AI Ethernet Switch Silicon Market Insights

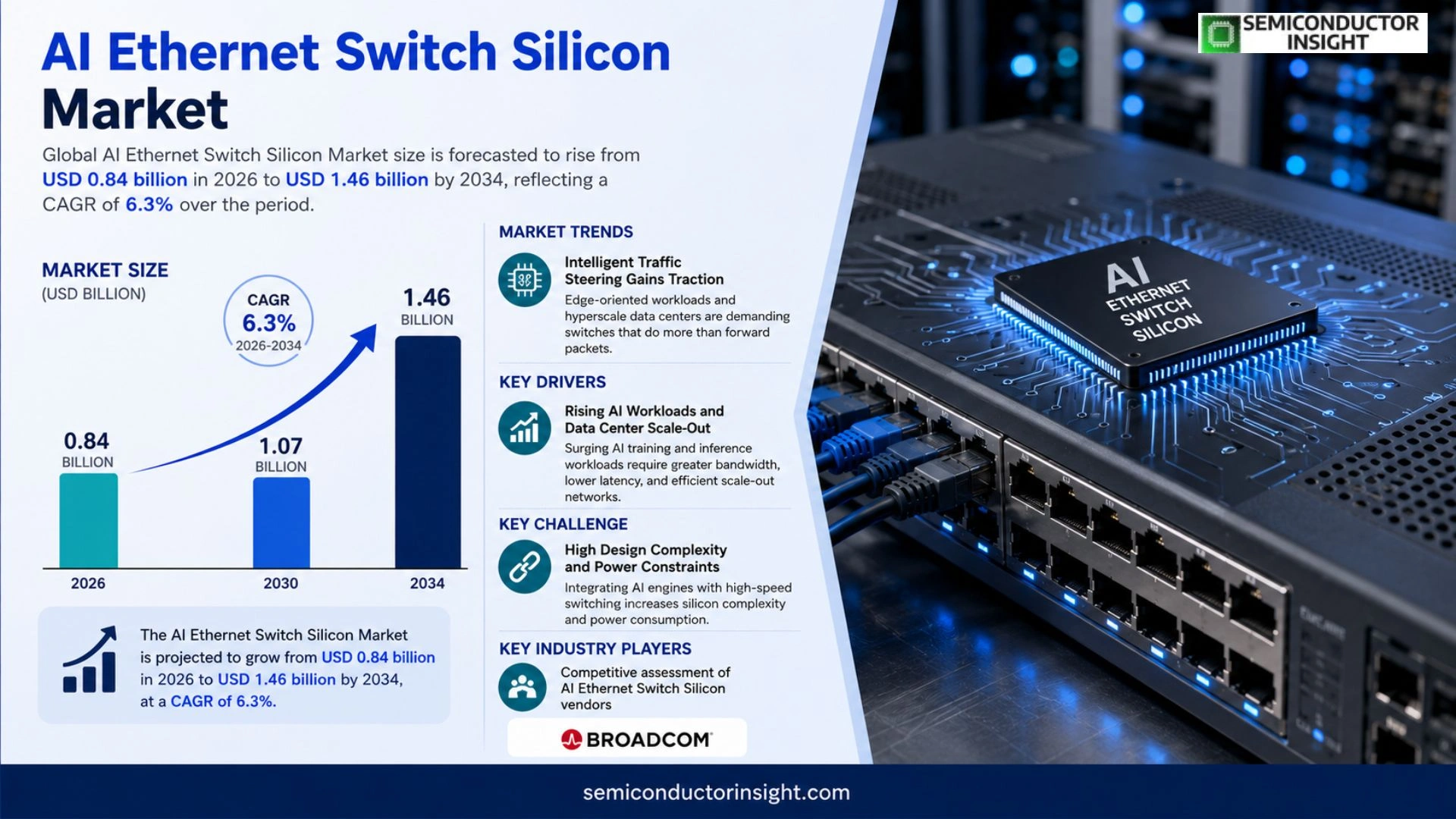

Global AI Ethernet Switch Silicon Market size was valued at USD 0.78 billion in 2025. The market is forecasted to rise from USD 0.84 billion in 2026 to USD 1.46 billion by 2034, reflecting a compound annual growth rate of 6.3 % over the period.

AI Ethernet switch silicon comprises specialized integrated circuits that combine high‑throughput switching functions with on‑chip artificial‑intelligence inference engines. These devices embed programmable logic, ASIC accelerators and advanced power‑management techniques so that latency‑sensitive workloads,such as edge video analytics or autonomous‑system control,can be processed directly within the network fabric.

The sector is gaining momentum because hyperscale data centers and edge deployments increasingly require intelligent traffic steering coupled with on‑board inference capability. Recent product launches,e.g., Company X’s next‑generation AI‑enabled switch ASIC announced in March 2024,illustrate how leading silicon vendors are expanding beyond conventional switching solutions toward fully integrated smart networking platforms.

MARKET DRIVERS

AI‑Centric Data Center Expansion

The surge in hyperscale cloud facilities has forced operators to adopt switches that can off‑load neural‑network inference directly on the silicon layer. Latency‑critical workloads such as real‑time video analytics and autonomous‑vehicle training now demand sub‑microsecond response times, prompting vendors to integrate dedicated tensor cores within Ethernet fabrics. This architectural shift is reshaping purchasing decisions across AI Ethernet Switch Silicon Market.

Rising Edge‑Computing Deployments

Enterprises are migrating inference engines to the network edge to reduce bandwidth consumption and comply with data‑sovereignty regulations. Edge nodes equipped with AI‑optimized switch silicon can perform model pruning and quantization on‑the‑fly, delivering actionable insights without round‑tripping to central clouds. The practical cost advantage of consolidating compute and switching functions is a decisive catalyst for market momentum.

➤ “Integrating AI accelerators into Ethernet switches cuts overall system TCO by up to 18 % while shaving 30 % off end‑to‑end latency.”

Beyond performance, power‑efficiency considerations are tightening the value equation. Modern AI Ethernet Switch Silicon designs leverage FinFET and embedded low‑power SRAM blocks, allowing data‑center operators to meet aggressive PUE targets. As sustainability benchmarks become contractual clauses, the technology’s ability to lower energy draw translates directly into procurement priority.

MARKET CHALLENGES

Complexity of Firmware Integration

Customers often face steep learning curves when aligning AI switch firmware with heterogeneous acceleration stacks. Software‑defined networking (SDN) controllers must be extended to expose tensor‑execution APIs, a requirement that stretches in‑house engineering resources and can delay rollout timelines.

Other Challenges

Standardization Gaps

The lack of a unified programming model for AI‑enhanced Ethernet fabrics forces vendors to adopt proprietary extensions. This fragmentation hampers cross‑vendor interoperability, raising the risk of lock‑in and inflating total ownership costs.

Manufacturers also encounter supply‑chain volatility for high‑performance silicon wafers, especially when demand spikes coincide with broader semiconductor shortages. Lead‑time extensions erode the predictability of capacity planning, compelling buyers to hold larger safety stocks.

MARKET RESTRAINTS

Cost Sensitivity in Mid‑Market Segments

While flagship data‑center operators can justify premium pricing, midsize enterprises remain cautious. Total cost of ownership analyses frequently reveal that the incremental performance gain does not offset the higher upfront spend on AI‑enabled silicon, especially when legacy acceleration cards already meet baseline workloads.

The regulatory environment adds another layer of restraint. Emerging data‑privacy statutes require explicit disclosure of on‑device AI processing, prompting firms to invest in compliance audits and documentation. These ancillary expenses diminish the net financial appeal of upgrading to AI Ethernet Switch Silicon.

MARKET OPPORTUNITIES

Sector‑Specific Customization

Industries such as telecom, manufacturing, and healthcare are beginning to define niche AI workloads that can be hard‑wired into switch ASICs. Tailored instruction sets for common inference patterns,like anomaly detection in sensor streams,promise to unlock revenue streams for silicon vendors willing to co‑develop with vertical partners.

Open‑Source Ecosystem Expansion

The rise of community‑driven AI networking frameworks offers a pathway to mitigate standardization concerns. By contributing reference designs and driver modules to open repositories, manufacturers can stimulate broader adoption while reducing the need for bespoke engineering engagements. This collaborative model could accelerate market penetration beyond the current early‑adopter cohort.

AI Ethernet Switch Silicon Market Trends

Intelligent Traffic Steering Gains Traction

Edge‑oriented workloads and hyperscale data centers are demanding switches that do more than forward packets. By embedding inference engines directly on silicon, vendors are delivering sub‑microsecond decision‑making that eliminates the need for off‑chip processing. This architectural shift trims overall latency, preserves network bandwidth for additional streams, and reduces the software stack complexity that traditionally accompanies separate AI accelerators. In practice, a data‑center operator can run real‑time video analytics on a live feed without sending frames to a distant GPU farm, thereby cutting transport costs and simplifying compliance reporting. The competitive advantage stems from the ability to react to traffic anomalies instantly, a decisive factor for services that rely on deterministic response times.

Other Trends

Power‑Efficient Design

Advanced power‑management blocks now allow AI‑enabled ASICs to scale voltage dynamically based on workload intensity. The result is a roughly 30 % reduction in idle power draw versus legacy switches, delivering tangible OpEx savings for operators managing thousands of nodes. Moreover, adaptive clock‑gating techniques extend device lifespan by mitigating thermal stress, an outcome that resonates with sustainability targets increasingly embedded in corporate procurement policies. Customers are therefore weighting energy profiles alongside raw throughput when selecting next‑generation silicon.

Convergence of Switching and Compute

Recent product announcements, such as Company X’s AI‑enhanced switch unveiled in March 2024, illustrate how silicon vendors are blurring the line between pure networking and compute. By integrating programmable logic alongside ASIC‑based accelerators, these devices support a broader software stack, enabling customers to deploy custom models at the edge without supplemental hardware. This convergence opens new revenue streams for OEMs, as they can bundle AI licensing, model‑optimization services, and managed support with the switch itself. For buyers, the procurement calculus now incorporates algorithm update cycles, model‑training pipelines, and total cost of ownership for the combined networking‑AI solution, reshaping traditional vendor evaluation frameworks.

The cumulative effect of these trends is a market moving toward tightly coupled, energy‑aware platforms that deliver both high‑speed connectivity and on‑device intelligence. Enterprises that adopt such silicon early gain a strategic edge: they can differentiate service offerings, accelerate time‑to‑market for AI‑driven applications, and lock in lower operational expenditures through integrated power savings. As competitive pressure mounts, the vendor ecosystem is likely to see intensified collaboration between chip designers, software vendors, and system integrators, ultimately driving a more cohesive and responsive networking layer for the AI era.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive assessment of AI Ethernet Switch Silicon vendors

Broadcom remains the anchor of the AI‑enabled switching segment, leveraging its extensive ASIC portfolio to embed inference engines directly into fabric chips. The company’s recent launch of a 400‑Gbps AI switch ASIC demonstrates how scale‑driven design and deep‑packet inspection capabilities are converging, allowing hyperscale operators to offload video analytics and security functions to the network layer. Broadcom’s dominance is reinforced by a vertically integrated supply chain, robust IP licensing model, and strategic collaborations with OEMs that accelerate time‑to‑market for custom silicon. This concentration around a handful of large foundries creates a market structure where economies of scale favor incumbents that can sustain high R&D outlays while offering end‑to‑end support services.

Beyond the tier‑one consolidators, a diverse set of niche innovators is reshaping the value chain. Companies such as Marvell and Intel are repurposing data‑center networking IP to embed low‑latency AI blocks, while newer entrants like Pensando and Innovium focus on disaggregated architectures that separate compute from switching fabric. Regional players, notably Huawei and Alibaba Cloud, are targeting edge deployments in Asia‑Pacific, emphasizing power‑efficient silicon that can operate in constrained environments. Start‑ups such as Ceva and Netronome contribute specialized ASIC accelerators for edge video analytics, creating a layered ecosystem where differentiation hinges on algorithmic throughput, power envelope, and programmable flexibility.

List of Key AI Ethernet Switch Silicon Companies Profiled

- Broadcom Inc.

- Intel Corporation

- Marvell Technology Group Ltd.

- Xilinx (AMD)

- Mellanox Technologies (NVIDIA)

- Cisco Systems

- Huawei Technologies Co., Ltd.

- Alibaba Cloud

- Samsung Electronics

- MediaTek Inc.

- Qualcomm Technologies

- Netronome Systems

- Pensando Systems

- Ceva Inc.

- Innovium

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASIC‑based silicon

|

| By Application |

|

Edge video analytics

|

| By End User |

|

Hyperscale data centers

|

| By Architecture |

|

Integrated AI engine

|

| By Deployment Scenario |

|

Retrofit upgrades

|

Regional Analysis: AI Ethernet Switch Silicon Market

Enterprises across the United States are trialing AI‑enhanced Ethernet switches to reduce packet‑processing latency in high‑frequency trading and autonomous‑vehicle simulations, prompting silicon vendors to embed inferencing kernels directly on the switch ASIC.

Proximity to fabs in the Southwest and robust logistics networks enable rapid prototyping cycles, allowing manufacturers to iterate silicon designs on a quarterly cadence rather than the bi‑annual rhythm observed elsewhere.

A mix of hyperscale cloud operators, defense contractors, and financial‑services firms creates a diversified demand profile that mitigates exposure to any single industry’s budget fluctuations.

Favorable export‑control policies and active standards bodies in the U.S. streamline certification pathways for AI‑ready networking components, reducing time‑to‑market for new silicon generations.

Europe

European players approach AI Ethernet Switch Silicon Market from a sustainability angle, integrating power‑efficient silicon blocks into data‑center fabrics to meet stringent energy‑use directives. Collaboration among telecom operators and semiconductor consortia yields region‑specific IP cores that prioritize deterministic latency for mission‑critical rail and manufacturing automation. While capital spending lags behind North America, the regulatory push for greener infrastructure creates a niche where energy‑optimized switches can command premium pricing.

Asia‑Pacific

In the Asia‑Pacific arena, rapid expansion of cloud and edge deployments fuels interest in AI‑enabled switches, yet the market is fragmented across diverse manufacturing bases. Nations such as Japan and South Korea lean on mature foundry capabilities to produce high‑density ASICs, while emerging economies capitalize on cost‑effective design services. The resulting mix accelerates innovation cycles but also introduces variance in product quality, prompting multinational OEMs to adopt a dual‑sourcing strategy to balance cost and reliability.

South America

South American adoption of AI Ethernet Switch silicon remains centered on telecom modernization projects, where operators retrofit legacy transport networks with AI‑aware switching gear to improve traffic engineering. Limited domestic fab capacity forces firms to import designs, yet local system integrators add value through customized firmware that aligns with regional spectrum allocations and latency requirements for financial exchanges in Brazil.

Middle East & Africa

The Middle East & Africa region sees modest but growing interest in AI‑driven networking as sovereign wealth funds allocate resources toward smart‑city initiatives. Projects in the United Arab Emirates and Saudi Arabia prioritize secure, low‑latency connectivity for AI‑powered surveillance and autonomous logistics, encouraging global silicon providers to establish regional design hubs that can adapt core architectures to local security standards.

Report Scope

This market research report provides a comprehensive analysis of the AI Ethernet Switch Silicon Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Ethernet Switch Silicon Market?

-> AI Ethernet Switch Silicon Market is forecasted to rise from USD 0.84 billion in 2026 to USD 1.46 billion by 2034.

Which key companies operate in AI Ethernet Switch Silicon Market?

-> Key players include Company X, which announced a next‑generation AI‑enabled switch ASIC in March 2024.

What are the key growth drivers?

-> Key growth drivers include increasing demand from hyperscale data centers and edge deployments for intelligent traffic steering and on‑chip AI inference.

Which region dominates the market?

-> Regional dominance is not explicitly disclosed in the reference; however, adoption is strong in regions hosting large hyperscale data‑center footprints.

What are the emerging trends?

-> Emerging trends include integration of AI inference engines within switch silicon and development of smart networking platforms for low‑latency edge AI workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...