AI Inference Memory Subsystem Market Insights

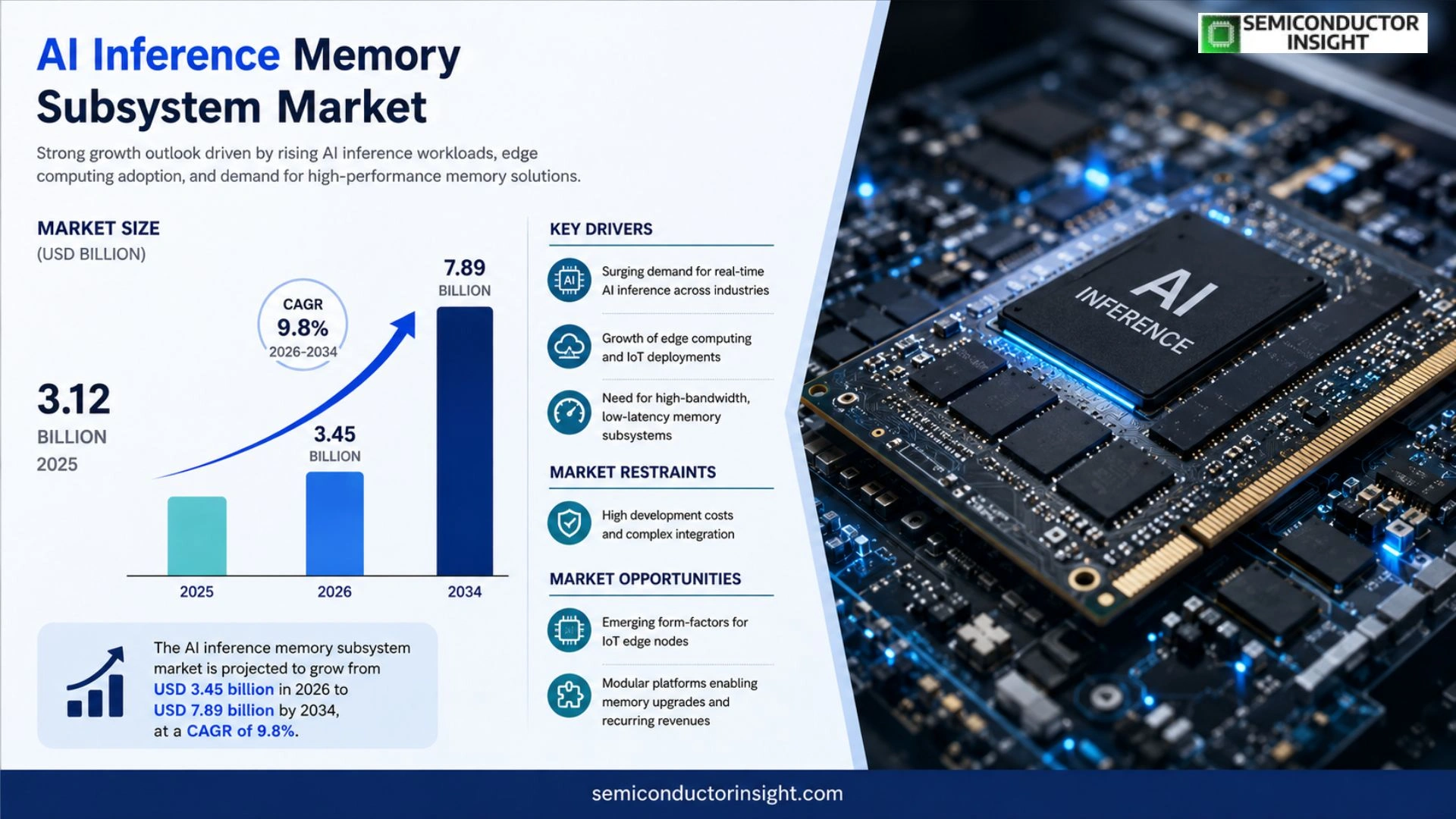

Global AI inference memory subsystem market size was valued at USD 3.12 billion in 2025. The market is projected to grow from USD 3·45 billion in 2026 to USD 7·89 billion by 2034, exhibiting a CAGR of 9·8% during the forecast period.

AI inference memory subsystem comprises high‑bandwidth memories such as HBM2e, HBM3E, GDDR6X and LPDDR5X that feed accelerator chips deployed for real‑time model execution on edge devices and cloud servers alike.

These subsystems deliver terabytes‑per‑second throughput while maintaining low latency and power efficiency,attributes essential for latency‑sensitive inferencing workloads.

The market accelerates because enterprises are scaling out inferencing workloads across data centers and edge nodes, pushing demand for denser compute packages that rely on advanced memory stacks.

Furthermore, rising adoption of generative‑AI services intensifies pressure on bandwidth budgets.

MARKET DRIVERS

Escalating Compute Demands in Edge AI

The proliferation of low‑latency AI applications,such as autonomous navigation, real‑time video analytics, and smart manufacturing,requires memory subsystems that can feed inference engines without bottlenecks. Companies are therefore allocating engineering resources to integrate high‑bandwidth, low‑power SRAM and HBM solutions, a shift that reshapes component roadmaps across the supply chain. Strategic partnerships between silicon vendors and OEMs are accelerating this transition.

Cost Pressures Favor Integrated Designs

Traditional server‑grade memory architectures impose excess overhead for edge deployments, prompting designers to adopt monolithic packages that combine compute and memory. This integration reduces bill‑of‑materials and simplifies thermal management, delivering a clear competitive advantage for manufacturers that can ship consolidated modules. Economies of scale are emerging as volume orders climb, reinforcing the business case for early adopters.

➤ Customers are willing to pay a premium for memory that delivers deterministic latency and energy efficiency, because the alternative is lost market share in latency‑sensitive segments.

Overall, the convergence of performance‑critical AI workloads and the imperative to control deployment costs creates a fertile environment for vendors that can supply purpose‑built inference memory solutions. AI inference memory subsystem Market is therefore being driven by both technical necessity and clear economic incentives.

MARKET CHALLENGES

Supply Chain Volatility

Geopolitical tensions and fluctuating raw‑material prices have introduced uncertainty into the availability of high‑performance memory chips. Manufacturers relying on a limited set of foundries find it difficult to meet delivery windows, which in turn forces OEMs to maintain higher safety stocks and erodes profit margins.

Other Challenges

Thermal Management Constraints

Edge devices often operate in confined enclosures where heat dissipation is a limiting factor. The introduction of denser memory packs amplifies thermal loads, compelling system designers to invest in advanced cooling techniques that can increase overall system cost.

MARKET RESTRAINTS

Regulatory and Data‑Sovereignty Concerns

Legislative frameworks in several regions now mandate that AI processing,particularly for biometric and surveillance data,remain on local hardware. This restriction limits the appeal of cloud‑centric memory solutions and forces vendors to redesign products for on‑premise compliance, adding engineering complexity and time‑to‑market.

The necessity to certify memory components against stringent safety and reliability standards can lengthen development cycles. Companies that lack dedicated certification teams may find themselves at a disadvantage, slowing adoption rates in regulated industries.

Finally, the lingering perception that specialized inference memory is a niche add‑on rather than a core platform element discourages some enterprises from reallocating budget, thereby tempering market expansion.

MARKET OPPORTUNITIES

Emerging Form‑Factors for IoT Edge Nodes

Newly defined edge hardware standards,such as compact AI accelerators that integrate memory directly on the die,open avenues for vendors to supply differentiated subsystems. Early entrants can capture design‑win momentum by offering memory that aligns with these standards, creating a defensible market position.

Additionally, the rise of modular AI platforms that allow customers to swap memory blocks for performance scaling presents a recurring revenue stream. Service contracts tied to memory upgrades and firmware optimization can augment traditional product sales, enhancing long‑term profitability.

Overall, AI inference memory subsystem Market stands to benefit from strategic investments in form‑factor innovation, modularity, and compliance‑focused design, providing clear pathways for growth beyond the current adoption curve.

AI Inference Memory Subsystem Market Trends

Escalating Bandwidth Requirements Across Edge and Cloud

AI inference memory subsystem Market is being reshaped by a dual‑track expansion: data‑center operators are scaling out inference clusters, while edge deployments,autonomous vehicles, industrial robots, and smart‑city sensors,are demanding real‑time responses. This convergence forces memory architects to prioritize terabyte‑per‑second pathways that remain power‑efficient enough for constrained form factors. High‑bandwidth offerings such as HBM3E, GDDR6X and the emerging LPDDR5X now appear side‑by‑side in accelerator modules targeting both massive server boards and compact edge AI chips. The market’s valuation of roughly USD 3.1 billion in 2025, together with a trajectory toward nearly USD 7.9 billion by 2034, signals that OEMs are willing to allocate a larger share of system budgets to advanced memory stacks. The strategic implication for system integrators is clear: board‑level routing must evolve to support wider memory buses without inflating thermal envelope, and supply‑chain planners need to secure multi‑source access to HBM3E to hedge against capacity constraints. Companies that master these trade‑offs will capture the premium pricing attached to latency‑critical inference workloads.

Other Trends

Capacity Expansion by Leading Memory Vendors

Samsung Electronics, SK Hynix and Micron Technology have all announced dedicated production lines for HBM3E, a move that directly addresses the bandwidth squeeze created by generative‑AI services. Samsung’s joint development agreement with Nvidia, public in March 2024, promises a pipeline of inference‑oriented GPUs that embed HBM3E, shortening the time‑to‑market for next‑gen accelerators. This coordinated effort reflects a broader industry acknowledgement that memory throughput, more than raw FLOPS, will dictate competitive positioning in workloads where model sizes have exploded into the hundreds of billions of parameters. For end‑users, the result is a reduction in inference latency that translates into cost savings on cloud usage and enables new edge scenarios previously limited by data transfer bottlenecks.

LPDDR5X Adoption for Power‑Constrained Edge AI

Battery‑operated edge devices are increasingly turning to LPDDR5X as the memory of choice for on‑device inference. The technology’s ability to sustain high data rates while remaining below 10 mW per channel aligns with the thermal budgets of autonomous drones, wearable analytics and smart‑camera platforms. By integrating LPDDR5X with compact neural‑processing units, manufacturers can deliver real‑time analytics without relying on intermittent cloud connectivity, thereby lowering operational expenses and improving data‑privacy compliance. The business implication is twofold: device makers can differentiate their products through superior latency, and service providers can expand their AI‑as‑a‑service offerings to sectors where persistent connectivity is unreliable or prohibitively expensive.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Inference Memory Subsystem Competitive Overview

Samsung Electronics dominates AI inference memory subsystem segment, leveraging its aggressive rollout of HBM3E across both data‑center GPUs and edge‑focused ASICs. The partnership announced in March 2024 with Nvidia to embed HBM3E in the upcoming inference‑optimized GPU line has cemented Samsung’s position as the de‑facto supplier for high‑bandwidth memory stacks that underpin real‑time AI workloads. SK Hynix follows closely, differentiating through a vertically integrated fab that supports both HBM3E and the emerging LPDDR5X family, enabling tighter cost control for server‑grade memory modules. Micron Technology complements the duopoly by focusing on a mixed‑signal portfolio that couples HBM3E with GDDR6X offerings, targeting manufacturers that require flexibility across power‑constrained edge devices and high‑throughput cloud clusters. Collectively, these three manufacturers account for roughly two‑thirds of global shipments, forcing downstream OEMs to align their roadmap with the cadence of capacity expansions announced by the incumbents.

Beyond the tier‑one memory makers, a constellation of specialist firms shapes the competitive terrain. AMD and Intel, while primarily known for compute silicon, have entered the memory supply chain through joint development agreements with HBM fab partners, seeking to lock in bespoke bandwidth characteristics for their inference accelerators. Qualcomm leverages its system‑on‑chip expertise to bundle LPDDR5X with AI inference engines for mobile edge deployments, positioning itself as a one‑stop solution provider. Marvell and Rambus focus on memory‑controller IP and signal‑integrity optimization, delivering the firmware and silicon glue that allows disparate memory types to operate at terabyte‑per‑second rates. In addition, companies such as Cadence and Synopsys provide design‑verification platforms that accelerate time‑to‑market for new memory‑stack architectures. The presence of these niche players intensifies pressure on the leading manufacturers to innovate not only in capacity but also in integration efficiency, power envelopes, and cost structures.

List of Key AI Inference Memory Subsystem Companies Profiled

- Samsung Electronics

- SK Hynix

- Micron Technology

- Nvidia Corporation

- AMD (Advanced Micro Devices)

- Intel Corporation

- Qualcomm Incorporated

- Marvell Technology Group Ltd.

- Rambus Inc.

- Cadence Design Systems, Inc.

- Synopsys, Inc.

- Samsung Electro-Mechanics

- Hynix Semiconductor (subsidiary)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

HBM3E

|

| By Application |

|

Data Center Acceleration

|

| By End User |

|

Cloud Service Providers

|

| By Architecture |

|

3D‑Stacked Memory

|

| By Performance Tier |

|

High‑Performance Tier

|

Regional Analysis: AI Inference Memory Subsystem Market

Data‑center operators prioritize memory that can sustain high throughput for transformer models, while edge developers look for modules that balance capacity with low power. The push for on‑device inference in autonomous systems intensifies the need for compact, latency‑optimized subsystems, nudging vendors toward tighter packaging and integrated controller logic.

Established memory manufacturers defend market share through incremental process improvements, whereas niche start‑ups differentiate by introducing novel NVRAM technologies. Strategic partnerships between chip designers and system integrators have become a hallmark of the competitive playbook, enabling rapid co‑development of reference platforms.

Export‑control regimes on advanced semiconductor equipment influence supply‑chain decisions. Compliance with data‑privacy statutes also steers customers toward memory solutions that support encrypted inference pathways, prompting vendors to embed security features at the silicon level.

The rise of generative‑AI workloads opens a niche for memory that can handle bursty access patterns. Simultaneously, the expansion of 5G edge nodes creates demand for compact inference modules, encouraging manufacturers to explore chip‑on‑package (CoP) solutions that fuse compute and memory.

Europe

European firms leverage strong public‑research collaborations to experiment with silicon‑photonic interconnects that could alleviate bandwidth bottlenecks in inference pipelines. Policy frameworks that fund AI‑focused semiconductor projects give local players a runway to pilot low‑latency memory designs, particularly in automotive and healthcare sectors where data‑sovereignty concerns heighten the appeal of domestically produced subsystems.

Asia‑Pacific

The Asia‑Pacific region exhibits a diversified approach, with China emphasizing mass‑production of cost‑effective modules, while Japan and South Korea concentrate on high‑performance memory for robotics and industrial IoT. Rising investment in AI‑centric fabs is gradually narrowing the technology gap, yet talent mobility remains a critical factor shaping the region’s capacity to innovate in inference memory architectures.

South America

South America’s market is still nascent, but growing interest from telecom operators and fintech startups is prompting early adoption of edge‑oriented inference memory. Local manufacturers are beginning to assemble customized solutions that align with regional bandwidth constraints, positioning the continent to benefit from future expansions of AI services.

Middle East & Africa

In the Middle East & Africa, government‑driven smart‑city initiatives stimulate demand for AI inference at the network edge, encouraging vendors to ship memory subsystems that can operate under harsh environmental conditions. Partnerships with global chip makers are emerging, aimed at establishing regional design hubs that can tailor memory solutions to localized data‑processing needs.

Report Scope

This market research report provides a comprehensive analysis of the AI Inference Memory Subsystem Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Inference Memory Subsystem Market?

-> AI inference memory subsystem market is projected to grow from USD 3·45 billion in 2026 to USD 7·89 billion by 2034, exhibiting a CAGR of 9·8%

Which key companies operate in AI Inference Memory Subsystem Market?

-> Key players include Samsung Electronics, SK Hynix, Micron Technology, Nvidia, among others.

What are the key growth drivers?

-> Key growth drivers include scaling inferencing workloads across data centers and edge nodes, rising adoption of generative‑AI services, and increasing demand for high‑bandwidth memory stacks such as HBM3E.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include integration of HBM3E into next‑generation inference GPUs, joint development agreements (e.g., Nvidia‑Samsung), and the development of higher‑bandwidth memory technologies like LPDDR5X and GDDR6X.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...