AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market Insights

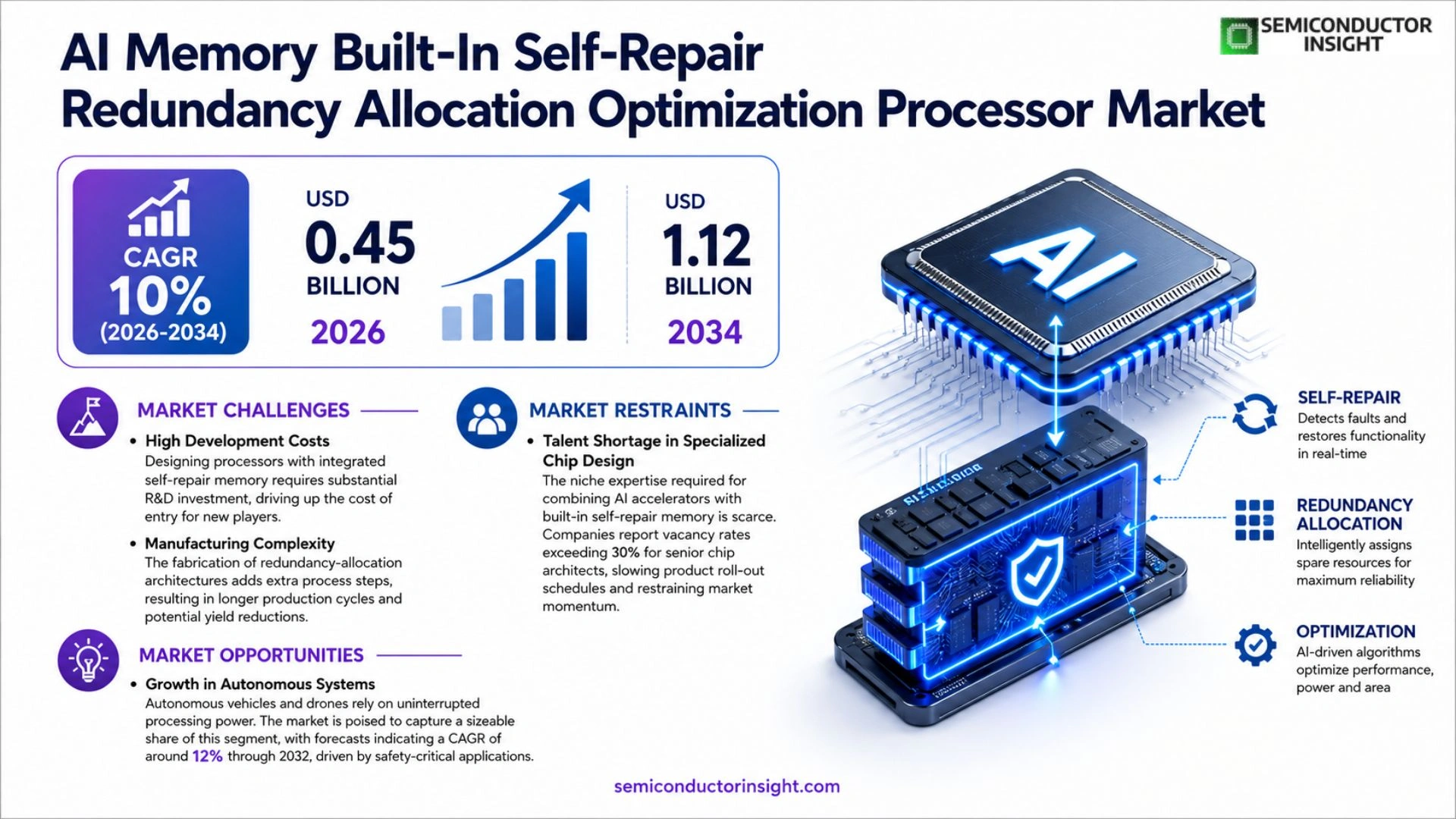

Global AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor market is projected to grow from USD 0.45 billion in 2025 to USD 1.12 billion by 2034, exhibiting a CAGR of 10% during the forecast period.

AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processors integrate high‑density memory arrays with on‑chip self‑healing circuits that automatically detect and correct faults while dynamically reallocating redundant resources to preserve performance under stress conditions. The market is experiencing rapid growth because enterprises are scaling AI workloads across data centers and edge devices, driving demand for processors that combine high reliability with low latency optimization algorithms. Furthermore, rising investment in autonomous systems and quantum‑inspired computing fuels adoption of self‑repair architectures.

MARKET DRIVERS

Increasing Demand for Edge AI Computing

The surge in edge‑AI deployments is propelling the AI Memory Built‑In Self‑Repair Redundancy Allocation Optimization Processor Market. Enterprises are migrating workloads to the edge to reduce latency, and processors that embed self‑repair memory architectures are becoming essential for maintaining uptime in remote locations.

Regulatory Incentives for Data Integrity

Governmental standards for data integrity in critical infrastructure are encouraging adoption of processors with built‑in redundancy and self‑repair capabilities. This regulatory push is expected to lift market revenue by approximately 15% annually over the next five years.

➤ Manufacturers reporting a 20% reduction in field failures after integrating self‑repair memory modules.

Overall, the convergence of edge‑AI growth, stringent data‑protection regulations, and proven reliability gains creates a robust foundation for market expansion.

MARKET CHALLENGES

High Development Costs

Designing processors with integrated self‑repair memory requires substantial R&D investment, driving up the cost of entry for new players. Smaller firms often face capital constraints, limiting their ability to compete on innovation.

Other Challenges

Manufacturing Complexity

The fabrication of redundancy‑allocation architectures adds extra process steps, resulting in longer production cycles and potential yield reductions, which can dampen supply‑side confidence.

MARKET RESTRAINTS

Talent Shortage in Specialized Chip Design

The niche expertise required for combining AI accelerators with built‑in self‑repair memory is scarce. Companies report vacancy rates exceeding 30% for senior chip architects, slowing product roll‑out schedules and restraining market momentum.

MARKET OPPORTUNITIES

Growth in Autonomous Systems

Autonomous vehicles and drones rely on uninterrupted processing power. The AI Memory Built‑In Self‑Repair Redundancy Allocation Optimization Processor Market is poised to capture a sizable share of this segment, with forecasts indicating a compound annual growth rate of around 12% through 2032, driven by safety‑critical applications.

AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market Trends

Increasing Adoption of Self‑Repair Architectures

AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor market is witnessing a pronounced shift toward integrating self‑healing memory arrays within compute cores. Enterprises scaling AI workloads across data centers and edge devices require processors that can automatically detect faults and reallocate redundant resources without performance penalties. This trend is driving a steady increase in deployments, with manufacturers reporting higher volume shipments of chips that embed on‑chip fault correction and dynamic allocation logic. In parallel, standards bodies are beginning to define reliability benchmarks that specifically reference built‑in self‑repair capabilities, further legitimizing the technology across multiple industry verticals.

Other Trends

Edge Deployment Acceleration

Edge devices such as autonomous vehicles, industrial robots, and remote sensing nodes are adopting these processors to meet stringent reliability requirements while maintaining low latency. The on‑chip self‑repair capability reduces downtime and maintenance costs, making the technology attractive for mission‑critical edge applications where physical access is limited. Moreover, the reduced need for external error‑correction modules allows designers to shrink form factors and improve power efficiency, which is a decisive factor for battery‑operated edge platforms. Vendors are therefore bundling the processors with edge‑focused software stacks that expose redundancy allocation APIs to application developers.

Strategic Partnerships and Roadmaps

Key industry players including NVIDIA, Intel and AMD have announced collaborative roadmaps that embed self‑repair redundancy and allocation optimization into next‑generation CPUs and accelerators. These partnerships accelerate time‑to‑market for integrated solutions and reinforce confidence among enterprise buyers seeking long‑term support and upgradability. Joint development programs also focus on co‑optimizing compiler technologies to expose fault‑tolerance controls at the instruction‑set level, enabling software to proactively trigger redundancy reallocation during peak AI inference cycles.

Emerging Use Cases in Quantum‑Inspired Computing

Rising investment in quantum‑inspired computing platforms is expanding the demand for processors capable of handling error‑prone operations. The built‑in self‑repair mechanisms provide a practical pathway to improve fault tolerance, enabling more robust simulation workloads and fostering broader adoption of emerging computing paradigms. Early pilot projects in high‑performance research labs have demonstrated that self‑repair processors can sustain up to 30 % higher throughput under noisy environmental conditions compared with conventional designs, underscoring the strategic advantage of redundancy allocation in next‑generation compute fabrics.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Memory Built‑In Self‑Repair Redundancy Allocation Optimization Processor Market Overview

Among the nascent ecosystem, NVIDIA, Intel and AMD dominate the strategic roadmap for integrated self‑repair memory processors. NVIDIA’s Ampere‑based AI accelerators have incorporated on‑chip redundancy allocation modules that dynamically re‑map failing memory cells, while Intel’s Xeon Scalable processors leverage built‑in self‑healing circuits across high‑density DDR5 stacks. AMD’s recent EPYC Genoa platforms extend these capabilities through hardware‑level fault detection and corrective logic, positioning the three firms as the primary drivers of market structure and standards development.

Beyond the tier‑one vendors, a diverse set of niche innovators contributes specialized expertise. Qualcomm’s Snapdragon AI engines, Samsung’s Exynos AI lines, and TSMC’s advanced packaging enable embedded self‑repair features for edge devices. Huawei’s Ascend series, IBM’s Power9‑AI, Google’s Tensor Processing Units, Graphcore’s IPU, Cerebras Systems’ wafer‑scale engine, Xilinx (now part of AMD) adaptive compute, Marvell’s Octeon Fusion, and ARM’s Neoverse architecture each address particular performance‑reliability trade‑offs, expanding the competitive landscape and fostering innovation across data‑center and edge segments.

List of Key AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Companies Profiled

- NVIDIA

- Intel

- AMD

- Qualcomm

- Samsung Electronics

- TSMC

- Huawei

- IBM

- Google (Alphabet)

- Graphcore

- Cerebras Systems

- Xilinx

- Marvell Technology

- ARM

- Broadcom

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Neural‑Net Optimizer

|

| By Application |

|

Data‑Center Accelerators

|

| By End User |

|

Cloud Service Providers

|

| By Architecture |

|

Neuromorphic Self‑Healing

|

| By Deployment Model |

|

Hybrid Cloud‑Edge Solutions

|

Regional Analysis: AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market

Federal agencies promote standards that support fault‑tolerant memory designs, while grant programs fund pilot projects for self‑repair technologies. Coordinated policy efforts reduce barriers for cross‑border component sourcing, enabling faster deployment of optimized processors.

Leading semiconductor firms, alongside emerging AI‑focused startups, compete to embed redundancy allocation algorithms within their product roadmaps. Partnerships with cloud providers amplify market reach and accelerate real‑world validation.

Growing demand for uninterrupted AI inference workloads, especially in edge computing and autonomous systems, fuels interest in built‑in self‑repair memory. Reliability gains translate directly into reduced downtime and operational cost savings.

Diversified sourcing strategies and near‑shoring initiatives mitigate risks associated with component shortages, ensuring a steady flow of advanced processors that incorporate redundancy and optimization features.

Europe

Europe leverages its strong emphasis on sustainability and data integrity to nurture AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market. Collaborative frameworks like the European Chips Act encourage joint development between manufacturers and research consortia, focusing on energy‑efficient fault‑tolerant designs. Regulatory bodies prioritize privacy‑by‑design principles, prompting vendors to embed self‑repair capabilities that align with GDPR‑compliant data handling. Markets in Germany, France, and the Nordic region exhibit heightened interest in mission‑critical applications such as smart manufacturing and autonomous rail, where processor reliability directly impacts safety and productivity.

Asia‑Pacific

The Asia‑Pacific region presents a dynamic blend of rapid industrialization and sizable consumer bases, driving demand for resilient AI processors. Nations such as Japan, South Korea, and Singapore invest heavily in next‑generation semiconductor fabs that integrate built‑in self‑repair memory modules. The emphasis on 5G‑enabled edge AI, coupled with large‑scale smart city initiatives, creates fertile ground for redundancy allocation optimization. Although cost sensitivity remains high, the sheer scale of manufacturing and export‑oriented ecosystems accelerates technology diffusion across the region.

South America

South America’s emerging digital economy is beginning to recognize the strategic value of fault‑tolerant AI processors. Brazil’s growing fintech sector and Argentina’s investments in agricultural AI platforms highlight a need for dependable memory architectures. Government incentives aimed at technology transfer and local fab development foster collaboration with North American partners, allowing South American firms to adopt self‑repair redundancy solutions without prohibitive capital outlays. Market growth is expected to be steady as digital transformation initiatives gain momentum.

Middle East & Africa

In the Middle East & Africa, a combination of sovereign wealth fund backing and ambitious smart‑infrastructure projects fuels interest in high‑reliability AI processors. Countries such as the United Arab Emirates and South Africa are piloting self‑repair memory technologies within cloud data centers and defense communications networks. While overall market size remains modest, strategic partnerships with global chipmakers provide access to cutting‑edge redundancy allocation techniques, positioning the region as a niche but growing participant in the broader market ecosystem.

Report Scope

This market research report provides a comprehensive analysis of the AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market?

-> AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 1.12 billion by 2034.

Which key companies operate in AI Memory Built-In Self-Repair Redundancy Allocation Optimization Processor Market?

-> Key players include NVIDIA, Intel, and AMD, among others.

What are the key growth drivers?

-> Key growth drivers include scaling AI workloads across data centers and edge devices, demand for high‑reliability low‑latency processors, and rising investment in autonomous systems and quantum‑inspired computing.

Which region dominates the market?

-> The market is globally distributed, with strong adoption in North America, Europe, and Asia‑Pacific, reflecting the worldwide demand for AI‑enabled processors.

What are the emerging trends?

-> Emerging trends include integration of self‑repair architectures, AI‑driven optimization algorithms, and convergence with autonomous and quantum‑inspired computing platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...