AI Edge Analog Front-End Market Insights

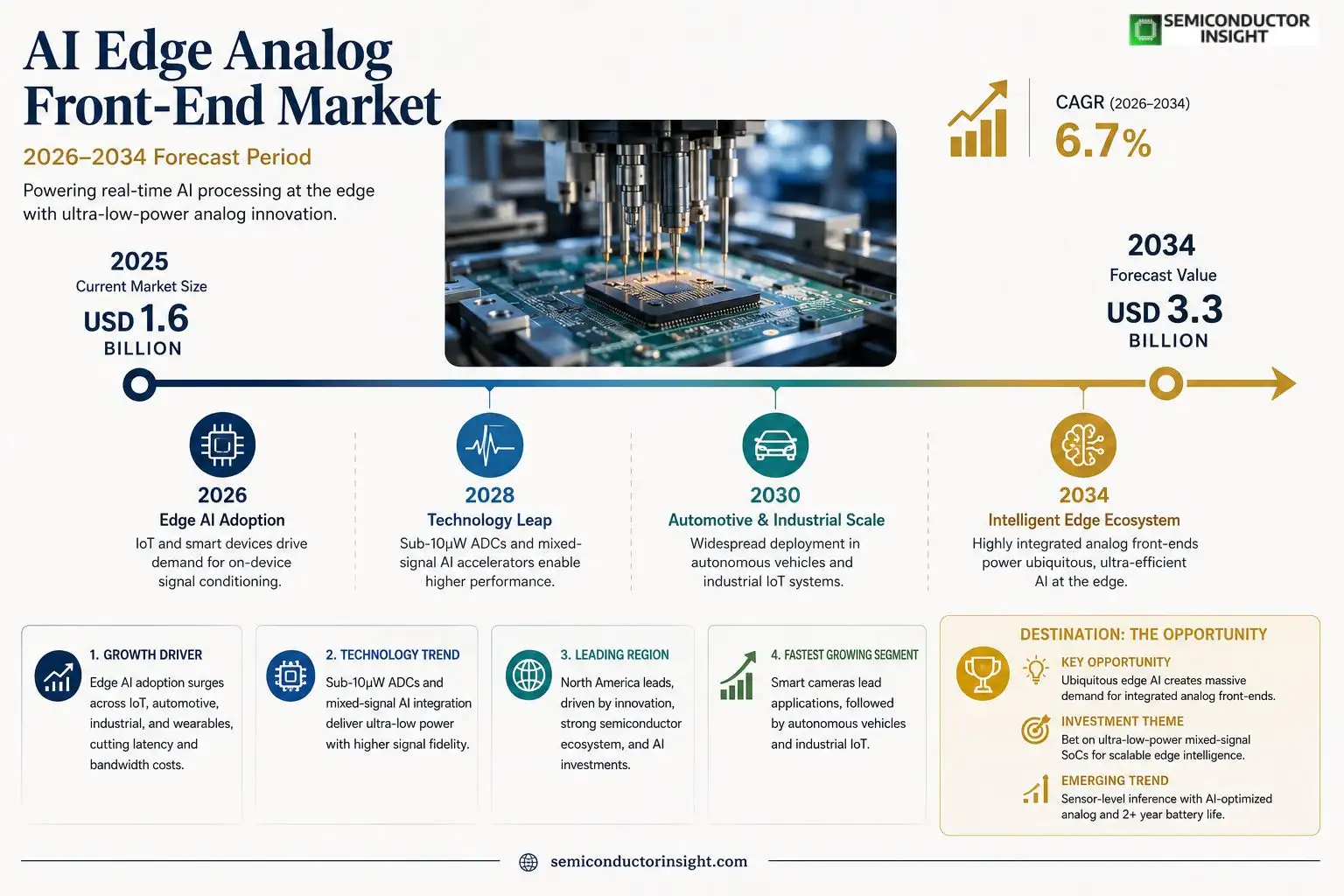

AI Edge Analog Front-End market size was valued at USD 1.6 billion in 2025. The market is projected to grow from USD 1.6 billion in 2025 to USD 3.3 billion by 2034, exhibiting a CAGR of 6.7 % during the forecast period.

AI Edge Analog Front‑End circuits are specialized semiconductor components that condition, amplify, and convert analog sensor signals for on‑device artificial intelligence processing at the edge. These front‑ends integrate low‑power amplifiers, filters, analog‑to‑digital converters (ADCs), and signal conditioning blocks optimized for neural network inference directly on sensors or microcontrollers.The market is experiencing rapid growth because enterprises are deploying AI workloads closer to data sources to reduce latency and bandwidth costs. Furthermore, rising demand for smart cameras, autonomous vehicles, industrial IoT, and wearable health devices drives adoption of highly integrated analog front‑ends. In addition, recent advances such as sub‑10 µW ADCs and mixed‑signal AI accelerators released by leading silicon vendors in early 2024 have accelerated deployment. Key playersincluding Texas Instruments, Analog Devices, Infineon Technologies, and STMicroelectronicsare expanding their portfolios through strategic partnerships and aggressive R&D investments, further fueling market expansion.

MARKET DRIVERS

Rising Adoption of Edge AI in IoT Devices

The rapid growth of Internet‑of‑Things (IoT) ecosystems is fueling demand for localized processing, which in turn drives AI Edge Analog Front-End Market. Manufacturers are integrating low‑power analog front‑ends to capture sensor data with high fidelity before it is processed by edge AI chips, resulting in reduced latency and bandwidth savings.

Advancements in Low‑Power Semiconductor Technologies

Recent breakthroughs in CMOS scaling and silicon‑on‑insulator (SOI) processes enable analog front‑end circuits that consume less than a milliwatt while maintaining high signal‑to‑noise ratios. This technological edge makes edge AI solutions economically viable for battery‑operated devices, accelerating market expansion.

➤ “Analog front‑end integration reduces overall system power by up to 30 % compared with discrete sensor‑to‑digital pipelines.”

Enterprise adoption of predictive maintenance and real‑time analytics further validates the business case for on‑device AI, ensuring sustained growth for AI Edge Analog Front-End Market over the next five years.

MARKET CHALLENGES

Complexity of Co‑Design with AI Processors

Designing analog front‑ends that seamlessly interface with diverse AI accelerators requires multidisciplinary expertise. The lack of standardized design kits often leads to longer development cycles and higher engineering costs.

Other Challenges

Thermal Management Constraints

Edge AI workloads generate localized heat, and compact analog front‑ends must operate reliably under elevated temperatures, limiting material choices and packaging options.

MARKET RESTRAINTS

High Initial Capital Expenditure

Early‑stage projects require significant investment in custom silicon and verification tools. Smaller OEMs often lack the financial resources to undertake such projects, restraining broader market participation.

MARKET OPPORTUNITIES

Emergence of 5G‑Enabled Edge Nodes

5G connectivity provides high‑bandwidth, low‑latency links for distributed edge nodes, creating a compelling use case for sophisticated analog front‑ends that preprocess data before transmission. This synergy opens new revenue streams for vendors in AI Edge Analog Front-End Market.

AI Edge Analog Front-End Market Trends

Rapid Adoption in Edge AI Devices

AI Edge Analog Front-End Market is seeing accelerated uptake as enterprises move inference workloads closer to sensors and cameras. Deployments in smart surveillance, autonomous navigation, and industrial IoT reduce latency to sub‑millisecond levels while trimming backhaul bandwidth costs. Recent field data indicate that edge‑centric designs now account for over 45 % of new AI semiconductor projects, driven by the need for real‑time decision making without reliance on cloud connectivity. This shift underpins a steady rise in demand for integrated front‑end blocks that can condition analog signals with ultra‑low power budgets.

Other Trends

Advances in Low‑Power ADCs

Sub‑10 µW analog‑to‑digital converters introduced in early 2024 have become a cornerstone of the market. These converters, paired with mixed‑signal AI accelerators, enable sensor‑level neural inference while maintaining battery life that exceeds 2 years in wearable health monitors. The integration of adaptive filtering and dynamic range optimization further improves signal fidelity, supporting higher‑resolution image processing in smart cameras without additional power draw.

Strategic Portfolio Expansion by Leading Vendors

Key players such as Texas Instruments, Analog Devices, Infineon Technologies, and STMicroelectronics are broadening their analog front‑end portfolios through targeted acquisitions and joint development programs. Investment in silicon‑photonic interfaces and AI‑optimized mixed‑signal IP blocks has accelerated time‑to‑market for customized solutions. Collaborative projects with automotive OEMs and cloud‑edge platform providers are expected to deepen ecosystem integration, reinforcing the market’s growth trajectory through 2034.

COMPETITIVE LANDSCAPEKey Industry Players

AI Edge Analog Front‑End Market Competitive Overview

AI Edge Analog Front‑End market is dominated by large semiconductor firms that integrate low‑power amplifiers, filters, and sub‑10 µW ADCs directly with AI inference engines. Texas Instruments and Analog Devices lead the space, leveraging extensive mixed‑signal portfolios and deep R&D pipelines to deliver highly integrated solutions for smart cameras, autonomous vehicles, and industrial IoT. Their aggressive roadmap, combined with strategic partnerships with AI accelerator vendors, creates a barrier to entry for smaller players. Meanwhile, Infineon Technologies and STMicroelectronics expand their offerings through acquisitions and co‑development programs, targeting automotive and wearable segments where power efficiency and miniaturization are critical.Beyond the tier‑one giants, a cohort of niche specialists adds depth to the ecosystem. NXP Semiconductors and Renesas Electronics focus on automotive‑grade reliability, providing rugged analog front‑ends for sensor fusion. ON Semiconductor and Microchip Technology address cost‑sensitive consumer applications, while Silicon Labs and Skyworks Solutions emphasize ultra‑low‑power designs for battery‑operated wearables. Emerging players such as ams AG, ROHM Semiconductor, and Qorvo bring advanced sensor‑centric analog technologies, strengthening the market’s overall innovation velocity. This layered competitive structure ensures continuous advancement in performance, power consumption, and integration density.

List of Key AI Edge Analog Front‑End Companies Profiled

- Texas Instruments

- Analog Devices

- Infineon Technologies

- STMicroelectronics

- NXP Semiconductors

- Renesas Electronics

- ON Semiconductor

- Microchip Technology

- Silicon Labs

- Skyworks Solutions

- ams AG

- ROHM Semiconductor

- Qorvo

- Broadcom

- Maxim Integrated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Voltage‑Mode Front‑Ends dominate due to their inherent linearity and ease of integration with existing digital signal paths.

|

| By Application |

|

Smart Cameras are the leading application segment because they combine high‑resolution imaging with on‑device inference, demanding compact and power‑efficient front‑ends.

|

| By End User |

|

Automotive OEMs emerge as the primary end‑user group, leveraging edge AI front‑ends to enable driver‑monitoring, sensor fusion, and predictive maintenance.

|

| By Power Efficiency |

|

Ultra‑Low Power front‑ends are gaining prominence as designers push battery life and thermal budgets on edge devices.

|

| By Integration Architecture |

|

Monolithic Mixed‑Signal SoCs are the leading architecture as manufacturers integrate analog conditioning directly with AI compute blocks.

|

Regional Analysis: North America

United States

The industrial sector is witnessing a surge in the adoption of AI Edge analog front-end technology for real-time monitoring, predictive maintenance, and process optimization. The need for robust and reliable analog-to-digital conversion in harsh industrial environments is key to the market’s expansion.

The automotive industry, particularly with the rise of autonomous driving, is a significant driver of demand. AI Edge analog front-end solutions are crucial for sensor fusion, object detection, and driver assistance systems, demanding high accuracy and low power consumption.

The healthcare sector is leveraging AI Edge analog front-end technology for real-time patient monitoring, diagnostic imaging, and wearable medical devices. The demand for miniaturized and power-efficient analog front-end components is particularly strong in this segment.

The proliferation of IoT devices in smart cities necessitates AI Edge analog front-end solutions for data acquisition and processing at the edge, supporting applications like intelligent traffic management and environmental monitoring.

Europe

Europe represents a significant and steadily growing market for AI Edge Analog Front-End technology. Driven by strong government initiatives promoting digital transformation and technological advancement, particularly within the manufacturing and automotive sectors, the region is witnessing increasing adoption. The focus on data privacy regulations, such as GDPR, influences the development of secure and compliant AI Edge solutions. Key markets within Europe include Germany, the UK, France, and the Netherlands, each with unique industry strengths and investment priorities. Businesses in Europe are increasingly collaborating with research institutions and startups to foster innovation in this space. The emphasis on sustainable technologies also creates opportunities for energy-efficient AI Edge analog front-end solutions.

Asia-Pacific

Asia-Pacific is poised for substantial growth in AI Edge Analog Front-End Market, fueled by rapid industrialization, increasing disposable incomes, and a burgeoning electronics manufacturing sector. Countries like China, Japan, South Korea, and India are key contributors to this growth. The demand for AI-powered solutions in areas such as manufacturing, automotive, and telecommunications is driving the need for advanced analog front-end technology. Government support for domestic semiconductor industries and ambitious digitalization plans are further accelerating market expansion. The region’s strong manufacturing base provides a cost-competitive environment for AI Edge analog front-end component production.

South America

South America presents a promising, albeit relatively nascent, market for AI Edge Analog Front-End technology. The growing adoption of IoT devices in agriculture, mining, and logistics is creating initial demand. Countries like Brazil and Argentina are expected to be key growth drivers, supported by increasing investments in infrastructure and technological development. However, challenges such as economic volatility and limited access to advanced technologies may constrain market growth in the near term. The focus on improving operational efficiency and resource management is driving interest in AI-powered edge solutions.

Middle East & Africa

The Middle East & Africa region is an emerging market with significant potential for AI Edge Analog Front-End technology adoption. The increasing focus on smart city initiatives, renewable energy projects, and industrial development is driving demand. Countries like Saudi Arabia, the UAE, and South Africa are witnessing growing investments in digitalization and automation. The region’s strategic location and abundant natural resources create opportunities for growth in various sectors. However, factors such as limited technological infrastructure and regulatory complexities may pose challenges to market development.

Report Scope

This market research report provides a comprehensive analysis of the AI Edge Analog Front-End Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Edge Analog Front-End Market?

-> AI Edge Analog Front-End Market was valued at USD 1.6 billion in 2025 and is expected to reach USD 3.3 billion by 2034.

Which key companies operate in AI Edge Analog Front-End Market?

-> Key players include Texas Instruments, Analog Devices, Infineon Technologies, and STMicroelectronics.

What are the key growth drivers?

-> Key growth drivers include deployment of AI workloads at the edge to reduce latency and bandwidth costs, rising demand for smart cameras, autonomous vehicles, industrial IoT, and wearable health devices, and recent advances such as sub‑10 µW ADCs and mixed‑signal AI accelerators.

Which region dominates the market?

-> The reference does not specify a single dominant region for AI Edge Analog Front-End Market.

What are the emerging trends?

-> Emerging trends include ultra‑low‑power ADCs, mixed‑signal AI accelerator integration, and highly integrated analog front‑ends optimized for on‑device neural network inference.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...