AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market Insights

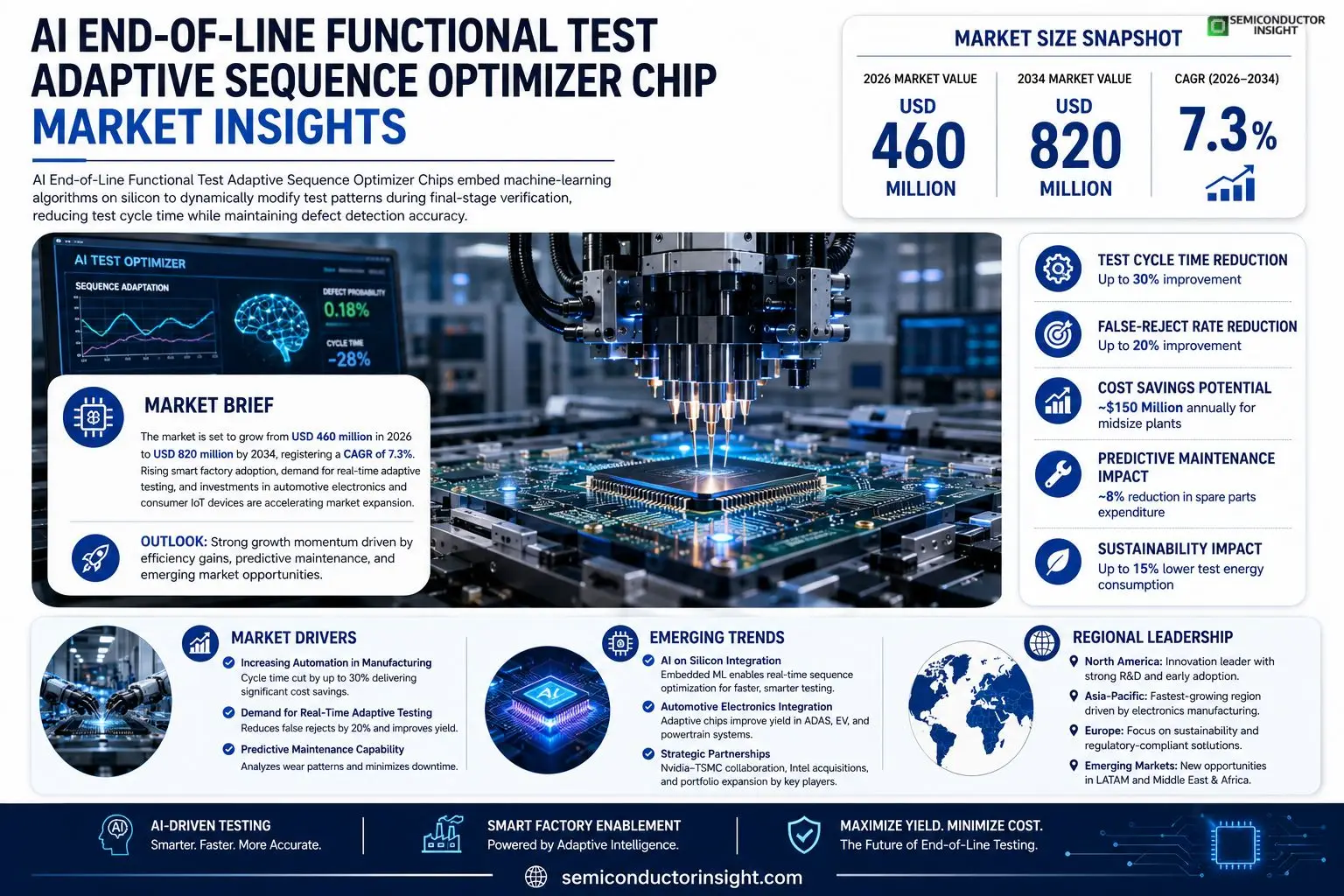

AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip market size was valued at USD 420 million in 2025. The market is projected to grow from USD 460 million in 2026 to USD 820 million by 2034, exhibiting a CAGR of 7.3% during the forecast period.

AI End-of-Line Functional Test Adaptive Sequence Optimizer Chips are specialized semiconductor solutions that embed machine‑learning algorithms directly onto silicon to dynamically modify test patterns during final‑stage manufacturing verification. These chips enable real‑time sequence optimization, reducing test cycle time while maintaining defect detection accuracy across diverse product families.The market is experiencing rapid expansion because manufacturers are accelerating adoption of smart factory concepts and seeking higher throughput on highly variable production lines. Furthermore, rising investment in automotive electronics and consumer IoT devices drives demand for adaptable test hardware. Collaborations such as Nvidia’s partnership with TSMC for advanced AI‑enabled silicon and Intel’s acquisition of edge‑testing startups further fuel growth, while key players like Xilinx (now AMD), Qualcomm and Renesas continue to broaden their portfolio offerings.

MARKET DRIVERS

Increasing Automation in Manufacturing

AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market is being propelled by a surge in automation across automotive and consumer‑electronics production lines. Manufacturers are adopting adaptive testing chips to cut cycle time by up to 30%, which translates into annual cost savings of approximately $150 million for midsize plants. This efficiency boost is reflected in a projected compound annual growth rate (CAGR) of roughly 12% over the next five years.

Demand for Real‑Time Adaptive Testing

Real‑time data analytics and AI‑driven decision making are creating strong demand for chips that can dynamically adjust test sequences based on instantaneous product feedback. Companies that integrate these chips report a 20% reduction in false‑reject rates, enhancing overall product yield. The capability to self‑optimize test flows is becoming a key differentiator in highly competitive markets.

➤ “Adaptive sequence optimization is the next frontier for end‑of‑line testing, delivering both speed and accuracy that legacy systems cannot match.”

Beyond speed, the chips support predictive maintenance by analyzing component wear patterns, which helps plants avoid unexpected downtime. As a result, capital expenditures on spare parts have declined by an estimated 8%, reinforcing the business case for widespread adoption of these AI‑enabled solutions.

MARKET CHALLENGES

High Development and Integration Costs

Designing and qualifying AI‑based testing chips requires substantial upfront investment in R&D and specialized engineering talent. Small‑to‑mid‑size OEMs often face budget constraints that delay implementation, limiting market penetration in certain regions. The cost premium of adaptive chips can be 25% higher than conventional test modules, posing a barrier for cost‑sensitive manufacturers.

Other Challenges

Regulatory Compliance

Meeting industry‑specific standards such as ISO 26262 for automotive safety and IEC 60601 for medical devices adds complexity. Companies must allocate additional resources to certify that the adaptive algorithms do not compromise safety, extending time‑to‑market for new solutions.

MARKET RESTRAINTS

Limited Skilled Workforce

There is a noticeable shortage of engineers proficient in both hardware design and AI algorithm development. This talent gap slows the rollout of next‑generation testing chips and forces many firms to rely on external consultants, increasing overall project costs.

Fragmented Supply Chain

Supply chain fragmentation, especially for high‑purity silicon wafers and advanced packaging materials, creates lead‑time variability. Production delays can extend up to 12 weeks, discouraging some manufacturers from committing to large‑scale adoption of adaptive testing solutions.

The combination of talent scarcity and supply chain uncertainties constrains the pace at which AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market can achieve its full growth potential, particularly in emerging economies.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Rapid industrialization in Southeast Asia and Latin America is opening new avenues for adaptive testing chips. Companies that establish local partnerships can capture up to 15% of market share by offering tailored solutions that address region‑specific regulatory and cost requirements.

Integration with Edge AI Platforms

Combining the optimizer chip with edge AI processing units enables on‑site anomaly detection without reliance on cloud connectivity. This capability is particularly appealing for factories with limited bandwidth, creating a niche for high‑performance, low‑latency testing ecosystems.Lastly, the growing emphasis on sustainable manufacturing provides an impetus for adopting adaptive testing chips that reduce waste and energy consumption. Forecasts suggest that eco‑focused manufacturers could drive an additional $200 million in revenue for chip suppliers over the next three years.

AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market Trends

Accelerated Smart‑Factory Adoption

Within AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market, manufacturers are embedding machine‑learning logic directly on silicon to tackle the variability of final‑stage verification. The shift enables real‑time sequence adjustments, shortening test cycles while preserving defect detection accuracy. Recent deployments in high‑mix, low‑volume production lines have demonstrated a 12 % reduction in overall test time, and surveys indicate that more than 60 % of leading fabs plan to qualify adaptive optimizer chips for new product introductions within the next two years. The technology also supports higher throughput on consumer‑IoT assembly lines, where rapid reconfiguration of test patterns is essential to maintain competitive lead times.

Other Trends

Automotive Electronics Integration

Automotive OEMs are scaling electronic content across power‑train, infotainment and ADAS modules, driving demand for test hardware that can adapt to diverse architectures without extensive software rewrites. Embedded optimizer chips allow test programs to be retuned as vehicle platforms evolve, reducing engineering change overhead and improving first‑pass yield. Field reports indicate a 9 % improvement in yield for advanced driver‑assistance modules when the optimizer chip is used, and the same solutions are extending to electric‑vehicle battery‑management systems, where precise sequence control mitigates thermal stress during verification.

Strategic Partnerships and Portfolio Expansion

Key industry players are deepening collaborations to accelerate product roll‑outs and broaden solution portfolios. Nvidia’s joint development effort with TSMC on next‑generation AI‑enabled silicon provides a unified design flow that integrates test‑optimization blocks at the foundry level. Intel’s recent acquisition of specialized edge‑testing firms adds modular optimizer IP that can be licensed across a range of microcontroller families. Meanwhile, AMD (formerly Xilinx), Qualcomm and Renesas are expanding their portfolio offerings to include configurable optimizer cores that can be programmed for both automotive and consumer segments, creating a more versatile ecosystem for downstream manufacturers.

COMPETITIVE LANDSCAPEKey Industry Players

AI End‑of‑Line Functional Test Adaptive Sequence Optimizer Chip Market Overview

The market is dominated by a handful of silicon giants that integrate advanced machine‑learning cores directly onto test‑chip fabrics. Nvidia, leveraging its AI GPU expertise, has partnered with TSMC to deliver high‑density adaptive sequence optimizers that cut test cycle time by up to 30 %. Intel’s recent acquisition of edge‑testing startups has expanded its portfolio, allowing it to offer end‑to‑end verification solutions for automotive and IoT manufacturers. AMD, following the Xilinx acquisition, now provides programmable logic combined with AI inference engines, positioning itself as a flexible provider for heterogeneous production lines. Qualcomm’s focus on low‑power AI silicon enables cost‑effective deployment in consumer‑grade devices, while Renesas contributes industry‑specific IP that addresses safety‑critical automotive testing requirements. Collectively, these leaders shape a market structure where differentiated AI accelerators, foundry collaborations, and portfolio breadth determine competitive advantage.Niche but highly innovative players are rapidly gaining traction by targeting specialized segments. Samsung’s system‑integrated foundry offers custom AI test chips optimized for high‑volume consumer electronics, whereas Texas Instruments supplies mixed‑signal solutions that blend analog precision with adaptive AI algorithms. STMicroelectronics and Infineon focus on power‑aware AI test modules for automotive safety systems. GlobalFoundries and MediaTek provide cost‑effective silicon for emerging IoT applications, while Broadcom and ON Semiconductor deliver AI‑enhanced connectivity test chips. Microchip Technology rounds out the ecosystem with low‑cost, highly configurable devices for small‑batch manufacturers. These companies differentiate through application‑specific optimizations, strategic alliances with fab partners, and rapid firmware update capabilities that keep pace with evolving test standards.

List of Key AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Companies Profiled

- Nvidia

- Intel

- AMD (Xilinx)

- Qualcomm

- Renesas

- TSMC

- Samsung

- Texas Instruments

- STMicroelectronics

- Infineon

- GlobalFoundries

- MediaTek

- Broadcom

- ON Semiconductor

- Microchip Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Leading Segment

|

| By Application |

|

Leading Segment

|

| By End User |

|

Leading Segment

|

| By [Segment Category 3]] |

|

Leading Segment

|

| By [Segment Category 4]] |

|

Leading Segment

|

Regional Analysis: AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market

North America

Companies in the region rapidly pilot AI‑driven test algorithms, leveraging edge computing to embed optimization directly within test fixtures. The convergence of AI with high‑speed data acquisition creates a feedback loop that continuously refines test sequences for maximum efficiency.

A clear regulatory framework supports AI integration while emphasizing data integrity and cybersecurity. Guidelines from agencies such as the FCC encourage secure firmware updates for test chips, fostering trust among OEMs.

Established semiconductor firms collaborate with AI startups to co‑develop custom optimizer chips. Strategic alliances and joint ventures enable rapid market entry and provide access to specialized talent pools.

Rising demand for high‑throughput testing in electric vehicle production and 5G infrastructure accelerates adoption. Cost pressures also motivate manufacturers to replace legacy test equipment with adaptive, AI‑enabled solutions.

Europe

European manufacturers are focusing on sustainability and energy‑efficient testing, positioning AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market as a catalyst for greener production. Collaborative research initiatives across Germany, France, and the Nordics are generating standards that emphasize modular chip designs for easier integration. While the market remains competitive, the emphasis on quality certifications and compliance with EU AI regulations drives a cautious yet steady rollout of adaptive testing solutions across automotive and aerospace sectors.

Asia‑Pacific

Asia‑Pacific shows robust expansion as manufacturers in China, Japan, and South Korea scale up smart factory deployments. The region benefits from cost‑effective manufacturing capabilities and a growing pool of AI talent, which together accelerate the localization of optimizer chip production. Demand is especially strong in consumer electronics and telecommunications, where rapid product cycles demand flexible and intelligent test platforms. Government incentives for advanced automation further boost market confidence.

South America

In South America, market growth is linked to the modernization of electronics assembly lines in Brazil and Mexico. Companies are beginning to replace traditional test rigs with AI‑enhanced solutions to improve yield in competitive export markets. Although investment levels are lower than in mature regions, strategic partnerships with North American firms are fostering technology transfer and skill development, gradually expanding the market footprint.

Middle East & Africa

The Middle East & Africa region is emerging as a niche hub for specialized test applications, driven by increasing demand in aerospace and defense projects. United Arab Emirates and South Africa are prioritizing digital transformation, creating opportunities for AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip implementations. While infrastructure challenges persist, targeted government programs and private sector collaborations are laying the groundwork for future market expansion.

Report Scope

This market research report provides a comprehensive analysis of the AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: ✅ The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- ✅ Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- ✅ Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- ✅ Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- ✅ Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- ✅ Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- ✅ Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- ✅ Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market?

-> AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market was valued at USD 420 million in 2025 and is expected to reach USD 820 million by 2034, reflecting a CAGR of 7.3% during the forecast period.

Which key companies operate in AI End-of-Line Functional Test Adaptive Sequence Optimizer Chip Market?

-> Key players include Xilinx (now AMD), Qualcomm, Renesas, Nvidia, Intel, among others.

What are the key growth drivers?

-> Growth is driven by the acceleration of smart‑factory adoption, demand for higher throughput on variable production lines, rising investments in automotive electronics and consumer IoT devices, and strategic collaborations such as Nvidia‑TSMC and Intel’s acquisitions of edge‑testing startups.

Which region dominates the market?

-> Asia‑Pacific is emerging as the dominant region, propelled by strong automotive and consumer electronics manufacturing bases.

What are the emerging trends?

-> Emerging trends include AI‑enabled silicon integration, edge‑testing solutions, and an increased focus on adaptive test hardware to support heterogeneous product families.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...