MARKET INSIGHTS

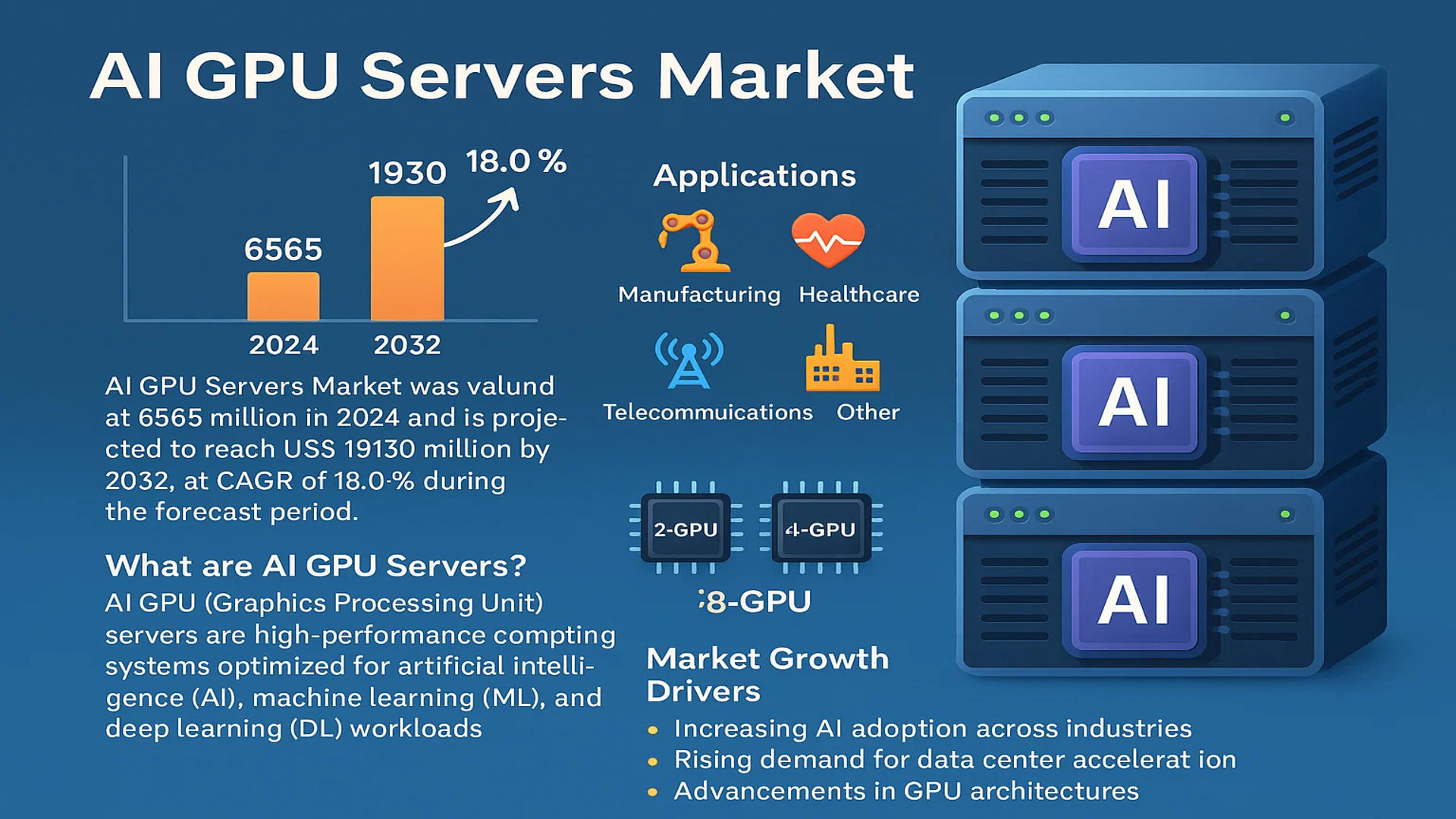

The global AI GPU Servers Market was valued at 6565 million in 2024 and is projected to reach US$ 19130 million by 2032, at a CAGR of 18.0% during the forecast period.

AI GPU (Graphics Processing Unit) servers are high-performance computing systems optimized for artificial intelligence (AI), machine learning (ML), and deep learning (DL) workloads. These servers leverage parallel processing capabilities of GPUs, delivering significantly faster performance than traditional CPU-based servers for computationally intensive AI tasks. Key configurations include 2-GPU, 4-GPU, and 8-GPU systems, with applications spanning manufacturing, healthcare, telecommunications, and other industries.

The market growth is driven by increasing AI adoption across industries, rising demand for data center acceleration, and advancements in GPU architectures. However, high costs and supply chain constraints pose challenges. Major players like Dell, HPE, and Lenovo dominate the market, collectively holding a significant revenue share. Recent developments include NVIDIA’s H100 GPU adoption in next-generation AI servers and growing investments in hyperscale data centers across North America and Asia-Pacific regions.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth of AI Workloads Fueling Demand for GPU-Accelerated Servers

The rapid expansion of artificial intelligence applications across industries is driving unprecedented demand for AI GPU servers. These specialized systems are now essential for training complex machine learning models, with the global AI market projected to grow nearly 20% annually through 2032. The healthcare sector alone has seen a 45% increase in AI adoption for medical imaging analysis, while financial institutions process over 65% of fraud detection algorithms on GPU-accelerated infrastructure. This surge is further amplified by the rise of generative AI, where GPU servers demonstrate 30-50x performance gains over traditional CPUs in large language model processing. Enterprises are prioritizing these high-performance computing solutions to maintain competitive advantage in an increasingly AI-driven economy.

Advancements in GPU Architecture Driving Performance Breakthroughs

Recent innovations in GPU technology have significantly enhanced server capabilities, making them indispensable for AI workloads. The latest generation of processing units deliver 4-5x improvement in floating-point performance compared to previous iterations, with some architectures achieving over 300 teraflops of AI performance in a single module. These technological leaps are enabling real-time processing of massive datasets – critical for applications like autonomous vehicle navigation systems which require sub-50 millisecond response times. Moreover, the integration of tensor cores and specialized AI accelerators has reduced energy consumption by 35% per computation, addressing both performance and sustainability concerns for enterprise data centers.

➤ The introduction of multi-GPU server configurations with 8 or more high-end accelerators is transforming data center architecture, allowing 80% faster model training times for deep learning applications.

Furthermore, cloud service providers are rapidly adopting these next-generation servers, with hyper-scale deployments growing at 28% year-over-year. This infrastructure expansion supports the democratization of AI tools, making advanced computing power accessible to businesses of all sizes through cloud-based GPU instances.

MARKET RESTRAINTS

Supply Chain Constraints and Component Shortages Impacting Market Growth

While demand for AI GPU servers continues to surge, the market faces significant supply-side challenges. The specialized components required for high-performance computing systems, particularly advanced GPUs, are subject to complex manufacturing processes with lead times exceeding 6-9 months in some cases. This imbalance has created allocation challenges throughout the value chain, with some server manufacturers reporting 20-30% order fulfillment delays. The situation is further complicated by export controls affecting certain chip technologies, creating regional disparities in availability and influencing procurement strategies for multinational enterprises.

Energy Consumption and Cooling Requirements Present Operational Challenges

The increasing power density of GPU-accelerated servers is creating infrastructure challenges for data center operators. A single rack of high-end AI servers can now consume over 40kW of power – nearly ten times traditional server power requirements. This exponential growth in energy demand is driving up operational costs, with some facilities reporting 50% increases in electricity expenditures after GPU server deployments. Additionally, the thermal output of these systems requires advanced liquid cooling solutions that can add 15-25% to total cost of ownership, making adoption prohibitive for smaller organizations without specialized data center infrastructure.

Other Constraints

Rapid Technological Obsolescence

The blistering pace of innovation in AI hardware creates deployment dilemmas, with new GPU architectures emerging every 12-18 months. This forces enterprises to balance the need for cutting-edge performance with concerns about asset depreciation and upgrade cycles.

MARKET CHALLENGES

Shortage of Specialized AI Talent Limiting Market Expansion

The industry faces a critical skills gap that threatens to constrain growth in the AI server market. There’s currently a 60% deficit in qualified professionals capable of designing, deploying and maintaining GPU-accelerated AI infrastructure. This talent shortage is particularly acute for professionals with expertise in both hardware optimization and machine learning frameworks. Educational institutions are struggling to keep pace with demand, producing only about 30% of required graduates with relevant competencies annually. The resulting competition for skilled personnel has driven salary increases of 25-40% in certain technical roles, adding pressure to operating costs throughout the ecosystem.

MARKET OPPORTUNITIES

Edge AI Deployments Creating New Growth Frontiers

The emergence of edge computing applications presents significant opportunities for GPU server manufacturers. Industrial IoT implementations are driving demand for compact, ruggedized server solutions capable of processing AI workloads locally. The edge AI market is projected to grow 30% annually, with applications ranging from smart city infrastructure to autonomous manufacturing systems. These deployments require specialized server configurations that balance performance with environmental resilience, creating opportunities for vendors to differentiate through customized solutions. Retail analytics, for example, is showing particular promise, with 65% of major retailers planning edge AI implementations for real-time customer behavior analysis within the next three years.

Vertical-Specific AI Solutions Driving Market Diversification

Industry-specific AI applications are generating substantial opportunities for specialized server solutions. The healthcare diagnostics sector is adopting GPU servers for medical imaging AI that can reduce analysis time from hours to minutes. Similarly, financial institutions are implementing GPU-accelerated fraud detection systems that process transactions with 99.9% accuracy in milliseconds. These vertical applications often require tailored server configurations with specific certifications, security features, and software integrations – factors that allow vendors to create differentiated offerings with higher margins. The automotive sector’s adoption of AI for autonomous driving development represents another high-growth segment, with testing fleets generating petabytes of data that require specialized server processing capabilities.

Explosive Growth in AI Workloads Driving the AI GPU Servers Market

The global AI GPU servers market is experiencing unprecedented growth, fueled by the surge in artificial intelligence applications across industries. With organizations increasingly adopting machine learning and deep learning models, the demand for high-performance computing infrastructure has skyrocketed. AI GPU servers, equipped with cutting-edge processors capable of handling parallel computations, have become the backbone of modern AI infrastructure. The market’s valuation at 6,565 million in 2024 reflects this growing adoption, with projections suggesting nearly threefold growth to reach 19,130 million by 2032. This 18.0% compound annual growth rate underscores the critical role these servers play in powering the AI revolution. Major players like Dell, HPE, and ASUS are rapidly expanding their offerings to meet this burgeoning demand, collectively holding significant market shares.

Other Trends

Specialization in Server Configurations

The market is witnessing increasing specialization in AI server configurations to meet diverse computational needs. While 2 GPU servers currently dominate the landscape, there’s growing demand for more powerful 4 GPU and 8 GPU configurations to handle complex deep learning models. The trend toward specialized configurations is particularly evident in sectors like autonomous vehicle development and pharmaceutical research, where massive datasets require intensive processing. This segmentation allows organizations to optimize their AI infrastructure investments, balancing performance needs with budget constraints.

Sector-Specific Adoption Patterns Emerging

Different industries are adopting AI GPU servers at varying rates, with manufacturing and telecommunications leading the charge. In manufacturing, these servers are revolutionizing quality control through computer vision applications, while telecommunication companies leverage them for network optimization and predictive maintenance. The medical sector shows particularly strong growth potential, with AI servers enabling breakthroughs in medical imaging analysis and drug discovery. Regional adoption patterns also vary significantly, with North America currently leading in deployment but Asia-Pacific – particularly China and Japan – showing the fastest growth rates as they invest heavily in AI infrastructure.

Technological Evolution and Performance Optimization

Continuous advancements in GPU architecture are dramatically improving AI server performance while reducing power consumption. New generations of processors offer enhanced tensor cores specifically optimized for AI workloads, delivering superior speed and efficiency. Energy efficiency has become a critical competitive differentiator, with data center operators demanding solutions that balance computational power with sustainability. This technological evolution is enabling organizations to process increasingly complex neural networks while managing operational costs – a key factor driving market expansion across diverse applications from natural language processing to edge computing implementations.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest Aggressively in AI-Optimized GPU Server Solutions

The global AI GPU servers market exhibits a competitive yet fragmented landscape, dominated by technology giants alongside specialized hardware manufacturers. Dell Technologies and Hewlett Packard Enterprise (HPE) collectively account for over 30% of the market share, leveraging their established server infrastructure and global distribution networks. Their dominance stems from early adoption of NVIDIA’s latest GPU architectures and customized AI workload optimizations.

Supermicro has emerged as a disruptive force, specializing in high-density GPU server solutions favored by hyperscalers and research institutions. The company’s rapid growth is attributed to its flexible, modular server designs that accommodate varying GPU configurations. Meanwhile, Lenovo continues to gain traction through strategic partnerships with cloud service providers, particularly in the Asia-Pacific region where AI adoption is accelerating.

The competitive intensity is further heightened by Taiwanese manufacturers like ASUS and GIGABYTE, whose cost-competitive but performance-oriented GPU servers are increasingly preferred by mid-market enterprises. These players are investing heavily in liquid cooling technologies to address the thermal challenges of dense GPU deployments, giving them an edge in energy efficiency.

While the market remains innovation-driven, recent developments show a trend toward vertical integration. Leading players are now developing proprietary software stacks to complement their hardware, creating complete AI solution ecosystems. This strategic shift is expected to reshape competitive dynamics as customers increasingly prefer turnkey AI infrastructure solutions.

List of Key AI GPU Server Manufacturers

- Dell Technologies (U.S.)

- Hewlett Packard Enterprise (U.S.)

- Supermicro (U.S.)

- Lenovo (China)

- ASUS (Taiwan)

- GIGABYTE (Taiwan)

- ADLINK Technology (Taiwan)

- Advantech (Taiwan)

- xFusion (China)

Segment Analysis:

By Type

4 GPU Servers Segment Dominates Due to Optimal Balance Between Performance and Cost Efficiency

The market is segmented based on type into:

- 2 GPU Servers

- 4 GPU Servers

- 8 GPU Servers

- Others (including configurations above 8 GPUs)

By Application

Manufacturing Segment Leads Due to Intensive AI Adoption in Predictive Maintenance and Quality Control

The market is segmented based on application into:

- Manufacturing

- Medical

- Telecommunications

- Others (including financial services, retail, and energy)

By End-User

Cloud Service Providers Show Highest Adoption Due to Scalable AI Infrastructure Needs

The market is segmented based on end-user into:

- Cloud Service Providers

- Enterprises

- Research Institutions

- Government Agencies

Regional Analysis: AI GPU Servers Market

North America

North America leads the global AI GPU Servers market, driven by technological advancements and strong investments in AI research and development. The region, particularly the U.S., is home to leading tech giants such as Nvidia, Intel, and AMD, which dominate GPU innovation. The growing demand for AI-driven applications in healthcare, autonomous vehicles, and cloud computing is accelerating market growth. Government initiatives, such as the National AI Initiative Act, further bolster investments in AI infrastructure. Additionally, data centers upgrading to AI-optimized GPU servers contribute significantly to regional expansion. However, high costs and supply chain constraints pose challenges for widespread adoption among smaller enterprises.

Asia-Pacific

The Asia-Pacific region is experiencing the fastest growth in AI GPU Servers adoption, primarily fueled by China, Japan, and South Korea. China’s aggressive push toward AI supremacy under its “Next Generation Artificial Intelligence Development Plan” has led to massive investments in GPU server infrastructure. Major companies like Alibaba, Tencent, and Huawei are expanding their AI data centers, contributing to the region’s market dominance. India’s burgeoning startup ecosystem and government AI policies are also propelling demand. While cost competitiveness benefits manufacturing-heavy economies, regulatory uncertainties and intellectual property concerns remain hurdles for international vendors.

Europe

Europe maintains a strong foothold in the AI GPU Servers market, supported by the European Commission’s AI strategy and Horizon Europe funding. Countries like Germany, France, and the U.K. prioritize AI server deployment in automotive, healthcare, and industrial automation. The GDPR-compliant AI infrastructure ensures data security but imposes additional compliance costs. Collaborative initiatives, such as the European Processor Initiative (EPI), aim to reduce dependency on non-European GPU suppliers. Despite steady growth, high energy costs and prolonged regulatory approvals slow down rapid market expansion in comparison to North America and Asia.

South America

South America’s AI GPU Servers market is emerging, with Brazil and Argentina being key growth contributors. The region benefits from increasing AI adoption in agriculture, finance, and telecommunications. However, economic instability and limited infrastructure investment slow down progress compared to other regions. Local enterprises favor cost-effective solutions, while international suppliers face trade restrictions and logistical challenges. Government-backed AI initiatives are slowly gaining traction, but large-scale implementation requires substantial foreign investment and policy reforms.

Middle East & Africa

The Middle East and Africa region is gradually embracing AI GPU Servers, with the UAE, Saudi Arabia, and South Africa leading adoption. The UAE’s National AI Strategy 2031 aims to position the country as a global AI hub, fueling demand for high-performance computing. Meanwhile, growing digitization in banking and smart city projects presents opportunities. Africa faces infrastructural gaps and energy deficits, limiting AI server scalability. Despite these challenges, partnerships with global tech firms and increased funding for AI research signal long-term growth potential.

Report Scope

This market research report provides a comprehensive analysis of the Global AI GPU Servers market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global AI GPU Servers market was valued at USD 6,565 million in 2024 and is projected to reach USD 19,130 million by 2032, growing at a CAGR of 18.0%.

- Segmentation Analysis: Detailed breakdown by product type (2 GPU, 4 GPU, 8 GPU, Others) and application (Manufacturing, Medical, Telecommunications, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with the U.S. and China being key growth markets.

- Competitive Landscape: Profiles of leading market participants including Dell, HPE, ASUS, GIGABYTE, Supermicro, Lenovo, ADLINK, Advantech, Hypertec, and MiTAC, covering their product portfolios, R&D strategies, and market share.

- Technology Trends & Innovation: Assessment of emerging AI/ML workloads, GPU advancements, and integration with cloud computing and edge applications.

- Market Drivers & Restraints: Evaluation of factors such as AI adoption across industries, data center expansion, and challenges like supply chain constraints and high costs.

- Stakeholder Analysis: Insights for server manufacturers, data center operators, AI solution providers, and investors regarding growth opportunities and strategic positioning.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global AI GPU Servers Market?

-> AI GPU Servers Market was valued at 6565 million in 2024 and is projected to reach US$ 19130 million by 2032, at a CAGR of 18.0% during the forecast period.

Which key companies operate in Global AI GPU Servers Market?

-> Key players include Dell, HPE, ASUS, GIGABYTE, Supermicro, Lenovo, ADLINK, Advantech, Hypertec, and MiTAC, among others.

What are the key growth drivers?

-> Key growth drivers include rising AI adoption, expansion of data centers, demand for high-performance computing, and advancements in GPU technology.

Which region dominates the market?

-> North America leads in market share, while Asia-Pacific is the fastest-growing region due to rapid AI adoption in China and other emerging economies.

What are the emerging trends?

-> Emerging trends include edge AI computing, hybrid cloud deployments, energy-efficient GPUs, and specialized AI server architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...