AI Memory Pooling Solutions Market Insights

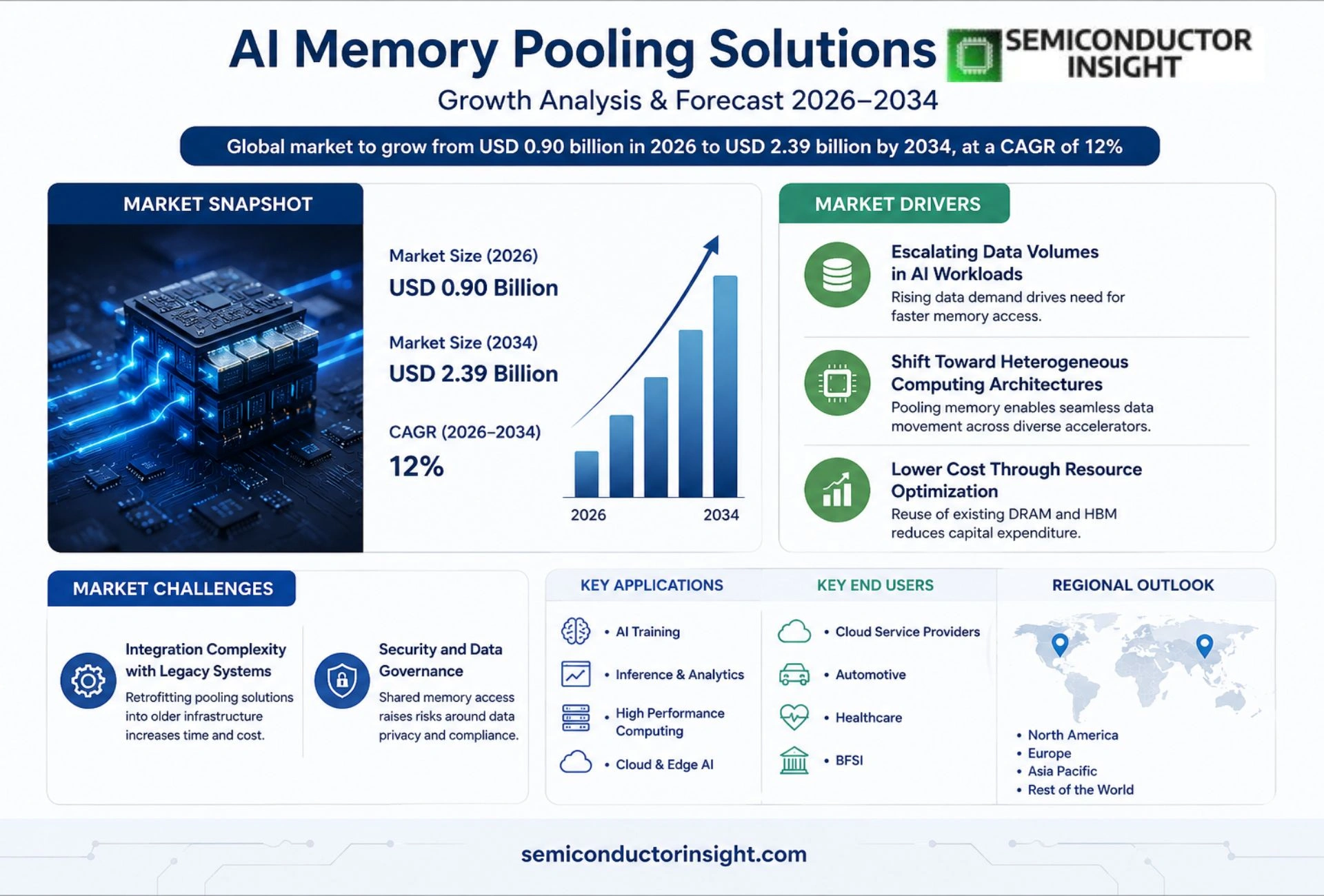

Global AI Memory Pooling Solutions market size was valued at USD 0.85 billion in 2025. It will expand from USD 0.90 billion in 2026 to USD 2.39 billion by 2034, delivering a CAGR of approximately 12 % over the forecast horizon.

AI Memory Pooling Solutions are software‑defined frameworks and hardware accelerators that aggregate heterogeneous memory resources,including DRAM, HBM, NVRAM and persistent‑memory modules,across CPUs, GPUs and dedicated AI inference chips into a single addressable pool. By presenting a unified memory space, these solutions enable large neural networks to exceed the capacity limits of individual devices while preserving low‑latency access required for real‑time inference.

The upward trajectory stems from several dynamics: the explosion of large language models forces data‑center operators to seek more flexible memory architectures; edge‑AI deployments demand efficient sharing of limited on‑device memory; and continuous improvements in high‑bandwidth memory technologies lower cost barriers for pooling implementations. Recent moves such as Nvidia’s collaboration with Samsung on HBM3E‑enabled pooling modules (March 2024) and Intel’s launch of Xeon processors featuring integrated memory‑pool management (April 2024) illustrate how leading vendors are translating these pressures into commercial offerings.

MARKET DRIVERS

Escalating Data Volumes in AI Workloads

Enterprises are confronting unprecedented data influx as generative models and real‑time inference demand faster access to large parameter sets. This pressure compels firms to adopt AI Memory Pooling Solutions that can aggregate fragmented memory resources, thereby delivering the bandwidth required for contemporary algorithms.

Shift Toward Heterogeneous Computing Architectures

Modern AI accelerators combine GPUs, TPUs, and specialized ASICs within a single chassis. The resulting architectural diversity creates memory silos, and pooling mechanisms become essential to orchestrate seamless data movement across these units.

➤ “Pooling memory across heterogeneous nodes reduces latency by up to 30 % while preserving total cost of ownership,”

From a financial perspective, the ability to reuse existing DRAM and high‑bandwidth memory (HBM) through pooling translates into lower capital expenditure, a factor that accelerates adoption across sectors ranging from autonomous vehicles to cloud‑native AI services.

MARKET CHALLENGES

Integration Complexity with Legacy Systems

Organizations that rely on entrenched server farms encounter friction when retrofitting pooling software onto older hardware. The necessity to harmonize firmware, drivers, and management layers can extend deployment timelines and inflate integration budgets.

Other Challenges

Security and Data Governance

Pooling memory inevitably creates shared access points. Without robust isolation and encryption controls, the risk of inadvertent data leakage or unauthorized access rises, prompting stricter compliance scrutiny.

MARKET RESTRAINTS

Limited Vendor Interoperability

Current offerings are often tied to proprietary hardware ecosystems, restricting customers who favor a multi‑vendor strategy. This lock‑in effect curtails broader market penetration and deters enterprises seeking flexibility.

Additionally, the nascent state of open standards for memory pooling means that cross‑platform compatibility remains an open question, slowing large‑scale rollouts.

MARKET OPPORTUNITIES

Emergence of Open‑Source Pooling Frameworks

Community‑driven projects are laying the groundwork for vendor‑agnostic pooling layers that integrate with popular orchestration tools. Early adopters stand to gain operational agility and a clearer path to scale.

Adjacent to this, edge AI deployments,where power and memory constraints are acute,present a fertile environment for lightweight pooling solutions that can extend device lifespans without sacrificing performance.

Finally, regulatory momentum around data residency encourages on‑premise AI clusters equipped with pooling capabilities, opening a niche for providers that can certify compliance while delivering high‑throughput memory access.

AI Memory Pooling Solutions Market Trends

Unified Memory Architecture Fuels Large‑Model Deployments

The surge in transformer‑based language models has exposed the limits of discrete memory stacks attached to CPUs, GPUs or dedicated inference ASICs. By collapsing these silos into a single addressable pool, AI Memory Pooling Solutions enable neural nets that exceed the capacity of any single device while keeping latency within tolerable bounds for real‑time services. Data‑center operators are therefore redesigning workloads around a consolidated memory fabric, which reduces data movement overhead and improves overall throughput. This shift is not merely technical; it translates into lower electricity bills and higher hardware utilization, directly influencing cost structures for cloud providers and large enterprises.

Other Trends

Edge AI Memory Optimization

Deployments at the network edge confront strict power envelopes and chip‑area constraints. Pooling frameworks that can dynamically allocate a shared pool among heterogeneous on‑device processors allow developers to run inference models that would otherwise require a larger silicon footprint. The result is a measurable extension of battery life for autonomous vehicles and a higher inference density for smart cameras, opening new revenue streams for OEMs that previously avoided AI‑intensive workloads on edge hardware.

Vendor Partnerships Accelerate Commercialization

Recent collaborations illustrate how ecosystem coordination lowers adoption barriers. Nvidia’s joint effort with Samsung to ship HBM3E‑enabled pooling modules in March 2024 supplies a high‑bandwidth substrate that aligns with the memory‑pooling software stack, while Intel’s April 2024 launch of Xeon processors with built‑in pool management demonstrates a hardware‑software co‑design approach. These moves signal that major chipmakers recognize the strategic advantage of offering integrated pooling capabilities, encouraging system integrators to embed the technology in the next generation of AI servers and specialized appliances.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics shaping AI memory pooling solutions

Nvidia remains the anchor of the ecosystem, leveraging its GPU dominance and the recent HBM3E partnership with Samsung to deliver tightly integrated pooling modules that address the bandwidth hunger of large language models. The company’s strategy of bundling hardware accelerators with a proprietary software stack gives it leverage over data‑center operators who prioritize predictable latency and ease of deployment. Intel follows a parallel track, embedding memory‑pool management directly into its Xeon processor line‑up, which appeals to enterprise customers favoring a single‑vendor roadmap. Both firms benefit from sizable R&D budgets and a global sales footprint that enable rapid iteration of reference designs, creating a tiered market where the top tier supplies turnkey solutions while smaller vendors compete on niche features or price points.

Beyond the two giants, a constellation of specialized companies is carving out relevance. Samsung supplies the high‑bandwidth memory chips that power many pooling configurations, while AMD’s acquisition of Xilinx adds programmable logic capability for custom pooling fabrics. Graphcore and Cerebras focus on architectural differentiation, offering wafer‑scale engines or IPU‑centric pools that target extreme model sizes. Qualcomm and MediaTek are extending the concept to edge devices, seeking to squeeze more inference capacity into limited silicon. Meanwhile, firms such as Micron, HPE, and Dell Technologies act as system integrators, packaging pooled memory solutions for hyperscale and private‑cloud environments. Their collective activity reflects a market where differentiation stems from memory technology leadership, software integration depth, and the ability to service disparate deployment scales.

List of Key AI Memory Pooling Solutions Companies Profiled

- Nvidia Corp.

- Intel Corporation

- Samsung Electronics

- Advanced Micro Devices (AMD)

- Qualcomm Incorporated

- Graphcore Ltd.

- Cerebras Systems

- MediaTek Inc.

- Xilinx (AMD)

- Micron Technology

- Hewlett Packard Enterprise

- Dell Technologies

- Google Cloud AI

- Microsoft Azure AI

- Habana Labs (Intel)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hardware Accelerators

|

| By Application |

|

Data‑Center Inference

|

| By End User |

|

Cloud Service Providers

|

| By Deployment Environment |

|

On‑Premises Data Centers

|

| By Integration Layer |

|

Hardware‑Level Integration

|

Regional Analysis: AI Memory Pooling Solutions Market

North America

The region’s appetite for real‑time analytics and large‑scale model training pushes firms to adopt shared‑memory fabrics that can serve multiple GPUs simultaneously. By consolidating memory resources, organizations reduce capital outlay and achieve higher utilization rates, a benefit that resonates strongly with cost‑conscious CIOs.

Data‑sovereignty rules in the United States favor architectures where memory pools can be isolated by jurisdiction. Vendors that embed compliance controls at the memory‑pool level gain a competitive edge, especially in regulated industries such as banking and health.

Established chipmakers are leveraging their foundry capabilities to deliver custom pooling ASICs, while emerging startups differentiate through software‑defined memory orchestration. This dual‑track competition accelerates innovation across both hardware and middleware layers.

A deep pool of AI researchers and systems engineers, many transitioning from high‑performance computing, fuels rapid prototyping of pooling solutions. Universities partnering with industry labs further amplify the pipeline of domain‑specific expertise.

Europe

European players benefit from a coordinated push toward AI sovereignty, prompting governments to fund projects that integrate memory‑pooling capabilities into national cloud infrastructures. Countries such as Germany and France are aligning research grants with industry roadmaps, encouraging cross‑border collaborations that blend hardware innovation with open‑source software stacks. The region’s emphasis on energy efficiency drives architects to favor pooling designs that minimize redundant memory footprints, aligning with stringent carbon‑reduction targets. As a result, enterprises are increasingly evaluating pooled memory as a lever to meet both performance and sustainability objectives.

Asia‑Pacific

In Asia‑Pacific, the surge of AI‑driven consumer services and the rise of edge‑computing hubs create a fertile ground for memory‑pooling adoption. Nations like South Korea and Singapore invest heavily in next‑generation data centers that rely on shared memory fabrics to support multilingual large‑language models. The competitive pressure among regional cloud providers fuels rapid rollout of pooling services, often bundled with AI‑as‑a‑service offerings. Meanwhile, talent pipelines from technical universities feed a growing ecosystem of niche startups focused on low‑latency pooling protocols, positioning the region as a hotbed for experimental deployments.

South America

South American economies are beginning to recognize the strategic advantage of pooled memory for scaling AI workloads without massive capital expense. Brazil’s emerging tech corridors, supported by government incentives for AI research, are experimenting with hybrid cloud models that rely on shared memory to bridge on‑premise data warehouses and public clouds. This approach helps local firms overcome bandwidth constraints while maintaining data residency. As regional players forge alliances with multinational vendors, the diffusion of memory‑pooling expertise accelerates, laying groundwork for broader market participation.

Middle East & Africa

The Middle East and Africa exhibit a nascent but increasingly visible interest in AI Memory Pooling solutions, driven by sovereign cloud initiatives and a desire to leapfrog traditional infrastructure models. Gulf states are allocating resources to build AI‑focused data hubs where memory pooling reduces the need for extensive hardware footprints, aligning with limited physical space and sustainability agendas. In Africa, pilot projects in fintech and agritech leverage pooled memory to run sophisticated predictive models on modest hardware, demonstrating the technology’s ability to deliver high value under resource constraints. Collaborative programs with global partners are beginning to transfer know‑how, suggesting a gradual but steady integration of pooling architectures across the region.

Report Scope

This market research report provides a comprehensive analysis of the AI Memory Pooling Solutions Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Memory Pooling Solutions Market?

-> AI Memory Pooling Solutions market will expand from USD 0.90 billion in 2026 to USD 2.39 billion by 2034, delivering a CAGR of approximately 12 %

Which key companies operate in AI Memory Pooling Solutions Market?

-> Key players include Nvidia, Intel, Samsung, Micron, and AMD, among others.

What are the key growth drivers?

-> Key growth drivers include the rapid expansion of large language models demanding larger memory footprints, edge‑AI deployments requiring efficient on‑device memory sharing, and continuous cost reductions in high‑bandwidth memory technologies.

Which region dominates the market?

-> While the reference provides global figures, North America currently leads adoption due to extensive data‑center investments, with Asia‑Pacific showing fast growth.

What are the emerging trends?

-> Emerging trends include HBM3E‑enabled pooling modules, integrated memory‑pool management in CPUs and AI accelerators, and collaborative developments between semiconductor and memory manufacturers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...