AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market Insights

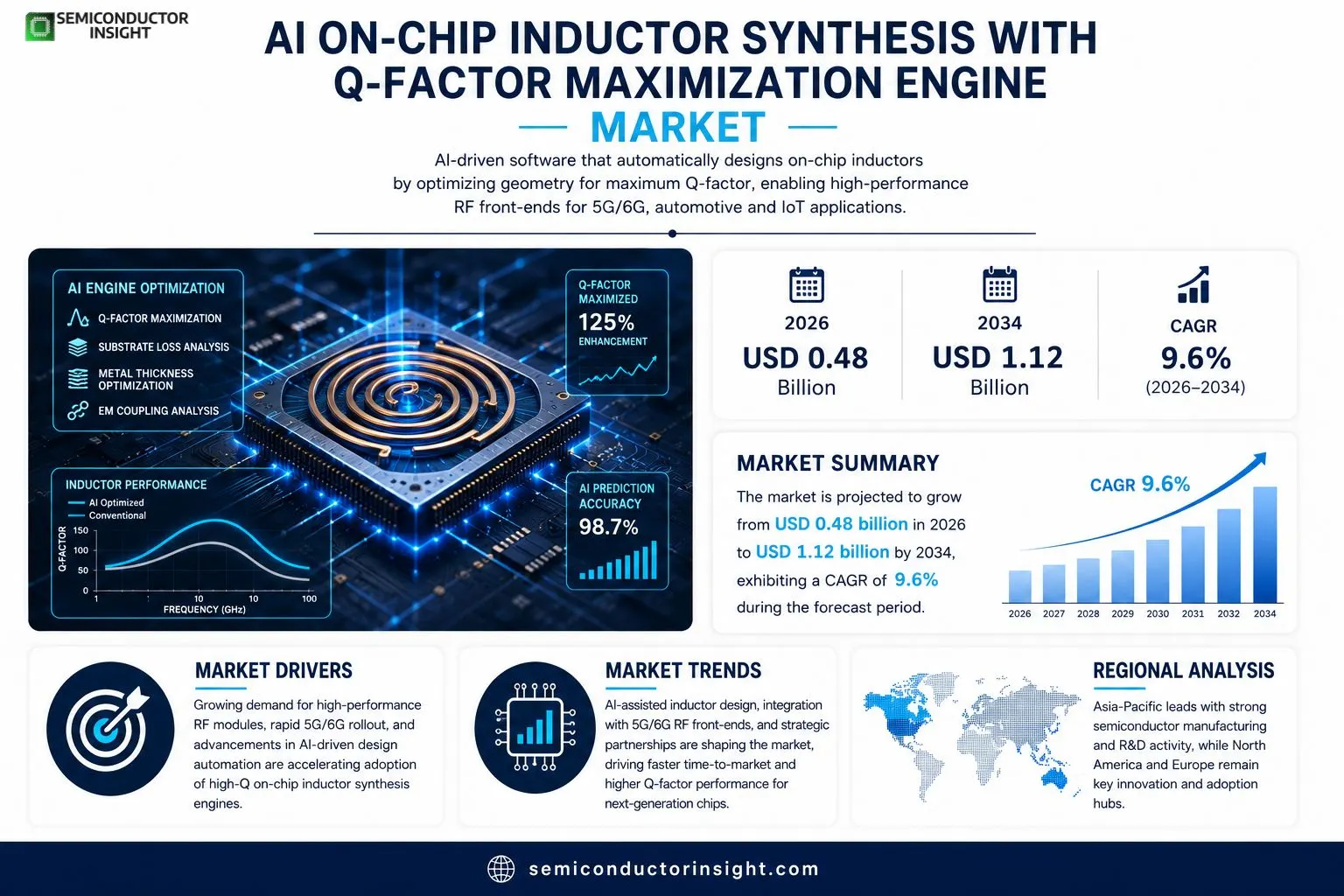

AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 1.12 billion by 2034, exhibiting a CAGR of 9.6% during the forecast period.

AI On‑Chip Inductor Synthesis with Q‑Factor Maximization Engine refers to an advanced software suite that employs machine‑learning algorithms to automatically generate on‑chip spiral or planar inductors while optimizing geometry for maximum quality factor (Q). The engine evaluates substrate losses, metal thickness, and electromagnetic coupling to deliver designs that meet stringent RF performance targets for wireless, automotive and IoT applications.The market is experiencing rapid growth because semiconductor manufacturers are accelerating integration of RF front‑ends onto silicon, driving demand for compact high‑Q inductors. Furthermore, the rise of 5G/6G infrastructure and edge‑computing devices pushes designers toward AI‑assisted tools that reduce time‑to‑market. Key players such as Cadence Design Systems, Synopsys Inc., Ansys Ltd., and Keysight Technologies are expanding their portfolios through strategic partnerships and acquisitions, further fueling adoption of the synthesis engine.

MARKET DRIVERS

Rising Demand for High‑Performance RF Modules

The proliferation of 5G infrastructure and advanced automotive radar systems is compelling chipset manufacturers to seek higher Q‑factor inductors that can operate at microwave frequencies without excessive loss. This trend directly fuels growth in AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market as designers adopt AI‑enabled tools to meet stringent performance targets.

Advancements in AI‑Driven Design Automation

Recent breakthroughs in generative AI algorithms enable rapid topology optimization of on‑chip inductors, reducing design cycles from weeks to days. Companies that integrate these engines into their EDA suites report 30 % faster time‑to‑market, creating a strong incentive for further investment.

➤ “AI‑assisted synthesis is becoming the de‑facto standard for achieving ultra‑high Q‑factor in silicon‑based inductors.”

Combined, the pressure to deliver compact, low‑loss RF front‑ends and the availability of sophisticated AI tools are the principal catalysts driving the market forward.

MARKET CHALLENGES

Design Complexity and Validation

Optimizing inductance values while simultaneously maximizing Q‑factor introduces a multidimensional trade‑off space. Traditional simulation loops struggle with convergence, making validation time‑consuming and costly for OEMs.

Other Challenges

Manufacturing Yield Constraints

Process variations in deep‑submicron CMOS steps can cause significant Q‑factor deviations, limiting the scalable adoption of AI‑generated designs without robust yield‑aware post‑processing.

MARKET RESTRAINTS

Limited Access to Proprietary Q‑Factor Models

Many leading semiconductor firms treat their high‑accuracy electromagnetic models as trade secrets, restricting the data pool available to AI synthesis engines. This barrier hampers the ability of newer entrants to create equally effective designs and slows overall market diffusion.

MARKET OPPORTUNITIES

Emerging 5G and Automotive Radar Applications

The rollout of 5G mmWave networks and the push for autonomous‑driving radar demand inductors with exceptionally high Q‑factors in ultra‑compact footprints. AI‑driven synthesis platforms are uniquely positioned to meet these specifications, representing a high‑growth opportunity for vendors that can bridge the gap between algorithmic design and manufacturable silicon.

AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market Trends

Accelerated Adoption of AI‑Driven Inductor Design

Design teams are increasingly turning to AI‑based synthesis engines to automate the creation of on‑chip spiral and planar inductors. The software evaluates substrate loss, metal thickness, and electromagnetic coupling in real time, delivering geometries that achieve the highest feasible quality factor (Q). By reducing manual iteration cycles, the technology shortens time‑to‑market for RF front‑ends used in wireless, automotive, and IoT devices. The convergence of AI optimization with advanced process nodes is creating a measurable shift toward fully integrated RF solutions on silicon.

Other Trends

Integration with 5G/6G RF Front‑Ends

The rollout of 5G networks and the early research into 6G have heightened the need for compact, high‑Q inductors that operate efficiently at millimeter‑wave frequencies. AI synthesis tools enable designers to tailor inductor layouts that meet stringent loss and linearity requirements while fitting within the limited real‑estate of modern System‑on‑Chip (SoC) dies. This capability is driving broader adoption across telecommunications equipment manufacturers and semiconductor fabs that prioritize vertical integration of RF components.

Strategic Partnerships and Portfolio Expansion

Major EDA vendors such as Cadence, Synopsys, Ansys, and Keysight are forming alliances with semiconductor manufacturers to embed AI synthesis engines directly into existing design flows. These collaborations often include joint development agreements, licensing models, and co‑marketing initiatives that accelerate customer uptake. By bundling the AI engine with simulation, verification, and layout tools, providers create a seamless workflow that reduces engineering overhead and improves design predictability.Collectively, these trends indicate a market moving toward tighter integration of AI‑enhanced design automation within the semiconductor ecosystem. Companies that adopt the synthesis engine early are positioned to capture performance advantages in emerging wireless standards, while the broader industry benefits from a more rapid, data‑driven design paradigm.

COMPETITIVE LANDSCAPE

Key Industry Players

AI On‑Chip Inductor Synthesis with Q‑Factor Maximization Engine Market Overview

The AI‑driven on‑chip inductor synthesis market is currently led by a small group of integrated circuit design‑software giants that combine extensive EDA platforms with specialized RF optimization modules. Cadence Design Systems, Synopsys Inc., Ansys Ltd., and Keysight Technologies dominate the ecosystem by offering end‑to‑end simulation, layout automation, and Q‑factor maximization engines that are tightly coupled with foundry design‑kits. Their deep relationships with semiconductor fabs and strong IP libraries create a high barrier to entry, resulting in a market structure that favors a few large players while smaller innovators focus on niche algorithmic enhancements or vertical integrations for automotive and 5G/6G front‑ends.Beyond the primary quartile, several niche and component‑oriented firms contribute differentiated capabilities. Mentor, now part of Siemens EDA, provides advanced electromagnetic solvers that complement AI synthesis workflows. NI‑AWR and Sonnet Technologies deliver focused RF‑centric tools that integrate AI‑assisted geometry tuning. Component manufacturers such as Murata, TDK, Qorvo, Skyworks, and Analog Devices supply high‑Q on‑chip inductor libraries and reference designs, often partnering with the major EDA vendors to embed their models. Additional semiconductor leadersincluding Qualcomm, Intel, NXP, and Broadcomare investing in internal AI design engines to accelerate custom RF front‑end development, further enriching the competitive landscape.

List of Key AI On‑Chip Inductor Synthesis with Q‑Factor Maximization Engine Companies Profiled

- Cadence Design Systems

- Synopsys Inc.

- Ansys Ltd.

- Keysight Technologies

- Siemens EDA (Mentor Graphics)

- NI‑AWR (National Instruments)

- Sonnet Technologies

- Murata Manufacturing

- TDK Corporation

- Qorvo, Inc.

- Skyworks Solutions

- Analog Devices, Inc.

- Qualcomm Technologies, Inc.

- Intel Corporation

- NXP Semiconductors

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Spiral Focused Solutions

|

| By Application |

|

Wireless Communications

|

| By End User |

|

Semiconductor Foundries

|

| By Design Complexity |

|

Multi‑Layer Stacked Inductors

|

| By Integration Level |

|

Embedded RF Front‑End Modules

|

Regional Analysis: AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market

North America

The United States leads in advanced process development, with major fabs integrating AI‑driven magnetic synthesis tools to push Q‑factor limits. Industry consortia focus on co‑design of inductor libraries that align with AI accelerator architectures, accelerating time‑to‑market for high‑performance chips.

Canadian research hubs specialize in low‑loss magnetic materials, providing critical know‑how for Q‑factor maximisation. Partnerships with U.S. firms translate these insights into scalable on‑chip inductor designs for AI workloads.

Mexico’s growing design‑service sector offers cost‑effective engineering support for AI chip makers, focusing on integration of compact inductors that meet stringent power‑budget constraints.

Cross‑border collaborations are fostering novel AI‑enabled synthesis algorithms that dynamically optimise inductor geometry, ensuring superior Q‑factor performance across diverse operating conditions.

Europe

Europe’s fragmented yet innovative landscape drives niche advancements in AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market. Germany’s precision manufacturing and France’s emphasis on sustainable semiconductor processes create a strong foundation for high‑efficiency magnetic component development. Collaborative EU research programmes encourage standardisation of synthesis workflows, enabling smaller firms to contribute specialized algorithms that improve inductor performance. While overall market share lags behind North America, Europe’s focus on reliability and regulatory compliance positions it as a valuable partner in value chain.

Asia‑Pacific

The Asia‑Pacific region, led by China, Japan, and South Korea, exhibits rapid adoption of AI‑centric chip design practices. Extensive fab capacity and aggressive government incentives accelerate the rollout of on‑chip inductors with enhanced Q‑factors. Regional players leverage dense design ecosystems to iterate synthesis tools quickly, catering to high‑volume consumer electronics and automotive AI applications. Although intellectual‑property concerns persist, the sheer scale of production reinforces the region’s growing influence on market dynamics.

South America

South America remains an emerging contributor, with Brazil and Chile nurturing early‑stage startups focused on AI‑optimized magnetic components. Investment in local semiconductor education and modest R&D grants encourage experimentation with novel material blends that can boost Q‑factor performance. While the market is still nascent, the region’s emphasis on cost‑effective solutions may attract niche AI hardware projects seeking affordable on‑chip inductors.

Middle East & Africa

In the Middle East & Africa, market activity is primarily driven by strategic partnerships and research initiatives rather than large‑scale production. United Arab Emirates and South Africa host innovation hubs that explore AI‑assisted inductor synthesis, emphasizing energy‑efficient designs for telecom infrastructure. Limited manufacturing capacity is offset by collaborations with North American and European firms, allowing the region to contribute specialized expertise in Q‑factor optimisation for emerging AI applications.

Report Scope

This market research report provides a comprehensive analysis of the AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market?

-> AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 1.12 billion by 2034.

Which key companies operate in AI On-Chip Inductor Synthesis with Q-Factor Maximization Engine Market?

-> Key players include Cadence Design Systems, Synopsys Inc., Ansys Ltd., and Keysight Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include accelerating integration of RF front‑ends onto silicon, rising demand for compact high‑Q inductors, and the expansion of 5G/6G infrastructure and edge‑computing devices.

Which region dominates the market?

-> Asia‑Pacific is showing strong growth due to a concentration of semiconductor manufacturing and R&D activities, while North America and Europe remain significant markets.

What are the emerging trends?

-> Emerging trends include AI‑assisted inductor design automation, integration of machine‑learning optimization for Q‑factor enhancement, and the convergence of RF design tools with broader system‑level AI/IoT platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...