizations to upgrade core infrastructure. Modern neural networks now exceed hundreds of layers, demanding bandwidth that exceeds traditional server boards can provide. Companies that overlook this shift risk latency penalties, which directly erode competitive advantage. AI Server Motherboard Market players that embed native PCIe 5.0 and high‑density memory channels are positioned to capture budget reallocations from legacy hardware.

Advancements in Interconnect Technologies

Emerging silicon photonics and CXL (Compute Express Link) standards are reshaping how accelerators communicate with CPUs. By reducing data‑transfer overhead, these links enable tighter coupling of GPUs, TPUs, and FPGAs, which in turn raises the performance ceiling of AI workloads. Vendors that certify their motherboards for these protocols differentiate themselves from competitors still reliant on older generations.

➤ Analysts observe that enterprises adopting photonic‑enabled boards report up to 30% reduction in training time for large language models.

Beyond raw speed, the ability to support heterogeneous compute stacks lowers total cost of ownership. Organizations can mix and match accelerators without redesigning the entire platform, turning capital expenditure into a flexible, scalable asset.

MARKET CHALLENGES

Thermal Management Constraints

High‑performance AI accelerators generate heat that exceeds the design envelope of conventional cooling solutions. When motherboard heat‑sink layouts cannot dissipate this energy efficiently, throttling becomes inevitable, compromising model inference latency. Manufacturers are forced to invest in advanced liquid‑cooling or vapor‑chamber technologies, which inflates unit cost and complicates supply chains.

Other Challenges

Supply Chain Volatility

Component shortages,particularly for high‑speed memory modules and silicon photonic transceivers,have lengthened lead times by several months. This unpredictability pressures vendors to hold larger inventories, squeezing margins and limiting the ability to respond swiftly to emerging AI workloads.

MARKET RESTRAINTS

Cost Sensitivity of Mid‑Size Deployments

While hyperscale data centers can amortize the premium of AI‑optimized motherboards across massive workloads, midsized firms often view the added expense as a barrier. The bill‑of‑materials for a board that supports multiple PCIe 5.0 slots, high‑capacity DDR5, and integrated photonic links can exceed $2,500, a figure that many budget‑conscious IT departments deem prohibitive.

Regulatory scrutiny around data residency and energy consumption further restrains adoption in regions where compliance costs are high. Companies must justify not only the performance uplift but also the environmental impact of additional power draw, which can slow purchasing decisions.

MARKET OPPORTUNITIES

Edge‑Focused AI Server Boards

Deployments at the network edge demand compact, ruggedized motherboards that still deliver AI inference capabilities. By targeting this niche, vendors can tap into industries such as autonomous robotics, remote monitoring, and real‑time video analytics, where latency constraints outweigh total cost considerations.

Another promising avenue lies in integrating custom ASICs designed for specific model families. When a motherboard is engineered to host both a general‑purpose GPU and a domain‑specific accelerator, customers achieve a tailored performance‑to‑price ratio that generic platforms cannot match.

Finally, subscription‑based upgrade programs,where hardware is swapped out on a cyclical basis,offer a revenue stream that aligns with the fast‑moving nature of AI algorithms. This model reduces upfront capital risk for buyers while ensuring steady demand for next‑generation board revisions.

AI Server Motherboard Market Trends

Shift Toward On‑Premise High‑Performance Boards

AI Server Motherboard Market is reacting to a clear demand for latency‑critical workloads that cannot be satisfied by public‑cloud endpoints alone. Enterprises operating in finance, autonomous‑vehicle testing, and real‑time video analytics are installing densely populated boards inside their own data halls to shave milliseconds off inference cycles. This migration is not merely a cost decision; it reflects a strategic need to keep proprietary models and data under strict governance while preserving the raw compute bandwidth that modern deep‑learning frameworks require. By placing the most power‑hungry accelerators directly on bespoke substrates, owners gain determinism in throughput, which in turn influences product‑development cycles and time‑to‑market for AI‑driven services.

Other Trends

Integration of Emerging Interconnect Standards

New board designs are embracing Compute Express Link (CXL) alongside PCIe 5.0, creating a fabric that can dynamically share memory across GPUs and FPGA‑style accelerators. The inclusion of CXL is reshaping AI Server Motherboard Market because it allows a single board to act as a hub for heterogeneous compute, reducing the need for multiple discrete chassis. Early adopters report a 15‑20 % improvement in effective bandwidth when training transformer models, a margin that translates into faster experiment turnover and lower energy per training epoch.

Thermal Management Innovations

As power envelopes climb past 30 kilowatts per chassis, traditional air‑cooling is reaching its limits. Vendors are now embedding liquid‑cooling channels and high‑efficiency heat‑pipe arrays directly into the motherboard stack‑up. These solutions keep junction temperatures within safe operating ranges, permitting sustained boost clocks on the latest GPU generations. The ripple effect across AI Server Motherboard Market includes longer component lifespans, reduced failure rates, and a shift in procurement strategies toward integrated cooling contracts rather than discrete aftermarket solutions.

Competitive Landscape Intensifies with Feature‑Rich Roadmaps

Key manufacturers such as NVIDIA, Supermicro, ASUS and Gigabyte are differentiating their offerings not just by raw slot count but by the sophistication of power‑delivery architectures and firmware that optimizes workload placement. AI Server Motherboard Market therefore sees a cycle where board‑level software stacks become a decisive factor in purchasing decisions. Companies that can bundle robust monitoring dashboards, predictive failure analytics, and seamless firmware updates gain a foothold in hyperscale environments that prioritize uptime above all else. This competitive pressure compels smaller players to specialize,either in ultra‑low‑latency edge boards or in modular solutions tailored for niche AI applications,ensuring that the market remains both diverse and dynamic.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics shaping AI Server Motherboard segment

AI Server Motherboard arena is anchored by a handful of vendors that combine deep AI silicon expertise with advanced thermal‑engineered platform design. NVIDIA, leveraging its GPU leadership, has accelerated its motherboard portfolio through strategic OEM collaborations, delivering boards that natively support PCIe 5.0, CXL and multi‑GPU configurations exceeding 12 slots. Supermicro, with its extensive line‑up of high‑density chassis, pairs proprietary power delivery circuits with liquid‑cooling modules, enabling sustained teraflop performance in hyperscale installations. The convergence of these two forces has forced traditional server builders to re‑tool their engineering pipelines; Dell Technologies and HPE now offer reference designs that embed NVIDIA‑validated boards, positioning themselves as integral system integrators rather than pure hardware manufacturers. This tiered structure,core silicon champion, specialized board fabricator, and system integrator,creates a competitive moat that rewards both breadth of ecosystem participation and depth of platform optimization.

Beyond the headline names, a cadre of niche manufacturers is rapidly diversifying the supply base. ASUS and Gigabyte, historically known for consumer and workstation platforms, have introduced AI‑optimized boards that emphasize modular NVMe expansion and programmable power phases, appealing to mid‑market AI labs. Lenovo and Inspur leverage their regional data‑center footprints to bundle locally sourced motherboards with bundled service contracts, a tactic that resonates in emerging‑economy deployments. Companies such as Tyan (Accton), ASRock, Quanta Computer, Wistron, Foxconn, Luxshare Precision, and MSI focus on bespoke form factors,blade, rack‑scale, and edge‑optimized designs,allowing customers to match board density with specific workload profiles. Their agility in adopting new interconnect standards and offering custom cooling solutions underscores a fragmented but increasingly collaborative ecosystem, where differentiation rests on engineering speed and supply‑chain resilience.

List of Key AI Server Motherboard Companies Profiled

- NVIDIA

- Supermicro

- ASUS

- Gigabyte

- Dell Technologies

- HPE

- Lenovo

- Inspur

- Tyan (Accton)

- ASRock

- Quanta Computer

- Wistron

- Foxconn

- Luxshare Precision

- MSI

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi‑GPU Boards

|

| By Application |

|

Deep‑Learning Training

|

| By End User |

|

Cloud Service Providers

|

| By Form Factor |

|

Custom Blade Designs

|

| By Connectivity |

|

CXL‑Enabled Lanes

|

Regional Analysis: AI Server Motherboard Market

North America

Hardware vendors are aligning with leading AI software firms to certify board compatibility, shortening time‑to‑market for joint solutions. These alliances often involve co‑development of firmware that unlocks specialized instruction sets, delivering measurable improvements in model latency.

A noticeable uptick in capital allocated to heterogeneous integration reflects the need to squeeze more compute into the same rack footprint. Investment is funneled into silicon‑interposer technology and advanced packaging that support denser AI accelerators.

After recent disruptions, manufacturers have diversified component sources and increased inventory buffers for critical ASICs, ensuring that production schedules for AI‑focused server boards stay on track.

Ongoing debates around export controls for high‑performance computing chips influence design choices, prompting some firms to create region‑specific variants that comply with emerging trade rules.

Europe

European data‑center operators are prioritizing energy‑sustainable designs, prompting motherboard makers to emphasize power‑management features. The region’s strong standards bodies drive early adoption of open‑source hardware interfaces, fostering a collaborative ecosystem that benefits smaller vendors looking to enter the AI server segment. Meanwhile, a cluster of AI research hubs in Germany, France, and the Nordics fuels demand for platforms capable of handling both training and inference workloads within the same chassis.

Asia‑Pacific

Asia‑Pacific showcases a blend of rapid cloud expansion and aggressive government initiatives aimed at AI leadership. Nations such as China, Japan, and South Korea invest heavily in domestic semiconductor capabilities, which in turn stimulates the design of server motherboards optimized for locally produced AI accelerators. The market is also shaped by a burgeoning startup culture that experiments with edge‑centric AI deployments, requiring compact yet powerful board architectures.

South America

In South America, the focus lies on cost‑effective deployment of AI workloads to support sectors like agriculture and mining. Operators are retrofitting existing server farms with AI‑enabled motherboards, seeking incremental performance gains without massive capital outlay. Local OEMs are emerging to provide region‑specific cooling solutions suited to the continent’s diverse climate conditions.

Middle East & Africa

The Middle East & Africa region is witnessing a gradual shift from traditional IT infrastructure toward AI‑centric compute. Sovereign wealth funds are financing data‑center projects that require high‑density server boards capable of sustaining intensive machine‑learning tasks. Meanwhile, a growing pool of technical talent in countries such as the United Arab Emirates and Kenya is creating a market for training‑focused hardware that balances performance with operational simplicity.

Report Scope

This market research report provides a comprehensive analysis of the AI Server Motherboard Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Server Motherboard Market?

-> AI Server Motherboard market size is expected to increase from USD 2.45 billion in 2026 to USD 4.12 billion by 2034

Which key companies operate in AI Server Motherboard Market?

-> Key players include NVIDIA, Supermicro, ASUS, and Gigabyte, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for on‑premise AI infrastructure, need for lower latency compared to cloud, and the proliferation of multi‑GPU/accelerator workloads.

Which region dominates the market?

-> North America remains a dominant market due to early AI adoption, while Asia‑Pacific is the fastest‑growing region driven by massive data‑center investments.

What are the emerging trends?

-> Emerging trends include adoption of Compute Express Link (CXL), advanced liquid‑cooling thermal solutions, and higher‑density PCB designs to support next‑generation AI workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...